Global Angiotensin Ii Receptor Blockers Arbs Market

Market Size in USD Billion

USD

9.40 Billion

USD

17.14 Billion

2024

2032

USD

9.40 Billion

USD

17.14 Billion

2024

2032

Forecast Period |

2025 - 2032 |

Market Size (Base Year) |

USD 9.40 Billion |

Market Size (Forecast Year) |

USD 17.14 Billion |

CAGR |

% |

Major Markets Players |

|

Angiotensin II Receptor Blockers (ARBs) Market Size

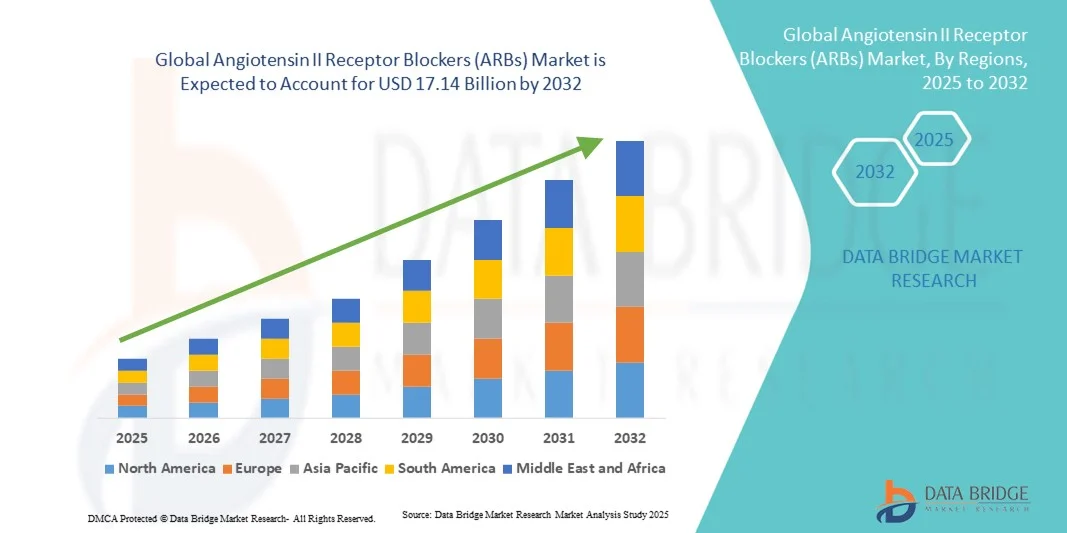

- The global angiotensin II receptor blockers (ARBs) market size was valued at USD 9.40 billion in 2024 and is expected to reach USD 17.14 billion by 2032, at a CAGR of7.80% during the forecast period

- The market growth is largely fueled by the growing prevalence of hypertension, cardiovascular diseases, and chronic kidney disorders, which has increased the adoption of Angiotensin II Receptor Blockers (ARBs) as an effective therapeutic option. Advancements in clinical research and the development of next-generation ARBs with improved safety and efficacy profiles are further supporting market expansion

- Furthermore, rising patient preference for well-tolerated, long-term treatment options and the increasing availability of generic ARBs are making these drugs more accessible and affordable across emerging as well as developed markets. These converging factors are accelerating the uptake of Angiotensin II Receptor Blockers (ARBs), thereby significantly boosting the industry’s growth

Angiotensin II Receptor Blockers (ARBs) Market Analysis

- The Angiotensin II Receptor Blockers (ARBs) market plays a crucial role in the management of hypertension, heart failure, and chronic kidney disease, driven by the increasing prevalence of cardiovascular disorders and rising adoption of evidence-based treatment protocols

- The growing demand for ARBs is primarily fueled by the rising global burden of hypertension, patient preference for drugs with fewer side effects compared to ACE inhibitors, and increased availability of generic formulations enhancing accessibility

- North America dominated the angiotensin II receptor blockers (ARBs) market with the largest revenue share of 38.6% in 2024, attributed to the high prevalence of hypertension, strong presence of pharmaceutical companies, favorable reimbursement policies, and widespread adoption of ARBs in clinical guidelines across the U.S. and Canada

- Asia-Pacific is expected to be the fastest-growing region in the angiotensin II receptor blockers (ARBs) market during the forecast period, projected to record a CAGR from 2025 to 2032, driven by a rising aging population, increasing healthcare expenditure, and rapid urbanization leading to lifestyle-related cardiovascular diseases

- The Hypertension segment dominated the angiotensin II receptor blockers (ARBs) market with the largest revenue share of 45.2% in 2024, owing to the high prevalence of hypertension globally and strong guideline-based recommendations favoring ARBs

Report Scope and Angiotensin II Receptor Blockers (ARBs) Market Segmentation

|

Attributes |

Angiotensin II Receptor Blockers (ARBs) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Angiotensin II Receptor Blockers (ARBs) Market Trends

Shift Towards Combination Therapies and Personalized Hypertension Management

- A prominent trend in the ARBs market is the rising adoption of fixed-dose combination (FDC) therapies, pairing ARBs with other antihypertensive classes such as diuretics, calcium channel blockers (CCBs), and beta-blockers. This approach enhances efficacy and improves patient adherence by reducing pill burden

- For instance, in July 2023, Daiichi Sankyo launched a new ARB/CCB fixed-dose combination in select Asia-Pacific markets to address resistant hypertension and improve treatment compliance

- Healthcare providers are increasingly following international guidelines (such as the American College of Cardiology/American Heart Association and the European Society of Cardiology), which recommend ARB-based combinations for patients with comorbid conditions like diabetes and chronic kidney disease (CKD)

- Pharmacogenomics is gradually shaping ARB therapy decisions, as genetic variations affecting drug metabolism and response are studied to deliver tailored, patient-specific regimens

- The growing preference for once-daily, extended-release formulations is also a trend, as these improve adherence and reduce missed doses

- Clinical trials are expanding the therapeutic scope of ARBs beyond hypertension, with research into heart failure with preserved ejection fraction (HFpEF), diabetic nephropathy, and even certain neurological disorders, which is expected to reshape demand over the forecast period

Angiotensin II Receptor Blockers (ARBs) Market Dynamics

Driver

Rising Global Burden of Hypertension and Cardiovascular Disorders

- The steadily increasing prevalence of hypertension, affecting over 1.2 billion people worldwide according to WHO (2023), is a critical driver for ARB market expansion. Hypertension is a major risk factor for stroke, myocardial infarction, and kidney failure, making ARBs central to long-term disease management

- For instance, in March 2022, the American Heart Association highlighted that 122 million U.S. adults were living with hypertension, underscoring the vast patient base for ARBs

- ARBs are favored by clinicians due to their superior tolerability compared to ACE inhibitors, especially for patients who develop persistent cough or angioedema from ACE therapy. This preference directly supports their widespread prescription

- The aging population worldwide, particularly in developed economies, is increasing the number of patients requiring chronic antihypertensive therapy. This demographic trend significantly expands ARB utilization

- High comorbidity rates with conditions such as type 2 diabetes, obesity, and chronic kidney disease are further driving ARB demand, since these drugs provide added renal-protective and cardioprotective benefits

- In emerging markets, rising awareness of hypertension screening and treatment, coupled with government-led initiatives to improve cardiovascular care, is fueling the penetration of ARBs

- Robust clinical evidence supporting ARBs’ efficacy and safety profile continues to solidify their role as a first-line therapy, ensuring sustained demand across both primary and specialist care settings

Restraint/Challenge

Patent Expiries, Generic Competition, and Quality Concerns

- Patent expiries of blockbuster ARBs such as valsartan (Diovan), losartan (Cozaar), and irbesartan (Avapro) have resulted in an influx of generics, exerting significant downward pressure on branded drug revenues

- For instance, after Diovan lost exclusivity, Novartis reported a sharp revenue decline, highlighting the long-term impact of generic erosion on innovator companies

- Price controls and reimbursement policies in many countries amplify pricing pressure, particularly in cost-sensitive markets where generics dominate prescribing patterns. This reduces profit margins for pharmaceutical firms and limits R&D reinvestment

- Regulatory and safety-related challenges also weigh heavily on the ARBs market. For example, the 2018–2019 global recalls of ARBs contaminated with nitrosamine impurities (NDMA, NDEA) led to shortages, heightened regulatory scrutiny, and a loss of patient trust in certain products

- While generics improve affordability and access, their uneven quality standards in some regions raise concerns about therapeutic consistency and patient outcomes, requiring stricter regulatory oversight

- The highly competitive generic environment also creates market fragmentation, making it challenging for smaller players to establish brand loyalty or differentiate their products

- In developed regions, physician hesitancy to switch stable patients from branded to generic ARBs—despite cost advantages—reflects lingering concerns over bioequivalence and patient response, which can slow adoption

- Finally, limited innovation in ARB monotherapy compared to newer classes of antihypertensives (e.g., ARNI or SGLT2 inhibitors in heart failure and diabetes care) poses a strategic challenge for companies relying heavily on ARBs

Angiotensin II Receptor Blockers (ARBs) Market Scope

The market is segmented on the basis of type, application, and end-users.

- By Type

On the basis of type, the global angiotensin II receptor blockers (ARBs) market is segmented into Azilsartan, Candesartan, Eprosartan, Irbesartan, Losartan, Olmesartan, Telmisartan, and Valsartan. The Losartan segment dominated the market with the largest revenue share of 28.5% in 2024, driven by its wide clinical adoption, well-established efficacy, and strong physician preference. Losartan’s versatility in managing hypertension and heart failure, along with its favorable safety profile, underpins its market dominance. Hospitals and specialty clinics prefer Losartan for long-term treatment, and it benefits from robust insurance coverage. The availability of generic options further enhances its accessibility, making it the most prescribed ARB globally. The segment also sees consistent growth due to ongoing clinical studies confirming its effectiveness across various patient populations, including elderly and comorbid patients. Physician trust, patient familiarity, and global supply chain stability contribute to its sustained market leadership.

The Azilsartan segment is anticipated to witness the fastest CAGR of 10.8% from 2025 to 2032, fueled by increasing clinical adoption for resistant hypertension cases. Azilsartan offers high potency and fewer adverse effects, attracting new prescriptions in hospitals and specialty clinics. Growing awareness among clinicians, coupled with favorable reimbursement policies and emerging guideline recommendations, drives market growth. Pharmaceutical companies are actively promoting Azilsartan through educational initiatives, boosting physician confidence. The introduction of fixed-dose combinations with diuretics further enhances its market potential. Expanding patient base in Asia-Pacific and Latin America supports rapid uptake. Strategic partnerships between manufacturers and hospitals for clinical programs also accelerate adoption. Rising preference for newer ARBs with improved cardiovascular outcomes continues to propel this segment.

- By Application

On the basis of application, the global angiotensin II receptor blockers (ARBs) market is segmented into Hypertension, Heart Failure, High Blood Pressure, Kidney Disease, and Others.The Hypertension segment dominated with the largest revenue share of 45.2% in 2024, owing to the high prevalence of hypertension globally and strong guideline-based recommendations favoring ARBs. Hospitals and specialty clinics extensively prescribe ARBs for primary hypertension management due to their efficacy and low risk of adverse effects. Patient adherence is enhanced by once-daily dosing and fixed-dose combinations. Ongoing clinical trials validating cardiovascular protection contribute to continued preference. Widespread physician familiarity and well-established treatment protocols reinforce market dominance. Reimbursement coverage in developed regions ensures affordability and drives higher prescription volumes. Public health initiatives emphasizing hypertension control further stimulate adoption. Urbanization and lifestyle-related risk factors support continued demand. ARBs remain first-line therapy in multiple global treatment guidelines, sustaining growth.

The Heart Failure segment is expected to witness the fastest CAGR of 9.6% from 2025 to 2032, driven by growing awareness of ARBs’ benefits in managing cardiac remodeling and reducing hospitalization rates. Rising prevalence of heart failure, especially in aging populations, fuels adoption. Increased hospital protocols for early intervention and combination therapy with ACE inhibitors or beta-blockers promote usage. Physician preference for safer alternatives to traditional medications drives segment growth. Expanding clinical evidence on ARBs’ role in improving ejection fraction and survival further encourages prescriptions. Emerging markets with improving healthcare infrastructure provide new opportunities. Innovative formulations and patient assistance programs support faster uptake.

- By End-Users

On the basis of end-users, the global angiotensin II receptor blockers (ARBs) market is segmented into Hospitals, Ambulatory Surgical Centers, Specialty Clinics, and Others.The Hospitals segment dominated with the largest revenue share of 52.1% in 2024, reflecting the primary role of hospitals in prescribing ARBs for chronic conditions such as hypertension and heart failure. Hospitals benefit from integrated pharmacy systems, patient monitoring, and bulk purchasing agreements, enhancing access and adoption. Clinical protocols and guideline adherence reinforce usage across inpatient and outpatient settings. Hospital-based awareness campaigns and physician-led initiatives increase prescription volumes. Strong collaborations with pharmaceutical companies ensure consistent supply and education. Emerging hospital networks in developing regions contribute to expanded market penetration. Hospitals’ capacity to manage complex comorbidities further solidifies dominance. Large-scale treatment programs and insurance coverage enhance affordability and access for patients.

The Specialty Clinics segment is expected to witness the fastest CAGR of 11.3% from 2025 to 2032, driven by increasing patient visits for chronic disease management and targeted therapies. Specialty clinics are adopting ARBs for hypertension, heart failure, and kidney disease management due to their effectiveness and safety profile. Improved healthcare access, patient-focused services, and physician recommendations support growth. Clinics are also leveraging patient education programs and telemedicine follow-ups to enhance adherence. Rising prevalence of lifestyle-related disorders boosts clinic visits. Collaboration with pharmaceutical companies for clinical studies and awareness campaigns drives rapid uptake. Emerging markets, expanding middle-class populations, and insurance reimbursement further accelerate adoption.

Angiotensin II Receptor Blockers (ARBs) Market Regional Analysis

- North America dominated the angiotensin II receptor blockers (ARBs) market with the largest revenue share of 38.6% in 2024, driven by the high prevalence of hypertension, strong presence of leading pharmaceutical companies, favorable reimbursement policies

- High adoption of combination therapies and advanced treatment guidelines for hypertension and cardiovascular diseases, which encourages the prescription of ARBs either alone or in combination with other antihypertensives

- Ongoing research and development activities in cardiovascular therapies, including newer ARB formulations and fixed-dose combinations, which drive market growth in North America

U.S. Angiotensin II Receptor Blockers (ARBs) Market Insight

The U.S. angiotensin II receptor blockers (ARBs) market captured the largest revenue share within North America in 2024, fueled by increasing awareness of cardiovascular disorders, early diagnosis, and the growing use of ARBs as first-line treatment options in hospitals and clinics. Advancements in patient monitoring, personalized therapy, and government initiatives promoting cardiovascular health are further contributing to market expansion.

Europe Angiotensin II Receptor Blockers (ARBs) Market Insight

The Europe angiotensin II receptor blockers (ARBs) market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing incidence of hypertension and cardiovascular diseases, favorable government policies supporting chronic disease management, and rising adoption of ARBs in clinical practice. Germany, France, and the U.K. are witnessing robust growth due to well-established healthcare infrastructure and increasing patient awareness.

U.K. Angiotensin II Receptor Blockers (ARBs) Market Insight

The U.K. angiotensin II receptor blockers (ARBs) market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by rising prevalence of hypertension, government initiatives to promote cardiovascular health, and the adoption of ARBs in both hospital and outpatient settings. Moreover, the country’s strong pharmaceutical network and increasing healthcare expenditure are fueling market growth.

Germany Angiotensin II Receptor Blockers (ARBs) Market Insight

The Germany angiotensin II receptor blockers (ARBs) market is expected to expand at a considerable CAGR during the forecast period, attributed to rising cardiovascular disease incidence, robust healthcare infrastructure, and growing emphasis on preventive care. Widespread prescription of ARBs in hospitals and clinics, coupled with ongoing research and development initiatives, is accelerating market adoption.

Asia-Pacific Angiotensin II Receptor Blockers (ARBs) Market Insight

The Asia-Pacific angiotensin II receptor blockers (ARBs) market is poised to grow at the fastest CAGR during the forecast period from 2025 to 2032, driven by a rising aging population, increasing healthcare expenditure, rapid urbanization, and a growing prevalence of lifestyle-related cardiovascular diseases in countries such as China, India, and Japan. Enhanced accessibility to ARBs, expanding hospital networks, and increased awareness among clinicians are contributing to market growth.

Japan Angiotensin II Receptor Blockers (ARBs) Market Insight

The Japan angiotensin II receptor blockers (ARBs) market is witnessing steady growth due to an aging population, high prevalence of hypertension, and increasing adoption of ARBs in clinical practice. Advanced healthcare infrastructure, government initiatives supporting chronic disease management, and growing patient awareness are further driving market expansion.

China Angiotensin II Receptor Blockers (ARBs) Market Insight

The China angiotensin II receptor blockers (ARBs) market accounted for the largest revenue share in Asia-Pacific in 2024, driven by rising cardiovascular disease prevalence, rapid urbanization, increasing healthcare expenditure, and expanding middle-class population. Strong domestic pharmaceutical companies, wider availability of ARBs, and government initiatives promoting cardiovascular health are key factors supporting market growth.

Angiotensin II Receptor Blockers (ARBs) Market Share

The Angiotensin II Receptor Blockers (ARBs) industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- AstraZeneca (U.K.)

- Sanofi S.A. (France)

- Bayer AG (Germany)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Daiichi Sankyo Company, Ltd. (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- Boehringer Ingelheim International GmbH (Germany)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Cipla Ltd. (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Torrent Pharmaceuticals Ltd. (India)

Latest Developments in Global Angiotensin II Receptor Blockers (ARBs) Market

- In February 2021, the U.S. Food and Drug Administration (FDA) announced recalls of multiple lots of valsartan, losartan, and irbesartan after detecting nitrosamine impurities above acceptable limits. The agency also published validated testing methods for manufacturers to detect nitrosamines and ensure patient safety

- In July 2022, the FDA approved the first generic versions of azilsartan medoxomil tablets (40 mg and 80 mg), broadening patient access to ARB therapy for hypertension while increasing competition in the U.S. market

- In September 2023, regulators and pharmacopeias, including the U.S. FDA and the European Medicines Agency (EMA), issued updated technical guidelines to strengthen controls for nitrosamine impurities in ARBs and other drug classes, requiring manufacturers to enhance quality assurance and supply-chain monitoring

- In April 2024, the FDA published new recommendations for assessing and preventing unacceptable nitrosamine levels in human drugs, directly impacting ARB manufacturers by requiring risk-based evaluations and robust impurity testing during production

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.