Global Anesthesia Dolorosa Treatment Market

Market Size in USD Billion

USD

3.91 Billion

USD

5.31 Billion

2024

2032

USD

3.91 Billion

USD

5.31 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.91 Billion | |

| USD 5.31 Billion | |

| % | |

|

Anesthesia Dolorosa Treatment Market Size

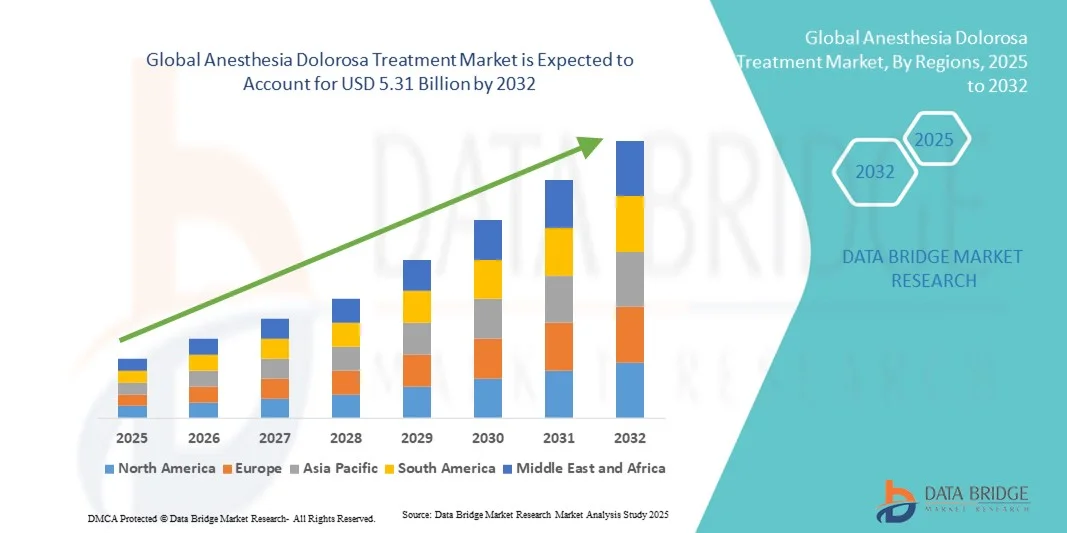

- The global anesthesia dolorosa treatment market size was valued at USD 3.91 billion in 2024 and is expected to reach USD 5.31 billion by 2032, at a CAGR of 3.9% during the forecast period

- The market growth is largely fueled by the rising prevalence of chronic neuropathic pain conditions and the increasing need for effective treatment options for facial nerve injuries and post-surgical complications, which are key contributors to the incidence of anesthesia dolorosa

- Furthermore, ongoing advancements in neuromodulation, nerve repair therapies, and pain management drugs are significantly enhancing patient outcomes, driving the adoption of innovative and personalized treatment approaches

Anesthesia Dolorosa Treatment Market Analysis

- Anesthesia Dolorosa Treatment, encompassing both pharmacological and non-pharmacological approaches for managing chronic neuropathic facial pain, is becoming an increasingly vital aspect of modern pain management and neurology care in both clinical and home-based settings due to its focus on improving patient comfort, enhancing quality of life, and reducing post-surgical complications

- The escalating demand for anesthesia dolorosa treatment is primarily fueled by the rising incidence of facial nerve damage following surgical procedures, growing awareness of neuropathic pain disorders, and the increasing availability of advanced pain management techniques, including neuromodulation and targeted nerve stimulation

- North America dominated the anesthesia dolorosa treatment market with the largest revenue share of 40% in 2024, supported by well-established healthcare infrastructure, strong presence of leading pharmaceutical and medical device companies, and high rates of diagnosis and treatment of neuropathic facial pain. The U.S. accounted for the majority of this share due to active clinical research, availability of specialized pain centers, and early adoption of innovative neuromodulation therapies

- Asia-Pacific is expected to be the fastest-growing region in the anesthesia dolorosa treatment market during the forecast period, projected to register a CAGR owing to increasing healthcare investments, rising awareness of chronic pain management, and growing access to advanced neurotherapeutic solutions in countries such as China, Japan, and India

- The oral segment dominated the market with a revenue share of 72.5% in 2024, driven by the high adoption of oral formulations such as gabapentin, pregabalin, and tricyclic antidepressants for long-term neuropathic pain management

Report Scope and Anesthesia Dolorosa Treatment Market Segmentation

|

Attributes |

Anesthesia Dolorosa Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Anesthesia Dolorosa Treatment Market Trends

Advancements in Neurostimulation and Pain Modulation Therapies

- A major and accelerating trend in the global anesthesia dolorosa treatment market is the growing integration of advanced neuromodulation and pain management technologies such as spinal cord stimulation (SCS), deep brain stimulation (DBS), and peripheral nerve stimulation (PNS). These approaches are redefining chronic neuropathic pain management by offering targeted relief for patients who do not respond to conventional medications

- For instance, in March 2024, Medtronic announced the expansion of its neurostimulation portfolio with next-generation SCS devices designed to deliver personalized pain modulation for craniofacial neuropathic pain, including Anesthesia Dolorosa. This innovation highlights the growing reliance on implantable neurotechnology in managing complex nerve pain disorders

- The market is witnessing an increasing preference for non-opioid and minimally invasive pain management therapies due to concerns over opioid dependency and long-term side effects of pharmacological treatments

- Advanced imaging and neuronavigation techniques are enhancing the accuracy of nerve-targeted interventions, improving patient outcomes and procedural safety

- In addition, ongoing clinical research focusing on understanding the trigeminal nerve pathways and pain transmission mechanisms has paved the way for more precise neuromodulation-based treatments

- This trend toward technologically enhanced pain modulation therapies underscores the shift toward personalized and device-based management strategies in the treatment of Anesthesia Dolorosa, with companies such as Abbott Laboratories and Boston Scientific leading advancements in this field

Anesthesia Dolorosa Treatment Market Dynamics

Driver

Rising Prevalence of Neuropathic Pain and Increasing Adoption of Advanced Pain Management Devices

- The growing incidence of nerve injury-related facial pain, along with a surge in cases following neurosurgical procedures and trauma, is a key driver propelling the Anesthesia Dolorosa Treatment market forward

- For instance, in May 2023, Abbott received U.S. FDA approval for its Proclaim XR neurostimulation system to address chronic facial neuropathic pain, significantly expanding its therapeutic indications. Such advancements are creating strong momentum in device-based treatment adoption

- Patients and healthcare providers are increasingly turning toward non-invasive and device-assisted treatment modalities due to limited efficacy of pharmacological therapies in chronic neuropathic pain

- Furthermore, technological innovations in neuromodulation and the availability of rechargeable, long-lasting implants are enhancing treatment adherence and long-term cost efficiency

- Comprehensive rehabilitation programs integrating nerve blocks, physiotherapy, and neurostimulation are gaining traction, leading to improved multidisciplinary management of the condition

- With increasing awareness about advanced pain relief options and supportive reimbursement for device-based therapies in developed markets, the global demand for effective Anesthesia Dolorosa treatments is expected to continue rising steadily over the forecast period

Restraint/Challenge

High Cost of Treatment and Limited Awareness Among Patients and Clinicians

- The high cost associated with neuromodulation devices, surgical interventions, and long-term maintenance remains a significant restraint in the Anesthesia Dolorosa Treatment market, particularly in low- and middle-income countries

- For instance, the total expense for neurostimulation implantation and post-surgical care can range between USD 25,000 and USD 60,000 per patient, limiting accessibility for large portions of the global population

- In addition, the rarity of Anesthesia Dolorosa often results in delayed diagnosis or misdiagnosis, reducing the likelihood of early and effective treatment

- A lack of specialized pain management centers and limited training among clinicians on advanced interventional procedures further hampers widespread adoption of device-based therapies

- Moreover, reimbursement gaps and varying insurance policies across regions make it difficult for patients to afford high-end therapeutic solutions

- To overcome these challenges, manufacturers and healthcare providers are focusing on developing cost-efficient neuromodulation systems, expanding clinical education programs, and increasing awareness of targeted pain management strategies, which are vital for sustaining market growth

Anesthesia Dolorosa Treatment Market Scope

The market is segmented on the basis of symptoms, treatment, route of administration, distribution channel, and end user.

- By Symptoms

On the basis of symptoms, the Anesthesia Dolorosa Treatment market is segmented into unilateral facial pain and numbness along the trigeminal nerve. The unilateral facial pain segment dominated the market with the largest revenue share of 61.3% in 2024, driven by the high prevalence of persistent neuropathic pain following trigeminal nerve injury or neurosurgical procedures. The condition is often chronic and debilitating, leading patients to seek advanced medical intervention and pharmacological management. Increased awareness among healthcare providers regarding pain differentiation and specialized pain mapping techniques has contributed to the diagnosis and treatment rate. Furthermore, the availability of effective pain-modulating drugs such as gabapentin and amitriptyline, coupled with technological improvements in nerve monitoring, supports sustained segment growth. The surge in clinical trials focusing on neuropathic facial pain further strengthens this segment’s leading position. The increasing number of patients undergoing radiotherapy or surgery for head and neck cancers has also indirectly contributed to rising cases of Anesthesia Dolorosa-associated facial pain, necessitating effective pain management approaches.

The numbness along the trigeminal nerve segment is projected to witness the fastest CAGR of 8.4% from 2025 to 2032, owing to increasing recognition of trigeminal sensory dysfunction as a post-procedural complication. Advancements in neuroimaging, such as MRI and 3D nerve mapping, have enhanced clinicians’ ability to detect subtle nerve impairments early. Growing research attention toward sensory restoration and neuroprotective interventions is accelerating innovation in this area. Moreover, patients’ demand for improved quality of life and relief from sensory loss-related discomfort is fostering the adoption of specialized therapies. Increased use of nerve-stimulating devices and regenerative medicine for sensory repair are expected to further drive this segment’s growth. Clinical collaboration between neurology and maxillofacial surgery departments is also improving patient outcomes. The trend toward personalized treatment based on nerve injury patterns and biomarker analysis adds further momentum to this segment.

- By Treatment

On the basis of treatment, the market is segmented into gabapentin and surgery. The gabapentin segment dominated the market with a revenue share of 68.9% in 2024, primarily due to its well-established efficacy as a first-line therapy for neuropathic pain management. Gabapentin’s mechanism of modulating calcium channel activity reduces abnormal nerve signaling, providing significant relief for Anesthesia Dolorosa patients. Physicians often favor gabapentin over opioid-based treatments because of its lower dependency risk and broader safety profile. The drug’s widespread availability in oral and extended-release formulations enhances patient adherence and convenience. The growing preference for combination therapies involving gabapentin and antidepressants is further boosting market penetration. Increasing insurance coverage and inclusion in global pain management protocols continue to strengthen this segment’s dominance. Furthermore, expanding distribution networks and the availability of cost-effective generics make it accessible across both developed and emerging economies.

The surgery segment is expected to witness the fastest CAGR of 9.1% from 2025 to 2032, driven by increasing advancements in microsurgical and neuromodulation techniques. Procedures such as microvascular decompression, nerve grafting, and peripheral nerve stimulation are being increasingly utilized for cases unresponsive to pharmacological treatment. The use of image-guided and robot-assisted surgical systems has improved precision, outcomes, and recovery times. A rising number of neurosurgeons specializing in pain-related cranial nerve surgeries is also supporting the segment’s expansion. Growing research into nerve regeneration and minimally invasive repair procedures is broadening surgical applicability. In addition, collaborations between medical device manufacturers and hospitals are helping introduce innovative implants for nerve modulation. Increasing patient willingness to opt for surgical correction after long-term medication failure further supports growth. The rising global prevalence of treatment-resistant neuropathic conditions continues to make surgery an essential intervention option.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral and injectable. The oral segment dominated the market with a revenue share of 72.5% in 2024, driven by the high adoption of oral formulations such as gabapentin, pregabalin, and tricyclic antidepressants for long-term neuropathic pain management. The oral route is favored for its non-invasive nature, cost efficiency, and ease of dosing, especially in outpatient and homecare settings. Pharmaceutical advancements have improved bioavailability and sustained-release delivery, enhancing therapeutic consistency. Patients prefer oral drugs for chronic therapy due to reduced hospital visits and convenience. Widespread availability of generics across retail pharmacies and favorable reimbursement coverage in developed economies further consolidate this segment’s dominance. In addition, clinical trials focusing on newer oral neuropathic pain modulators continue to expand the product pipeline, ensuring future growth stability.

The injectable segment is anticipated to register the fastest CAGR of 8.8% from 2025 to 2032, driven by growing use in hospital-based settings for patients with severe or refractory pain. Injectable formulations, including nerve blocks and corticosteroid injections, offer immediate and localized relief for intense pain episodes. Increasing preference for targeted delivery methods to avoid systemic side effects is fostering clinical adoption. Hospitals and pain clinics are increasingly integrating image-guided injection procedures to enhance precision and reduce complications. Moreover, advancements in biomaterial-based injectables and extended-release formulations are extending therapeutic duration. Rising research into nerve-regenerative injectables and growth factor-based pain therapies adds new potential to this route. The increasing number of clinical centers offering outpatient injection therapy programs also supports segment expansion.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and mail order pharmacies. The hospital pharmacies segment dominated the market with the largest revenue share of 58.6% in 2024, driven by the higher concentration of patients receiving inpatient and surgical treatment for Anesthesia Dolorosa. Hospitals serve as key points of access for both prescribed pain medications and advanced injectable therapies. Centralized medication management ensures regulatory compliance, especially for controlled substances used in neuropathic pain. The presence of specialized pain management units within hospitals enhances prescription rates. Furthermore, the availability of pharmacists trained in neuropathic pain therapy contributes to safe and effective medication administration. Partnerships between hospital systems and pharmaceutical companies facilitate consistent drug availability. Increasing patient reliance on multidisciplinary care within hospitals further sustains this segment’s dominance.

The mail order pharmacies segment is projected to witness the fastest CAGR of 9.4% from 2025 to 2032, propelled by the rapid expansion of telemedicine and digital pharmacy services. Patients suffering from chronic neuropathic pain increasingly prefer home-based delivery models for convenience and privacy. Digital platforms allow automated prescription refills and doorstep delivery, minimizing hospital visits. The COVID-19 pandemic accelerated e-pharmacy adoption, creating a lasting behavioral shift toward online medication procurement. Global e-commerce integration and improved cold chain logistics for temperature-sensitive injectables also support growth. Furthermore, increasing collaboration between healthcare providers and online pharmacy networks ensures compliance with treatment guidelines. Growing investment in cybersecurity and data privacy reinforces consumer confidence in this channel.

- By End User

On the basis of end user, the market is segmented into hospitals, laboratories, clinics, therapeutic usage, and others. The hospitals segment accounted for the largest market share of 54.8% in 2024, driven by the availability of multidisciplinary pain management programs and advanced diagnostic facilities. Hospitals remain the primary treatment centers for Anesthesia Dolorosa, where patients benefit from integrated pharmacological and surgical care. The presence of neurology and neurosurgery departments supports early detection and intervention. Hospitals also have access to specialized imaging technologies essential for diagnosing trigeminal nerve damage. The ability to manage complex cases and monitor treatment outcomes enhances trust in hospital-based care. Reimbursement support and government funding for chronic pain research further sustain hospital leadership in this market. Growing collaborations between tertiary hospitals and research institutions continue to expand the range of available therapies.

The clinics segment is expected to witness the fastest CAGR of 8.6% from 2025 to 2032, as specialized pain and neurology clinics gain popularity for outpatient management. Clinics offer cost-effective care and faster service delivery compared to hospitals. The rise in private pain clinics equipped with advanced diagnostic tools is expanding accessibility. Increased patient awareness about targeted pain management and individualized therapy drives traffic to these centers. Clinics are also embracing digital health records and teleconsultation services for continuous monitoring. Collaboration with pharmaceutical and device companies enables clinics to offer the latest treatments. The global trend toward decentralizing healthcare from hospitals to specialized clinics further supports sustained growth in this segment.

Anesthesia Dolorosa Treatment Market Regional Analysis

- North America dominated the anesthesia dolorosa treatment market with the largest revenue share of 40% in 2024, supported by a well-established healthcare infrastructure, strong presence of leading pharmaceutical and medical device companies, and high diagnosis and treatment rates for neuropathic facial pain

- The region’s dominance is further strengthened by ongoing advancements in neuromodulation and targeted drug delivery systems aimed at managing refractory facial pain cases

- Consumers in this region also benefit from early access to novel pain management therapies, supported by favorable reimbursement structures and government initiatives that promote chronic pain awareness and treatment optimization

U.S. Anesthesia Dolorosa Treatment Market Insight

The U.S. anesthesia dolorosa treatment market captured the largest revenue share in 2024 within North America, driven by active clinical research, the availability of specialized pain and neurosurgical centers, and early adoption of innovative neuromodulation therapies. The presence of key industry players, such as Medtronic, Abbott, and Boston Scientific, accelerates the commercialization of advanced spinal cord and trigeminal nerve stimulation devices. In addition, a growing patient pool with chronic post-surgical neuropathic pain and increasing preference for minimally invasive therapeutic options continue to propel market growth.

Europe Anesthesia Dolorosa Treatment Market Insight

The Europe anesthesia dolorosa treatment market is projected to grow at a steady CAGR during the forecast period, primarily supported by strong healthcare infrastructure, widespread access to pain management specialists, and increasing adoption of non-opioid and interventional pain therapies. European countries emphasize clinical protocols for neuropathic facial pain, while regulatory support for novel neuromodulation devices further strengthens regional adoption. Rising collaboration among hospitals and research institutions across Germany, France, and the U.K. contributes to technological advancements and improved patient outcomes.

U.K. Anesthesia Dolorosa Treatment Market Insight

The U.K. anesthesia dolorosa treatment market is expected to witness significant expansion during the forecast period, fueled by increasing awareness of chronic facial pain syndromes and advancements in nerve repair and stimulation therapies. A robust healthcare system supported by the National Health Service (NHS) ensures patient access to advanced diagnostic tools and treatment modalities. The growing trend toward personalized pain management approaches and government funding for neurorehabilitation research are expected to bolster market growth.

Germany Anesthesia Dolorosa Treatment Market Insight

The Germany anesthesia dolorosa treatment market is anticipated to record notable growth due to a strong focus on technological innovation, adoption of cutting-edge neuromodulation systems, and the presence of leading device manufacturers. Increasing patient preference for non-invasive pain therapies and a growing number of multidisciplinary pain clinics contribute to the country’s market expansion. Moreover, continuous R&D investment in neural interface technologies supports Germany’s position as a key hub for neurotherapeutic advancements.

Asia-Pacific Anesthesia Dolorosa Treatment Market Insight

The Asia-Pacific anesthesia dolorosa treatment market is expected to be the fastest-growing region during the forecast period, projected to register a high CAGR driven by increasing healthcare investments, rising awareness of chronic pain management, and expanding access to advanced neurotherapeutic solutions in countries such as China, Japan, and India. Rapid urbanization, expanding healthcare coverage, and growing government support for medical technology adoption are catalyzing regional growth. The region’s strengthening pharmaceutical manufacturing capabilities and emerging clinical research collaborations are further boosting availability and affordability of Anesthesia Dolorosa treatment options.

Japan Anesthesia Dolorosa Treatment Market Insight

The Japan anesthesia dolorosa treatment market is expanding steadily, propelled by the country’s advanced medical infrastructure, aging population, and growing prevalence of chronic pain conditions. The integration of neuromodulation therapies into mainstream clinical practice and supportive reimbursement policies contribute to Japan’s market growth. Furthermore, increasing collaboration between domestic and international device manufacturers is enhancing the development of precision-targeted pain management solutions.

China Anesthesia Dolorosa Treatment Market Insight

The China anesthesia dolorosa treatment market accounted for the largest revenue share in the Asia-Pacific region in 2024, driven by a rapidly expanding healthcare sector, technological advancements, and rising awareness of neuropathic pain disorders. The government’s ongoing investments in healthcare innovation and digital medicine are fostering the availability of affordable treatment solutions. In addition, the growing participation of Chinese research institutions in global clinical trials and partnerships with multinational pain management companies are expected to accelerate market expansion across both urban and secondary care centers.

Anesthesia Dolorosa Treatment Market Share

The Anesthesia Dolorosa Treatment industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Novartis AG (Switzerland)

- GSK plc (U.K.)

- AstraZeneca plc (U.K.)

- Eli Lilly and Company (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Merck & Co., Inc. (U.S.)

- Grünenthal GmbH (Germany)

- Biogen Inc. (U.S.)

- Bayer AG (Germany)

- Endo International plc (Ireland)

- Mallinckrodt Pharmaceuticals (U.K.)

- Dr. Reddy’s Laboratories Ltd. (India)

Latest Developments in Global Anesthesia Dolorosa Treatment Market

- In January 2022, Medtronic reported FDA approval for an expanded indication of its spinal cord stimulation therapy for certain chronic neuropathic pain conditions, marking a continued shift toward device-based management pathways for difficult-to-treat peripheral neuropathies and reinforcing the role of SCS platforms in multidisciplinary chronic pain care

- In February 2023, a peer-reviewed case report published in Frontiers in Neurology described successful use of peripheral nerve stimulation (PNS) to relieve refractory post-traumatic trigeminal neuropathic pain, demonstrating durable pain reduction in a patient who had failed conservative treatments and highlighting PNS as a promising, less-invasive neuromodulation approach for focal facial deafferentation pain syndromes

- In January 2023, Abbott announced that the U.S. FDA approved the Proclaim™ XR spinal cord stimulation system for an expanded indication to treat painful diabetic peripheral neuropathy, providing clinicians with an additional neuromodulation option for chronic neuropathic pain and underscoring broader regulatory momentum for implantable stimulation technologies in refractory neuropathic conditions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.