Global Amblyopia Drugs Market

Market Size in USD Billion

USD

4.13 Billion

USD

5.43 Billion

2025

2033

USD

4.13 Billion

USD

5.43 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.13 Billion | |

| USD 5.43 Billion | |

| % | |

|

Amblyopia Drugs Market Size

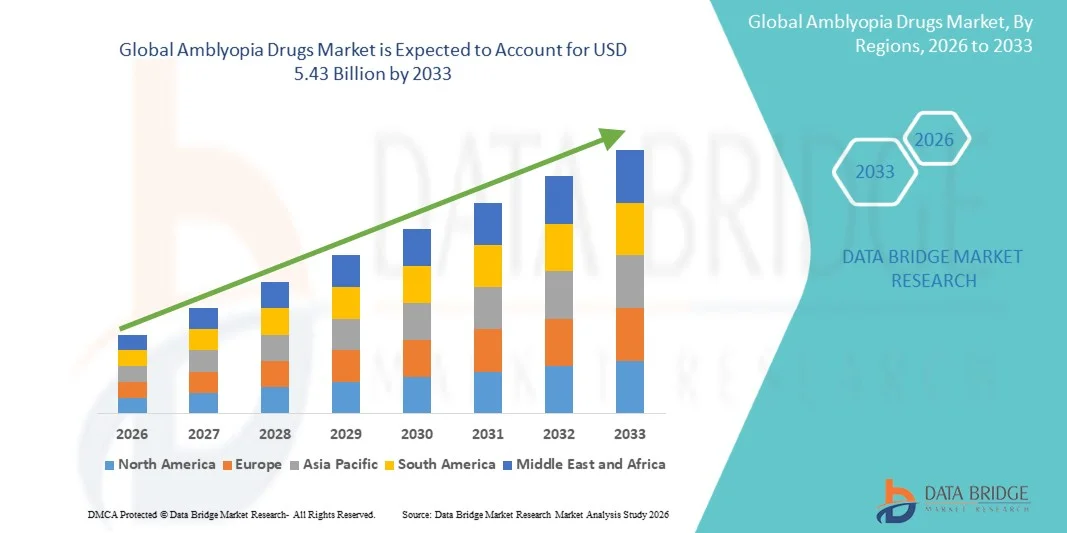

- The global amblyopia drugs market size was valued at USD 4.13 billion in 2025and is expected to reach USD 5.43 billion by 2033, at a CAGR of 3.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of amblyopia (lazy eye) across pediatric populations, along with rising awareness regarding early diagnosis and pharmacological interventions, leading to improved treatment adoption in ophthalmic care settings

- Furthermore, growing demand for non-invasive and adjunct drug therapies to complement traditional treatments such as patching and vision therapy is establishing amblyopia drugs as an important component of pediatric vision care. These converging factors are accelerating the uptake of amblyopia pharmacological solutions, thereby significantly boosting the industry's growth

Amblyopia Drugs Market Analysis

- Amblyopia drugs, primarily consisting of pharmacological therapies such as atropine eye drops and emerging neuro-visual and dopaminergic agents, are increasingly being integrated into pediatric ophthalmology practice as important adjuncts to conventional treatments such as patching and vision therapy due to their ability to improve treatment adherence and support visual cortex development in children with lazy eye

- The escalating demand for amblyopia drugs is primarily fueled by the rising global incidence of pediatric vision disorders, increasing awareness of early eye screening and intervention programs, and a growing clinical shift toward non-invasive, pharmacologically supported treatment approaches that enhance visual recovery outcomes

- North America dominated the amblyopia drugs market with the largest revenue share of 39.4% in 2025, supported by advanced ophthalmic care infrastructure, strong adoption of pediatric vision screening programs, and early uptake of novel pharmacological therapies, with the U.S. showing significant growth driven by active clinical research and widespread use of atropine-based treatments

- Asia-Pacific is expected to be the fastest growing region in the amblyopia drugs market during the forecast period due to a large pediatric population base, improving access to eye care services, rising healthcare expenditure, and increasing awareness regarding early diagnosis and treatment of vision impairment in countries such as China and India

- Atropine segment dominated the amblyopia drugs market with a market share of 44.1% in 2025, driven by its proven clinical efficacy, ease of administration, and increasing preference among clinicians as an alternative or adjunct to patching therapy for improving treatment compliance in pediatric patients

Report Scope and Amblyopia Drugs Market Segmentation

|

Attributes |

Amblyopia Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Development of digital therapeutics and gamified vision-training platforms · Expansion of prescription-based home therapy models |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Amblyopia Drugs Market Trends

“Shift Toward Digital-Pharmacological Combination Therapies”

- A significant and accelerating trend in the global amblyopia drugs market is the integration of pharmacological treatments such as atropine with digital vision therapy platforms and pediatric neuro-visual training tools to improve treatment adherence and visual recovery outcomes in children

- For instance, emerging atropine-based treatment regimens are increasingly being paired with app-based vision training programs that guide children through structured eye exercises while monitoring progress in real time under clinician supervision

- Integration of adjunct drug therapy in amblyopia enables improved modulation of visual cortex adaptation, with low-dose atropine showing enhanced effectiveness when combined with structured vision stimulation protocols in pediatric patients

- The growing use of tele-ophthalmology platforms is facilitating centralized monitoring of amblyopia drug response, allowing clinicians to remotely adjust dosage and therapy plans based on patient compliance and visual improvement trends

- Increasing research focus on neuroplasticity-targeting drugs is driving innovation in next-generation amblyopia therapies aimed at improving binocular vision recovery beyond conventional treatment windows

- Rising adoption of personalized treatment algorithms based on patient age, severity, and response patterns is enabling more tailored amblyopia drug regimens for improved clinical outcomes

Amblyopia Drugs Market Dynamics

Driver

“Rising Early Screening and Expanding Pediatric Eye Care Programs”

- The increasing global emphasis on early childhood vision screening programs and expanding pediatric ophthalmology infrastructure is a key driver accelerating the demand for amblyopia drugs across both developed and emerging healthcare markets

- For instance, national school-based vision screening initiatives are increasingly identifying amblyopia at earlier stages, leading to higher prescription rates of pharmacological therapies such as atropine eye drops alongside traditional patching methods

- Growing clinical recognition of the importance of early intervention in preventing long-term visual impairment is encouraging physicians to adopt drug-based adjunct therapies to enhance treatment success rates in young patients

- Furthermore, rising healthcare investments in pediatric eye care services and improved access to ophthalmic specialists are supporting wider adoption of amblyopia drug therapies in outpatient and clinical settings

- The increasing preference for non-invasive and compliance-friendly treatment options among parents and clinicians is further driving the integration of drug-based approaches into standard amblyopia management protocols

- Expanding insurance coverage and reimbursement support for pediatric vision treatments in several countries is further improving affordability and access to amblyopia drug therapies

Restraint/Challenge

“Limited Long-Term Efficacy Evidence and Treatment Compliance Issues”

- Concerns regarding limited long-term clinical evidence on sustained efficacy of amblyopia drugs, particularly in severe cases, pose a significant challenge to broader adoption among ophthalmologists and healthcare providers

- For instance, variability in patient response to atropine therapy and uncertainty about long-term visual stability after discontinuation of drug treatment have led to cautious prescribing practices in some clinical settings

- Treatment compliance issues, especially among young pediatric patients, remain a key challenge as prolonged use of eye drops or combination therapies may lead to inconsistent adherence and reduced therapeutic outcomes

- In addition, mild side effects such as light sensitivity and near vision blur associated with atropine use can discourage continuous treatment adherence among children and caregivers

- Lack of standardized global treatment protocols for amblyopia drug therapy creates variability in prescribing practices and limits consistent clinical adoption across regions

- High dependence on caregiver supervision for proper drug administration further increases the risk of missed doses and suboptimal treatment effectiveness

Amblyopia Drugs Market Scope

The market is segmented on the basis of type, drugs, end user, and distribution channel.

- By Type

On the basis of type, the amblyopia drugs market is segmented into strabismic amblyopia, refractive amblyopia, deprivation amblyopia, and others. The refractive amblyopia segment dominated the market with the largest revenue share of 41.6% in 2025, driven by its high prevalence globally, particularly in children with uncorrected refractive errors such as hyperopia and anisometropia. This segment benefits from early detection through school screening programs, where pharmacological therapies such as atropine are increasingly used as adjunct treatment. The clinical preference for combining refractive correction with drug therapy to improve visual acuity outcomes further strengthens its dominance. In addition, better awareness among parents regarding corrective eye care is supporting sustained demand for treatment in this category. Expanding pediatric ophthalmology services in urban and semi-urban regions is further reinforcing its leading position in the market.

The strabismic amblyopia segment is expected to witness the fastest growth rate of 19.8% from 2026 to 2033, driven by rising incidence of ocular misalignment in pediatric populations and increasing early diagnosis through advanced eye screening technologies. This segment is gaining traction as clinicians increasingly adopt pharmacological therapies alongside corrective surgery and vision therapy to enhance binocular vision recovery. Growing awareness regarding long-term complications of untreated strabismus is encouraging early therapeutic intervention. Furthermore, advancements in neuro-visual drugs aimed at improving cortical adaptation are expanding treatment possibilities. Increasing availability of specialized pediatric ophthalmic care in emerging economies is also contributing to rapid growth in this segment.

- By Drugs

On the basis of drugs, the amblyopia drugs market is segmented into atropine and others. The atropine segment dominated the market with the largest revenue share of 44.1% in 2025, driven by its established clinical efficacy as a penalization therapy for improving vision in the stronger eye and stimulating the weaker eye. It is widely prescribed as an alternative or adjunct to patching due to its ease of use and higher patient compliance, especially among children. Ophthalmologists prefer low-dose atropine therapy because of its reversible effects and strong clinical backing from multiple pediatric studies. The increasing availability of standardized atropine formulations is further strengthening its dominance. In addition, its integration into combined treatment protocols with vision therapy is expanding its clinical acceptance across healthcare systems.

The others segment is expected to witness the fastest growth rate of 21.3% from 2026 to 2033, driven by rising research into novel pharmacological agents targeting neuroplasticity and visual cortex stimulation. Emerging drug classes focusing on dopaminergic modulation and binocular vision enhancement are gaining attention in clinical trials. Increasing investment in pediatric ophthalmic drug development is accelerating innovation beyond traditional atropine-based therapy. Furthermore, growing demand for personalized and combination treatment approaches is expanding the adoption of adjunct therapeutic drugs. Expanding pipeline products from biotech firms focusing on vision restoration therapies are expected to significantly contribute to segment growth.

- By End User

On the basis of end user, the amblyopia drugs market is segmented into hospital/clinical laboratories, physician offices, reference laboratories, and other end users. The physician offices segment dominated the market with the largest revenue share of 46.8% in 2025, driven by the high volume of outpatient pediatric consultations and routine vision screening services conducted in ophthalmology clinics. These settings are the primary point of diagnosis and initial prescription of amblyopia drugs such as atropine eye drops. Physicians prefer office-based treatment management due to ease of follow-up and monitoring of visual improvement. Increasing accessibility of specialized eye care professionals in urban areas further strengthens this segment’s dominance. In addition, growing preference for non-hospital-based, cost-effective treatment environments supports continued demand in physician offices.

The hospital/clinical laboratories segment is expected to witness the fastest growth rate of 18.9% from 2026 to 2033, driven by increasing hospital-based pediatric eye screening programs and advanced diagnostic capabilities. Hospitals are increasingly adopting integrated amblyopia treatment pathways combining pharmacological therapy with imaging and visual function testing. Rising cases of complex or late-diagnosed amblyopia requiring multidisciplinary care are further boosting hospital-based treatment adoption. Expansion of pediatric ophthalmology departments in tertiary care hospitals is also contributing to growth. Moreover, government initiatives to improve child eye health infrastructure are strengthening hospital-based treatment utilization globally.

- By Distribution Channel

On the basis of distribution channel, the amblyopia drugs market is segmented into direct tender, retail sales, and other. The retail sales segment dominated the market with the largest revenue share of 57.2% in 2025, driven by the widespread availability of prescription eye drops in pharmacies and ease of access for parents managing long-term pediatric treatment. Retail pharmacies serve as a convenient distribution point for recurring drug purchases, particularly for atropine-based therapies. Strong pharmacy networks in urban and semi-urban regions ensure continuous drug availability. Increasing awareness among caregivers regarding prescribed amblyopia treatment regimens is further strengthening this segment. In addition, growing physician preference for outpatient prescriptions contributes to sustained retail channel dominance.

The direct tender segment is expected to witness the fastest growth rate of 20.5% from 2026 to 2033, driven by increasing procurement of amblyopia drugs through government healthcare programs and institutional purchasing by hospitals. Public health initiatives focusing on pediatric vision screening and treatment are boosting bulk drug procurement through tenders. Rising investments in national eye health programs, particularly in emerging economies, are further supporting this growth. Hospitals and clinics are increasingly relying on centralized procurement systems to ensure consistent drug supply. Moreover, cost-effective purchasing through direct tenders is encouraging wider adoption in public healthcare systems.

Amblyopia Drugs Market Regional Analysis

- North America dominated the amblyopia drugs market with the largest revenue share of 39.4% in 2025, supported by advanced ophthalmic care infrastructure, strong adoption of pediatric vision screening programs, and early uptake of novel pharmacological therapies

- Consumers and healthcare providers in the region highly prioritize early diagnosis and effective management of amblyopia, supported by widespread use of pharmacological therapies such as atropine eye drops alongside vision correction and patching methods

- This widespread adoption is further supported by high healthcare expenditure, strong insurance coverage for pediatric eye care, and a technologically advanced clinical ecosystem that enables early intervention and continuous monitoring of treatment outcomes, establishing amblyopia drugs as a key component of pediatric ophthalmic care in both hospital and outpatient settings

U.S. Amblyopia Drugs Market Insight

The U.S. amblyopia drugs market captured the largest revenue share of 82% in 2025 within North America, driven by a high burden of pediatric vision disorders and strong adoption of early eye screening programs across schools and healthcare systems. Healthcare providers are increasingly prioritizing pharmacological interventions such as atropine eye drops alongside traditional patching therapy to improve treatment compliance and visual outcomes. The growing preference for evidence-based, non-invasive treatment approaches, combined with strong insurance coverage for pediatric ophthalmic care, further supports market expansion. Moreover, the presence of advanced clinical research infrastructure and continuous development of novel vision therapies is significantly contributing to market growth.

Europe Amblyopia Drugs Market Insight

The Europe amblyopia drugs market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing government-led pediatric vision screening initiatives and rising awareness of early diagnosis of amblyopia. The region is witnessing growing clinical adoption of pharmacological therapies as adjuncts to vision therapy and patching, supported by well-established ophthalmology care systems. European healthcare systems emphasize early intervention, which is encouraging wider prescription of atropine-based treatments in pediatric patients. In addition, increasing healthcare expenditure and improved access to specialist eye care services are fostering steady market growth across both Western and Eastern Europe.

U.K. Amblyopia Drugs Market Insight

The U.K. amblyopia drugs market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing emphasis on childhood vision screening and early therapeutic intervention programs under public healthcare initiatives. Rising awareness among parents regarding long-term vision impairment risks is encouraging early diagnosis and pharmacological treatment adoption. The National Health Service (NHS) plays a key role in supporting access to amblyopia therapies, including atropine eye drops as part of standard care protocols. Furthermore, increasing integration of digital eye health monitoring tools is enhancing treatment adherence and follow-up care, contributing to sustained market growth.

Germany Amblyopia Drugs Market Insight

The Germany amblyopia drugs market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure and increasing focus on pediatric ophthalmic health. Germany’s emphasis on early diagnosis and preventive healthcare is driving adoption of pharmacological treatments for amblyopia in combination with corrective vision therapies. The country’s well-developed clinical research ecosystem is supporting the evaluation of advanced neuro-visual drug therapies aimed at improving binocular vision. In addition, rising awareness among healthcare professionals and parents regarding untreated amblyopia complications is further strengthening market demand.

Asia-Pacific Amblyopia Drugs Market Insight

The Asia-Pacific amblyopia drugs market is poised to grow at the fastest CAGR of 21% during the forecast period of 2026 to 2033, driven by a large pediatric population base, increasing prevalence of refractive vision disorders, and improving access to eye care services in emerging economies. Rapid urbanization and rising healthcare awareness are supporting early diagnosis and wider adoption of pharmacological therapies such as atropine. Government-led school vision screening programs and expanding ophthalmology infrastructure are further accelerating treatment uptake. In addition, growing affordability of eye care treatments and increasing penetration of specialized pediatric clinics are significantly contributing to regional market growth.

Japan Amblyopia Drugs Market Insight

The Japan amblyopia drugs market is gaining momentum due to the country’s advanced healthcare system, high awareness of pediatric eye disorders, and strong focus on early medical intervention. The increasing adoption of pharmacological therapies alongside vision training programs is supporting improved treatment outcomes in children. Japan’s aging population and emphasis on lifelong vision health awareness are indirectly strengthening early screening practices in younger populations. Furthermore, integration of digital health tools and precision-based ophthalmic care is enhancing treatment monitoring and adherence in clinical settings.

India Amblyopia Drugs Market Insight

The India amblyopia drugs market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to its large pediatric population, increasing prevalence of uncorrected refractive errors, and rapid expansion of eye care infrastructure. Rising awareness of childhood vision disorders and growing penetration of school-based eye screening programs are driving early diagnosis and treatment adoption. The availability of affordable pharmacological options such as atropine eye drops is further supporting market accessibility. In addition, government initiatives focused on child healthcare and expanding reach of ophthalmology services in rural and semi-urban areas are key factors propelling market growth.

Amblyopia Drugs Market Share

The Amblyopia Drugs industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Alcon Inc. (Switzerland)

- Bausch Health (Canada)

- Bayer AG (Germany)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Sun Pharmaceutical Industries Limited (India)

- Teva Pharmaceutical Industries Limited (Israel)

- Hikma Pharmaceuticals PLC (U.K.)

- Apotex Inc. (Canada)

- AstraZeneca (U.K.)

- Bausch + Lomb Corporation (U.S.)

- Akorn Operating Company LLC (U.S.)

- ENTOD Pharmaceuticals (India)

- Ophthalmic Therapeutics LLC (U.S.)

- Genentech, Inc. (U.S.)

- Hoya Corporation (Japan)

What are the Recent Developments in Global Amblyopia Drugs Market?

- In October 2025, the U.S. FDA issued a Complete Response Letter for a low-dose atropine-based ophthalmic therapy candidate targeting pediatric vision disorders, citing concerns related to inconsistent efficacy outcomes. Despite positive trial safety profiles, the regulatory decision delayed potential commercialization of the pharmacological treatment. The setback highlighted ongoing challenges in achieving uniform clinical response in amblyopia-related drug development. It also reflected stricter regulatory scrutiny for pediatric ophthalmic pharmacotherapies

- In April 2025, ENTOD Pharmaceuticals announced regulatory approval from India’s CDSCO for its 0.05% atropine eye drop formulation (Myatro XL) designed for pediatric use in vision-related conditions, including amblyopia-related therapeutic protocols and refractive control support. The product was positioned for long-term, once-daily use in children aged 6–12 years and aimed at improving treatment adherence through improved formulation design and pH-balanced delivery

- In March 2025, Luminopia received an expanded FDA clearance for its digital therapeutic used in amblyopia treatment, extending its indication to a broader pediatric age group. The VR-based platform delivers dichoptic visual stimulation to improve binocular vision and visual acuity in children with lazy eye. Clinical outcomes demonstrated improved patient adherence compared to traditional patching therapy, highlighting growing acceptance of digital-first ophthalmic treatments. This development reinforces the shift toward non-invasive, software-driven adjunct therapies in amblyopia management

- In November 2024, a late-stage clinical study evaluating a low-dose atropine formulation combined with a drug delivery mechanism for pediatric vision disorders was discontinued after failing to demonstrate statistically significant superiority over placebo. Although the therapy was well tolerated, efficacy endpoints were not met. The decision led to strategic pipeline realignment for the sponsoring company. It also reinforced the challenges in developing consistent pharmacological solutions for amblyopia treatment

- In July 2024, clinical real-world evidence from multiple pediatric ophthalmology centers confirmed the effectiveness of FDA-cleared digital amblyopia therapy in improving visual outcomes in children with amblyopia. Patients using the therapy showed significant improvement in visual acuity over a 12-week treatment period. The study also highlighted higher compliance rates compared to traditional occlusion therapy methods. These findings support the growing clinical adoption of interactive digital platforms in amblyopia treatment protocols

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.