Global Angle Closure Glaucoma Market

Market Size in USD Million

USD

645.90 Million

USD

968.93 Million

2024

2032

USD

645.90 Million

USD

968.93 Million

2024

2032

| 2025 - 2032 | |

| USD 645.90 Million | |

| USD 968.93 Million | |

| % | |

|

Angle-Closure Glaucoma Market Size

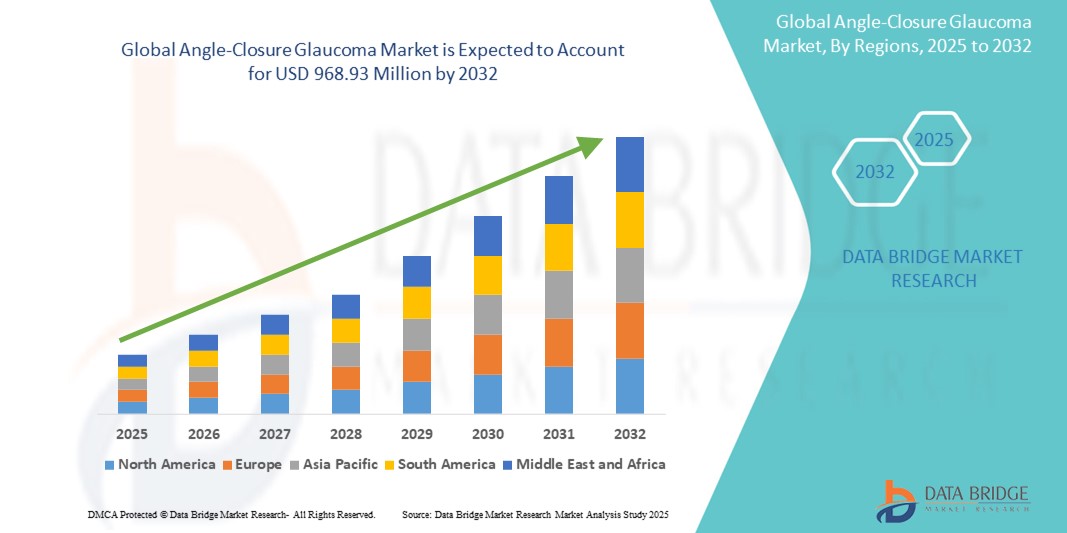

- The Global Angle-Closure Glaucoma Market size was valued at USD 645.9 Million in 2024 and is expected to reach USD 968.93 Million by 2032, at a CAGR of 5.2% during the forecast period

- The market growth is primarily driven by the increasing prevalence of glaucoma-related vision impairment, especially in aging populations across Asia-Pacific and developing regions, where angle-closure glaucoma is more common

- Moreover, growing awareness about early diagnosis and treatment, advancements in diagnostic techniques such as gonioscopy and imaging tools, and the rising availability of minimally invasive surgical options are contributing to market expansion. These factors, coupled with supportive healthcare policies and rising demand for effective intraocular pressure management, are accelerating the adoption of both surgical and pharmacological treatment solutions—significantly boosting the angle-closure glaucoma market

Angle-Closure Glaucoma Market Analysis

- Angle-closure glaucoma, a serious ophthalmic condition characterized by a sudden rise in intraocular pressure due to blocked drainage angles in the eye, remains a leading cause of irreversible blindness, particularly in aging populations and certain ethnic groups such as East Asians and Inuits. Early detection and timely treatment are critical to prevent vision loss, making diagnostic accuracy and therapeutic innovation essential in managing the disease.

- The increasing prevalence of age-related eye disorders, rising healthcare awareness, and advances in diagnostic imaging techniques such as gonioscopy, tonometry, and anterior segment optical coherence tomography (AS-OCT) are driving market growth. Additionally, growing availability of surgical and pharmacological treatments is expanding patient access to effective disease management.

- Asia-Pacific dominates the angle-closure glaucoma market, accounting for the largest revenue share of over 38.5% in 2025, owing to a higher prevalence of the disease in the region, large aging population base, and increased government initiatives to support eye health. Countries such as China and India are witnessing significant improvements in screening infrastructure and awareness campaigns.

- North America is anticipated to show steady growth during the forecast period due to favorable reimbursement frameworks, high adoption of advanced ophthalmic technologies, and ongoing clinical research on novel therapies and combination treatments.

- The surgery segment is expected to lead the treatment category with a projected market share of 47.6% in 2025, driven by the increasing preference for laser peripheral iridotomy (LPI), trabeculectomy, and minimally invasive glaucoma surgery (MIGS) to reduce intraocular pressure in high-risk patients.

Report Scope and Angle-Closure Glaucoma Market Segmentation

|

Attributes |

Angle-Closure Glaucoma Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Angle-Closure Glaucoma Market Trends

“Technological Advancements in Early Diagnosis and Personalized Treatment”

- A key and accelerating trend in the global angle-closure glaucoma market is the integration of advanced diagnostic tools such as anterior segment optical coherence tomography (AS-OCT), ultrasound biomicroscopy (UBM), and AI-powered image analysis to improve early detection, staging, and monitoring of angle-closure glaucoma. These innovations are driving a shift toward personalized treatment approaches and more targeted clinical interventions.

- For instance, AS-OCT and automated gonioscopy systems enable precise visualization of the iridocorneal angle, facilitating accurate classification and progression monitoring of angle-closure glaucoma subtypes. AI-based diagnostic tools are increasingly being employed to analyze large volumes of ocular imaging data, allowing for earlier detection and risk stratification.

- Companies such as Topcon Corporation and Carl Zeiss Meditec AG are introducing integrated imaging platforms that support real-time decision-making and treatment planning. These platforms are helping clinicians tailor treatment regimens, such as selecting between laser iridotomy or lens extraction based on individual anatomical parameters.

- Additionally, personalized medicine is gaining momentum, particularly in pharmacological therapies where genetic markers and patient profiles are being considered to optimize drug selection and minimize adverse effects.

- This trend toward intelligent, data-driven glaucoma management is transforming clinical practices, improving patient outcomes, and fostering increased collaboration between ophthalmologists and diagnostic device manufacturers. As access to precision diagnostics improves in both developed and emerging markets, this trend is poised to reshape treatment paradigms in angle-closure glaucoma care

Angle-Closure Glaucoma Market Dynamics

Driver

“Rising Prevalence and Increasing Awareness of Early Ophthalmic Intervention”

- The rising global prevalence of primary angle-closure glaucoma (PACG), particularly in aging populations across Asia-Pacific and African regions, is a major driver fueling the demand for early diagnosis and treatment. PACG is more likely to cause bilateral blindness than other forms of glaucoma, which heightens the urgency for proactive screening and intervention.

- For instance, public health campaigns by organizations such as the World Glaucoma Association (WGA) and Asia-Pacific Glaucoma Society (APGS) are expanding awareness and promoting regular eye screenings, especially among high-risk demographics such as individuals over 50, females, and those with a family history of glaucoma.

- The increased adoption of laser peripheral iridotomy (LPI), phacoemulsification with IOL, and minimally invasive glaucoma surgeries (MIGS) as frontline interventions is also accelerating market growth. These procedures offer effective intraocular pressure reduction with improved safety and recovery profiles.

- Simultaneously, advances in pharmacological therapy, including fixed-dose combinations and sustained-release drug implants, are improving patient adherence and treatment outcomes. The emergence of AI-assisted tele-ophthalmology platforms is further broadening access to diagnostics and specialist consultations, especially in underserved regions.

Restraint/Challenge

“Limited Access to Diagnostic Infrastructure and Post-Surgical Care in Developing Regions”

- One of the critical challenges restraining the growth of the angle-closure glaucoma market is the limited availability of specialized ophthalmic diagnostic equipment and trained eye care professionals in low- and middle-income countries (LMICs). Despite the high disease burden, many rural and underserved regions lack access to gonioscopy, AS-OCT, or laser therapy facilities, leading to delayed diagnosis and higher rates of blindness

- For instance, large parts of Sub-Saharan Africa and South Asia still depend on basic visual acuity tests, which are insufficient for detecting angle closure in early stages. This lack of infrastructure limits the effectiveness of nationwide screening and early intervention programs

- Moreover, even where surgical interventions such as laser iridotomy are available, post-operative care and follow-up adherence remain inadequate due to systemic healthcare limitations and socioeconomic barriers. This results in suboptimal outcomes and persistent disease progression in many patients

- Another restraint is the lack of disease-specific therapies for certain PACG subtypes, where traditional open-angle glaucoma medications may not offer the same efficacy. In some cases, patients may experience poor response or side effects, highlighting the need for more targeted and PACG-specific drug development

- Overcoming these challenges will require greater investment in healthcare infrastructure, capacity-building for ophthalmologists, and affordable access to diagnostic tools and therapeutics tailored for high-prevalence regions

Angle-Closure Glaucoma Market Scope

The market is segmented on the basis of diagnosis, treatment, route of administration, end-users, and distribution channel.

• By Diagnosis

On the basis of diagnosis, the angle-closure glaucoma market is segmented into gonioscopy, tonometry, ophthalmoscopy, and others. The gonioscopy segment accounted for the largest market revenue share of 41.2% in 2025, owing to its status as the gold standard for diagnosing angle-closure glaucoma. Gonioscopy allows direct visualization of the anterior chamber angle and is essential for classifying the severity and type of angle closure, thereby enabling timely treatment decisions. Increasing training programs for ophthalmologists and widespread clinical use across hospitals and specialty clinics are contributing to its dominance.

The "others" segment, which includes anterior segment imaging tools such as anterior segment OCT and ultrasound biomicroscopy, is expected to witness the fastest CAGR of 11.7% from 2025 to 2032. These technologies offer non-contact, high-resolution images that enhance diagnostic accuracy and are increasingly favored in both preoperative assessments and routine screenings. Their growing adoption, particularly in technologically advanced and urban healthcare centers, is driving this segment’s rapid expansion.

• By Treatment

On the basis of treatment, the angle-closure glaucoma market is segmented into surgery, medication, and others. The surgery segment held the largest market revenue share in 2025, primarily due to the widespread adoption of laser peripheral iridotomy (LPI) and lens extraction surgery for patients with primary angle closure and PACG. Surgical options offer long-term intraocular pressure (IOP) control and are often the preferred treatment in moderate to severe cases or in patients unresponsive to medication.

The medication segment is projected to grow at the fastest CAGR from 2025 to 2032. With increasing development of fixed-dose combination drugs and sustained-release therapies, pharmacological treatment is gaining traction, especially for early-stage or medically manageable cases. New drug formulations aimed at enhancing compliance and minimizing side effects are fueling this segment's growth.

• By Route of Administration

Based on route of administration, the market is segmented into oral, parenteral, ocular, and others. The ocular segment dominated the market in 2025, as topical eye drops remain the most common first-line therapy for lowering intraocular pressure in angle-closure glaucoma patients. These include beta-blockers, alpha agonists, prostaglandin analogs, and carbonic anhydrase inhibitors. Their ease of administration and effectiveness in IOP management drive this segment’s leadership.

The parenteral segment is anticipated to grow at the fastest CAGR through 2032. Injectable agents, including those used perioperatively or in sustained-release formats, are being explored for long-term IOP control, particularly in severe or refractory cases. The introduction of injectable sustained-release implants for glaucoma management is a key contributor to this segment’s growth.

• By End-Users

On the basis of end-users, the angle-closure glaucoma market is segmented into hospitals, specialty clinics, and others. The hospitals segment captured the highest market revenue share in 2025, driven by access to advanced diagnostic and surgical infrastructure, availability of glaucoma specialists, and increasing hospital-based glaucoma screening programs. Hospitals also act as referral centers for severe and complex glaucoma cases requiring surgical intervention.

The specialty clinics segment is expected to register the fastest growth during the forecast period. With growing preference for outpatient care, rising number of standalone eye care centers, and cost-effective glaucoma management models, specialty clinics are gaining prominence, especially in urban and semi-urban regions.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and others. Hospital pharmacies held the largest market share in 2025 due to the high volume of prescriptions generated through in-house ophthalmologists and immediate post-surgical drug requirements. Hospital-linked distribution ensures availability of both generic and branded therapies, especially in Tier 1 healthcare facilities.

The retail pharmacies segment is projected to witness the highest CAGR from 2025 to 2032, driven by the increasing availability of prescription glaucoma medications across community-based pharmacies, growing home-based treatment preferences, and improved patient access through pharmacy chains in developing economies.

Angle-Closure Glaucoma Market Regional Analysis

- Asia-Pacific dominates the angle-closure glaucoma market with the largest revenue share of 38.5% in 2025, driven by the high prevalence of primary angle-closure glaucoma (PACG), particularly in countries like China, India, and Japan, where aging populations are more susceptible to the disease.

- The region’s dominance is supported by increasing government-led eye health initiatives, expanding healthcare infrastructure, and a growing emphasis on early detection through nationwide screening programs.

- Rising awareness of glaucoma-related blindness, improving access to ophthalmologists, and the increasing availability of diagnostic tools such as gonioscopy and anterior segment OCT are accelerating the adoption of early intervention therapies in the region.

- Furthermore, advancements in minimally invasive surgical techniques and the availability of affordable generic medications are contributing to the widespread management of angle-closure glaucoma. These factors, along with the rising burden of age-related eye conditions, are positioning Asia-Pacific as the key growth engine of the global market.

U.S. Angle-Closure Glaucoma Market Insight

The U.S. angle-closure glaucoma market captured the largest revenue share of 79% within North America in 2025, driven by increasing awareness of glaucoma-related vision loss and the availability of advanced diagnostic and surgical technologies. The widespread adoption of laser peripheral iridotomy (LPI) and minimally invasive glaucoma surgeries (MIGS), coupled with a strong presence of leading ophthalmic device manufacturers, supports continued market growth. Furthermore, a high level of ophthalmologist access, favorable reimbursement policies, and the integration of AI in ocular imaging solutions are propelling the U.S. market forward, particularly in both hospital and specialty clinic settings.

Europe Angle-Closure Glaucoma Market Insight

The European angle-closure glaucoma market is projected to grow at a steady CAGR throughout the forecast period, fueled by an aging population and government-backed screening programs aimed at preventing vision impairment. Increasing investment in public eye health campaigns and widespread use of gonioscopy and anterior segment OCT for early detection support market expansion. The market is also benefitting from the adoption of digital ophthalmic diagnostics and cross-border collaboration on glaucoma awareness initiatives. Both Western and Eastern European countries are witnessing growth across public and private healthcare settings, with emphasis on early intervention and personalized treatment.

U.K. Angle-Closure Glaucoma Market Insight

The U.K. angle-closure glaucoma market is anticipated to expand at a noteworthy CAGR during the forecast period, owing to heightened awareness of glaucoma risk among the elderly population and a strong push toward early detection and preventive care. The National Health Service (NHS) continues to play a pivotal role by facilitating access to diagnostic tools such as tonometry and imaging-based screening for at-risk groups. Additionally, robust academic research and integration of tele-ophthalmology solutions are improving accessibility and diagnosis rates, thereby supporting market growth.

Germany Angle-Closure Glaucoma Market Insight

The German angle-closure glaucoma market is expected to show strong growth due to its technologically advanced healthcare infrastructure and proactive screening initiatives. Germany’s focus on precision diagnostics and early intervention is evident in its use of cutting-edge tools like ultrasound biomicroscopy (UBM) and anterior segment OCT in ophthalmology clinics. Additionally, partnerships between hospitals and research institutions to explore AI-assisted glaucoma diagnostics are likely to fuel adoption. A growing geriatric population and a high prevalence of glaucoma-related visual impairment continue to drive the need for timely and effective treatments.

Asia-Pacific Angle-Closure Glaucoma Market Insight

The Asia-Pacific angle-closure glaucoma market is poised to grow at the fastest CAGR of over 10.5% in 2025, driven by a high disease burden in countries like China, India, and Southeast Asia, where primary angle-closure glaucoma (PACG) is more prevalent than in other global regions. Rising public health awareness, increasing access to ophthalmic care, and the proliferation of affordable diagnostic equipment are accelerating early detection. Government-led blindness prevention programs and public-private partnerships are expanding reach in rural and urban areas alike, positioning Asia-Pacific as a central driver of global market expansion.

Japan Angle-Closure Glaucoma Market Insight

The Japan angle-closure glaucoma market is advancing rapidly due to the country’s aging demographic and a well-established eye care infrastructure. Japan’s healthcare system emphasizes preventive care and technology adoption, making it a fertile ground for the integration of advanced glaucoma diagnostics and laser-based therapies. The rise in routine eye screenings for older adults and the availability of sophisticated diagnostic devices like AS-OCT are fostering early identification and management of PACG. Additionally, collaborative efforts between academic institutions and medical device companies are boosting innovation and treatment accessibility.

China Angle-Closure Glaucoma Market Insight

The China angle-closure glaucoma market accounted for the largest market revenue share within Asia-Pacific in 2025, driven by a combination of rapid urbanization, a large aging population, and government-supported eye health programs. The rollout of nationwide glaucoma awareness initiatives and improved access to advanced diagnostics in both public and private hospitals have led to a surge in early-stage diagnosis. Domestic medical device manufacturers are increasingly offering cost-effective diagnostic and surgical solutions, making treatments more accessible across Tier 2 and Tier 3 cities. China's efforts toward building a digitally enabled healthcare system are further enhancing the management of glaucoma.

Angle-Closure Glaucoma Market Share

The Angle-Closure Glaucoma industry is primarily led by well-established companies, including:

- Taro Pharmaceutical Industries Ltd. (Israel)

- Novartis AG (Switzerland)

- ALLERGAN (U.S.)

- Akorn Pharmaceuticals (U.S.)

- Bausch & Lomb Incorporated (Canada)

- Aerie Pharmaceuticals (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Alcon Inc. (Switzerland)

- Pfizer Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- AbbVie Inc. (U.S.)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Bayer AG (Germany)

- Aurobindo Pharma Ltd. (India)

- Meda Pharmaceuticals Inc. (U.S.)

- Nicox S.A. (France)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.