Global Aliphatic Thinners Market

Market Size in USD Billion

USD

5.26 Billion

USD

7.42 Billion

2024

2032

USD

5.26 Billion

USD

7.42 Billion

2024

2032

| 2025 - 2032 | |

| USD 5.26 Billion | |

| USD 7.42 Billion | |

| % | |

|

Aliphatic Thinners Market Size

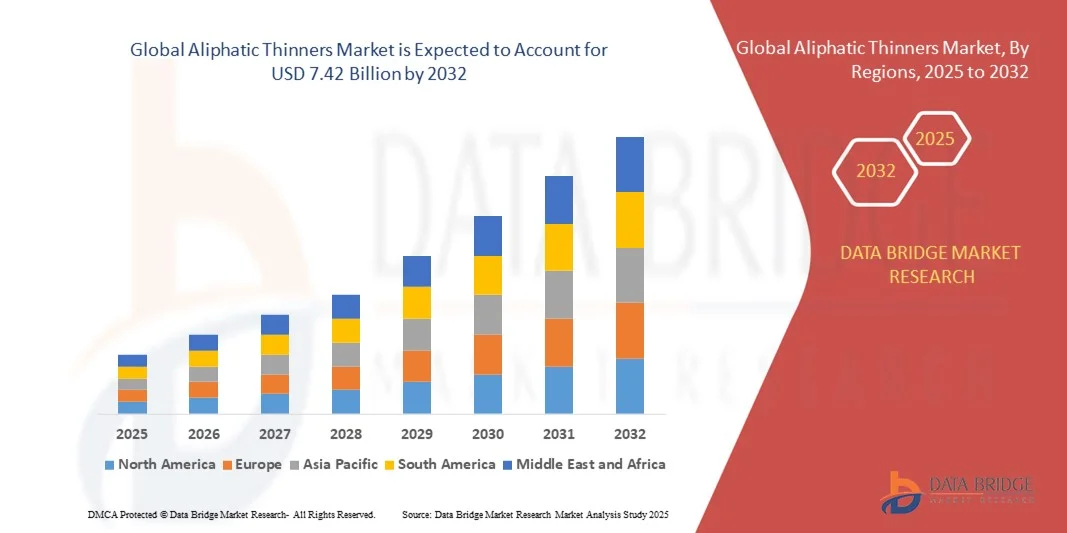

- The global aliphatic thinners market size was valued at USD 5.26 billion in 2024 and is expected to reach USD 7.42 billion by 2032, at a CAGR of 4.4% during the forecast period

- The market growth is largely fuelled by increasing demand from paints, coatings, and adhesives industries, rising adoption in cleaning and degreasing applications, and the shift toward solvent-based formulations that improve product performance and drying efficiency

- Growing industrialization, expanding construction activities, and rising automotive production are further driving the adoption of aliphatic thinners across various end-use applications

Aliphatic Thinners Market Analysis

- The market is witnessing a preference for eco-friendly and low-VOC aliphatic thinners that comply with stringent environmental regulations, enhancing sustainability and reducing harmful emissions

- Rising demand from paints and coatings, adhesives, and aerosol industries is driving volume growth, particularly in regions with robust manufacturing and construction activities

- North America dominated the aliphatic thinners market with the largest revenue share in 2024, driven by rising industrial production, extensive use in paints and coatings, and growing demand from automotive and construction sectors

- Asia-Pacific region is expected to witness the highest growth rate in the global aliphatic thinners market, driven by rising demand from emerging economies, increasing construction and automotive activities, and growing adoption of sustainable and low-VOC solvent solutions

- The Mineral Spirit segment held the largest market revenue share in 2024, driven by its widespread application in paints, coatings, cleaning, and degreasing operations, offering effective solvency and lower toxicity compared to other solvents. Mineral spirits are preferred for their compatibility with various industrial and decorative coatings, contributing to high adoption across multiple sectors

Report Scope and Aliphatic Thinners Market Segmentation

|

Attributes |

Aliphatic Thinners Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Aliphatic Thinners Market Trends

Shift Toward Low-VOC And Eco-Friendly Solvents

- Growing adoption of low-VOC and environmentally compliant aliphatic thinners is transforming the market by enabling manufacturers to meet regulatory standards while maintaining product performance, reducing environmental footprint, and enhancing workplace safety. Companies are increasingly prioritizing sustainable solutions to align with global green building initiatives, circular economy practices, and evolving consumer preferences for eco-friendly products

- Increasing demand for faster-drying and high-performance thinners is driving the development of specialty solvent blends suitable for industrial, automotive, and decorative coatings. These formulations improve surface finish, reduce curing time, and enhance coating durability, providing manufacturers with a competitive edge in quality and efficiency

- Manufacturers are focusing on product innovation, including bio-based and renewable solvent alternatives, to enhance sustainability and reduce environmental impact. Research and development efforts are directed toward creating solvents that balance performance, cost-effectiveness, and regulatory compliance, enabling adoption in diverse industrial applications

- For instance, in 2023, several chemical companies in Europe and North America launched low-VOC mineral spirits and hexane-based thinners to meet green building and environmental certification requirements. These products also offer reduced odor, lower flammability, and improved handling safety, driving greater acceptance in professional and commercial markets

- While eco-friendly thinners are gaining traction, their adoption depends on regulatory support, production scalability, and industry acceptance across various applications. Market growth is also influenced by consumer education, availability of raw materials, and collaboration with coatings and adhesive manufacturers to ensure product compatibility

Aliphatic Thinners Market Dynamics

Driver

Increasing Demand From Paints, Coatings, And Industrial Applications

- Rising demand from paints, coatings, adhesives, aerosols, and rubber industries is driving growth of aliphatic thinners, which are used for viscosity adjustment, cleaning, and efficient solvent evaporation. Manufacturers are leveraging these solvents to enhance product quality, ensure uniform application, and meet high-performance standards across industrial and decorative applications

- Expansion of the automotive, construction, and industrial sectors is fueling thinners consumption due to the need for high-performance coatings and cleaning solutions. Growing vehicle production, urban infrastructure projects, and industrial plant expansion are directly contributing to increased solvent demand and consistent market growth

- Adoption of solvent-based formulations for enhanced product quality, drying time, and application efficiency supports market growth. Companies are investing in R&D to improve solvency, reduce odor, and ensure safety compliance while meeting stringent VOC emission limits, which enhances competitiveness and market penetration

- Government initiatives promoting industrial development and infrastructure projects in emerging economies are further boosting demand for thinners in construction, paints, and coatings. Policy support for sustainable industrial chemicals, green building standards, and export promotion programs drives higher consumption and adoption of compliant aliphatic thinners

- While industrial growth is driving demand, challenges such as regulatory restrictions on VOC emissions, solvent flammability, and environmental concerns must be addressed for sustained market growth. Manufacturers are focusing on safer handling procedures, worker training, and development of low-VOC alternatives to mitigate these challenges and ensure long-term market sustainability

Restraint/Challenge

Stringent Environmental Regulations And Health Concerns

- Increasing regulatory restrictions on VOC content and solvent emissions in paints, coatings, and adhesives limit the usage of traditional aliphatic thinners, especially in North America and Europe. Companies must navigate complex compliance standards, certifications, and reporting requirements, which can increase operational costs and limit product availability

- Health and safety concerns, including flammability, inhalation hazards, and skin irritation, restrict handling and storage, particularly in small-scale or unregulated operations. Ensuring proper ventilation, protective equipment, and safe transportation practices adds operational complexity and impacts overall adoption

- Fluctuating raw material prices, dependency on petroleum-derived feedstock, and supply chain disruptions pose challenges to consistent production and pricing. Volatility in crude oil markets, trade restrictions, and logistics constraints may affect availability, cost-effectiveness, and profit margins for aliphatic thinners manufacturers

- For instance, in 2023, several chemical manufacturers in Europe faced compliance challenges due to new VOC emission standards, impacting production schedules and market availability. This led to temporary supply shortages, increased costs for reformulation, and delays in meeting customer demand

- To overcome these challenges, manufacturers are investing in low-VOC, bio-based, and environmentally compliant thinners, along with robust safety measures and training programs. Collaborative efforts with regulatory bodies, technology adoption for emissions control, and product standardization initiatives are further supporting market resilience and adoption

Aliphatic Thinners Market Scope

The aliphatic thinners market is segmented on the basis of product type and application

- By Product Type

On the basis of product type, the market is segmented into Varnish Makers and Painters Naphtha, Mineral Spirit, Hexane, Heptane, and Others. The Mineral Spirit segment held the largest market revenue share in 2024, driven by its widespread application in paints, coatings, cleaning, and degreasing operations, offering effective solvency and lower toxicity compared to other solvents. Mineral spirits are preferred for their compatibility with various industrial and decorative coatings, contributing to high adoption across multiple sectors.

The Hexane segment is expected to witness the fastest growth rate from 2025 to 2032, driven by its high solvency power and increasing usage in adhesives, rubber, and polymer applications. Hexane’s efficiency in removing grease, oil, and resin residues makes it a preferred choice in industrial cleaning and degreasing, particularly in emerging economies with growing manufacturing activities.

- By Application

On the basis of application, the market is segmented into Paints and Coatings, Cleaning and Degreasing, Adhesives, Aerosols, Rubber and Polymer, and Others. The Paints and Coatings segment held the largest revenue share in 2024, driven by robust demand from industrial, automotive, and decorative coatings. Manufacturers rely on aliphatic thinners to adjust viscosity, improve application efficiency, and ensure uniform drying and finish quality.

The Cleaning and Degreasing segment is expected to witness the fastest growth from 2025 to 2032, propelled by increasing industrial cleaning requirements, rising focus on equipment maintenance, and expanding end-user industries such as automotive, aerospace, and manufacturing. The segment benefits from thinners’ excellent solvency and fast evaporation properties, enabling efficient cleaning and maintenance operations.

Aliphatic Thinners Market Regional Analysis

- North America dominated the aliphatic thinners market with the largest revenue share in 2024, driven by rising industrial production, extensive use in paints and coatings, and growing demand from automotive and construction sectors

- Manufacturers and end-users in the region prioritize high-performance, low-VOC thinners that comply with stringent environmental and safety regulations, supporting widespread adoption across industrial and commercial applications

- Strong R&D capabilities, advanced chemical manufacturing infrastructure, and high awareness of eco-friendly solvents are further contributing to market growth, establishing North America as a leading region for aliphatic thinners

U.S. Aliphatic Thinners Market Insight

The U.S. aliphatic thinners market captured the largest revenue share in North America in 2024, fueled by increasing demand from automotive, industrial coatings, and adhesives sectors. Companies are focusing on eco-friendly, low-VOC, and high-performance solvent formulations to meet regulatory compliance and customer expectations. The growing use of solvent-based coatings, combined with the need for faster-drying and efficient thinners, is driving adoption. Moreover, government initiatives promoting green chemicals and sustainable industrial practices are significantly supporting market expansion.

Europe Aliphatic Thinners Market Insight

The Europe aliphatic thinners market is expected to witness the fastest growth rate from 2025 to 2032, primarily driven by strict environmental regulations, increasing industrial activities, and growing adoption of eco-friendly and low-VOC solvents. Manufacturers are developing bio-based and renewable solvent alternatives to meet compliance standards. The region is seeing significant demand from automotive, paints and coatings, and construction sectors, with a strong focus on sustainable and safe chemical usage.

U.K. Aliphatic Thinners Market Insight

The U.K. aliphatic thinners market is expected to witness substantial growth from 2025 to 2032, driven by stringent VOC emission regulations, growing construction and automotive industries, and increased awareness of environmentally friendly products. Companies are increasingly adopting low-VOC, bio-based thinners to meet consumer and regulatory demands. Strong R&D capabilities and a preference for high-quality, safe solvent products are contributing to rising market penetration.

Germany Aliphatic Thinners Market Insight

The Germany aliphatic thinners market is expected to witness robust growth from 2025 to 2032, fueled by a mature industrial base, focus on sustainable chemical solutions, and stringent environmental regulations. Demand is primarily driven by paints, coatings, adhesives, and automotive sectors. Integration of low-VOC and eco-friendly thinners into industrial and decorative applications, along with strong innovation in bio-based solvents, is accelerating adoption across the country.

Asia-Pacific Aliphatic Thinners Market Insight

The Asia-Pacific aliphatic thinners market is expected to witness the fastest growth rate from 2025 to 2032, driven by rapid industrialization, urbanization, and increasing demand from automotive, construction, and manufacturing sectors in countries such as China, India, and Japan. Rising export-oriented industrial production, expansion of coatings and adhesive manufacturing, and growing awareness of eco-friendly solvents are further supporting market growth. The region’s cost advantages and availability of raw materials are also contributing to higher adoption rates.

Japan Aliphatic Thinners Market Insight

The Japan aliphatic thinners market is expected to witness strong growth from 2025 to 2032 due to the country’s advanced industrial base, high-quality coating and adhesives production, and focus on sustainable chemical solutions. Demand is driven by automotive, industrial coatings, and electronics sectors. Adoption of low-VOC and bio-based thinners, combined with technological innovation in solvent formulations, is enhancing efficiency, safety, and regulatory compliance across industries.

China Aliphatic Thinners Market Insight

The China aliphatic thinners market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rapid industrial growth, expanding automotive and construction sectors, and increasing demand for high-performance solvents. Domestic manufacturers are actively producing eco-friendly, low-VOC, and bio-based aliphatic thinners to meet both regulatory requirements and consumer preferences. Government initiatives promoting green chemicals, industrial modernization, and export-oriented production further support market expansion.

Aliphatic Thinners Market Share

The Aliphatic Thinners industry is primarily led by well-established companies, including:

- BASF SE (Germany)

- Calumet Specialty Products Partners, L.P. (U.S.)

- Exxon Mobil Corporation (U.S.)

- Gadiv Petrochemical Industries Ltd. (Israel)

- Ganga Rasayanie (P) Ltd (India)

- Industries Gotham Inc (Les) (U.S.)

- Gulf Chemical & Industrial Oils (U.A.E.)

- HCS Group GmBH (Germany)

- Heritage-Crystal Clean, Inc (U.S.)

- Honeywell International Inc. (U.S.)

- Hunt Refining Company (U.S.)

- Kandla Energy & Chemical Limited (India)

- The NOCO Company (U.S.)

- Pon Pure Chemicals (India)

- Rb Products, Inc. (U.S.)

- Recochem Inc. (Canada)

- Royal Dutch Shell Plc (U.K.)

- SK Global Chemical Co. Ltd. (South Korea)

- Tradenote (U.S.)

- Solvchem (India)

- W.M. Barr (U.S.)

- LyondellBasell Industries Holdings B.V (Netherlands)

- Phillips (U.K.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Aliphatic Thinners Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Aliphatic Thinners Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Aliphatic Thinners Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.