Global Aircraft Ailerons Market

Market Size in USD Billion

USD

2.04 Billion

USD

3.59 Billion

2025

2033

USD

2.04 Billion

USD

3.59 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.04 Billion | |

| USD 3.59 Billion | |

| % | |

|

What is the Global Aircraft Ailerons Market Size and Growth Rate?

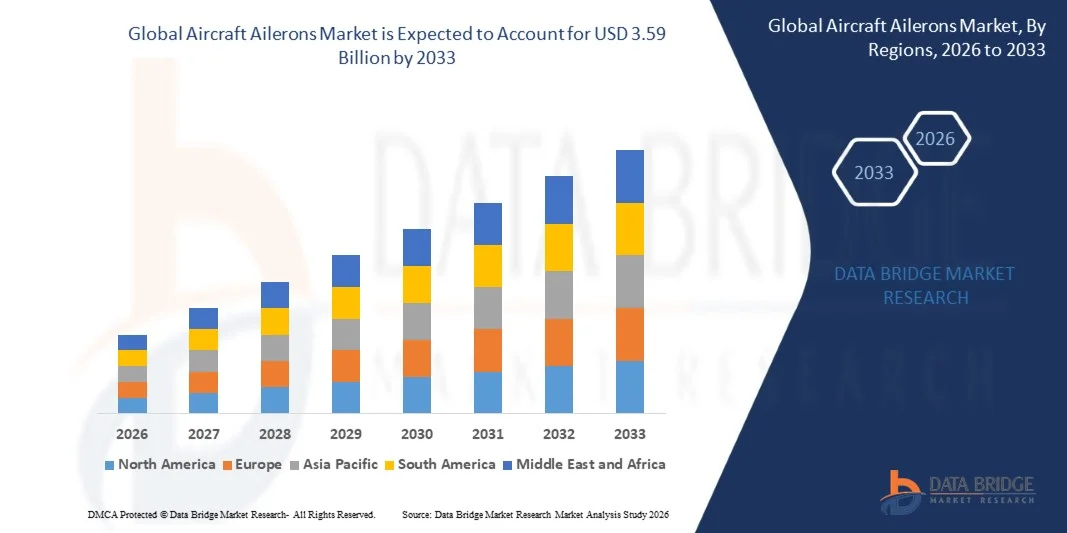

- The global aircraft ailerons market size was valued at USD 2.04 billion in 2025 and is expected to reach USD 3.59 billion by 2033, at a CAGR of 7.30% during the forecast period

- Major factors that are expected to boost the growth of the aircraft ailerons market in the forecast period are the innovation of fly-by-wire technology

- Furthermore, the decrease in the weight of the ailerons fitted on the win is further anticipated to propel the growth of the aircraft ailerons market

What are the Major Takeaways of Aircraft Ailerons Market?

- The utilization of the multiple ailerons on the aircraft is further estimated to cushion the growth of the aircraft ailerons market. On the other hand, the fly-by-wire technology in the older aircrafts are challenging because of the complex mechanisms is further projected to impede the growth of the aircraft ailerons market in the timeline period

- In addition, the rise in the concerning issues regarding the smooth aircraft operation which has enhanced the interest for automated flight control surfaces will further provide potential opportunities for the growth of the aircraft ailerons market in the coming years. However, rise in the cost of manufacturing and designing might further challenge the growth of the aircraft ailerons market in the near future

- North America dominated the aircraft ailerons market with a 41.36% revenue share in 2025, driven by strong aircraft production, advanced aerostructure manufacturing capabilities, and continuous investments in commercial and military aviation programs across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 7.71% from 2026 to 2033, driven by rapid expansion of commercial aviation fleets, increasing defense procurement, and strengthening domestic aircraft manufacturing capabilities across China, Japan, India, and South Korea

- The Commercial Aircraft segment dominated the market with a 41.6% share in 2025, driven by rising global air passenger traffic, increasing narrow-body aircraft deliveries, and continuous fleet expansion by major airlines

Report Scope and Aircraft Ailerons Market Segmentation

|

Attributes |

Aircraft Ailerons Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Aircraft Ailerons Market?

“Increasing Shift Toward Lightweight Composite and Fly-by-Wire Integrated Aileron Systems”

- The aircraft ailerons market is witnessing strong adoption of lightweight composite materials such as carbon fiber-reinforced polymers to reduce aircraft weight and improve fuel efficiency

- Manufacturers are integrating ailerons with fly-by-wire (FBW) systems, enabling precise electronic control, reduced mechanical complexity, and improved flight stability

- Growing emphasis on aerodynamic optimization and drag reduction is driving the development of high-performance, digitally actuated aileron structures for commercial and military aircraft

- For instance, companies such as Boeing, Airbus, Saab AB, and Turkish Aerospace Industries are incorporating advanced composite wing and control surface technologies in next-generation aircraft platforms

- Increasing demand for fuel-efficient narrow-body aircraft, UAVs, and advanced fighter jets is accelerating the shift toward smart, lightweight, and electronically controlled aileron systems

- As aircraft designs become more energy-efficient and digitally integrated, advanced aileron systems will remain critical for roll control precision, structural efficiency, and flight safety

What are the Key Drivers of Aircraft Ailerons Market?

- Rising demand for fuel-efficient aircraft across commercial aviation is increasing the need for lightweight and aerodynamically optimized aileron systems

- For instance, during 2024–2025, leading manufacturers such as Bombardier and TATA Advanced Systems Limited expanded their aerostructure capabilities to support advanced composite control surfaces and wing components

- Growing defense modernization programs and procurement of next-generation fighter jets are boosting demand for high-performance, durable, and electronically actuated ailerons

- Increasing production of unmanned aerial vehicles (UAVs) and regional aircraft is creating demand for compact, lightweight, and cost-efficient control surfaces

- Advancements in actuation systems, smart sensors, and structural health monitoring technologies are improving reliability, performance, and lifecycle management

- Supported by rising global air passenger traffic, military upgrades, and investments in aerospace manufacturing infrastructure, the Aircraft Ailerons market is expected to witness steady long-term growth

Which Factor is Challenging the Growth of the Aircraft Ailerons Market?

- High costs associated with advanced composite materials, precision manufacturing, and certification processes restrict adoption among smaller aircraft manufacturers

- For instance, during 2024–2025, fluctuations in raw material prices such as carbon fiber and aerospace-grade alloys increased overall production costs for several aerostructure suppliers

- Stringent aviation safety regulations and lengthy certification timelines increase development complexity and delay product launches

- Integration challenges between mechanical structures and fly-by-wire electronic systems require specialized engineering expertise and testing infrastructure

- Supply chain disruptions in aerospace components and reliance on limited Tier-1 suppliers create production bottlenecks and pricing pressures

How is the Aircraft Ailerons Market Segmented?

The market is segmented on the basis of aircraft type, material type, and aileron type.

• By Aircraft Type

On the basis of aircraft type, the Aircraft Ailerons market is segmented into Commercial Aircraft, Passenger Aircrafts, Logistics Aircrafts, Military Aircraft, Combat Aircrafts, and Non-Combat Aircrafts. The Commercial Aircraft segment dominated the market with a 41.6% share in 2025, driven by rising global air passenger traffic, increasing narrow-body aircraft deliveries, and continuous fleet expansion by major airlines. Commercial platforms require lightweight, fuel-efficient, and aerodynamically optimized aileron systems to enhance roll control and operational efficiency. Growing aircraft production programs and modernization initiatives further support segment dominance.

The Military Aircraft segment is expected to grow at the fastest CAGR from 2026 to 2033, fueled by rising defense budgets, procurement of next-generation fighter jets, and increasing adoption of advanced fly-by-wire control systems. Combat and surveillance aircraft require high-performance, durable, and precision-controlled ailerons capable of operating under extreme flight conditions, accelerating innovation and demand in this segment.

• By Material Type

On the basis of material type, the Aircraft Ailerons market is segmented into Composite Materials, Thermoplastic Materials, Thermoset Materials, and Metals. The Composite Materials segment dominated the market with a 48.3% share in 2025, owing to their superior strength-to-weight ratio, corrosion resistance, and fatigue durability. Aircraft manufacturers increasingly prefer carbon fiber-reinforced polymers and advanced composites to reduce overall aircraft weight and improve fuel efficiency. Composite ailerons also support better aerodynamic shaping and lower lifecycle maintenance costs, strengthening their widespread adoption in both commercial and military aircraft.

The Thermoplastic Materials segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by advantages such as recyclability, impact resistance, and faster manufacturing cycles. Growing focus on sustainable aviation, cost-efficient production techniques, and automated composite processing technologies is expected to accelerate thermoplastic material adoption in future aircraft programs.

• By Aileron Type

On the basis of aileron type, the Aircraft Ailerons market is segmented into Single Acting Ailerons, Frise Ailerons, Wingtip Ailerons, and Differential Ailerons. The Single Acting Ailerons segment dominated the market with a 37.5% share in 2025, as they are widely used in conventional aircraft designs due to their simple mechanical structure, reliability, and cost-effectiveness. These systems are commonly deployed in training aircraft, light commercial aircraft, and certain transport platforms where operational simplicity and ease of maintenance are critical.

The Differential Ailerons segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by increasing demand for improved roll control efficiency and reduced adverse yaw. Advanced aircraft platforms are adopting differential and performance-optimized aileron configurations to enhance maneuverability, flight stability, and aerodynamic performance, particularly in next-generation commercial jets and high-agility military aircraft.

Which Region Holds the Largest Share of the Aircraft Ailerons Market?

- North America dominated the aircraft ailerons market with a 41.36% revenue share in 2025, driven by strong aircraft production, advanced aerostructure manufacturing capabilities, and continuous investments in commercial and military aviation programs across the U.S. and Canada. High adoption of lightweight composite materials, fly-by-wire systems, and next-generation wing technologies continues to fuel demand for advanced aileron systems across OEMs and Tier-1 supplier

- Leading aerospace companies in North America are introducing high-performance, aerodynamically optimized, and electronically integrated aileron systems, strengthening the region’s technological leadership. Continuous investments in defense modernization, UAV development, and sustainable aviation initiatives support long-term market expansion

- Strong aerospace R&D infrastructure, presence of major aircraft manufacturers, and well-established supply chains further reinforce regional dominance in advanced flight control surface production

U.S. Aircraft Ailerons Market Insight

The U.S. is the largest contributor in North America, supported by extensive commercial aircraft manufacturing, defense aviation programs, and advanced composite production capabilities. Increasing development of next-generation fighter jets, unmanned aerial systems, and fuel-efficient narrow-body aircraft intensifies demand for lightweight and digitally controlled ailerons. Strong collaboration between OEMs, Tier-1 suppliers, and research institutions further accelerates innovation and large-scale deployment.

Canada Aircraft Ailerons Market Insight

Canada contributes significantly to regional growth, driven by a strong aerostructure manufacturing base and expertise in composite wing components. Expanding aircraft assembly programs, supplier partnerships, and government-supported aerospace innovation initiatives support increasing production of advanced aileron systems for commercial and business aircraft platforms.

Asia-Pacific Aircraft Ailerons Market

Asia-Pacific is projected to register the fastest CAGR of 7.71% from 2026 to 2033, driven by rapid expansion of commercial aviation fleets, increasing defense procurement, and strengthening domestic aircraft manufacturing capabilities across China, Japan, India, and South Korea. Growing investments in indigenous aircraft programs, UAV development, and regional airline expansion are accelerating demand for lightweight and high-performance ailerons.

China Aircraft Ailerons Market Insight

China is the largest contributor to Asia-Pacific growth due to rising aircraft production, strong government backing for aerospace self-reliance, and increasing development of commercial and military platforms. Expanding composite manufacturing capabilities further support market expansion.

Japan Aircraft Ailerons Market Insight

Japan shows steady growth supported by advanced materials engineering, precision manufacturing, and participation in global aircraft supply chains. Increasing focus on lightweight aerostructures and fuel efficiency drives sustained demand.

India Aircraft Ailerons Market Insight

India is emerging as a growth hub, supported by expanding defense aviation programs, indigenous aircraft development, and growing aerospace manufacturing investments under government initiatives.

South Korea Aircraft Ailerons Market Insight

South Korea contributes significantly due to rising fighter jet programs, UAV development, and strengthening aerospace export capabilities, driving long-term demand for advanced aileron systems.

Which are the Top Companies in Aircraft Ailerons Market?

The aircraft ailerons industry is primarily led by well-established companies, including:

- Saab AB (Sweden)

- Sealand Aviation Ltd. (U.A.E)

- ShinMaywa Industries, Ltd. (Japan)

- Strata Manufacturing PJSC. (U.A.E)

- TATA Advanced Systems Limited (India)

- Bombardier (Canada)

- Asian Composites Manufacturing (ACM) (Thailand)

- Turkish Aerospace Industries, Inc. (Türkiye)

- Zenith Aircraft Company (U.S.)

- LAM AVIATION (U.A.E)

- Boeing (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- Honeywell International Inc. (U.S.)

- Cobham Limited (U.K.)

- Collins Aerospace (U.S.)

- Amphenol Corporation (U.S.)

- McMurdo Group (U.K.)

- Sensor Systems (U.S.)

- TECOM Industries, Inc. (U.S.)

- Antcom (U.S.)

What are the Recent Developments in Global Aircraft Ailerons Market?

- In November 2023, Airbus, headquartered in the Netherlands, entered into fresh agreements with Indian aerospace suppliers including Aequs, Dynamatic, Gardner, and Mahindra Aerospace for manufacturing critical airframe and wing components supporting its A320neo, A330neo, and A350 aircraft programs, strengthening its global supply chain footprint and expanding industrial collaboration in India, thereby reinforcing long-term production scalability and cost efficiency

- In August 2023, the United States Air Force announced plans to fund the next development phase of a blended wing body prototype in partnership with JetZero, a company focused on designing next-generation sustainable aircraft aimed at significantly lowering fuel consumption and carbon emissions, marking a major step toward advanced fuel-efficient military aviation platforms and sustainable aerospace innovation

- In March 2023, Tata Group, based in Mumbai, signed an agreement with Lockheed Martin to initiate fighter wing production at their joint venture facility, Tata Lockheed Martin Aerostructures Limited (TLMAL) in Hyderabad, with plans to manufacture 29 fighter wing ship sets and potential additional orders starting deliveries from 2025, significantly enhancing India’s aerospace manufacturing capabilities and global defense supply chain integration

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.