Global Amylin Analog Market

Market Size in USD Billion

USD

645.14 Billion

USD

982.60 Billion

2025

2033

USD

645.14 Billion

USD

982.60 Billion

2025

2033

| 2026 - 2033 | |

| USD 645.14 Billion | |

| USD 982.60 Billion | |

| % | |

|

Amylin Analog Market Size

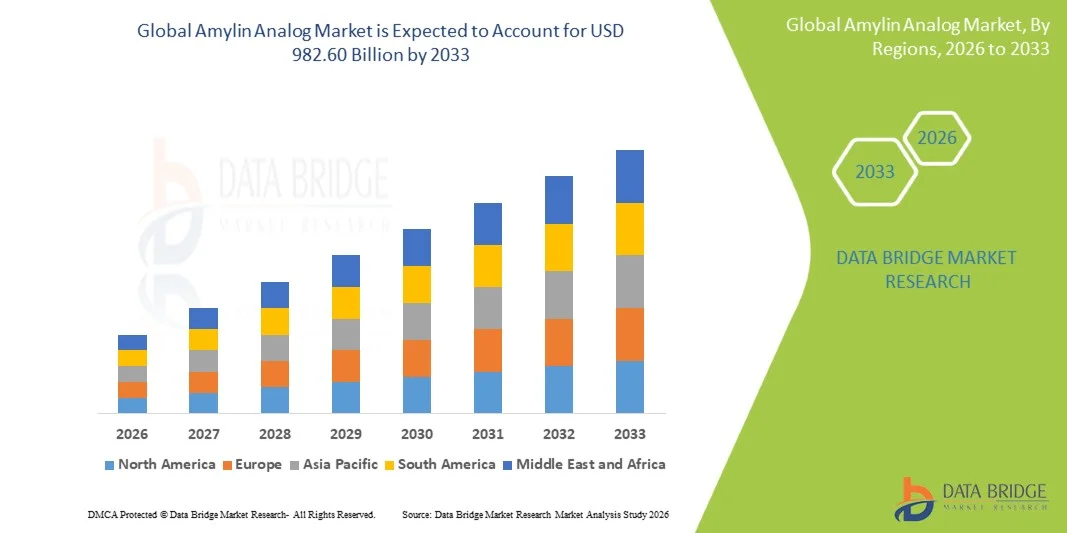

- The global amylin analog market size was valued at USD 645.14 billion in 2025 and is expected to reach USD 982.60 billion by 2033, at a CAGR of 5.40% during the forecast period

- The market growth is largely fueled by the rising prevalence of diabetes and obesity, increasing focus on metabolic disorder management, and continuous advancements in peptide-based therapeutics, leading to greater adoption of innovative glycemic control treatments across healthcare settings

- Furthermore, growing demand for effective postprandial glucose control, increasing use of combination therapies with insulin and GLP-1 receptor agonists, and expanding awareness regarding long-term diabetes complications are establishing Amylin Analog solutions as an important component of modern diabetes management. These converging factors are accelerating the uptake of Amylin Analog solutions, thereby significantly boosting the industry's growth

Amylin Analog Market Analysis

- Amylin Analog therapies, including pramlintide-based formulations and emerging long-acting peptide analogs, are increasingly vital components of modern diabetes management due to their role in improving postprandial glucose control, slowing gastric emptying, and reducing glucagon secretion alongside insulin therapy

- The escalating demand for Amylin Analog therapies is primarily fueled by the rising global prevalence of type 1 and type 2 diabetes, increasing need for improved glycemic control in insulin-dependent patients, and growing adoption of combination injectable therapies for better metabolic outcomes

- North America dominated the amylin analog market with the largest revenue share of approximately 41.8% in 2025, characterized by advanced diabetes care infrastructure, high diagnosis rates, strong adoption of injectable biologics, and presence of major pharmaceutical companies, with the U.S. accounting for significant usage in both type 1 and insulin-intensive type 2 diabetes populations

- Asia-Pacific is expected to be the fastest growing region in the amylin analog market during the forecast period due to rising diabetes prevalence, increasing healthcare expenditure, improving access to advanced biologic therapies, and growing awareness of early glycemic control strategies across China, India, Japan, and Southeast Asia

- The Subcutaneous segment dominated the largest market revenue share of 96.2% in 2025, driven by its effectiveness in delivering peptide-based drugs like pramlintide directly into systemic circulation

Report Scope and Amylin Analog Market Segmentation

|

Attributes |

Amylin Analog Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Amylin Analog Market Trends

“Growing Role of Combination Therapies and Postprandial Glucose Control”

- A significant and accelerating trend in the global Amylin Analog market is the growing adoption of combination therapy approaches in diabetes management, where amylin analogs are increasingly used alongside insulin and other antidiabetic agents. This strategy is improving overall glycemic stability by targeting both fasting and postprandial glucose levels, which remain a major challenge in diabetes care

- Amylin analogs such as pramlintide are being increasingly incorporated into insulin-based regimens for patients with type 1 and insulin-dependent type 2 diabetes, particularly to address post-meal glucose excursions

- For instance, pramlintide is clinically used as an adjunct therapy in patients who fail to achieve adequate postprandial control with intensive insulin therapy alone, demonstrating improved HbA1c reduction and reduced glucose variability in controlled clinical settings

- The growing clinical shift toward personalized diabetes management is encouraging endocrinologists to adopt multi-hormonal treatment strategies, where amylin analogs complement insulin by slowing gastric emptying, suppressing glucagon secretion, and enhancing satiety

- This approach is increasingly being supported by diabetes care guidelines in developed markets such as North America and Europe, where combination injectable therapies are becoming more common in complex diabetes cases

- Rising physician awareness regarding the limitations of insulin monotherapy in controlling postprandial hyperglycemia is further accelerating adoption of adjunct therapies like amylin analogs across global healthcare systems

Amylin Analog Market Dynamics

Driver

“Rising Global Prevalence of Diabetes and Demand for Improved Glycemic Control”

- The primary driver of the global Amylin Analog market is the rapidly increasing prevalence of diabetes worldwide, driven by aging populations, sedentary lifestyles, urbanization, and rising obesity rates. This has created a strong demand for advanced therapies that can provide more comprehensive glycemic control beyond conventional insulin therapy

- For instance, large-scale epidemiological studies in 2025 continue to show a steady rise in diabetes cases globally, with countries such as India, China, and the United States reporting significant increases in both type 1 and type 2 diabetes prevalence, directly expanding the patient pool requiring adjunct therapies like amylin analogs

- The growing clinical need to manage postprandial glucose spikes more effectively is encouraging healthcare providers to prescribe amylin analogs in combination with insulin, especially for patients with poor glycemic control despite optimized insulin regimens

- In addition, increasing awareness among endocrinologists regarding the role of amylin deficiency in diabetes pathophysiology is supporting greater clinical acceptance of these therapies.

- Expanding access to diabetes diagnostics and treatment in emerging economies is also contributing to earlier detection and increased initiation of advanced therapeutic regimens globally

Restraint/Challenge

“Gastrointestinal Side Effects, Injection Burden, and Limited Patient Adherence”

- One of the major restraints in the Amylin Analog market is the occurrence of gastrointestinal adverse effects, particularly nausea, vomiting, and reduced appetite, which can significantly affect patient tolerance and long-term adherence to therapy

- For instance, in clinical initiation of pramlintide therapy, a notable proportion of patients experience dose-dependent nausea during the early treatment phase, which often requires gradual titration or temporary dose adjustments to improve tolerability in real-world practice

- Another major challenge is the requirement for multiple daily injections in addition to insulin therapy, which increases treatment complexity and reduces patient convenience, especially among elderly patients and those already managing complex insulin regimens

- Limited awareness among patients and healthcare providers in developing regions also restricts adoption, as amylin analog therapy requires careful dosing coordination with meals and insulin to avoid hypoglycemia risk

- Furthermore, concerns regarding hypoglycemia when used in combination with insulin, along with the need for close clinical monitoring during initiation, act as barriers to widespread prescription

- Overcoming these challenges through improved patient education, simplified dosing protocols, fixed-dose combination research, and development of longer-acting formulations will be critical for future market expansion

Amylin Analog Market Scope

The market is segmented on the basis of diabetes type, drug type, dosage, route of administration, end-users, and distribution channel.

• By Diabetes Type

On the basis of diabetes type, the Amylin Analog market is segmented into Type I Diabetes, Type II Diabetes, and Gestational Diabetes. The Type I Diabetes segment dominated the largest market revenue share of 46.8% in 2025, driven by the absolute deficiency of insulin and amylin in patients requiring adjunctive therapies like amylin analogs for postprandial glucose control. Rising prevalence of autoimmune diabetes and long-term dependency on insulin therapy further support demand. Increasing adoption of combination therapy with insulin enhances clinical outcomes. Strong clinical guidelines recommending amylin analogs in Type I patients reinforce dominance. Growing awareness of glycemic variability management also contributes to uptake. Expanding endocrinology care infrastructure strengthens segment leadership.

The Type II Diabetes segment is expected to witness the fastest growth rate of 22.6% from 2026 to 2033, driven by rapidly increasing global prevalence of lifestyle-related diabetes. Rising obesity rates, sedentary lifestyles, and aging populations are major contributing factors. Amylin analogs are increasingly used as adjunct therapy in patients inadequately controlled on insulin. Expanding use of injectable anti-diabetic therapies is boosting demand. Growing physician preference for combination treatments improves adoption. Increasing awareness of postprandial glucose control benefits supports expansion. Continuous innovation in diabetes management therapies further accelerates growth.

• By Drug Type

On the basis of drug type, the Amylin Analog market is segmented into Pramlintide and Others. The Pramlintide segment held the largest market revenue share of 89.3% in 2025, driven by its status as the only widely approved synthetic amylin analog used as an adjunct therapy in both Type I and Type II diabetes. It effectively regulates postprandial glucose levels by slowing gastric emptying and suppressing glucagon secretion. Strong clinical adoption and established efficacy in reducing HbA1c levels support dominance. Physician familiarity and guideline-based recommendations further strengthen usage. Increasing diabetes burden globally continues to drive demand. Availability across major pharmaceutical markets reinforces segment leadership.

The Others segment is expected to witness the fastest CAGR of 24.2% from 2026 to 2033, driven by ongoing research into next-generation amylin analogs and combination therapies. Pharmaceutical companies are developing improved formulations with enhanced stability and patient compliance. Growing investment in metabolic disorder therapeutics is accelerating innovation. Expanding clinical trials for dual-acting peptide therapies is supporting future growth. Rising demand for personalized diabetes treatment solutions further boosts potential. Advancements in peptide engineering technologies are strengthening pipeline development.

• By Dosage

On the basis of dosage, the Amylin Analog market is segmented into Injectables and Others. The Injectables segment accounted for the largest market revenue share of 94.6% in 2025, driven by the peptide nature of amylin analogs that require subcutaneous injection for effective absorption. Injectable formulations ensure precise dosing and rapid therapeutic action in glycemic control. High reliance on insulin-based regimens supports injectable dominance. Strong clinical preference for controlled administration reinforces usage. Increasing diabetes management programs further boost demand. Hospital and homecare settings widely adopt injectable therapies. Continuous patient education on self-injection supports sustained adoption.

The Others segment is expected to witness the fastest CAGR of 21.3% from 2026 to 2033, driven by research into alternative delivery systems such as oral peptides and long-acting formulations. Pharmaceutical innovation is focused on improving patient compliance and reducing injection burden. Growing demand for non-invasive diabetes therapies is supporting development. Advancements in drug delivery technology are accelerating progress. Increasing R&D investment in metabolic disease treatment enhances pipeline expansion. Emerging formulation technologies continue to create new growth opportunities.

• By Route of Administration

On the basis of route of administration, the Amylin Analog market is segmented into Subcutaneous and Others. The Subcutaneous segment dominated the largest market revenue share of 96.2% in 2025, driven by its effectiveness in delivering peptide-based drugs like pramlintide directly into systemic circulation. It ensures stable absorption and consistent glycemic control in diabetic patients. Strong clinical guidelines recommend subcutaneous administration as standard practice. Widespread patient familiarity with insulin injections supports adoption. Homecare usage of self-administered injections strengthens dominance. Increasing diabetes prevalence continues to drive segment growth. Established safety and efficacy profile further reinforces leadership.

The Others segment is expected to witness the fastest CAGR of 20.8% from 2026 to 2033, driven by ongoing research into alternative delivery routes such as oral and intranasal formulations. Pharmaceutical companies are investing in non-invasive delivery technologies to improve compliance. Rising patient preference for needle-free options is supporting innovation. Advancements in peptide stabilization techniques are enabling new possibilities. Increasing focus on convenience-driven therapies is accelerating development. Expanding clinical trials continue to support future adoption.

• By End-Users

On the basis of end-users, the Amylin Analog market is segmented into Hospitals, Specialty Clinics, Homecare, and Others. The Hospitals segment held the largest market revenue share of 52.9% in 2025, driven by high patient admissions for diabetes management and specialist endocrinology care. Hospitals provide structured treatment plans involving insulin and amylin analog combination therapy. Strong diagnostic and monitoring infrastructure supports usage. Rising diabetes complications requiring hospital care further strengthen demand. Availability of trained healthcare professionals ensures proper administration. Increasing inpatient and outpatient diabetes cases reinforce dominance.

The Homecare segment is expected to witness the fastest CAGR of 23.7% from 2026 to 2033, driven by growing preference for self-management of chronic diabetes. Rising adoption of self-injectable therapies is supporting outpatient care. Increasing awareness of home-based glucose monitoring improves treatment adherence. Expanding elderly diabetic population further boosts demand. Technological advancements in delivery devices enhance ease of use. Rising healthcare cost pressures are shifting care to home settings. Strong patient education programs continue to accelerate adoption.

• By Distribution Channel

On the basis of distribution channel, the Amylin Analog market is segmented into Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, and Others. The Hospital Pharmacy segment accounted for the largest market revenue share of 57.4% in 2025, driven by high prescription volumes for hospitalized diabetic patients and controlled dispensing of injectable therapies. Hospitals serve as primary points of diagnosis and treatment initiation. Strong regulatory control over peptide-based drugs supports hospital distribution. Increasing inpatient diabetes management strengthens demand. Availability of specialist supervision ensures safe administration. Growing hospitalization rates for complications reinforce leadership.

The Online Pharmacy segment is expected to witness the fastest CAGR of 25.1% from 2026 to 2033, driven by increasing digital healthcare adoption and rising preference for convenient drug access. Expansion of e-prescription systems is supporting online sales growth. Growing awareness of home delivery services is boosting adoption. Improved cold chain logistics for injectable drugs enhances feasibility. Rising telemedicine usage further accelerates demand. Increasing smartphone penetration supports digital pharmacy expansion. Continuous growth in e-health platforms strengthens long-term outlook.

Amylin Analog Market Regional Analysis

- North America dominated the amylin analog market with the largest revenue share of approximately 41.8% in 2025, characterized by advanced diabetes care infrastructure, high diagnosis rates, strong adoption of injectable biologics, and the presence of major pharmaceutical companies. The region has also witnessed increasing use of amylin analog therapies as adjunct treatments to insulin in both type 1 diabetes and insulin-intensive type 2 diabetes populations

- Patients and healthcare providers in the region highly value improved postprandial glucose control, weight management benefits, and complementary glycemic regulation offered by amylin analog therapies alongside insulin. Growing preference for integrated diabetes management approaches continues to strengthen market demand

- This widespread adoption is further supported by high healthcare expenditure, strong reimbursement frameworks, increasing prevalence of obesity-related diabetes, and growing focus on advanced injectable therapies, establishing amylin analogs as an important component of modern diabetes treatment strategies

U.S. Amylin Analog Market Insight

The U.S. amylin analog market captured the largest revenue share in 2025 within North America, fueled by high diabetes prevalence, strong clinical adoption of advanced biologic therapies, and widespread use of combination insulin–amylin regimens. Healthcare providers are increasingly prioritizing adjunct therapies such as pramlintide to improve glycemic control in patients with uncontrolled postprandial glucose levels. The growing preference for personalized diabetes management plans, combined with robust demand across endocrinology clinics, hospitals, and specialty diabetes centers, further propels the market. Moreover, increasing integration of continuous glucose monitoring systems and digital diabetes management platforms is significantly contributing to market expansion.

Europe Amylin Analog Market Insight

The Europe amylin analog market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising diabetes prevalence, increasing adoption of advanced injectable therapies, and strong healthcare system support for chronic disease management. Growing emphasis on improving long-term glycemic outcomes and reducing diabetes complications is fostering adoption of amylin analogs. European healthcare providers are also drawn to their ability to complement insulin therapy and improve metabolic control. The region is experiencing significant growth across hospitals, specialty clinics, and diabetes care centers, with amylin analogs increasingly included in structured diabetes treatment protocols.

U.K. Amylin Analog Market Insight

The U.K. amylin analog market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising incidence of type 2 diabetes and increasing focus on optimizing insulin therapy outcomes. Additionally, growing awareness among clinicians regarding adjunctive therapies for postprandial glucose control is encouraging adoption. The UK’s strong NHS diabetes care programs and expanding use of specialist endocrinology services are expected to continue stimulating market growth.

Germany Amylin Analog Market Insight

The Germany amylin analog market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing diabetes burden, strong healthcare infrastructure, and demand for innovative biologic therapies. Germany’s well-developed clinical care systems and emphasis on evidence-based treatment promote the adoption of amylin analogs in combination diabetes therapies. The integration of modern diabetes management tools and structured care pathways is also becoming increasingly prevalent, supporting improved patient outcomes.

Asia-Pacific Amylin Analog Market Insight

The Asia-Pacific amylin analog market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rising diabetes prevalence, increasing healthcare expenditure, improving access to advanced biologic therapies, and growing awareness of early glycemic control strategies across China, India, Japan, and Southeast Asia. The region’s rapidly expanding diabetic population and improving diagnostic rates are accelerating demand for advanced treatment options. Furthermore, increasing government healthcare investments and expanding insurance coverage are making biologic diabetes therapies more accessible across both urban and semi-urban populations.

Japan Amylin Analog Market Insight

The Japan amylin analog market is gaining momentum due to the country’s aging population, high diabetes prevalence among elderly groups, and advanced healthcare system. Japanese clinicians place strong emphasis on precise glycemic control, driving adoption of adjunct therapies such as amylin analogs. Integration with structured diabetes care programs and increasing use in combination with insulin therapy is fueling growth. Moreover, demand for therapies that reduce post-meal glucose spikes is expected to rise steadily.

China Amylin Analog Market Insight

The China amylin analog market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large diabetic population, rapid urbanization, expanding healthcare infrastructure, and increasing adoption of advanced diabetes therapies. China is witnessing growing use of insulin-based combination treatments in both hospital and outpatient settings. Government efforts to improve chronic disease management, rising awareness of glycemic control, and expanding availability of biologic drugs are key factors propelling market growth in China.

Amylin Analog Market Share

The Amylin Analog industry is primarily led by well-established companies, including:

- Amylin Pharmaceuticals (U.S.)

- AstraZeneca plc (U.K.)

- Eli Lilly and Company (U.S.)

- Novo Nordisk A/S (Denmark)

- Sanofi S.A. (France)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Boehringer Ingelheim International GmbH (Germany)

- Bayer AG (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Astellas Pharma Inc. (Japan)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Cipla Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Lupin Limited (India)

- Viatris Inc. (U.S.)

- Sandoz Group AG (Switzerland)

- Biocon Limited (India)

Latest Developments in Global Amylin Analog Market

- In April 2021, clinical research published findings on ADO09, a fixed combination of pramlintide (an amylin analog) and insulin A21G, showing improved postprandial glucose control compared to standard insulin therapy in type 1 diabetes patients. This development highlighted renewed interest in amylin-based co-formulations for diabetes management

- In June 2023, Zealand Pharma reported Phase 1 clinical trial results for petrelintide (ZP8396), a long-acting amylin analog, demonstrating meaningful weight loss of approximately 8.6% over 16 weeks, supporting its potential as a next-generation obesity treatment

- In March 2024, Novo Nordisk announced Phase I clinical results for amycretin, a dual amylin and GLP-1 receptor co-agonist, showing strong weight-loss efficacy and advancing it as a next-generation injectable and oral obesity treatment candidate

- In January 2025, Novo Nordisk released Phase 1b/2a clinical trial data for subcutaneous amycretin, confirming sustained weight reduction and acceptable safety profile over 36 weeks, strengthening its position in the amylin-based obesity pipeline

- In March 2025, Roche entered a major licensing agreement with Zealand Pharma to co-develop petrelintide, a long-acting amylin analog, in a deal valued up to several billion dollars. This marked Roche’s strategic entry into the amylin receptor agonist obesity drug market

- In June 2025, Phase III clinical data for cagrilintide (amylin analog) in combination therapy (CagriSema) showed significant weight reduction and metabolic improvements compared to GLP-1 monotherapy, reinforcing amylin analogs as a key future obesity treatment class

- In September 2025, clinical pipeline analyses confirmed that amylin analog therapies such as pramlintide, cagrilintide, and petrelintide are increasingly being positioned as next-generation metabolic treatments either alone or in combination with GLP-1 drugs for obesity and diabetes

- In November 2025, Roche–Zealand Pharma collaboration updates highlighted strong industry momentum in amylin analog development, with petrelintide emerging as a leading candidate in once-weekly obesity injection therapies targeting appetite regulation and weight loss

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.