Global Ambulatory Specialty Care Networks Market

Market Size in USD Billion

USD

4.28 Billion

USD

12.73 Billion

2025

2033

USD

4.28 Billion

USD

12.73 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.28 Billion | |

| USD 12.73 Billion | |

| % | |

|

Ambulatory Specialty Care Networks Market Overview

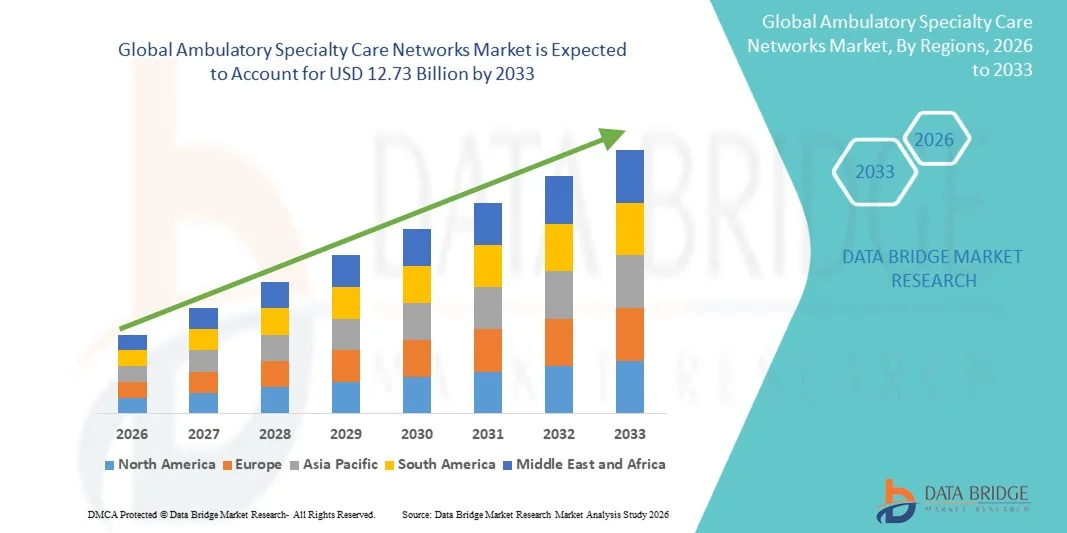

The Ambulatory Specialty Care Networks Market was valued at USD 4.28 billion in 2025 and is projected to reach USD 12.73 billion by 2033, growing at a CAGR of 14.60% from 2026 to 2033. The market is witnessing steady growth driven by the increasing shift from inpatient to outpatient care models, rising prevalence of chronic diseases requiring long-term specialty management, and growing demand for cost-efficient and accessible healthcare delivery systems.

The expansion of value-based care initiatives, coupled with advancements in digital health, telemedicine, and integrated care coordination platforms, is further accelerating the adoption of ambulatory specialty care networks. Hospitals, physician groups, and corporate healthcare providers are increasingly forming network-based outpatient specialty centers to improve patient outcomes, reduce hospital congestion, and lower overall healthcare costs while ensuring continuous and specialized care delivery.

Key Market Trends & Insights

- North America dominated the Ambulatory Specialty Care Networks Market with the largest revenue share of 38.6% in 2025, supported by a highly developed outpatient care infrastructure, strong presence of integrated healthcare systems, and rapid adoption of value-based care models.

- The Treatment Services segment led the market with a 46.8% share in 2025, driven by the increasing shift of complex medical procedures such as minimally invasive surgeries, infusion therapies, and chronic disease interventions to outpatient settings

- Asia-Pacific is expected to be the fastest-growing region from 2026 to 2033, expanding at a CAGR of 8.1%, fueled by rising healthcare expenditure, expanding private hospital networks, increasing burden of chronic diseases, and rapid development of specialty clinics in countries such as China and India.

- Diagnostic Services are the fastest-growing service type, projected to register a CAGR of 8.4%, reflecting the surge in demand for early disease detection and preventive healthcare screening.

- The Cardiology segment dominated the speciality area category with a 29.4% revenue share in 2025, led by the global rise in cardiovascular diseases and increasing need for long-term outpatient cardiac care.

- Ambulatory Surgery Centers accounted for 44.2% of the market, preferred by the increasing preference for cost-effective same-day surgical procedures. ASCs provide efficient surgical care with reduced hospital stay requirements and lower infection risks.

- The Specialty Clinics segment is the fastest-growing facility type category, with a CAGR of 7.9%, driven by the rising demand for disease-specific outpatient care delivery.

Market Size & Forecast

- Global Market Value (2025): USD 4.28 Billion

- Expected Market Value (2033): USD 12.73 Billion

- Forecast CAGR (2026–2033): 14.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Ambulatory Specialty Care Networks Market Segmentation

|

Attributes |

Ambulatory Specialty Care Networks Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· CVS Health (U.S.) · UnitedHealth Group (U.S.) · Kaiser Permanente (U.S.) · HCA Healthcare (U.S.) · Tenet Healthcare (U.S.) · Trinity Health (U.S.) · CommonSpirit Health (U.S.) · Providence (U.S.) · Mayo Clinic (U.S.) · Cleveland Clinic (U.S.) · Intermountain Health (U.S.) · Ascension (U.S.) · Surgery Partners (U.S.) · Privia Health Group (U.S.) · Agilon Health (U.S.) · ChenMed (U.S.) · DaVita Inc. (U.S.) · Humana (U.S.) · Apollo Hospitals Enterprise Ltd (India) · Ramsay Health Care (Australia) |

|

Market Opportunities |

· Expansion of hospital-at-home and hybrid outpatient care models · Integration of AI-driven clinical decision support and predictive analytics · Rapid growth in employer-led and insurance-backed bundled payment programs |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Ambulatory Specialty Care Networks Market Trends

Trend: Expansion of Integrated Multispecialty Outpatient Networks

Healthcare providers are increasingly forming integrated ambulatory specialty care networks that combine multiple disciplines such as cardiology, orthopedics, and oncology under a unified outpatient system to improve care coordination and patient outcomes. These networks leverage shared electronic health records and centralized referral systems to streamline patient flow, reduce duplication of diagnostics, and enhance continuity of care across specialties. The model is also supported by value-based reimbursement structures that reward efficiency and long-term patient management, while digital platforms enable seamless communication between specialists and primary care providers. For instance, large hospital systems are consolidating standalone specialty clinics into unified outpatient networks to improve efficiency and care delivery consistency.

Ambulatory Specialty Care Networks Market Dynamics

Key Market Driver: Rising Shift from Inpatient to Outpatient Specialty Care Delivery

The increasing preference for outpatient care over traditional inpatient hospitalization is significantly driving the growth of ambulatory specialty care networks, as patients and payers seek lower-cost, high-quality, and more convenient treatment options. Advances in minimally invasive procedures, improved diagnostic technologies, and enhanced post-acute care protocols are enabling more complex treatments to be safely performed in outpatient settings. This shift is further reinforced by insurance providers promoting outpatient reimbursement models and hospitals expanding satellite specialty centers to reduce inpatient burden and optimize resource utilization. For instance, healthcare systems are relocating elective surgical procedures such as orthopedics and gastroenterology into ambulatory centers to improve efficiency.

Key Restraint/Challenge: Fragmentation and Lack of Interoperability Across Care Networks

A major challenge in the ambulatory specialty care networks market is the fragmentation of healthcare systems and limited interoperability between different providers, which restricts seamless patient data exchange and coordinated treatment planning. Many outpatient specialty providers operate on separate digital platforms, leading to inefficiencies in patient tracking, delayed diagnoses, and duplication of clinical tests. In addition, regulatory constraints and inconsistent adoption of standardized electronic health record systems further complicate integration across networks. For instance, independent specialty clinics often face difficulties sharing real-time patient data with hospital-owned systems, resulting in fragmented care delivery across regions.

Key Market Opportunity: Expansion of AI-Enabled Care Coordination and Predictive Patient Management

The integration of artificial intelligence and predictive analytics presents a significant opportunity for ambulatory specialty care networks to enhance patient management, optimize resource allocation, and improve clinical decision-making. AI-driven tools can analyze patient histories, predict disease progression, and support personalized treatment pathways across multiple specialties within a network. Cloud-based platforms further enable real-time monitoring and coordination between providers, improving efficiency and reducing hospital readmissions. For instance, healthcare networks are deploying AI-powered care coordination systems to identify high-risk patients early and proactively manage chronic disease progression.

Ambulatory Specialty Care Networks Market Scope

The ambulatory specialty care networks market is segmented on the basis of service type, specialty area, facility type, and end user.

- By Service Type

On the basis of service type, the Ambulatory Specialty Care Networks Market is segmented into diagnostic services, treatment services, consultation services, preventive & wellness services, and rehabilitation services. The Treatment Services segment dominated the market with a share of 46.8% in 2025, driven by the increasing shift of complex medical procedures such as minimally invasive surgeries, infusion therapies, and chronic disease interventions to outpatient settings. These services are widely preferred due to lower hospitalization costs, faster recovery times, and improved patient convenience. Growing adoption of same-day surgical procedures across specialties such as orthopedics, cardiology, and gastroenterology is further strengthening demand. Expansion of ambulatory surgery centers and specialty clinics is also boosting utilization of treatment-based services. Integration of advanced medical technologies in outpatient environments is improving procedural efficiency. Rising healthcare cost pressures are pushing payers and providers toward outpatient treatment models.

The Diagnostic Services segment is expected to witness the fastest growth from 2026 to 2033, with a CAGR of 8.4%, driven by increasing demand for early disease detection and preventive healthcare screening. Rising prevalence of chronic diseases is accelerating the need for frequent imaging, laboratory testing, and pathology services in outpatient settings. Advances in point-of-care diagnostics and AI-enabled imaging are significantly improving diagnostic accuracy and speed. Growing adoption of decentralized diagnostic centers is expanding accessibility across urban and semi-urban regions. Integration of diagnostics with specialty care networks is enhancing coordinated treatment planning. Increasing emphasis on preventive healthcare programs is further supporting segment growth.

- By Specialty Area

On the basis of specialty area, the market is segmented into cardiology, orthopedics, ophthalmology, gastroenterology, dermatology, gynecology, ENT, neurology, oncology, pain management, and others. The Cardiology segment dominated the market in 2025 with a share of 29.4%, driven by the global rise in cardiovascular diseases and increasing need for long-term outpatient cardiac care. Ambulatory networks are widely used for diagnostic monitoring, post-operative care, and chronic condition management such as hypertension and heart failure. Expansion of outpatient cardiac imaging, stress testing, and catheter-based procedures is further supporting growth. Strong adoption of remote patient monitoring and wearable cardiac devices is improving continuous care delivery. Hospitals are increasingly shifting cardiac rehabilitation programs to outpatient networks. High patient volume and long-term treatment requirements make cardiology the leading specialty segment.

The Orthopedics segment is expected to witness the fastest growth from 2026 to 2033, with a CAGR of 8.1%, driven by rising cases of musculoskeletal disorders, sports injuries, and aging population-related joint issues. Increasing preference for minimally invasive orthopedic surgeries is enabling same-day discharge procedures in ambulatory centers. Advances in arthroscopy, robotic-assisted surgery, and pain management techniques are enhancing outpatient feasibility. Growing demand for physical therapy and post-surgical rehabilitation is further boosting this segment. Expansion of specialty orthopedic clinics is improving accessibility and reducing hospital dependency. Rising healthcare expenditure on mobility-related conditions is accelerating adoption.

- By Facility Type

On the basis of facility type, the market is segmented into ambulatory surgery centers, specialty clinics, diagnostic & imaging centers, hospital outpatient departments, and urgent care centers. The Ambulatory Surgery Centers (ASCs) segment dominated the market in 2025 with a share of 44.2%, driven by increasing preference for cost-effective same-day surgical procedures. ASCs provide efficient surgical care with reduced hospital stay requirements and lower infection risks. Strong adoption across orthopedics, ophthalmology, and gastroenterology procedures is driving utilization. Integration with hospital networks and insurance providers is further strengthening their role in healthcare delivery systems. Technological advancements in surgical equipment and anesthesia techniques are expanding procedural capabilities. High patient throughput and operational efficiency make ASCs the dominant facility type.

The Specialty Clinics segment is expected to witness the fastest growth from 2026 to 2033, with a CAGR of 7.9%, driven by rising demand for disease-specific outpatient care delivery. Increasing prevalence of chronic conditions is encouraging the establishment of focused clinics for cardiology, dermatology, and neurology care. Specialty clinics offer personalized treatment pathways and improved patient engagement. Digital health integration and teleconsultation capabilities are enhancing accessibility and efficiency. Growing investments from private healthcare providers are expanding clinic networks globally. Rising demand for convenient, localized care is accelerating adoption.

- By End User

On the basis of end user, the market is segmented into adults, geriatric population, pediatrics, and corporate. The Adult population segment dominated the market in 2025 with a share of 57.6%, driven by high prevalence of chronic diseases, lifestyle disorders, and increasing outpatient treatment utilization. Adults represent the primary user base for specialty services such as cardiology, orthopedics, and gastroenterology. Rising healthcare awareness and early diagnosis trends are further increasing service consumption. Employment-related insurance coverage is also supporting higher outpatient care utilization. Expansion of preventive screening programs targeting adults is strengthening demand. This segment remains the core revenue contributor across ambulatory networks.

The Geriatric population segment is expected to witness the fastest growth from 2026 to 2033, with a CAGR of 8.6%, driven by global population aging and higher incidence of age-related chronic conditions. Elderly patients require frequent specialty consultations, long-term disease management, and rehabilitation services. Outpatient care models are preferred due to reduced hospitalization risks and improved accessibility. Expansion of home-linked ambulatory services is further supporting this segment. Increasing healthcare spending on elderly care is boosting adoption. Integration of remote monitoring and chronic care programs is accelerating growth.

Ambulatory Specialty Care Networks Market Regional Analysis

North America dominated the Ambulatory Specialty Care Networks Market with the largest revenue share of 38.6% in 2025, supported by a highly developed outpatient care infrastructure, strong presence of integrated healthcare systems, and rapid adoption of value-based care models. The region also benefits from high healthcare expenditure, advanced digital health integration, and rapid expansion of ambulatory surgery centers and specialty clinics. Increasing prevalence of chronic diseases and strong insurance coverage for outpatient services continue to reinforce demand. Growing emphasis on cost-efficient care delivery and reduced hospital burden further strengthens North America’s leadership position in the global market.

U.S. Ambulatory Specialty Care Networks Market Insight

The U.S. ambulatory specialty care networks market is witnessing strong growth due to rising healthcare digitization, increasing demand for outpatient specialty services, and expansion of large integrated health systems. The country’s mature healthcare infrastructure, along with strong penetration of insurance-driven care models, is driving widespread adoption of ambulatory surgery centers and specialty clinics. Growing prevalence of chronic diseases such as cardiovascular disorders and diabetes is further accelerating outpatient care utilization. In addition, increasing focus on value-based reimbursement and cost containment is pushing providers to shift procedures from inpatient hospitals to ambulatory settings. Rapid adoption of telehealth and remote patient monitoring is also enhancing care coordination across specialty networks.

Europe Ambulatory Specialty Care Networks Market Insight

The Europe ambulatory specialty care networks market remains a major contributor to global revenue, driven by strong public healthcare systems, aging population, and increasing demand for efficient outpatient care delivery. The widespread use of structured referral systems and integrated care pathways is supporting expansion of specialty care networks across the region. Governments are actively promoting outpatient treatment models to reduce hospital congestion and improve healthcare efficiency. Rising adoption of digital health platforms and electronic health records is further enhancing coordination between specialists. Increasing burden of chronic diseases and growing focus on preventive healthcare continue to strengthen market growth across Europe.

U.K. Ambulatory Specialty Care Networks Market Insight

The U.K. ambulatory specialty care networks market is experiencing steady growth, supported by strong National Health Service (NHS) reforms, rising demand for outpatient services, and increasing focus on reducing hospital waiting times. Expansion of community-based specialty clinics is improving access to cardiology, orthopedics, and diagnostic services. Growing investment in digital health infrastructure is enhancing care coordination and patient management across networks. The country is also witnessing increased adoption of telemedicine and remote monitoring solutions to support chronic disease management. Emphasis on cost-efficient healthcare delivery is further driving the shift toward ambulatory care models.

Germany Ambulatory Specialty Care Networks Market Insight

The Germany ambulatory specialty care networks market is expanding steadily due to a strong hospital system, advanced medical infrastructure, and increasing shift toward outpatient treatment models. The country’s aging population and high prevalence of chronic diseases are driving demand for continuous specialty care outside hospital settings. Integrated care networks are increasingly being adopted to improve efficiency and reduce inpatient burden. Strong regulatory support for outpatient surgical procedures is further boosting market expansion. In addition, rising adoption of digital health solutions and electronic patient records is improving coordination across specialty care providers.

Asia-Pacific Ambulatory Specialty Care Networks Market Insight

The Asia-Pacific ambulatory specialty care networks market is expected to witness rapid growth, driven by rising healthcare expenditure, expanding private healthcare infrastructure, and increasing burden of chronic diseases. Growing urbanization and improving access to specialty care services are accelerating outpatient care adoption across countries such as China, India, and Japan. Governments are increasingly investing in healthcare modernization and outpatient care expansion to reduce hospital overcrowding. Rising awareness regarding preventive healthcare and early diagnosis is further supporting demand. In addition, rapid digital health adoption and telemedicine integration are strengthening specialty care network development across the region.

Japan Ambulatory Specialty Care Networks Market Insight

The Japan ambulatory specialty care networks market is witnessing consistent growth due to its rapidly aging population and strong focus on efficient healthcare delivery systems. Increasing demand for chronic disease management and long-term specialty care is driving outpatient service utilization. Hospitals and clinics are increasingly adopting integrated care models to improve coordination and reduce inpatient dependency. Advanced adoption of digital health technologies and electronic medical records is enhancing patient monitoring and care efficiency. Strong emphasis on preventive healthcare and early diagnosis is further supporting market expansion.

China Ambulatory Specialty Care Networks Market Insight

The China ambulatory specialty care networks market is growing rapidly, driven by expanding healthcare infrastructure, rising urban population, and increasing demand for affordable specialty care services. Government healthcare reforms are encouraging the development of outpatient care systems to reduce pressure on hospitals. Rapid growth in private healthcare providers and specialty clinics is further supporting market expansion. Increasing prevalence of chronic diseases and growing awareness of preventive healthcare are boosting demand for continuous outpatient management. In addition, strong adoption of digital health platforms and telemedicine services is accelerating the development of integrated specialty care networks.

Ambulatory Specialty Care Networks Market Share

The Ambulatory Specialty Care Networks industry is primarily led by well-established companies, including:

- CVS Health (U.S.)

- UnitedHealth Group (U.S.)

- Kaiser Permanente (U.S.)

- HCA Healthcare (U.S.)

- Tenet Healthcare (U.S.)

- Trinity Health (U.S.)

- CommonSpirit Health (U.S.)

- Providence (U.S.)

- Mayo Clinic (U.S.)

- Cleveland Clinic (U.S.)

- Intermountain Health (U.S.)

- Ascension (U.S.)

- Surgery Partners (U.S.)

- Privia Health Group (U.S.)

- Agilon Health (U.S.)

- ChenMed (U.S.)

- DaVita Inc. (U.S.)

- Humana (U.S.)

- Apollo Hospitals Enterprise Ltd (India)

- Ramsay Health Care (Australia)

Latest Developments in Ambulatory Specialty Care Networks Market

- In March 2023, CVS Health, a leading U.S. healthcare company, completed the acquisition of Oak Street Health, a value-based primary and ambulatory care provider, to expand its outpatient care network and strengthen its specialty care delivery capabilities. The acquisition enhances CVS’s ability to provide integrated, community-based healthcare services for chronic disease patients and Medicare populations, reinforcing its long-term ambulatory care strategy

- In May 2023, CVS Health announced the completion of its acquisition of Signify Health, a major in-home and outpatient care services provider, expanding its value-based care and ambulatory service network across the United States. The integration strengthens CVS’s ability to deliver coordinated care through physician groups, home-based services, and specialty outpatient programs, improving patient access and care continuity

- In December 2022, UnitedHealth Group completed the acquisition of LHC Group, a leading home health and ambulatory care provider, significantly expanding Optum’s outpatient and post-acute care network across the U.S. The deal enhances integrated care delivery capabilities, particularly for elderly and chronic disease patients requiring continuous specialty care outside hospitals

- In April 2022, Optum, part of UnitedHealth Group, completed the acquisition of Atrius Health, a major physician-led ambulatory care network in Massachusetts, strengthening its presence in integrated specialty care delivery. The acquisition supports expansion of value-based care models and improves coordination across outpatient specialty services including cardiology and oncology

- In November 2021, Walgreens Boots Alliance and VillageMD expanded their partnership by opening additional co-located primary and ambulatory care clinics across the United States, significantly increasing access to outpatient specialty and chronic disease management services. The expansion supports Walgreens’ strategy to build a nationwide integrated ambulatory care network combining pharmacy and physician-led services

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.