Global Alpers Disease Treatment Market

Market Size in USD Billion

USD

1.44 Billion

USD

1.94 Billion

2025

2033

USD

1.44 Billion

USD

1.94 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.44 Billion | |

| USD 1.94 Billion | |

| % | |

|

Alpers Disease Treatment Market Size

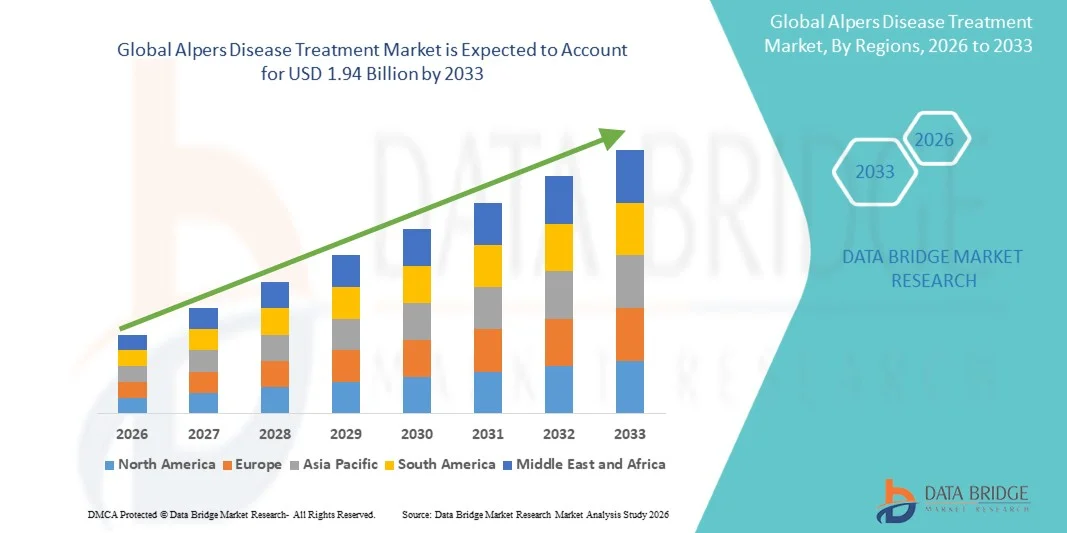

- The global alpers disease treatment market size was valued at USD 1.44 billion in 2025 and is expected to reach USD 1.94 billion by 2033, at a CAGR of 3.80% during the forecast period

- The market growth is largely fueled by the rising incidence of mitochondrial disorders, advancements in genetic testing technologies, and increasing awareness of rare neurological diseases, which are improving early diagnosis and treatment initiation for Alpers Disease across clinical settings

- Furthermore, growing research efforts aimed at understanding POLG gene mutations, expanding access to supportive therapies, and increased clinical focus on managing progressive neurological and hepatic symptoms are accelerating the uptake of Alpers Disease Treatment solutions, thereby significantly boosting the industry’s growth

Alpers Disease Treatment Market Analysis

- Alpers Disease Treatment, involving supportive neurological care, seizure management, and mitochondrial-targeted therapies, is increasingly vital within pediatric and rare disease healthcare systems due to rising awareness, improved diagnostic capabilities, and expanding access to genetic testing across both developed and developing regions

- The escalating demand for Alpers Disease Treatment is primarily fueled by the growing prevalence of POLG-related disorders, early diagnosis through advanced molecular techniques, and a rising clinical emphasis on timely intervention to slow neurological decline and improve patient outcomes

- North America dominated the alpers disease treatment market with the largest revenue share of 36.7% in 2025, supported by advanced healthcare infrastructure, high diagnostic accuracy, increased adoption of genetic sequencing, and strong availability of specialized neurology and mitochondrial disorder centers. The U.S. experienced substantial growth due to early disease recognition, better access to pediatric neurologists, and increased research funding for rare neurodegenerative conditions

- Asia-Pacific is expected to be the fastest growing region in the alpers disease treatment market during the forecast period, driven by rising healthcare expenditure, improving access to rare disease diagnostics, growing awareness among clinicians, and ongoing investments in pediatric neurology across countries such as India, China, and Japan

- The Childhood segment dominated the largest market revenue share of 54.3% in 2025, as Alpers Disease most commonly manifests between ages 2 and 10. High diagnostic activity in pediatric neurology centers supports segment dominance

Report Scope and Alpers Disease Treatment Market Segmentation

|

Attributes |

Alpers Disease Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Alpers Disease Treatment Market Trends

“Enhanced Advancements Through AI-Enabled Clinical Tools and Precision Medicine Integration”

- A significant and accelerating trend in the global alpers disease treatment market is the deepening integration of artificial intelligence (AI), precision-genomics platforms, and advanced clinical decision-support systems aimed at improving early diagnosis and personalized treatment planning for this rare mitochondrial disorder. This fusion of technologies is significantly enhancing clinician capability, monitoring accuracy, and patient management efficiency

- For instance, AI-driven genomic interpretation tools used in leading neurometabolic research centers can now analyze POLG gene variations more rapidly and accurately, enabling clinicians to identify pathogenic mutations associated with Alpers disease with greater confidence. Similarly, digital neurology platforms that use machine-learning algorithms can assist in tracking seizure patterns and neurological decline, offering more informed and timely clinical interventions

- AI integration in Alpers disease management is enabling features such as automated detection of metabolic abnormalities, prediction of disease progression, and the ability to generate more intelligent clinical alerts based on individual patient data. For example, several research-grade neuro-analytics tools utilize AI to improve EEG interpretation accuracy over time and can send intelligent alerts if unusual neurological activity is detected. Furthermore, advanced digital monitoring systems offer clinicians the ease of remote patient surveillance, allowing them to adjust medications or supportive therapies through data-driven insights

- The seamless integration of AI-supported platforms with broader hospital information systems facilitates centralized control over various aspects of rare-disease management. Through a single interface, clinicians can analyze genetic reports, metabolic markers, imaging results, and neurological data, creating a unified and highly automated clinical workflow for complex neuro-metabolic disorders such as Alpers disease

- This trend toward more intelligent, intuitive, and interconnected diagnostic-treatment systems is fundamentally reshaping expectations for rare-disease care. Consequently, companies and research institutions are investing in AI-powered genomic sequencing tools and digital neurology platforms with capabilities such as automated mitochondrial-function assessment and advanced patient monitoring dashboards

- The demand for solutions that offer seamless AI-powered diagnostic support and precision-medicine alignment is growing rapidly across both academic medical centers and specialized neurometabolic clinics, as clinicians increasingly prioritize diagnostic accuracy, early detection, and comprehensive long-term disease management

Alpers Disease Treatment Market Dynamics

Driver

“Growing Need Due to Rising Disease Awareness and Advancements in Genetic Testing”

- The increasing recognition of mitochondrial disorders among healthcare providers and families, coupled with rapid advancements in genetic and metabolic diagnostic technologies, is a significant driver of the rising demand for improved Alpers Disease Treatment solutions

- For instance, in April 2025, several clinical genetics laboratories announced advancements in next-generation sequencing (NGS) workflows designed to enhance detection of POLG mutations—one of the primary causes of Alpers disease. Such strategic progress by key institutions is expected to drive the Alpers Disease Treatment industry growth in the forecast period

- As clinicians become more aware of the overlapping symptoms of mitochondrial disorders and the importance of early identification, demand for more accurate diagnostic tools and supportive therapies continues to rise. Modern approaches offer detailed mitochondrial function analysis, improved seizure management, and enhanced supportive neurological care—representing a significant upgrade over previous limited treatment options

- Furthermore, the growing emphasis on precision medicine, coupled with the development of newborn screening initiatives and metabolic testing protocols, is making Alpers disease diagnosis more accessible within specialized care settings. This evolution supports earlier intervention, informed treatment decisions, and improved patient outcomes

- The availability of advanced neuro-monitoring tools, targeted nutritional therapies, mitochondrial-support regimens, and specialized anticonvulsant protocols are key factors propelling the adoption of Alpers disease treatment approaches across pediatric neurology and rare-disease clinics. Increasing awareness among caregivers and improved referral pathways further contribute to market growth

- The trend toward personalized medicine and the increasing availability of user-friendly genetic testing solutions also supports expansion of the Alpers Disease Treatment market, particularly in developed healthcare systems that prioritize early disease detection and long-term patient monitoring

Restraint/Challenge

“Concerns Regarding Limited Therapeutic Options and High Diagnostic Costs”

- The limited availability of approved therapies for Alpers Disease, combined with the high cost of diagnostic testing, poses a significant challenge to broader market growth. The complex nature of the disease, including its genetic heterogeneity, makes the development of effective treatment regimens difficult, which raises concerns among clinicians and patients regarding timely and adequate care

- For instance, high costs associated with molecular genetic testing and specialized laboratory diagnostics have made some patients and healthcare providers hesitant to pursue early or comprehensive disease management, particularly in developing regions or underfunded healthcare systems

- Addressing these concerns through increased investment in research and development of targeted therapies, broader access to affordable diagnostic solutions, and the integration of genetic counseling services is crucial for improving patient outcomes. Additionally, insurance coverage and government reimbursement programs play a vital role in mitigating financial barriers for patients seeking care

- While efforts are being made to expand therapeutic pipelines and reduce diagnostic costs, the scarcity of disease-modifying treatments and specialized testing options continues to limit widespread adoption of comprehensive management approaches

- Overcoming these challenges through the development of cost-effective diagnostic technologies, expanded clinical trials for novel therapies, and educational programs for healthcare providers and patients will be essential for sustained market growth and improved disease management

Alpers Disease Treatment Market Scope

The market is segmented on the basis of treatment, diagnosis, dosage, route of administration, demographic, symptoms, end-users, and distribution channel.

• By Treatment

On the basis of treatment, the Alpers Disease Treatment market is segmented into Anticonvulsant Drugs, Speech Therapy, Physical Therapy, Occupational Therapy, and Others. The Anticonvulsant Drugs segment dominated the largest market revenue share of 46.8% in 2025, driven by the critical need to control frequent and severe seizures associated with Alpers Disease. As seizures remain one of the earliest and most debilitating clinical symptoms, anticonvulsants are typically the first-line therapy prescribed across hospitals and specialty neurology clinics. Increasing availability of advanced antiepileptic drugs and improved dosing formulations enhances physician preference. The segment benefits from rising awareness of early symptom management among caregivers. Expanded clinical guidelines for pediatric seizure control further support adoption. Pharmaceutical companies are investing in novel antiepileptic compounds tailored for mitochondrial disorders, strengthening long-term segment positioning. High prescription rates in both developed and emerging regions contribute substantially to volume demand. The rise in early diagnostic rates also leads to earlier initiation of anticonvulsant therapy. Improved tolerability profiles of newer drugs enhance patient adherence. Ongoing research collaborations between neurology specialists and mitochondrial disease foundations further reinforce adoption. Overall, this segment remains foundational to Alpers Disease management.

The Physical Therapy segment is expected to witness the fastest CAGR of 21.9% from 2026 to 2033, driven by growing emphasis on improving motor function, managing spasticity, and delaying disability progression. As Alpers Disease leads to rapid neuromuscular degeneration, physical therapy plays a crucial role in maintaining mobility and reducing muscle stiffness. Increasing recommendations from neurologists for integrated rehabilitation plans boosts segment growth. Pediatric and adolescent patient populations benefit significantly from early physiotherapeutic interventions. Expansion of rehabilitation centers and adoption of home-based therapy programs enhance accessibility. Technological advancements such as robotic-assisted therapy and neuromuscular stimulation devices support faster growth. NGOs and rare disease support groups promote therapy awareness. Insurance coverage expansion for rehabilitative care also encourages uptake. Rising demand for personalized physiotherapy sessions strengthens the market outlook. Caregiver education programs further support therapy continuation. Growing global focus on non-pharmacological supportive care positions physical therapy as a high-growth segment.

• By Diagnosis

On the basis of diagnosis, the market is segmented into Laboratory Tests, Molecular Genetic Testing, Electroencephalography (EEG), and Others. The Molecular Genetic Testing segment dominated the largest market revenue share of 48.2% in 2025, owing to its indispensable role in confirming POLG gene mutations responsible for Alpers Disease. Genetic testing provides high diagnostic accuracy, enabling early and definitive identification of mitochondrial dysfunction. Increasing adoption in tertiary healthcare centers strengthens demand. Rising awareness among neurologists and pediatricians regarding early genetic screening enhances diagnostic rates. Government-supported rare disease genetic testing initiatives also fuel expansion. Advanced sequencing platforms and reduced test costs increase accessibility. Families with hereditary mitochondrial disorders opt for early testing, boosting uptake. Integration of next-generation sequencing (NGS) improves sensitivity and turnaround times. Research institutions rely heavily on molecular diagnostics for case documentation. Growing availability of testing kits across Asia-Pacific and Latin America widens market reach. Genetic counseling services further complement segment strength.

The Electroencephalography (EEG) segment is expected to witness the fastest CAGR of 20.6% from 2026 to 2033, driven by its essential role in identifying seizure patterns and cerebral deterioration in Alpers patients. EEG remains a frontline diagnostic tool in emergency and neurology care centers. Increasing incidence of recurrent seizures drives demand for repeated EEG monitoring. Technological advancements such as portable EEG systems boost usage in home-care and outpatient settings. Hospitals increasingly integrate EEG into standard evaluation for pediatric seizures. Rising adoption of continuous EEG monitoring in critical care settings enhances growth. Educational programs for neurologists promote advanced EEG interpretation. Cost-effective EEG solutions in developing countries widen access. Integration with tele-neurology platforms accelerates diagnostic utilization. Increased awareness among caregivers leads to timely EEG assessment. Strong clinical relevance ensures sustained segment expansion.

• By Dosage

On the basis of dosage, the market is segmented into Tablet, Injection, and Others. The Tablet segment dominated the largest market revenue share of 44.7% in 2025, due to widespread use of oral anticonvulsants and supportive medications for long-term management. Tablets are easy to administer in home settings, enhancing patient adherence. Pediatric-friendly formulations such as dispersible and low-dose tablets boost adoption. Hospitals and clinics frequently prescribe oral drugs for chronic seizure control. Cost-effectiveness and wider availability in pharmacies sustain segment leadership. Oral medications have standardized dosing protocols, increasing clinician preference. Pharmaceutical companies produce a wide variety of oral therapies suitable for mitochondrial disorders. The dominance is also supported by high prescribing rates of adjunct therapies such as vitamins, co-factors, and anti-inflammatory agents. Outpatient treatment models further strengthen the segment. Availability through retail and online pharmacies ensures consistent supply. Overall, oral dosage remains the most practical and preferred route for long-term disease management.

The Injection segment is expected to witness the fastest CAGR of 19.8% from 2026 to 2033, due to the need for rapid seizure control and management of acute neurological decline in hospitalized patients. Injections provide immediate therapeutic action, making them essential during severe episodes. Hospitals increasingly rely on IV anticonvulsants for emergency stabilization. The segment benefits from improving pediatric critical care infrastructure. Rising use of intravenous nutrient and metabolic support in advanced disease stages boosts demand. Growing recommendations for hospital-based administration in critical mitochondrial disorders support expansion. Development of safer injectable formulations enhances clinician confidence. Increased availability of IV medications in tertiary care facilities strengthens growth. Emergency neurology programs in emerging markets improve accessibility. NGO-supported programs for rare diseases often provide injectable therapies, further supporting uptake.

• By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Intravenous, and Others. The Oral segment accounted for the largest market revenue share of 49.1% in 2025, owing to its convenience, non-invasiveness, and suitability for long-term disease management. Oral therapies are commonly used for seizure suppression and symptom relief across all age groups. High patient compliance supports the segment’s dominance. Hospitals and clinics routinely prescribe oral treatments as part of home-care plans. Availability of multiple generic options enhances affordability. Pediatric formulations improve adaptability for younger patients. Oral therapy is often recommended for early-stage symptom management. Strong distribution networks ensure consistent availability. Growing awareness of self-administered care among caregivers supports adoption. Clinical guidelines emphasize oral route for maintenance therapy. Rising outpatient visits contribute significantly to revenue.

The Intravenous segment is expected to witness the fastest CAGR of 20.4% from 2026 to 2033, driven by increasing use in managing severe neurological deterioration. IV therapies deliver rapid therapeutic action, making them essential during emergencies. Hospitals prefer IV formulations during acute seizures or liver failure episodes. Technological improvements in infusion therapy enhance safety. Expansion of critical care units boosts demand. Pediatric and adolescent patients with rapid neurological decline rely heavily on IV therapies. Availability of metabolic and nutritional IV support expands clinical utility. Government and private programs improving hospital infrastructure accelerate growth. IV therapy remains a core component of advanced-stage disease management. Increasing clinician adoption in specialized neurology centers supports high CAGR.

• By Demographic

On the basis of demographic, the market is segmented into Adult, Adolescent, Childhood, and Infancy. The Childhood segment dominated the largest market revenue share of 54.3% in 2025, as Alpers Disease most commonly manifests between ages 2 and 10. High diagnostic activity in pediatric neurology centers supports segment dominance. Parents seek early medical attention due to rapid symptom progression. Genetic counseling programs emphasize testing in children. Hospitals prioritize pediatric seizure management, reinforcing demand. Supportive therapies and rehabilitation programs are widely provided to children. Pediatric specialists frequently prescribe long-term anticonvulsant therapy. Increased awareness among caregivers boosts early diagnosis. NGOs and rare disease foundations provide strong support for pediatric cases. Research initiatives focus heavily on childhood-onset mitochondrial diseases. Clinical guidelines are centered on pediatric manifestations.

The Infancy segment is expected to witness the fastest CAGR of 22.4% from 2026 to 2033, owing to increasing recognition of early-onset Alpers variants. Neonatal screening advancements contribute to earlier detection. Infants often exhibit rapid neurological decline, necessitating immediate clinical intervention. Hospitals increasingly perform genetic testing in newborns with unexplained seizures. High vulnerability of infants accelerates specialist referrals. Expansion of neonatal care units boosts therapeutic adoption. Pediatric neurologists emphasize early supportive care in infants. Increasing parental awareness drives early diagnosis. NGOs support early intervention programs in high-risk populations. Overall, rising focus on early detection and care drives fastest growth in this segment.

• By Symptoms

On the basis of symptoms, the market is segmented into Headache, Dementia, Seizures, Spasticity, Liver Dysfunction, Blindness, Cerebral Degeneration, and Others. The Seizures segment dominated the largest market revenue share of 51.6% in 2025, given that recurrent seizures are the primary and earliest clinical manifestation. Hospitals and clinics prioritize seizure management as the cornerstone of therapy. High frequency of emergency cases boosts revenue. Pediatric and adolescent patients contribute significantly to demand. Clinical protocols mandate immediate anticonvulsant treatment. Caregivers seek rapid medical support during seizure episodes. Increased diagnostic testing for seizure origin enhances adoption of therapy. Pharmaceutical advancements further reinforce dominance. High rates of hospital admissions due to status epilepticus strengthen segment leadership. Seizure monitoring technologies complement treatment strategies. Education programs raise awareness about early symptom recognition.

The Liver Dysfunction segment is expected to witness the fastest CAGR of 21.7% from 2026 to 2033, driven by rising incidence of POLG-related hepatic failure. Hospitals increasingly monitor liver function in Alpers patients. Early detection programs emphasize routine liver enzyme testing. Critical patients require intensive care and metabolic treatments. IV therapies and hospital stays increase segment revenue. Genetic counseling promotes awareness of hepatic risks. Therapies supporting liver metabolism gain traction. Pediatric patients with progressive liver damage require continuous intervention. Emergency care infrastructure supports segment expansion. The severity of liver deterioration contributes to rapid clinical intervention demand.

• By End-Users

On the basis of end-users, the market is segmented into Clinic, Hospital, and Others. The Hospital segment accounted for the largest market revenue share of 55.2% in 2025, driven by the need for specialized pediatric neurology, ICU support, genetic testing, and seizure management. Hospitals manage acute and chronic stages effectively. Availability of advanced EEG, MRI, and genetic testing boosts diagnostic precision. Multidisciplinary teams support complex symptom management. Hospital pharmacies ensure continuous drug access. Pediatric ICUs specialize in managing rapid neurological decline. Rehabilitation units within hospitals offer integrated care. Government programs improve rare disease support in hospitals. Research collaborations strengthen clinical expertise. Overall, hospitals remain the primary treatment hub for Alpers Disease.

The Clinic segment is expected to witness the fastest CAGR of 20.9% from 2026 to 2033, due to rising outpatient visits for early symptoms, follow-up management, and supportive care. Clinics provide accessible pediatric neurology services. Growing awareness encourages families to seek early consultations. Expansion of diagnostic capabilities in private clinics boosts growth. Outpatient therapy programs increase clinic visits. Lower cost compared to hospitals attracts more families. Home-care coordination services enhance adoption. Early-stage cases are often managed in clinics before hospitalization becomes necessary.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Hospital Pharmacy segment dominated the largest market revenue share of 51.8% in 2025, due to direct access to critical therapies prescribed during inpatient and emergency care. Hospitals stock a wide range of IV and oral therapies essential for Alpers management. Pediatric and neurology centers rely heavily on hospital pharmacies for timely drug availability. Integration with inpatient care ensures seamless treatment. Complex cases requiring specialized medications support dominance. Insurance coverage for hospital-based procurement boosts patient access. Hospital pharmacies maintain strict drug storage protocols, enhancing reliability. Government-funded rare disease drug programs are often distributed through hospital systems. High-frequency prescriptions for anticonvulsants sustain demand.

The Online Pharmacy segment is expected to witness the fastest CAGR of 23.4% from 2026 to 2033, driven by increased digital adoption and convenience. Families managing chronic Alpers cases prefer home delivery of long-term medications. Telemedicine integration boosts online prescription fulfillment. Online platforms offer cost comparison options, increasing affordability. Patient adherence improves with subscription-based delivery models. Expansion of e-health infrastructure in Asia-Pacific accelerates growth. Modern caregivers prefer digital ordering for consistent medication supply. Regulatory improvements ensure secure online dispensing of neurological drugs.

Alpers Disease Treatment Market Regional Analysis

- North America dominated the alpers disease treatment market with the largest revenue share of 36.7% in 2025, driven by advanced healthcare infrastructure, high diagnostic accuracy, increased adoption of genetic sequencing technologies, and strong availability of specialized neurology and mitochondrial disorder centers

- Consumers (patients and families) in the region benefit from early diagnosis, improved access to pediatric neurologists, and wide availability of multidisciplinary care programs, which collectively contribute to higher treatment adoption and better disease management outcomes

- This strong regional presence is further supported by extensive research funding, high awareness of rare neurodegenerative disorders, and continuous development of advanced diagnostic tools, making North America a leading hub for Alpers disease treatment and research

U.S. Alpers Disease Treatment Market Insight

The U.S. alpers disease treatment market accounted for 81% of the North American share in 2025, supported by early disease recognition, a strong network of children’s hospitals, and widespread adoption of molecular genetic testing. Growing research investments in mitochondrial disorders, availability of advanced anticonvulsant therapies, and increased participation in clinical studies further drive market expansion. The country also benefits from strong collaborations between research institutions and biotechnology companies working on novel neuroprotective and mitochondrial-targeted therapies.

Europe Alpers Disease Treatment Market Insight

The Europe alpers disease treatment market is projected to grow at a substantial CAGR during the forecast period, driven by rising awareness of mitochondrial disorders, improvement in early diagnostic programs, and increasing adoption of genetic testing technologies. Many European countries have established rare-disease registries and specialized neurology centers, supporting better patient identification and care pathways. Growth is strong across Germany, the U.K., France, Spain, and Italy, where advancements in pediatric neurology and rare-disease funding are accelerating treatment access.

U.K. Alpers Disease Treatment Market Insight

The U.K. alpers disease treatment market is expected to expand at a noteworthy CAGR due to government-supported rare-disease initiatives, improved access to genomic sequencing through national health programs, and rising clinician awareness of early symptoms. The country's strong clinical research ecosystem and increasing participation in rare-disease trials continue to strengthen market growth. Additionally, improvements in pediatric neurology services and multidisciplinary care pathways support early diagnosis and better disease management outcomes.

Germany Alpers Disease Treatment Market Insight

The Germany alpers disease treatment market is projected to grow significantly, supported by high adoption of molecular genetic testing, widespread access to advanced pediatric and neurology care, and strong emphasis on medical innovation. Germany’s well-developed healthcare infrastructure, along with its leadership in mitochondrial research and rare-disease clinical trials, contributes to growing treatment demand. A strong preference for precision diagnostics and early detection also enhances market penetration.

Asia-Pacific Alpers Disease Treatment Market Insight

The Asia-Pacific Alpers Disease Treatment market is expected to grow at the fastest CAGR of 24% from 2026 to 2033, driven by rising healthcare expenditure, growing awareness of pediatric neurology disorders, and improving access to specialized diagnostics such as EEG, MRI, and genetic sequencing. Countries like China, Japan, and India are increasing investments in rare-disease programs, which is expanding treatment availability. Government-led digital health initiatives, along with expanding hospital infrastructure, are also making advanced diagnostics more accessible.

Japan Alpers Disease Treatment Market Insight

The Japan Alpers Disease Treatment market is gaining strong momentum due to the country’s technological leadership in genetic diagnostics, high clinical awareness of mitochondrial disorders, and advanced pediatric neurology ecosystem. Early adoption of next-generation sequencing, robust hospital infrastructure, and strong emphasis on research surrounding neurodegenerative diseases are driving demand. Japan’s aging population and rising focus on advanced neurological care also support long-term market growth.

China Alpers Disease Treatment Market Insight

The China alpers disease treatment market held the largest share within the Asia-Pacific region in 2025, supported by rapid expansion of healthcare infrastructure, growing adoption of genetic testing, and increasing awareness of pediatric neurological disorders. China’s large population, expanding middle class, and strengthening hospital networks contribute to growing diagnosis rates. Government investments in rare-disease management, along with strong growth in domestic biotechnology companies, play a major role in advancing treatment availability.

Alpers Disease Treatment Market Share

The Alpers Disease Treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Roche Holding AG (Switzerland)

- GlaxoSmithKline plc (U.K.)

- Novartis AG (Switzerland)

- Sanofi S.A. (France)

- AbbVie Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- AstraZeneca plc (U.K.)

- Johnson & Johnson (U.S.)

- Merck & Co., Inc. (U.S.)

- Biogen Inc. (U.S.)

- Takeda Pharmaceutical Company Ltd. (Japan)

- Bayer AG (Germany)

- Teva Pharmaceutical Industries Ltd. (Israel)

- UCB Pharma (Belgium)

- Amgen Inc. (U.S.)

- Ipsen Pharma (France)

- Vertex Pharmaceuticals (U.S.)

- Alexion Pharmaceuticals (U.S.)

- Horizon Therapeutics (Ireland)

Latest Developments in Global Alpers Disease Treatment Market

- In May 2023, a neuropathology study published in Acta Neuropathologica Communications characterized reactive astrocytic pathology in post-mortem brain tissue of Alpers syndrome patients — showing decreased abundance of mitochondrial oxidative-phosphorylation proteins and altered expression of key astrocytic proteins (Kir4.1, AQP4, glutamine synthetase), implicating astrocyte dysfunction (not only neuronal damage) in disease pathogenesis

- In January 2024, researchers published in International Journal of Biological Sciences that using patient-derived induced pluripotent stem cells (iPSCs) differentiated into cortical organoids, they replicated mitochondrial DNA depletion, complex I deficiency, and neuronal loss typical of Alpers disease. Crucially, they found that supplementation with the NAD⁺ precursor Nicotinamide Riboside (NR) significantly ameliorated mitochondrial defects and reduced neuronal loss — identifying NR as a potential therapeutic candidate

- In April 2025, a biotech company announced that its small-molecule therapy PX578 (or associated compound PZL‑A), designed to restore function of mutant mitochondrial DNA polymerase γ (POLG) enzymes, had entered Phase 1 clinical development. This represents the first-ever disease-modifying therapeutic candidate targeting the underlying POLG mutation mechanism implicated in Alpers disease

- In May 2025, a research article published in Acta Neuropathologica described novel insights into mechanisms of cerebellar degeneration in pediatric and adult mitochondrial diseases (including POLG-related disorders), shedding light on neurodegenerative pathways relevant to Alpers disease — potentially informing future therapeutic strategies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.