Global Airborne Satellite Communications Satcom Market

Market Size in USD Billion

USD

7.24 Billion

USD

10.95 Billion

2023

2031

USD

7.24 Billion

USD

10.95 Billion

2023

2031

| 2024 - 2031 | |

| USD 7.24 Billion | |

| USD 10.95 Billion | |

| % | |

|

Airborne Satellite Communications (SATCOM) Market Size

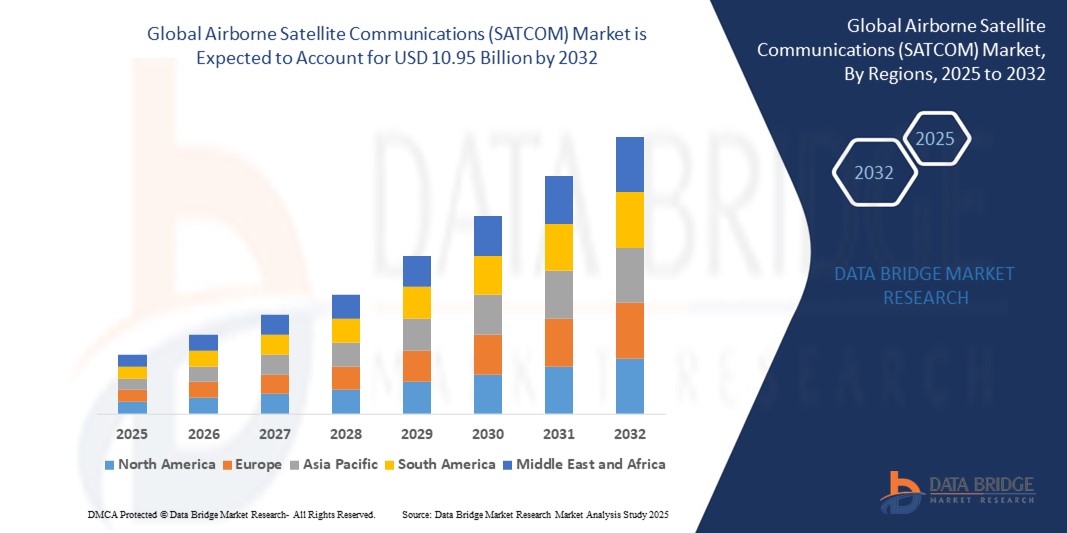

- The global airborne satellite communications (SATCOM) market size was valued at USD 7.24 billion in 2024 and is expected to reach USD 10.95 billion by 2032, at a CAGR of 5.30% during the forecast period

- The market growth is primarily driven by the increasing demand for high-speed, reliable connectivity in aviation, fueled by advancements in satellite technology and the growing need for real-time data transmission in both commercial and defense applications

- Rising adoption of in-flight connectivity solutions, coupled with the expansion of unmanned aerial vehicles (UAVs) and business aviation, is further accelerating market growth, as stakeholders prioritize seamless communication systems for enhanced safety and operational efficiency

Airborne Satellite Communications (SATCOM) Market Analysis

- Airborne SATCOM systems, providing robust and secure communication for aircraft, UAVs, and helicopters, are critical for modern aviation, enabling real-time data exchange, voice communication, and connectivity for passengers and operators

- The surge in demand is driven by the growing need for in-flight entertainment, real-time navigation, and mission-critical communications in defense applications, alongside increasing investments in satellite infrastructure

- North America dominated the airborne SATCOM market with the largest revenue share of 42.5% in 2024, driven by advanced aerospace infrastructure, significant defense spending, and the presence of leading SATCOM providers in the U.S., with innovations in Ka-band and Ku-band technologies fueling growth

- Europe is expected to be the fastest-growing region during the forecast period, propelled by increasing investments in aviation modernization, growing demand for commercial in-flight connectivity, and supportive regulatory frameworks for satellite communications

- The Commercial Aircraft segment dominated the largest market revenue share of 38.5% in 2024, driven by the increasing demand for in-flight connectivity and entertainment services in commercial aviation

Report Scope and Airborne Satellite Communications (SATCOM) Market Segmentation

|

Attributes |

Airborne Satellite Communications (SATCOM) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Airborne Satellite Communications (SATCOM) Market Trends

“Increasing Integration of AI and Low Earth Orbit (LEO) Satellite Technology”

- The Global Airborne Satellite Communications (SATCOM) market is experiencing a significant trend toward integrating Artificial Intelligence (AI) and Low Earth Orbit (LEO) satellite technology.

- AI enables advanced data processing, offering insights into aircraft performance, communication efficiency, and predictive maintenance needs.

- AI-driven SATCOM systems facilitate proactive issue resolution, such as optimizing satellite connectivity or identifying potential system failures before they disrupt operations.

- For instances, companies are developing AI-powered platforms to optimize bandwidth allocation for in-flight connectivity and enhance real-time communication for unmanned aerial vehicles (UAVs).

- LEO satellite constellations, with their lower latency and higher data rates, are revolutionizing airborne SATCOM by enabling faster and more reliable communication for both commercial and military applications.

- This trend enhances the value of SATCOM systems, making them more appealing to airlines, defense organizations, and business jet operators.

Airborne Satellite Communications (SATCOM) Market Dynamics

Driver

“Rising Demand for In-Flight Connectivity and Mission-Critical Communications”

- Growing consumer demand for seamless in-flight connectivity, including high-speed internet, real-time navigation, and entertainment, is a key driver for the airborne SATCOM market.

- SATCOM systems enhance safety and operational efficiency through features such as beyond-line-of-sight communication, real-time surveillance, and mission-critical data transfer for military applications.

- Government mandates, such as those in Europe for advanced air traffic management systems, are accelerating the adoption of SATCOM technologies.

- The proliferation of Internet of Things (IoT) and 5G technology is enabling faster data transmission and lower latency, supporting advanced applications such as real-time UAV control and in-flight streaming services.

- Aircraft manufacturers are increasingly integrating factory-fitted SATCOM systems as standard or optional features to meet consumer expectations and enhance aircraft functionality.

Restraint/Challenge

“High Implementation Costs and Cybersecurity Risks”

- The high initial costs of SATCOM hardware, software, and integration into aircraft systems pose a significant barrier, particularly for smaller operators or in emerging markets.

- Retrofitting existing aircraft with SATCOM systems can be complex and expensive, limiting widespread adoption.

- Cybersecurity and data privacy concerns are major challenges, as SATCOM systems transmit sensitive data, such as flight paths and military communications, raising risks of breaches or unauthorized access.

- The fragmented global regulatory landscape for data privacy and spectrum allocation complicates compliance for manufacturers and service providers operating across multiple regions.

- These factors may deter adoption, especially in regions with high cost sensitivity or stringent data protection regulations.

Airborne Satellite Communications (SATCOM) market Scope

The market is segmented on the basis of platform, component, frequency, installation, and application.

- By Platform

On the basis of platform, the Global Airborne Satellite Communications (SATCOM) Market is segmented into Commercial Aircraft, Narrow Body Aircraft (NBA), Wide Body Aircraft (WBA), Regional Transport Aircraft (RTA), Military Aircraft, Business Jets, Helicopters, Unmanned Aerial Vehicles (UAV), and Special-purpose UAVs. The Commercial Aircraft segment dominated the largest market revenue share of 38.5% in 2024, driven by the increasing demand for in-flight connectivity and entertainment services in commercial aviation. The rise in passenger traffic and airline investments in enhanced passenger experiences further bolster this segment.

The Unmanned Aerial Vehicles (UAV) segment is expected to witness the fastest growth rate of 8.2% from 2025 to 2032, fueled by the growing adoption of UAVs for military and commercial applications, such as surveillance, reconnaissance, and delivery services. The need for reliable, high-speed SATCOM systems for beyond-line-of-sight (BLOS) operations drives this segment’s growth.

- By Component

On the basis of component, the market is segmented into SATCOM Terminals, Transceivers, Airborne Radio, Modems and Routers, SATCOM Radomes, and Others. The SATCOM Terminals segment accounted for the largest market revenue share of 32.7% in 2024, driven by their critical role in enabling seamless connectivity for voice, data, and video communications across airborne platforms. The increasing demand for high-speed internet and real-time data exchange in commercial and military applications supports this segment’s dominance.

The Modems and Routers segment is anticipated to experience the fastest growth rate of 7.5% from 2025 to 2032, propelled by advancements in satellite technology, such as high-throughput satellites (HTS), which enhance data transmission rates and network efficiency. These components are essential for managing complex data traffic and ensuring reliable communication.

- By Frequency

On the basis of frequency, the market is segmented into C-band, L-band, X-band, Ka-band, S-band, Ku-band, and UHF-band. The Ku-band segment held the largest market revenue share of 29.4% in 2024, owing to its widespread use in commercial aviation for in-flight connectivity and its balance of high data rates and reliable coverage. Its adoption in business jets and commercial aircraft further strengthens its position.

The Ka-band segment is expected to witness significant growth from 2025 to 2032, driven by its ability to deliver higher bandwidth and faster data rates, making it ideal for next-generation SATCOM applications. The shift toward high-throughput satellites and low-latency communication supports this segment’s rapid adoption.

- By Installation

On the basis of installation, the market is segmented into New Installation and Upgradation. The New Installation segment dominated the market with a revenue share of 62.3% in 2024, driven by the increasing integration of advanced SATCOM systems in newly manufactured aircraft, particularly in commercial and military aviation. Regulatory requirements and consumer demand for connected services further fuel this segment.

The Upgradation segment is anticipated to witness robust growth from 2025 to 2032, as operators seek to retrofit existing aircraft with modern SATCOM systems to enhance connectivity, security, and operational efficiency. The rise in demand for advanced antenna technologies and software-defined radios accelerates this segment’s growth.

- By Application

On the basis of application, the market is segmented into Government and Defense and Commercial. The Commercial segment held the largest market revenue share of 58.6% in 2024, driven by the growing demand for in-flight connectivity, real-time navigation, and entertainment services in commercial aviation. Airlines are increasingly investing in SATCOM to improve passenger experience and operational efficiency.

The Government and Defense segment is expected to witness rapid growth of 7.8% from 2025 to 2032, fueled by increasing military modernization programs and the need for secure, reliable communication for mission-critical operations. The adoption of SATCOM in UAVs and military aircraft for surveillance, reconnaissance, and tactical communication drives this segment’s expansion.

Airborne Satellite Communications (SATCOM) Market Regional Analysis

- North America dominated the airborne SATCOM market with the largest revenue share of 42.5% in 2024, driven by advanced aerospace infrastructure, significant defense spending, and the presence of leading SATCOM providers in the U.S., with innovations in Ka-band and Ku-band technologies fueling growth

- Consumers and operators prioritize SATCOM systems for real-time communication, enhanced situational awareness, and secure data transfer, particularly in military and commercial aviation

- Growth is supported by technological advancements in high-throughput satellites (HTS), compact SATCOM terminals, and increasing adoption in both OEM and aftermarket segments

U.S. Airborne Satellite Communications (SATCOM) Market Insight

The U.S. airborne satellite communications (SATCOM) market captured the largest revenue share of 89.8% in 2024 within North America, fueled by strong demand for secure and reliable communication systems in defense and commercial applications. The trend towards integrating advanced SATCOM solutions in unmanned aerial vehicles (UAVs) and commercial aircraft, coupled with growing consumer awareness of in-flight connectivity benefits, drives market expansion. Regulatory support for modernizing air traffic management and increasing investments from key players such as Viasat and Honeywell further bolster growth.

Europe Airborne Satellite Communications (SATCOM) Market Insight

The European airborne SATCOM market is expected to witness the fastest growth rate, driven by increasing demand for in-flight connectivity and regulatory emphasis on aviation safety and efficiency. Consumers and operators seek SATCOM systems that provide seamless communication, improved navigation, and enhanced passenger experiences. Countries such as Germany and the U.K. show significant uptake due to rising air passenger traffic and military modernization programs.

U.K. Airborne SATCOM Market Insight

The U.K. market for airborne SATCOM is expected to experience rapid growth, propelled by the demand for enhanced in-flight connectivity and secure communication systems in both commercial and military aviation. The increasing focus on passenger comfort, such as high-speed internet access, and the integration of SATCOM in urban air mobility platforms drive adoption. Evolving regulations ensuring secure and reliable communication further influence market trends, balancing performance with compliance.

Germany Airborne SATCOM Market Insight

Germany is expected to witness the fastest growth rate in the European airborne SATCOM market, attributed to its advanced aerospace sector and focus on secure, high-bandwidth communication systems. German operators prioritize technologically advanced SATCOM solutions, such as Ka-band and Ku-band systems, to enhance operational efficiency and support real-time data transfer. The integration of SATCOM in premium military aircraft and aftermarket applications sustains market growth.

Asia-Pacific Airborne SATCOM Market Insight

The Asia-Pacific region is expected to exhibit significant growth in the airborne SATCOM market, driven by expanding aviation industries and rising defense budgets in countries such as China, India, and Japan. Increasing awareness of the benefits of real-time communication, secure data transfer, and in-flight connectivity boosts demand. Government initiatives to modernize aviation infrastructure and the growing use of UAVs for commercial and military purposes further support market expansion.

Japan Airborne SATCOM Market Insight

Japan’s airborne SATCOM market is expected to witness rapid growth due to strong consumer and industry preference for high-performance SATCOM systems that enhance safety, connectivity, and operational efficiency. The presence of major aerospace manufacturers and the integration of SATCOM in OEM aircraft accelerate market penetration. Growing interest in aftermarket upgrades and the adoption of advanced satellite constellations, such as low Earth orbit (LEO) systems, contribute to sustained growth.

China Airborne SATCOM Market Insight

China holds the largest share of the Asia-Pacific airborne SATCOM market, driven by rapid urbanization, increasing aircraft production, and growing demand for secure and high-speed communication solutions. The country’s expanding middle class and focus on smart aviation technologies support the adoption of advanced SATCOM systems. Strong domestic manufacturing capabilities and competitive pricing, combined with government investments in satellite infrastructure, enhance market accessibility and growth

Airborne Satellite Communications (SATCOM) Market Share

The airborne satellite communications (SATCOM) industry is primarily led by well-established companies, including:

- ASELSAN A.S. (Turkey)

- Thales (France)

- Collins Aerospace (U.S.)

- Cobham Limited (U.K.)

- Honeywell International Inc. (U.S.)

- General Dynamics Corporation (U.S.)

- Gilat Satellite Networks (Israel)

- L3Harris Technologies, Inc. (U.S.)

- Hughes Network Systems, LLC (U.S.)

- Viasat (U.S.)

- Orbit Communications Systems Ltd. (Israel)

- Astronics Corporation (U.S.)

- Norsat International Inc. (Canada)

- Raytheon Technologies Corporation (U.S.)

- Smiths Group plc (U.K.)

- ST Engineering (Singapore)

- Mitsubishi Electric Corporation (Japan)

- Iridium Communications Inc. (U.S.)

- Teledyne Defense Electronics (U.S.)

What are the Recent Developments in Global Airborne Satellite Communications (SATCOM) Market?

- In July 2024, Türkiye achieved a historic milestone with the launch of TURKSAT-6A, its first domestically developed communication satellite, from Cape Canaveral, Florida. Engineered by ASELSAN, the satellite features advanced Ku-Band and X-Band payloads, enabling robust communication services across Türkiye, Europe, and South Asia. This achievement places Türkiye among a select group of nations capable of producing their own communication satellites. The satellite’s deployment is expected to significantly enhance airborne SATCOM capabilities, defense communications, and global data infrastructure, while showcasing ASELSAN’s growing expertise in space technologies

- In June 2024, Gilat Satellite Networks Ltd. secured over $14 million in orders from leading system integrators and service providers for its In-Flight Connectivity (IFC) solutions. The orders include solid-state power amplifiers (SSPAs), network equipment, and auxiliary IFC components, underscoring the growing demand for advanced airborne connectivity in commercial and business aviation. This momentum follows Gilat’s strategic acquisition of Stellar Blu Solutions, a move that strengthens its position in the IFC market and expands its portfolio with next-generation SATCOM terminals. The company’s airborne technologies are deployed globally across thousands of aircraft

- In June 2024, Viasat Inc. expanded its partnership with Airbus Defence and Space to integrate the GAT-5530 dual-band (Ku/Ka) broadband terminal into Spain’s C295 Maritime Patrol Aircraft (MPA) fleet. This advanced SATCOM solution supports multi-orbit and multi-band connectivity, enabling seamless communication across sovereign and commercial networks. Designed to operate with the next-generation SpainSat NG satellites, the GAT-5530 enhances mission-critical capabilities such as command and control (C2), intelligence, surveillance, and reconnaissance (ISR). The collaboration reflects Spain’s commitment to resilient airborne connectivity and Viasat’s leadership in secure satellite communications

- In April 2024, ASELSAN Latin America, a subsidiary of Türkiye’s defense electronics leader ASELSAN A.S., announced the opening of its new office in Santiago, Chile, marking a major step in its regional expansion strategy. Timed with its participation in FIDAE 2024, Latin America’s premier aerospace exhibition, the move aims to strengthen ties with local government agencies, defense organizations, and industry stakeholders. The Santiago office will serve as a regional hub for strategic partnerships, technology transfers, and joint ventures—particularly in airborne SATCOM, radar, and electronic warfare systems—reinforcing ASELSAN’s commitment to innovation and collaboration across Latin America

- In March 2024, Astronics Corporation launched the Typhon T-400 Series, a next-generation SATCOM system engineered for seamless operation on any GEO-based Ku-band satellite network. The system features a streamlined dual Line Replaceable Unit (LRU) design, reducing the number of components from four to two—significantly lowering installation complexity and fly-away costs. It incorporates iQ800 modem technology from iDirect and a versatile Modem Manager (MODMAN) that supports flexible mounting and integration. With options for modem-less configurations, the Typhon T-400 is tailored for commercial, special mission, and military aircraft, offering high-performance connectivity with reduced lifecycle costs

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.