Global Ai Hardware Market

Market Size in USD Billion

USD

112.07 Billion

USD

614.39 Billion

2025

2033

USD

112.07 Billion

USD

614.39 Billion

2025

2033

| 2026 - 2033 | |

| USD 112.07 Billion | |

| USD 614.39 Billion | |

| % | |

|

AI Hardware Market Overview

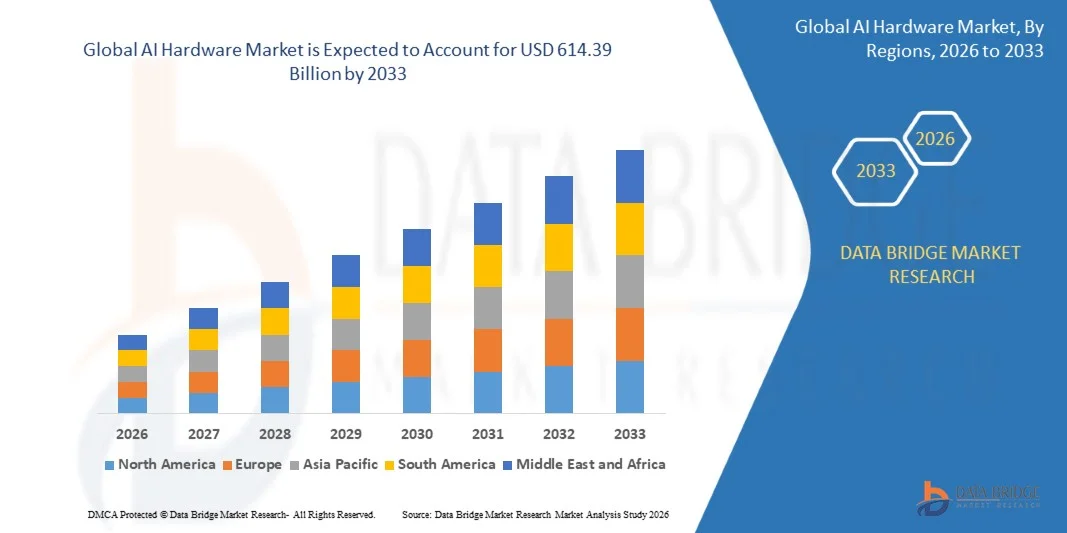

The AI Hardware Market was valued at USD 112.07 billion in 2025 and is projected to reach USD 614.39 billion by 2033, growing at a CAGR of 23.70% from 2026 to 2033. The market is experiencing rapid expansion driven by increasing adoption of artificial intelligence across data centers, edge computing systems, automotive applications, and enterprise digital transformation initiatives. Rising demand for high-performance computing infrastructure, specialized AI processors, and energy-efficient hardware architectures is further accelerating market growth.

The growing deployment of AI workloads such as machine learning, deep learning, natural language processing, and computer vision is significantly increasing the need for advanced GPUs, ASICs, FPGAs, and AI-optimized servers. In addition, the rapid expansion of cloud-based AI services, autonomous systems, and smart devices is compelling enterprises and technology providers to invest heavily in scalable and high-speed computing hardware, supporting continuous innovation and global market expansion.

Key Market Trends & Insights

- North America dominated the AI hardware market with the largest revenue share of 38.9% in 2025, supported by strong presence of leading semiconductor companies, hyperscale cloud providers, advanced R&D capabilities, and early adoption of AI technologies across industries such as IT & telecom, automotive, and BFSI.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 25.8% from 2026 to 2033. Growth is driven by rapid digital transformation, expanding semiconductor manufacturing base, increasing AI adoption in consumer electronics and industrial automation, and strong government initiatives supporting AI infrastructure development.

- The AI Processors segment held the largest market revenue share of approximately 52.4% in 2025 driven by strong demand for high-performance computing in training and inference of AI models across data centers, enterprise applications, and cloud platforms. Increasing deployment of GPUs, TPUs, and AI-specific ASICs is further strengthening segment dominance.

- The Network Devices segment is projected to register the fastest growth at a CAGR of 24.1% from 2026 to 2033, driven by rising demand for high-speed interconnects, low-latency communication, and scalable data center infrastructure supporting distributed AI workloads and real-time processing applications. Expanding AI data center clusters require advanced networking solutions such as high-bandwidth switches and optical interconnects. Increasing adoption of distributed AI training models is further enhancing demand for ultra-fast data transmission. In addition, growth in edge computing ecosystems is accelerating deployment of intelligent network hardware.

- The Processors segment held the largest market revenue share of approximately 48.7% in 2025 driven by extensive usage of GPUs and ASICs in AI model training, deep learning workloads, and generative AI applications across hyperscale data centers and enterprise computing environments. Strong demand for AI accelerators is driven by exponential growth in computational requirements for training foundation models. Enterprises are increasingly shifting from traditional CPU-based systems to GPU-dominant architectures. Continuous improvements in chip architecture are enabling faster processing and reduced energy consumption.

- The Edge Devices segment is projected to register the fastest growth at a CAGR of 26.3% from 2026 to 2033, driven by rapid adoption of edge AI in autonomous vehicles, smart devices, industrial automation, and IoT ecosystems requiring real-time on-device processing and reduced latency. Growing deployment of smart sensors and connected devices is increasing demand for localized computing power. Edge AI reduces dependency on cloud infrastructure and improves real-time decision-making efficiency. In addition, rising use of AI in industrial robotics and smart manufacturing is further accelerating segment expansion.

- The Deep Learning segment held the largest market revenue share of approximately 44.9% in 2025 driven by growing use in large language models, generative AI systems, and advanced neural network training across enterprise and cloud platforms. Increasing complexity of AI models is significantly boosting demand for deep learning optimized hardware such as GPUs and tensor processing units. Enterprises are investing heavily in AI infrastructure to support model training at scale. Rising adoption in predictive analytics and automation systems is further strengthening segment growth.

- The Natural Language Processing segment is projected to register the fastest growth at a CAGR of 25.7% from 2026 to 2033, driven by increasing adoption of conversational AI, chatbots, virtual assistants, and enterprise automation tools across industries such as BFSI, healthcare, and retail. Rapid expansion of AI-powered customer engagement platforms is driving hardware requirements for real-time language processing. Enterprises are deploying NLP models for sentiment analysis, translation, and automation workflows. In addition, integration of NLP in enterprise software is accelerating demand for optimized AI computing infrastructure.

- The Cloud-Based AI Hardware segment held the largest market revenue share of approximately 61.5% in 2025 driven by widespread adoption of hyperscale cloud platforms, scalable computing infrastructure, and AI-as-a-service offerings across enterprises. Cloud platforms enable flexible scaling of AI workloads without heavy upfront infrastructure investment. Major providers are expanding global data center networks to support AI computing demand. Increasing use of hybrid cloud architectures is also contributing to segment growth.

- The On-Premise AI Hardware segment is projected to register the fastest growth at a CAGR of 21.9% from 2026 to 2033, driven by increasing demand for data security, regulatory compliance, and low-latency AI processing in sensitive industries such as defense, healthcare, and BFSI. Organizations handling confidential data prefer on-premise deployment for enhanced control and privacy. Rising cybersecurity concerns are further encouraging localized AI infrastructure investments. In addition, latency-sensitive applications in critical industries are boosting adoption.

- The Data Center & Cloud Computing segment held the largest market revenue share of approximately 46.8% in 2025 driven by rapid expansion of AI training clusters, hyperscale infrastructure, and enterprise digital transformation initiatives. Growing demand for generative AI model training is significantly increasing data center hardware investments. Cloud service providers are continuously upgrading infrastructure to support AI workloads. Expansion of enterprise digital ecosystems is further accelerating segment dominance.

- The Automotive segment is projected to register the fastest growth at a CAGR of 27.2% from 2026 to 2033, driven by rising adoption of autonomous driving systems, advanced driver assistance systems, and AI-based in-vehicle computing platforms. Increasing penetration of electric vehicles is further boosting demand for AI chips in mobility systems. Automotive OEMs are investing in real-time edge AI processing for safety and navigation. In addition, advancements in autonomous vehicle testing are accelerating hardware adoption.

- The IT & Telecom segment held the largest market revenue share of approximately 39.6% in 2025 driven by strong demand for cloud computing infrastructure, data center expansion, and AI-enabled network optimization. Telecom operators are increasingly deploying AI for network traffic management and predictive maintenance. Rising data consumption is pushing investment in high-performance computing systems. In addition, AI-driven automation is improving operational efficiency across IT services.

- The Automotive segment is projected to register the fastest growth at a CAGR of 26.8% from 2026 to 2033, driven by increasing integration of AI chips in autonomous vehicles, EV platforms, and smart mobility systems enabling real-time decision-making and enhanced vehicle intelligence. Growing focus on vehicle automation and safety systems is accelerating adoption of AI hardware. OEMs are integrating advanced computing modules for ADAS and infotainment systems. Expansion of connected vehicle ecosystems is further strengthening segment growth.

Market Size & Forecast

- Global Market Value (2025): USD 112.07 Billion

- Expected Market Value (2033): USD 614.39 Billion

- Forecast CAGR (2026–2033): 23.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and AI Hardware Market Segmentation

|

Attributes |

AI Hardware Key Market Insights |

|

Segments Covered |

• By Component: AI Processors, Memory Devices, Storage Devices, Network Devices, and Others • By HardwareType: Processors (CPU, GPU, ASIC, FPGA), Servers, Storage Systems, Networking Hardware, and Edge Devices • By Technology: Machine Learning, Deep Learning, Natural Language Processing, Computer Vision, and Others • By Deployment Mode: Cloud-Based AI Hardware, and On-Premise AI Hardware • By Application: Data Center & Cloud Computing, Edge Computing, Automotive, Healthcare, Consumer Electronics, Robotics, BFSI, and Others • By End-User: IT & Telecom, Healthcare, Automotive, Retail, BFSI, Government & Defense, Manufacturing, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• NVIDIA (U.S.) |

|

Market Opportunities |

• Expansion In Edge AI Infrastructure • Rising Demand For AI Accelerators |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

AI Hardware Market Trends

Trend: Growth In AI Accelerated Computing And Energy Efficient Hardware Architectures

Increasing demand for high-performance, energy-efficient, and scalable computing infrastructure across data centers, edge computing, automotive systems, and enterprise AI workloads. Traditional CPU-based architectures are increasingly unable to handle large-scale AI processing demands, encouraging industries to adopt specialized AI accelerators such as GPUs, TPUs, ASICs, and FPGAs with optimized parallel processing capabilities.

In modern data centers, companies are integrating AI optimized GPU clusters, For instance NVIDIA H100 and AMD Instinct MI300 series, to support large language model training and inference workloads, significantly improving processing speed and reducing training time for complex AI models by over 30–50% compared to previous-generation hardware. In automotive systems, AI chips are being used in advanced driver assistance systems and autonomous driving platforms to enable real-time decision-making, object detection, and sensor fusion with high computational accuracy.

The rapid expansion of generative AI, cloud computing, and edge AI applications is also increasing demand for compact and low-latency AI hardware capable of processing data closer to the source. In addition, hyperscale cloud providers such as AWS, Google Cloud, and Microsoft Azure are increasingly deploying custom AI silicon, such as AWS Trainium and Google TPU v5, to optimize workload efficiency and reduce operational costs. Growing industry adoption in 2025 indicates that AI optimized hardware can reduce inference latency by approximately 40–60% in large-scale distributed computing environments under production workloads.

AI Hardware Market Dynamics

Key Market Driver: Rising Adoption Of AI Driven Data Centers And High Performance Computing Systems

Industries worldwide are experiencing rapid adoption of artificial intelligence across cloud computing, enterprise analytics, and automation systems, driving strong demand for high-performance AI hardware infrastructure. Increasing data generation from digital platforms, IoT devices, and enterprise systems is creating significant pressure on traditional computing architectures, accelerating the shift toward AI optimized hardware solutions.

Technology companies and hyperscale cloud providers are increasingly investing in AI ready data centers equipped with GPUs, ASIC-based accelerators, and high bandwidth memory systems to support large-scale machine learning workloads. For instance in training generative AI models and real-time inference systems, to improve computational efficiency and reduce processing bottlenecks.

Global data center investments exceeded USD 450 billion in 2024, with a significant portion allocated to AI infrastructure expansion, reflecting strong demand for accelerated computing systems and next-generation hardware platforms across North America and Asia-Pacific.

Key Restraint/Challenge: High Power Consumption And Increasing Hardware Cost Pressure

AI hardware systems, particularly GPU and ASIC based architectures, require substantial energy consumption to support intensive computational workloads, creating challenges related to operational efficiency and sustainability. The growing complexity of AI models, especially large language models, significantly increases power density requirements in data centers, leading to higher cooling and infrastructure costs.

In addition, the high cost of advanced semiconductor fabrication, limited availability of cutting-edge chips, and supply chain constraints are increasing the overall cost of AI hardware deployment. Smaller enterprises face challenges in adopting large-scale AI infrastructure due to capital-intensive investment requirements and rapid hardware obsolescence cycles.

Industry estimates indicate that AI optimized data centers can consume up to 2–3 times more power per rack compared to traditional cloud computing setups, with large-scale AI training clusters requiring several megawatts of continuous power, creating significant cost and sustainability pressures for global operators.

Key Market Opportunity: Expansion Of Edge AI And Custom AI Chip Development

The increasing deployment of edge computing devices, autonomous systems, and real-time analytics applications is creating strong opportunities for compact and efficient AI hardware solutions. Demand for low-latency processing in smart devices, industrial automation, healthcare systems, and connected vehicles is driving innovation in edge AI accelerators and embedded computing hardware.

Technology companies are increasingly developing custom AI chips, For instance Apple Neural Engine, Tesla Dojo, and Qualcomm AI Engine, to enhance on-device processing capabilities while reducing dependency on cloud infrastructure. These solutions enable faster response times, improved data privacy, and reduced network bandwidth usage across distributed computing environments.

In addition, advancements in semiconductor manufacturing, including 3nm and 2nm process nodes, are improving performance efficiency and enabling higher transistor density for AI workloads. Pilot deployments in 2025 across industrial automation and smart city projects in Asia-Pacific have demonstrated latency reductions of approximately 35–55% in edge AI inference applications compared to centralized cloud processing systems

AI Hardware Market Scope

The market is segmented on the basis of component, hardware type, technology, deployment mode, application, and end-user.

- By Component

On the basis of component, the AI hardware market is segmented into AI Processors, Memory Devices, Storage Devices, Network Devices, and Others. The AI Processors segment held the largest market revenue share of approximately 52.4% in 2025 driven by strong demand for high-performance computing in training and inference of AI models across data centers, enterprise applications, and cloud platforms. Increasing deployment of GPUs, TPUs, and AI-specific ASICs is further strengthening segment dominance.

The Network Devices segment is projected to register the fastest growth at a CAGR of 24.1% from 2026 to 2033, driven by rising demand for high-speed interconnects, low-latency communication, and scalable data center infrastructure supporting distributed AI workloads and real-time processing applications. Expanding AI data center clusters require advanced networking solutions such as high-bandwidth switches and optical interconnects. Increasing adoption of distributed AI training models is further enhancing demand for ultra-fast data transmission. In addition, growth in edge computing ecosystems is accelerating deployment of intelligent network hardware.

- By Hardware Type

On the basis of hardware type, the AI hardware market is segmented into Processors (CPU, GPU, ASIC, FPGA), Servers, Storage Systems, Networking Hardware, and Edge Devices. The Processors segment held the largest market revenue share of approximately 48.7% in 2025 driven by extensive usage of GPUs and ASICs in AI model training, deep learning workloads, and generative AI applications across hyperscale data centers and enterprise computing environments. Strong demand for AI accelerators is driven by exponential growth in computational requirements for training foundation models. Enterprises are increasingly shifting from traditional CPU-based systems to GPU-dominant architectures. Continuous improvements in chip architecture are enabling faster processing and reduced energy consumption.

The Edge Devices segment is projected to register the fastest growth at a CAGR of 26.3% from 2026 to 2033, driven by rapid adoption of edge AI in autonomous vehicles, smart devices, industrial automation, and IoT ecosystems requiring real-time on-device processing and reduced latency. Growing deployment of smart sensors and connected devices is increasing demand for localized computing power. Edge AI reduces dependency on cloud infrastructure and improves real-time decision-making efficiency. In addition, rising use of AI in industrial robotics and smart manufacturing is further accelerating segment expansion.

- By Technology

On the basis of technology, the AI hardware market is segmented into Machine Learning, Deep Learning, Natural Language Processing, Computer Vision, and Others. The Deep Learning segment held the largest market revenue share of approximately 44.9% in 2025 driven by growing use in large language models, generative AI systems, and advanced neural network training across enterprise and cloud platforms. Increasing complexity of AI models is significantly boosting demand for deep learning optimized hardware such as GPUs and tensor processing units. Enterprises are investing heavily in AI infrastructure to support model training at scale. Rising adoption in predictive analytics and automation systems is further strengthening segment growth.

The Natural Language Processing segment is projected to register the fastest growth at a CAGR of 25.7% from 2026 to 2033, driven by increasing adoption of conversational AI, chatbots, virtual assistants, and enterprise automation tools across industries such as BFSI, healthcare, and retail. Rapid expansion of AI-powered customer engagement platforms is driving hardware requirements for real-time language processing. Enterprises are deploying NLP models for sentiment analysis, translation, and automation workflows. In addition, integration of NLP in enterprise software is accelerating demand for optimized AI computing infrastructure.

- By Deployment Mode

On the basis of deployment mode, the AI hardware market is segmented into Cloud-Based AI Hardware and On-Premise AI Hardware. The Cloud-Based AI Hardware segment held the largest market revenue share of approximately 61.5% in 2025 driven by widespread adoption of hyperscale cloud platforms, scalable computing infrastructure, and AI-as-a-service offerings across enterprises. Cloud platforms enable flexible scaling of AI workloads without heavy upfront infrastructure investment. Major providers are expanding global data center networks to support AI computing demand. Increasing use of hybrid cloud architectures is also contributing to segment growth.

The On-Premise AI Hardware segment is projected to register the fastest growth at a CAGR of 21.9% from 2026 to 2033, driven by increasing demand for data security, regulatory compliance, and low-latency AI processing in sensitive industries such as defense, healthcare, and BFSI. Organizations handling confidential data prefer on-premise deployment for enhanced control and privacy. Rising cybersecurity concerns are further encouraging localized AI infrastructure investments. In addition, latency-sensitive applications in critical industries are boosting adoption.

- By Application

On the basis of application, the AI hardware market is segmented into Data Center & Cloud Computing, Edge Computing, Automotive, Healthcare, Consumer Electronics, Robotics, BFSI, and Others. The Data Center & Cloud Computing segment held the largest market revenue share of approximately 46.8% in 2025 driven by rapid expansion of AI training clusters, hyperscale infrastructure, and enterprise digital transformation initiatives. Growing demand for generative AI model training is significantly increasing data center hardware investments. Cloud service providers are continuously upgrading infrastructure to support AI workloads. Expansion of enterprise digital ecosystems is further accelerating segment dominance.

The Automotive segment is projected to register the fastest growth at a CAGR of 27.2% from 2026 to 2033, driven by rising adoption of autonomous driving systems, advanced driver assistance systems, and AI-based in-vehicle computing platforms. Increasing penetration of electric vehicles is further boosting demand for AI chips in mobility systems. Automotive OEMs are investing in real-time edge AI processing for safety and navigation. In addition, advancements in autonomous vehicle testing are accelerating hardware adoption.

- By End-User

On the basis of end-user, the AI hardware market is segmented into IT & Telecom, Healthcare, Automotive, Retail, BFSI, Government & Defense, Manufacturing, and Others. The IT & Telecom segment held the largest market revenue share of approximately 39.6% in 2025 driven by strong demand for cloud computing infrastructure, data center expansion, and AI-enabled network optimization. Telecom operators are increasingly deploying AI for network traffic management and predictive maintenance. Rising data consumption is pushing investment in high-performance computing systems. In addition, AI-driven automation is improving operational efficiency across IT services.

The Automotive segment is projected to register the fastest growth at a CAGR of 26.8% from 2026 to 2033, driven by increasing integration of AI chips in autonomous vehicles, EV platforms, and smart mobility systems enabling real-time decision-making and enhanced vehicle intelligence. Growing focus on vehicle automation and safety systems is accelerating adoption of AI hardware. OEMs are integrating advanced computing modules for ADAS and infotainment systems. Expansion of connected vehicle ecosystems is further strengthening segment growth.

AI Hardware Market Regional Analysis

North America AI Hardware Market Insight

North America dominated the AI hardware market with the largest revenue share of 38.9% in 2025, supported by strong presence of hyperscale cloud providers, advanced semiconductor ecosystem, and early adoption of artificial intelligence across enterprise and government sectors. The region benefits from high investments in data center infrastructure, AI chip development, and cloud computing expansion, driving strong demand for GPUs, ASICs, and AI optimized servers. Increasing integration of AI in industries such as automotive, healthcare, BFSI, and IT & telecom is further strengthening regional dominance.

U.S. AI Hardware Market Insight

The U.S. AI hardware market captured the largest revenue share within North America in 2025, driven by rapid expansion of AI data centers, strong R&D investments in semiconductor technologies, and widespread adoption of generative AI applications. Leading technology companies such as NVIDIA, AMD, Intel, and major cloud providers are significantly increasing deployment of advanced AI accelerators. Growing demand for large language models, autonomous systems, and AI powered enterprise solutions is further accelerating hardware consumption.

Europe AI Hardware Market Insight

The Europe AI hardware market is expected to witness steady growth from 2026 to 2033, primarily driven by increasing adoption of AI across industrial automation, automotive manufacturing, and healthcare systems. Strong regulatory focus on data privacy and sovereign cloud infrastructure is encouraging investment in localized AI computing systems. Countries across the region are increasingly deploying AI optimized hardware in smart factories, research institutions, and public sector digital transformation initiatives.

U.K. AI Hardware Market Insight

The U.K. AI hardware market is expected to witness strong growth from 2026 to 2033, driven by rising adoption of AI in financial services, cybersecurity, and enterprise analytics. London’s position as a global fintech hub is contributing significantly to demand for high-performance computing infrastructure. Increasing investments in AI startups and government backed AI innovation programs are further strengthening deployment of advanced processors and cloud based AI systems.

Germany AI Hardware Market Insight

The Germany AI hardware market is expected to witness strong growth from 2026 to 2033, supported by rapid adoption of Industry 4.0 technologies, smart manufacturing systems, and industrial automation. Germany’s strong automotive and engineering sectors are increasingly integrating AI chips into autonomous driving systems and robotics applications. Rising focus on energy efficient computing and secure data processing is further driving demand for on-premise AI hardware solutions.

Asia-Pacific AI Hardware Market Insight

The Asia-Pacific AI hardware market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid digital transformation, expanding semiconductor manufacturing capabilities, and rising adoption of AI across consumer electronics and industrial sectors. Countries such as China, Japan, South Korea, and India are heavily investing in AI infrastructure, cloud platforms, and edge computing systems. The region is also emerging as a major hub for AI chip production and assembly, significantly improving hardware affordability and accessibility.

Japan AI Hardware Market Insight

The Japan AI hardware market is expected to witness strong growth from 2026 to 2033 due to high adoption of robotics, automation technologies, and advanced manufacturing systems. The country’s focus on precision engineering and smart factory development is driving deployment of AI processors in industrial applications. Increasing demand for AI enabled healthcare systems and autonomous mobility solutions is further supporting market expansion.

China AI Hardware Market Insight

The China AI hardware market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to massive investments in AI infrastructure, strong domestic semiconductor ecosystem, and rapid expansion of smart city projects. China is one of the largest markets for AI powered applications across surveillance, cloud computing, and industrial automation. Government support for AI development and strong presence of local chip manufacturers are key factors driving market growth across multiple sectors.

AI Hardware Market Share

The AI Hardware industry is primarily led by well-established companies, including:

• NVIDIA (U.S.)

• Microsoft (U.S.)

• Qualcomm Technologies (U.S.)

• Amazon Web Services (U.S.)

• Intel (U.S.)

• Advanced Micro Devices (U.S.)

• International Business Machines (U.S.)

• Apple Inc. (U.S.)

• Google LLC (U.S.)

• Hewlett Packard Enterprise (U.S.)

• Arm Holdings (U.K.)

• Samsung Electronics (South Korea)

• Taiwan Semiconductor Manufacturing Company (Taiwan)

• Broadcom Inc. (U.S.)

• Meta Platforms (U.S.)

Latest Developments in AI Hardware Market

- In July 2025, HNSE Asia announced the expansion of its AI Hardware Battle 2025 into Japan, representing a strategic event development aimed at strengthening international collaboration in advanced computing technologies. The initiative, conducted in partnership with major retail channels, will showcase next-generation AI hardware innovations across consumer electronics and enterprise solutions. This expansion is expected to enhance visibility for emerging technology firms and startups in Asia’s high-end electronics ecosystem. The program will support cross-border innovation exchange and accelerate commercialization of AI-enabled hardware solutions. It is also likely to strengthen Japan’s position as a key hub for AI hardware adoption and innovation in the region.

- In June 2025, Apple Inc. introduced its A18 and A18 Pro chips alongside the iPhone 16 series, marking a major product advancement in AI-enabled consumer hardware. The development features an upgraded Neural Engine delivering up to 35 TOPS, significantly improving on-device machine learning performance. This enables real-time AI functions such as text summarization, image processing, and Siri enhancements while maintaining strong privacy through local processing. The innovation reduces dependency on cloud computing and enhances device efficiency. It is expected to drive strong demand for AI-integrated smartphones and set new benchmarks for mobile AI hardware performance.

- In June 2025, Nvidia Corporation unveiled its Blackwell GPU architecture, representing a major product innovation in high-performance AI computing hardware. The new GPUs, expected to power the RTX 50 series, demonstrate up to 50 times higher efficiency compared to traditional CPUs in AI workloads. Improvements in FLOPS performance, memory bandwidth, and energy optimization significantly enhance large-scale AI computation capabilities. This development strengthens Nvidia’s leadership in AI accelerator technology. It is expected to accelerate adoption of GPU-based AI infrastructure across data centers and enterprise computing environments globally.

- In March 2025, SoftBank Group completed the acquisition of Ampere Computing, marking a strategic corporate expansion in the AI hardware sector. The acquisition aims to strengthen SoftBank’s synergy across Arm-based processor ecosystems and AI data center technologies. Ampere’s expertise in cloud-native and energy-efficient processors is expected to enhance SoftBank’s AI computing portfolio. This move supports the development of scalable, high-performance AI infrastructure solutions. It is anticipated to intensify competition in the global AI processor market while accelerating innovation in energy-efficient data center hardware architectures.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.