Global Anomamaly Detection Market

Market Size in USD Billion

USD

7.00 Billion

USD

23.51 Billion

2025

2033

USD

7.00 Billion

USD

23.51 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 7.00 Billion |

Market Size (Forecast Year) |

USD 23.51 Billion |

CAGR |

% |

Major Markets Players |

|

Anomamaly Detection Market Size

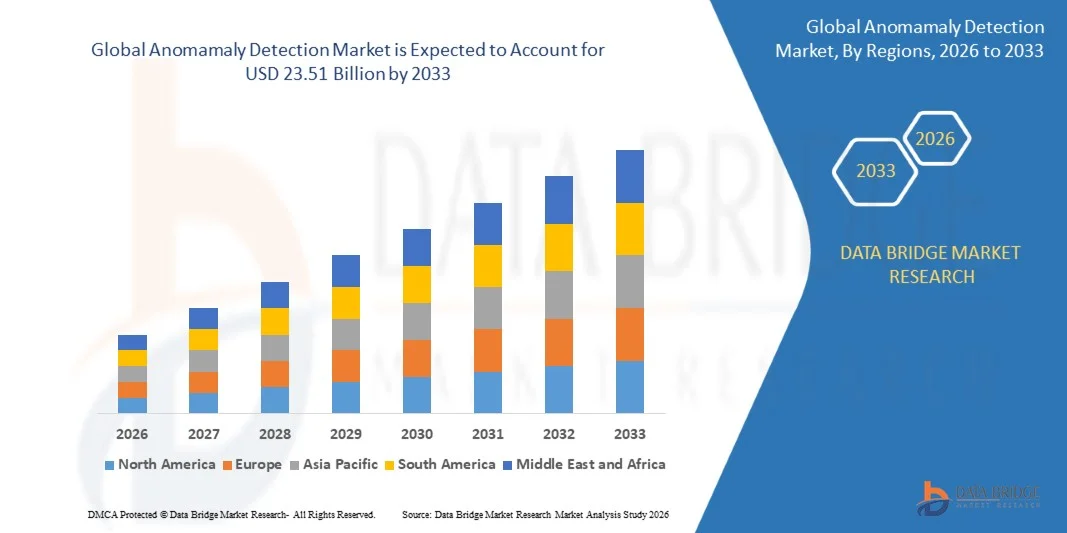

- The global anomamaly detection market size was valued at USD 7.00 billion in 2025 and is expected to reach USD 23.51 billion by 2033, at a CAGR of 16.35% during the forecast period

- The market growth is largely fuelled by the rapid increase in cyber threats and the rising need for real-time security monitoring across enterprises

- Expanding adoption of AI and machine learning–based analytics in financial services, healthcare, and IT is further accelerating demand

Anomamaly Detection Market Analysis

- The market is witnessing strong traction due to the growing emphasis on predictive analytics and automated threat intelligence across industries

- The increasing integration of advanced algorithms, behavioural analytics, and data-driven security frameworks is reshaping enterprise risk management and enhancing overall threat detection accuracy

- North America dominated the global anomaly detection market with the largest revenue share of 38.5% in 2025, driven by the growing need for advanced cybersecurity solutions, fraud detection, and operational risk management across industries

- Asia-Pacific region is expected to witness the highest growth rate in the global anomamaly detection market, driven by rapid digitalization, rising cyber threats, increasing cloud adoption, and government initiatives supporting smart cities and digital infrastructure

- The solution segment held the largest market revenue share in 2025, driven by the increasing need for robust real-time monitoring and threat identification tools. Solutions provide end-to-end capabilities, including anomaly detection engines, dashboards, and analytics, enabling enterprises to proactively mitigate risks

Report Scope and Anomamaly Detection Market Segmentation

|

Attributes |

Anomamaly Detection Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Anomamaly Detection Market Trends

“Rise of AI-Driven Real-Time Threat Identification”

• The rapid shift toward AI-powered and machine learning–based anomaly detection solutions is transforming threat monitoring by enabling immediate identification of unusual patterns across networks, devices, and applications. These intelligent systems support faster decision-making and reduce the time required to detect zero-day attacks and insider threats, resulting in enhanced overall security posture. The increased accuracy and automation offered by these systems are helping organizations streamline their detection workflows and reduce manual intervention

• The growing reliance on automated analytics in high-risk and data-intensive environments such as BFSI, healthcare, and government is accelerating the adoption of real-time anomaly detection platforms. These tools are particularly valuable in environments lacking dedicated cybersecurity teams, helping organizations respond to threats without delay. The capability to analyze large volumes of data at scale further strengthens proactive threat mitigation across critical infrastructure

• The increasing affordability and scalability of modern AI detection platforms are making them suitable for both large enterprises and SMEs, improving continuous monitoring capabilities. Businesses benefit from reduced manual oversight, fewer false positives, and more accurate risk detection across digital ecosystems. This accessibility is enabling even resource-constrained organizations to enhance their cybersecurity resilience through intelligent automation

• For instance, in 2024, several global financial institutions reported a significant decline in fraud-related losses after integrating advanced anomaly detection engines that monitored transaction behavior in real time, enabling early intervention and improved risk controls. These systems helped institutions identify irregular spending patterns, unauthorized access attempts, and unusual customer interactions. The resulting improvements in security efficiency also contributed to strengthened regulatory compliance

• While AI-driven detections are improving threat visibility, ongoing algorithm refinement, data quality enhancement, and user training are essential to maximize performance and reduce detection blind spots across complex network environments. Organizations must also prioritize integrating these tools with existing security ecosystems to ensure seamless data flow and timely response. Continued innovation in behavioral analytics will further elevate the precision and adaptability of anomaly detection technologies

Anomamaly Detection Market Dynamics

Driver

“Rising Cybersecurity Threats and Growing Adoption of Advanced Analytics”

• The surge in sophisticated cyberattacks is compelling organizations to adopt anomaly detection tools as a core defense mechanism. Threats such as ransomware, phishing, insider misuse, and identity fraud are becoming more frequent and complex, prompting heightened investment in real-time monitoring and predictive security analytics. This rising threat landscape is pushing enterprises to shift from reactive to proactive security approaches

• Businesses are increasingly aware of the financial, operational, and reputational risks associated with undetected anomalies, including prolonged downtime, data breaches, and compliance penalties. This awareness is driving widespread implementation of automated threat detection across various industries. Companies are leveraging these tools to strengthen their resilience, ensure continuity, and maintain customer trust

• Government regulations and global cybersecurity frameworks are further accelerating the deployment of anomaly detection technologies. Mandatory reporting standards, data protection laws, and sector-specific security requirements are pushing organizations to adopt continuous monitoring solutions. This regulatory pressure is contributing to a steady rise in adoption across both developed and emerging economies

• For instance, in 2023, regulatory bodies across the U.S. and Europe reinforced cybersecurity compliance mandates for enterprises, resulting in a substantial rise in the adoption of behavioral analytics and AI-driven security solutions. These mandates encouraged organizations to enhance logging capabilities, monitor user activity more closely, and strengthen access controls. As a result, anomaly detection tools became essential for meeting evolving compliance standards

• While regulatory and industry-driven adoption is rising, continued investments in advanced analytics, integration capabilities, and workforce upskilling are crucial to ensure long-term efficiency and resilience in anomaly detection deployments. Building internal expertise and improving security automation remain key priorities for enterprises. Strengthening collaboration between IT and security teams will further enhance overall detection accuracy and response agility

Restraint/Challenge

“High Implementation Costs and Complexity of Integration”

• The high initial investment required for deploying advanced anomaly detection systems—including AI engines, behavioral analytics platforms, and large-scale data processing tools—remains a major barrier for SMEs. These systems often require dedicated infrastructure and ongoing operational expenses, making widespread adoption challenging. Budget limitations and competing IT priorities further slow adoption across smaller enterprises

• Many organizations face difficulties integrating anomaly detection tools with their existing security frameworks due to complex architectures and limited internal expertise. The lack of skilled cybersecurity professionals further complicates implementation and day-to-day management. Integration challenges often lead to performance gaps, delayed threat detection, and increased workload for existing IT teams

• Adoption is also hindered by data quality issues and fragmented IT environments, where inconsistent or incomplete datasets reduce algorithm accuracy and increase false alerts. This results in operational inefficiencies and slower incident response. Organizations must invest in data governance and system modernization to fully leverage the capabilities of anomaly detection tools

• For instance, in 2024, several mid-sized enterprises across Asia-Pacific reported significant integration delays due to incompatible legacy systems and inconsistent data pipeline structures. These issues led to prolonged deployment timelines, increased costs, and reduced early-stage operational effectiveness. Addressing such technical bottlenecks remains essential for improving overall adoption rates

• While technological advancements continue to improve system capabilities, addressing integration complexity, enhancing data readiness, and reducing deployment costs remain essential to unlocking broader adoption and ensuring sustained market growth. Streamlined deployment frameworks and cloud-supportive architectures will further ease implementation burdens. Partnerships with managed security service providers can also help organizations overcome skill and infrastructure limitations

Anomamaly Detection Market Scope

The anomaly detection market is segmented on the basis of component, technology, deployment mode, and end user

• By Component

On the basis of component, the market is segmented into solution and services. The solution segment held the largest market revenue share in 2025, driven by the increasing need for robust real-time monitoring and threat identification tools. Solutions provide end-to-end capabilities, including anomaly detection engines, dashboards, and analytics, enabling enterprises to proactively mitigate risks.

The services segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for managed detection, consulting, and support services that help organizations optimize deployment and operational efficiency

• By Technology

On the basis of technology, the market is segmented into big data analytics, data mining and business intelligence, and machine learning and artificial intelligence. The machine learning and AI segment held the largest market revenue share in 2025, driven by its ability to detect complex patterns, reduce false positives, and automate threat detection across large-scale IT environments.

The big data analytics segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the need to process massive volumes of structured and unstructured data for accurate anomaly identification in real time

• By Deployment Mode

On the basis of deployment mode, the market is segmented into hybrid, on-premises, and cloud. The cloud segment held the largest market revenue share in 2025, driven by its scalability, cost efficiency, and ease of integration with existing IT infrastructure.

The hybrid deployment mode is expected to witness the fastest growth rate from 2026 to 2033, fueled by enterprises seeking a balance between on-premises control and cloud flexibility for enhanced data security and performance

• By End User

On the basis of end user, the market is segmented into banking, financial services, and insurance (BFSI), retail, manufacturing, IT and telecom, defense and government, healthcare, and others. The BFSI segment held the largest market revenue share in 2025, driven by the critical need to secure financial transactions and prevent fraud.

The healthcare segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing digitization, regulatory compliance requirements, and the need to protect sensitive patient data across hospitals and clinics.

Anomamaly Detection Market Regional Analysis

• North America dominated the global anomaly detection market with the largest revenue share of 38.5% in 2025, driven by the growing need for advanced cybersecurity solutions, fraud detection, and operational risk management across industries

• Organizations in the region increasingly adopt anomaly detection solutions to identify irregular patterns in real time, minimize financial losses, and enhance regulatory compliance

• This widespread adoption is further supported by the presence of major technology providers, high IT infrastructure investments, and a digitally mature corporate environment, establishing anomaly detection as a critical tool for enterprises in banking, retail, and IT sectors

U.S. Anomaly Detection Market Insight

The U.S. anomaly detection market captured the largest revenue share in 2025 within North America, fueled by the rapid adoption of big data analytics, AI-driven solutions, and cloud-based deployment models. Enterprises are prioritizing the identification of fraudulent transactions, network intrusions, and operational inefficiencies through automated systems. The growing reliance on AI and machine learning for predictive analytics, coupled with stringent regulatory requirements in banking and healthcare, is further propelling the market. Moreover, integration with existing enterprise security platforms enhances the efficiency and accuracy of anomaly detection, contributing to market growth.

Europe Anomaly Detection Market Insight

The Europe anomaly detection market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing cyber threats, regulatory compliance mandates, and digital transformation initiatives across sectors. The adoption of AI- and machine learning-based detection solutions is rising in banking, manufacturing, and IT industries. European organizations are also focusing on reducing operational risks and improving decision-making through real-time anomaly monitoring. The market growth is further supported by investments in smart infrastructure, connected devices, and analytics-driven business intelligence systems.

U.K. Anomaly Detection Market Insight

The U.K. anomaly detection market is expected to witness significant growth from 2026 to 2033, driven by the increasing adoption of AI-based fraud detection and cybersecurity solutions. Heightened concerns regarding financial fraud, data breaches, and operational risks are encouraging enterprises to implement real-time anomaly detection systems. In addition, the U.K.’s strong IT ecosystem, adoption of cloud computing, and government initiatives to secure digital infrastructure are expected to continue stimulating market growth.

Germany Anomaly Detection Market Insight

The Germany anomaly detection market is expected to witness rapid growth from 2026 to 2033, fueled by increasing awareness of cybersecurity, regulatory compliance, and operational efficiency. Germany’s well-developed industrial and IT sectors, combined with strong investments in AI and machine learning, promote the deployment of anomaly detection solutions in manufacturing, banking, and defense. Integration with advanced analytics platforms and cloud-based solutions is also enhancing the effectiveness of anomaly detection, aligning with local industry requirements.

Asia-Pacific Anomaly Detection Market Insight

The Asia-Pacific anomaly detection market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid digitalization, increasing cybercrime incidents, and growing adoption of AI- and ML-based technologies in countries such as China, Japan, and India. Rising investments in IT infrastructure and the growing emphasis on operational risk management across industries are fueling market adoption. In addition, government initiatives supporting smart city projects and cybersecurity frameworks are further propelling the use of anomaly detection solutions.

Japan Anomaly Detection Market Insight

The Japan anomaly detection market is expected to witness strong growth from 2026 to 2033 due to the country’s advanced technological infrastructure, high digital adoption, and increasing reliance on predictive analytics. Enterprises are deploying anomaly detection solutions to enhance cybersecurity, monitor industrial operations, and prevent financial fraud. Integration with IoT devices, smart manufacturing systems, and cloud platforms is further driving market expansion.

China Anomaly Detection Market Insight

The China anomaly detection market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s expanding enterprise sector, rapid digital transformation, and strong adoption of AI- and big data-driven solutions. China is increasingly deploying anomaly detection across banking, manufacturing, and IT industries to improve security, operational efficiency, and risk management. The government’s focus on smart cities and digital infrastructure, combined with the availability of domestic technology providers, is a key factor propelling market growth.

Anomamaly Detection Market Share

The Anomamaly Detection industry is primarily led by well-established companies, including:

- Cisco Systems, Inc. (U.S.)

- Dell Technologies, Inc. (U.S.)

- Hewlett Packard Enterprise Company (U.S.)

- Anodot, Ltd. (Israel / U.S.)

- Happiest Minds Technologies Limited (India)

- GURUCUL (U.S.)

- Trend Micro Incorporated (U.S.)

- Flowmon Networks a.s. (Czech Republic)

- Wipro Limited (India)

- IBM (U.S.)

- Trustwave Holdings, Inc. (U.S.)

- LogRhythm, Inc. (U.S.)

- Splunk, Inc. (U.S.)

- GREYCORTEX s.r.o. (Czech Republic)

- Securonix, Inc. (U.S.)

- Infosys Limited (India)

- SAS Institute, Inc. (U.S.)

- Broadcom Inc. (U.S.)

- Tracxn Technologies (India)

- PATTERNEX, Inc. (U.S.)

Latest Developments in Global Anomamaly Detection Market

- In June 2023, Wipro launched a new suite of banking and financial services solutions built on Microsoft Cloud. This development combines Microsoft Cloud capabilities with Wipro FullStride Cloud, leveraging Wipro’s and Capco’s deep domain expertise in financial services. The initiative aims to develop innovative solutions that help financial services clients accelerate growth, enhance customer engagement, and strengthen client relationships, thereby reinforcing Wipro’s position in the BFSI technology market

- In June 2023, Cisco announced the rollout of its AI-driven Cisco Security Cloud, a cybersecurity innovation designed to simplify security operations. By integrating advanced artificial intelligence and machine learning capabilities, the solution empowers security teams to operate more efficiently, respond to threats faster, and maintain secure remote work environments. This development is expected to strengthen Cisco’s leadership in the cybersecurity market and drive adoption of AI-enabled security solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.