Global Andersen Disease Treatment Market

Market Size in USD Billion

USD

1.27 Billion

USD

2.05 Billion

2025

2033

USD

1.27 Billion

USD

2.05 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.27 Billion | |

| USD 2.05 Billion | |

| % | |

|

Andersen Disease Treatment Market Size

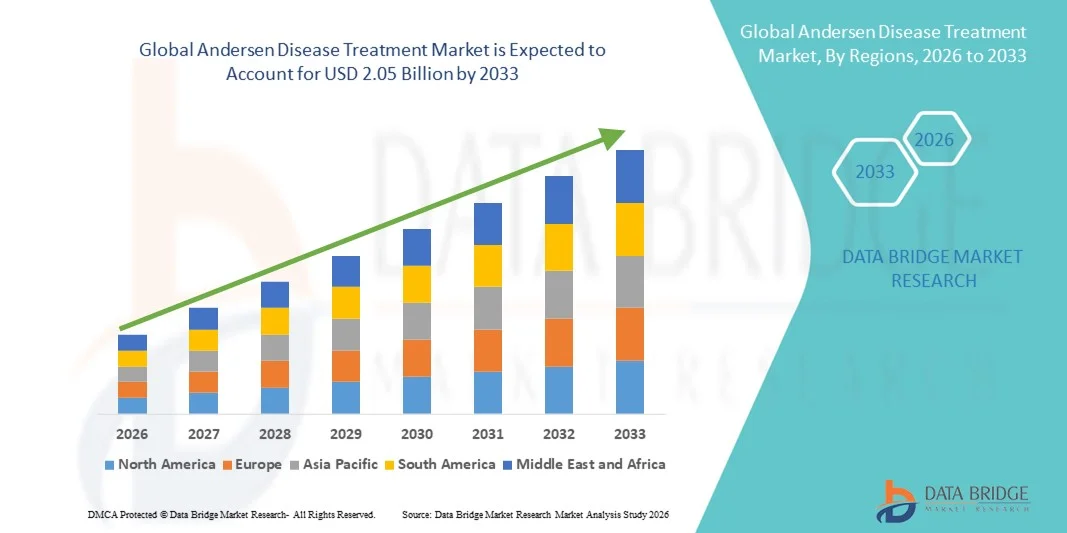

- The global andersen disease treatment market size was valued at USD 1.27 billion in 2025 and is expected to reach USD 2.05 billion by 2033, at a CAGR of 6.20% during the forecast period

- The market growth is largely fueled by rising prevalence of Andersen disease, increasing awareness of rare genetic disorders, and advancements in diagnostic and therapeutic solutions, leading to higher adoption of Andersen Disease Treatment in hospitals, clinics, and specialized care centers

- Furthermore, the growing demand for targeted therapies, including enzyme replacement treatments, gene therapies, and supportive care measures, is driving market expansion, as healthcare providers focus on improving patient outcomes and quality of life through early diagnosis and comprehensive treatment plans

Andersen Disease Treatment Market Analysis

- Andersen Disease Treatment, encompassing therapies for the rare genetic disorder, is witnessing increasing adoption in both clinical and hospital settings due to advancements in diagnostic capabilities, early intervention protocols, and the availability of targeted treatment options, including enzyme replacement therapy and supportive care measures

- The escalating demand for andersen disease treatment is primarily fueled by growing awareness among healthcare professionals and patients, rising incidence of related genetic mutations, and expanding government and private initiatives supporting rare disease research and management

- North America dominated the andersen disease treatment market with the largest revenue share of 43.5% in 2025, driven by well-established healthcare infrastructure, high adoption of advanced therapeutic protocols, and strong presence of key pharmaceutical and biotechnology companies, with the U.S. witnessing substantial growth due to expanding clinical trials, hospital-based therapies, and early adoption of innovative treatment options

- Asia-Pacific is expected to be the fastest growing region in the andersen disease treatment market during the forecast period, registering a CAGR from 2026 to 2033, driven by increasing healthcare investments, rising prevalence of rare genetic disorders, expansion of specialized treatment centers, and improving access to advanced therapies in countries such as China and India

- The children segment dominated the market, with 49.2% revenue in 2025, due to higher prevalence of perinatal and childhood onset cases, requiring early intervention and intensive care. Pediatric hospitals and specialty clinics are key revenue drivers, offering multi-disciplinary treatment approaches

Report Scope and Andersen Disease Treatment Market Segmentation

|

Attributes |

Andersen Disease Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Andersen Disease Treatment Market Trends

Enhanced Patient Outcomes Through Advanced Therapeutic Approaches

- A significant and accelerating trend in the global Andersen disease treatment market is the increasing adoption of integrated therapeutic strategies combining surgery, pharmacological interventions, and supportive care. These approaches are significantly improving patient recovery, reducing disease progression, and enhancing overall quality of life

- For instance, the introduction of combination antimicrobial therapies alongside minimally invasive surgical procedures enables clinicians to target the underlying cause of Andersen Disease while preserving healthy tissues

- Advances in molecular diagnostics and imaging technologies, such as MRI and CT-based assessment, allow for earlier and more precise detection of disease manifestations, improving treatment planning and outcomes

- Personalized medicine approaches, including targeted drug regimens and patient-specific therapy plans, are being increasingly implemented in clinical settings to optimize efficacy and minimize adverse effects

- Integration of multidisciplinary care teams, involving infectious disease specialists, surgeons, and clinical pharmacists, ensures a holistic approach to managing complex cases of Andersen Disease

- The trend towards more precise, timely, and patient-centric treatment protocols is reshaping clinician expectations for disease management, highlighting the importance of evidence-based interventions and continuous monitoring

- Hospitals, specialty clinics, and research institutions are increasingly adopting these advanced protocols to improve treatment outcomes and minimize recurrence rates

Andersen Disease Treatment Market Dynamics

Driver

Increasing Disease Prevalence and Expanding Healthcare Infrastructure

- The rising incidence of Andersen Disease globally is driving the need for more effective therapeutic interventions

- For instance, in April 2025, leading hospitals in North America expanded their Andersen Disease care units to include multidisciplinary teams capable of managing severe and complex cases

- Investments in healthcare infrastructure, advanced diagnostic facilities, and specialized training for clinicians are enabling wider access to effective treatments

- Development of novel therapeutic agents and improved clinical protocols supports adoption and enhances patient outcomes

- Growing awareness among primary care providers and specialists about early detection and intervention further fuels the demand for structured treatment solutions

- Government initiatives and healthcare policies promoting disease management and patient safety are also contributing to market growth

Restraint/Challenge

High Treatment Costs and Limited Access to Specialized Care

- The high cost associated with complex surgical procedures, long-term hospitalization, and specialized pharmacological therapies limits accessibility in certain regions, particularly in developing economies

- Limited availability of experienced clinicians and specialized treatment centers can delay therapy, increasing disease progression and complications

- For instance, in 2023, a study in Southeast Asia highlighted delays in initiating Andersen Disease treatment due to insufficient access to specialized hospitals, resulting in higher morbidity rates among patients

- The requirement for continuous monitoring, multidisciplinary intervention, and individualized therapy plans can also pose logistical and financial challenges for patients

- While ongoing investments are improving healthcare access, disparities in availability of advanced treatment options still restrict market penetration in emerging regions

- Addressing these challenges through infrastructure development, training programs for healthcare providers, and cost-effective therapeutic options is essential for sustained growth of the Andersen Disease Treatment market

Andersen Disease Treatment Market Scope

The market is segmented on the basis of type, treatment, demographic, symptoms, diagnosis, end-users, and distribution channel.

- By Type

On the basis of type, the Andersen Disease Treatment market is segmented into Perinatal Onset and Childhood Onset. The Perinatal Onset segment dominated the market, accounting for 46.5% revenue share in 2025, due to its early manifestation of symptoms and high clinical severity. Perinatal cases often require immediate medical intervention and monitoring in specialized neonatal and pediatric centers, driving higher hospital utilization and treatment costs. The segment is characterized by rapid disease progression, which necessitates timely diagnosis and intensive treatment, including liver transplantation, dietary therapy, and supportive care. Clinical awareness and early genetic screening programs in many regions have improved early detection rates, further strengthening market dominance. Perinatal cases tend to have a higher dependency on multidisciplinary care teams, including hepatologists, nutritionists, and genetic counselors, contributing to revenue. Hospital protocols prioritize early intervention to reduce long-term complications such as cirrhosis or hepatosplenomegaly. Research initiatives focusing on neonatal liver diseases enhance treatment efficacy and patient outcomes, supporting sustained demand. Insurance and government healthcare coverage for neonatal care increase adoption of available therapies. Hospitals and specialized clinics invest in advanced diagnostics to manage perinatal cases effectively. Parental awareness campaigns emphasize early screening, improving timely hospital visits. The availability of high-cost therapies like liver transplantation further boosts revenue contribution. Multicenter treatment programs also help maintain segment leadership.

The Childhood Onset segment is expected to witness the fastest CAGR of 18.9% from 2026 to 2033, driven by rising awareness, improved diagnostic facilities, and increasing access to treatment in emerging regions. Childhood cases often present with delayed symptoms, including growth retardation, cardiomyopathy, or metabolic disturbances, necessitating a combination of dietary therapy, medication, and lifestyle management. Clinics and hospitals are increasingly investing in pediatric specialty units to manage these cases efficiently. Advancements in gene testing and early intervention protocols enhance outcomes and reduce disease complications, fueling segment growth. Patient advocacy groups and awareness campaigns are improving early recognition of symptoms. Home-based care programs complement hospital treatment for non-critical cases, expanding the reach of therapy. Insurance coverage for chronic management, including medication and dietary support, supports adoption. Hospitals adopt integrated care approaches combining genetic counseling and exercise programs for pediatric patients. Collaboration between research institutes and pediatric centers promotes innovative treatment strategies. Telemedicine solutions improve adherence to therapy schedules. Rising birth rates in some regions contribute to a larger patient pool. Education programs for caregivers increase effective disease management at home. Government initiatives supporting pediatric healthcare enhance segment penetration. Advanced monitoring and follow-up programs ensure improved treatment outcomes, accelerating CAGR.

- By Treatment

On the basis of treatment, the market is segmented into liver transplantation, dietary therapy, exercise, genetic counseling, and medication. The Liver Transplantation segment dominated the market, accounting for 44.7% revenue in 2025, due to its status as the most definitive treatment for severe cases of Andersen Disease. Liver transplantation offers a curative approach for end-stage liver complications, including cirrhosis and severe hepatosplenomegaly. Hospitals with transplant units drive high revenue due to complex surgical procedures, post-operative care, and long-term follow-ups. The segment benefits from advanced surgical technologies and improved organ preservation techniques, enhancing success rates. Insurance coverage and government support for transplantation programs increase adoption. Multidisciplinary care teams ensure comprehensive management, which further strengthens hospital revenues. Hospitals implement stringent pre- and post-transplant protocols to maximize patient survival. Global awareness of liver transplantation as a life-saving therapy encourages patient referrals to specialized centers. Continuous research on immunosuppressive therapies and post-transplant care improves outcomes. Public awareness campaigns support early evaluation and listing for transplantation. Pediatric transplant programs contribute significantly to revenue share in perinatal onset cases. Regulatory frameworks supporting organ donation programs boost segment growth.

The Dietary Therapy segment is expected to witness the fastest CAGR of 19.3% from 2026 to 2033, driven by the growing emphasis on non-invasive management of metabolic complications. Dietary therapy is crucial for managing symptoms such as atrophy, cardiomyopathy, and metabolic imbalance. Clinics and hospitals increasingly recommend individualized nutrition plans in combination with medication and exercise. Home-based dietary programs improve patient adherence and reduce hospital visits. Advances in nutritional science and specialized food products for metabolic disorders support rapid adoption. Pediatric patients benefit from tailored diets to manage growth and development effectively. Telehealth and remote dietary consultation services expand reach to patients in remote areas. Insurance policies covering nutritional therapy contribute to increased utilization. Hospitals integrate dietary therapy into broader treatment protocols to ensure holistic care. Public health campaigns emphasize dietary management to prevent disease progression. Research on nutritional interventions continues to improve outcomes. Collaboration between dieticians, genetic counselors, and clinicians ensures comprehensive patient management. Online platforms for dietary monitoring facilitate adherence and patient engagement.

- By Demographic

On the basis of demographic, the market is segmented into children and adults. The children segment dominated the market, with 49.2% revenue in 2025, due to higher prevalence of perinatal and childhood onset cases, requiring early intervention and intensive care. Pediatric hospitals and specialty clinics are key revenue drivers, offering multi-disciplinary treatment approaches. Early diagnosis and management in children reduce complications such as cirrhosis and cardiomyopathy. Hospitals adopt comprehensive care programs integrating dietary therapy, medication, exercise, and genetic counseling. Parental awareness campaigns support timely hospital visits and therapy adherence. Telehealth programs enhance monitoring and compliance in pediatric patients. Government and NGO programs targeting pediatric metabolic disorders further drive adoption. Insurance coverage for pediatric treatments encourages hospital visits. Specialized training for pediatric healthcare providers improves treatment quality. Home healthcare services complement hospital care for chronic management. Nutritional and exercise programs are tailored to growth requirements. Public-private partnerships expand access to specialized treatment centers. Research into pediatric gene therapies continues to expand options.

The adults segment is expected to witness the fastest CAGR of 18.5% from 2026 to 2033, fueled by the rising diagnosis of late-onset metabolic and liver complications in previously undiagnosed patients. Adults increasingly access liver transplantation, medication, and lifestyle management programs. Hospitals are expanding adult metabolic disorder units and specialized outpatient clinics. Adult patient awareness campaigns encourage early symptom recognition. Telemedicine adoption supports remote management and adherence. Insurance coverage for adult chronic care encourages treatment uptake. Workplace wellness and health monitoring programs support early detection. Clinics focus on integrated care combining dietary, exercise, and medication protocols. Research into adult-onset gene therapies enhances treatment options. Home healthcare services complement hospital-based care for adult patients. Chronic disease prevalence and lifestyle-related complications increase therapy demand. Multi-specialty care teams optimize adult treatment outcomes. Online platforms provide education and support for adult patients.

- By Symptoms

On the basis of symptoms, the market is segmented into cirrhosis, hepatosplenomegaly, ascites, esophageal varices, cardiomyopathy, atrophy, and others. The cirrhosis segment dominated the market, accounting for 45.9% revenue in 2025, due to its high clinical severity and association with late-stage disease requiring liver transplantation. Hospitals generate revenue from surgical interventions, post-operative care, and long-term monitoring. Early intervention protocols, imaging, and laboratory tests improve outcomes and hospital efficiency. Public awareness campaigns encourage early diagnosis to prevent cirrhosis progression. Multidisciplinary teams, including hepatologists, surgeons, and nutritionists, contribute to comprehensive care. Insurance coverage and government healthcare initiatives support adoption. Advanced diagnostic techniques like MRI and gene testing facilitate early detection. Pediatric and adult cases both contribute to segment growth. Hospital pharmacies supply associated medications, steroids, and nutritional supplements. Telehealth and home monitoring enhance adherence and reduce complications. Clinical research improves treatment efficacy and survival rates.

The atrophy segment is expected to witness the fastest CAGR of 17.8% from 2026 to 2033, driven by rising recognition of musculoskeletal and cardiac complications requiring integrated care programs. Pediatric and adult patients with atrophy require dietary therapy, exercise, and medication, creating a multi-pronged revenue stream. Home healthcare adoption supports long-term therapy adherence. Hospitals and clinics integrate physiotherapy and nutritional support to mitigate atrophy effects. Research into novel rehabilitation protocols enhances outcomes. Telemedicine programs support continuous monitoring and patient engagement. Awareness programs among caregivers encourage early intervention. Insurance coverage for rehabilitation therapies accelerates adoption. Clinics collaborate with hospitals for follow-up care. Digital tools and mobile apps facilitate exercise monitoring. Hospital pharmacies provide supportive supplements to improve muscle function. Growth in chronic metabolic disorders drives segment adoption. Early intervention programs reduce complications, sustaining revenue growth.

- By Diagnosis

On the basis of diagnosis, the market is segmented into biopsy, blood tests, urine tests, MRI, gene testing, and others. The gene testing segment dominated the market, with 46.8% revenue in 2025, owing to its ability to identify genetic mutations early, enabling timely intervention and treatment planning. Hospitals and specialized clinics invest in advanced genetic labs and testing protocols. Early diagnosis through gene testing supports preemptive dietary therapy, medication, and monitoring programs. Multidisciplinary treatment planning enhances patient outcomes. Public awareness and newborn screening programs improve test adoption. Insurance coverage supports high-cost gene testing, encouraging utilization. Hospitals integrate gene testing with routine diagnostics for comprehensive evaluation. Gene testing facilitates personalized treatment plans, improving efficacy. Telehealth platforms support remote genetic counseling. Advanced laboratory equipment enhances testing accuracy and speed. Pediatric and adult populations both benefit from early genetic screening. Clinical research and studies continually improve test reliability.

The urine tests segment is expected to witness the fastest CAGR of 18.2% from 2026 to 2033, driven by the convenience, affordability, and early detection capabilities of urine-based biomarkers. Clinics and hospitals adopt urine tests as non-invasive, rapid screening tools. Urine test protocols complement blood tests and gene testing for monitoring disease progression. Home healthcare kits increase patient compliance. Pediatric and adult patients benefit from easy sample collection. Laboratories invest in automation to improve throughput and accuracy. Early intervention based on urine test results enhances treatment outcomes. Insurance coverage supports adoption in routine monitoring. Awareness campaigns highlight non-invasive testing benefits. Telehealth programs integrate test results for remote care planning. Research on novel urine biomarkers enhances specificity. Hospital pharmacies supply reagents and kits, ensuring reliable availability. Online platforms enable remote test ordering and result interpretation.

- By End-Users

On the basis of end-users, the market is segmented into clinic, hospital, and others. The hospitals segment dominated the market, accounting for 52.1% revenue in 2025, due to their capacity to deliver complex treatment modalities, including liver transplantation, genetic counseling, and intensive care. Hospitals are equipped with advanced diagnostics, surgical units, and multidisciplinary teams, ensuring comprehensive treatment. Insurance coverage and government healthcare programs facilitate hospital adoption. Hospitals manage high patient inflows from perinatal and childhood onset cases. Telemedicine support enhances follow-up care. Specialized pediatric and adult units strengthen market leadership. Hospitals maintain strategic partnerships with diagnostic and pharmaceutical providers. Awareness programs encourage early hospital visits. Hospital pharmacies provide critical medications and dietary support. Multicenter care programs improve treatment outcomes. Advanced post-operative care protocols support sustained revenue. Hospitals integrate home healthcare for long-term management.

The clinics segment is expected to witness the fastest CAGR of 19.0% from 2026 to 2033, driven by rising outpatient care for mild and chronic cases, genetic counseling, and dietary therapy programs. Clinics provide accessible, convenient treatment options for follow-up care. Telehealth platforms complement in-clinic services. Clinics increasingly collaborate with hospitals for specialized interventions. Home-based monitoring and therapy support drive clinic adoption. Awareness programs promote early screening at local clinics. Insurance coverage for outpatient services encourages utilization. Clinics integrate exercise, dietary, and medication management programs. Pediatric and adult patient populations benefit from regular clinic follow-ups. Technology-enabled patient tracking enhances compliance. Clinics expand services to include genetic counseling and diagnostic support. Public-private partnerships improve clinic infrastructure. Clinics play a vital role in post-transplant monitoring, supporting growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market, with 49.3% revenue in 2025, due to immediate access to critical medications such as steroids, dietary supplements, and medications for liver support. Hospitals ensure availability during acute care and post-transplant therapy. Bulk procurement and in-house distribution enhance operational efficiency. Insurance coverage facilitates hospital pharmacy adoption. Advanced inventory systems improve drug management. Multidisciplinary teams rely on hospital pharmacies for timely supply. Public awareness campaigns encourage hospital-based dispensing. Pediatric and adult care require specialized formulations available in hospital pharmacies. Emergency care protocols prioritize hospital pharmacy readiness. Collaboration with pharmaceutical companies ensures steady supply. Hospitals integrate pharmacies with diagnostic and clinical departments. Strategic procurement policies enhance cost efficiency.

The online pharmacy segment is expected to witness the fastest CAGR of 20.1% from 2026 to 2033, driven by growing e-prescription adoption, home delivery, and telehealth consultations. Online pharmacies expand access to patients in remote and underserved regions. Integration with hospital and clinic systems enables seamless prescription fulfillment. Digital apps and reminders improve adherence. Online pharmacies offer subscription-based medication delivery. Specialized medications for pediatric and adult patients are more accessible. Cold-chain logistics ensure drug safety. Insurance and reimbursement programs increasingly cover online delivery. Telehealth and mobile health platforms enhance patient convenience. E-commerce penetration accelerates market growth. Online pharmacies reduce hospital burden while improving therapy compliance. Remote genetic counseling and dietary support are integrated with online platforms. Growing patient preference for home-based care drives segment adoption.

Andersen Disease Treatment Market Regional Analysis

- North America dominated the Andersen Disease Treatment market with the largest revenue share of 43.5% in 2025

- Driven by well-established healthcare infrastructure, high adoption of advanced therapeutic protocols, and strong presence of key pharmaceutical and biotechnology companies

- The market witnessed substantial growth due to expanding clinical trials, hospital-based therapies, and early adoption of innovative treatment options

U.S. Andersen Disease Treatment Market Insight

The U.S. Andersen Disease Treatment market captured the largest revenue share in 2025 within North America, fueled by advanced hospital networks, strong clinical research capabilities, and rapid uptake of novel therapeutic interventions. Increasing investments in early diagnosis, multidisciplinary care, and specialized treatment centers further propelled the market’s expansion, particularly in managing complex and rare cases.

Europe Andersen Disease Treatment Market Insight

The Europe Andersen Disease Treatment market is projected to expand at a substantial CAGR throughout the forecast period, driven by stringent healthcare standards, growing prevalence of genetic and rare disorders, and rising adoption of innovative therapeutic approaches. Key markets such as Germany, France, and Italy are witnessing increasing hospital-based therapy adoption and clinical trial activities for advanced treatment protocols.

U.K. Andersen Disease Treatment Market Insight

The U.K. Andersen Disease Treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by investments in specialized healthcare facilities and early access programs for innovative treatments. The country’s emphasis on clinical research, coupled with rising awareness of rare disease management, is driving increased adoption of advanced therapeutic interventions.

Germany Andersen Disease Treatment Market Insight

The Germany Andersen Disease Treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced hospital infrastructure, a strong focus on personalized medicine, and high adoption of novel treatment protocols. Germany’s emphasis on research and development, combined with public and private healthcare investments, is fostering growth in the management of rare and complex disorders.

Asia-Pacific Andersen Disease Treatment Market Insight

The Asia-Pacific Andersen Disease Treatment market is poised to grow at the fastest CAGR of 23.8% during the forecast period of 2026 to 2033, driven by increasing healthcare investments, rising prevalence of rare genetic disorders, expansion of specialized treatment centers, and improving access to advanced therapies in countries such as China and India. Government initiatives supporting rare disease care and infrastructure development are further boosting market growth.

Japan Andersen Disease Treatment Market Insight

The Japan Andersen Disease Treatment market is gaining momentum due to strong healthcare infrastructure, emphasis on early diagnosis, and adoption of advanced therapeutic protocols. Expansion of specialized care centers and ongoing clinical trials for innovative treatments are further contributing to growth in the management of complex cases.

China Andersen Disease Treatment Market Insight

The China Andersen Disease Treatment market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rising healthcare spending, improved access to advanced treatment options, and growing awareness of rare disease management. Expansion of specialized medical centers and ongoing clinical research initiatives are supporting market growth across the country.

Andersen Disease Treatment Market Share

The Andersen Disease Treatment industry is primarily led by well-established companies, including:

• Ultragenyx Pharmaceutical Inc. (U.S.)

• Sanofi (France)

• Fresenius Kabi (Germany)

• Takeda Pharmaceutical Company (Japan)

• Novartis (Switzerland)

• Rare Disease Therapeutics Ltd. (U.S.)

• Vertex Pharmaceuticals (U.S.)

• Sobi (Sweden)

• Biomarin Pharmaceutical Inc. (U.S.)

• Amicus Therapeutics (U.S.)

• Avrobio Inc. (U.S.)

Latest Developments in Global Andersen Disease Treatment Market

- In February 2023, a Clinical Practice Guideline for GSD IV (including its adult form, APBD) was published, providing the first comprehensive, expert-backed recommendations on diagnosis and management — covering imaging, genetic testing, and long-term follow-up

- In August 2024, researchers from Duke University published a “natural history” study on hepatic GSD IV, revealing for the first time that liver disease progression in GSD IV is highly variable. Some patients progress rapidly to liver failure, while others remain stable for decades

- In March 2025, the Adult Polyglucosan Body Disease (APBD) Research Foundation shared a powerful patient story: a mother described her daughter’s diagnosis of GSD IV, highlighting how early genetic testing (GBE1) made the diagnosis possible and how the patient and family want to raise awareness and push for therapies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.