Global Anti Arrhythmic Drugs Market

Market Size in USD Billion

USD

1.28 Billion

USD

1.96 Billion

2025

2033

USD

1.28 Billion

USD

1.96 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.28 Billion | |

| USD 1.96 Billion | |

| % | |

|

Anti Arrhythmic Drugs Market Size

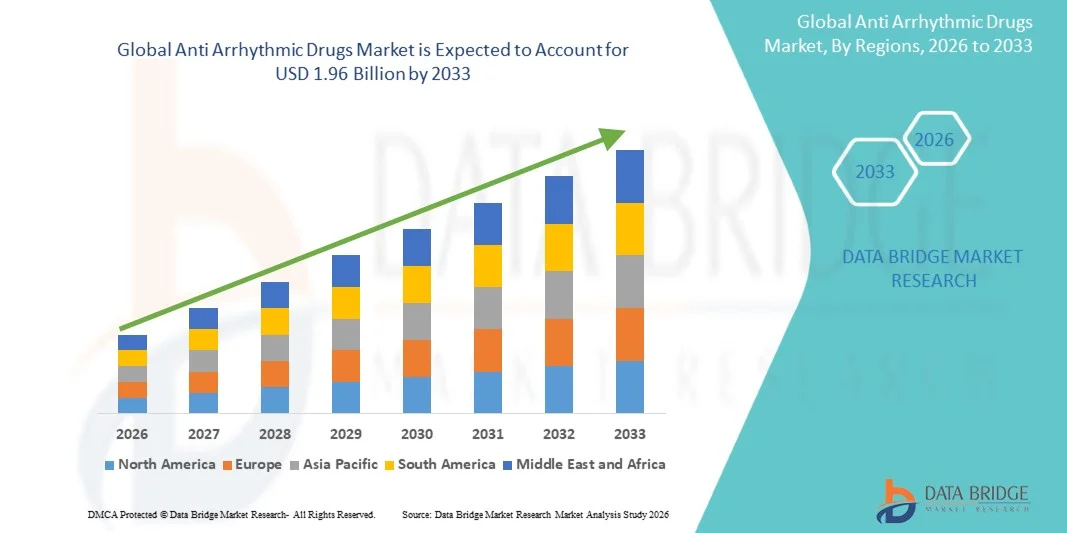

- The global anti arrhythmic drugs market size was valued at USD 1.28 billion in 2025 and is expected to reach USD 1.96 billion by 2033, at a CAGR of 5.50% during the forecast period

- The market growth is primarily driven by the rising prevalence of cardiac arrhythmias, including atrial fibrillation and ventricular arrhythmias, alongside an increasing global burden of cardiovascular diseases and an aging population more susceptible to heart rhythm disorders

- Furthermore, advancements in drug development, improved diagnostic capabilities, and growing awareness regarding early detection and management of arrhythmias are supporting wider adoption of pharmacological therapies. In addition, increasing access to healthcare services and the availability of both branded and generic anti-arrhythmic drugs are contributing to sustained market expansion, thereby strengthening the overall growth trajectory of the industry

Anti Arrhythmic Drugs Market Analysis

- Anti-arrhythmic drugs, used to manage and restore normal heart rhythm in conditions such as atrial fibrillation, atrial flutter, and ventricular arrhythmias, are increasingly essential components of cardiovascular treatment protocols in both hospital and outpatient settings due to their role in reducing morbidity, preventing complications, and improving patient outcomes

- The escalating demand for anti-arrhythmic drugs is primarily fueled by the rising global prevalence of cardiovascular diseases, increasing incidence of arrhythmias among the aging population, and growing awareness regarding early diagnosis and long-term management of heart rhythm disorders

- North America dominated the anti-arrhythmic drugs market with the largest revenue share of 38.5% in 2025, attributed to advanced healthcare infrastructure, high adoption of innovative therapies, strong presence of key pharmaceutical players, and widespread screening and diagnosis of cardiac conditions, particularly in the United States where treatment rates and access to specialized care remain high

- Asia-Pacific is expected to be the fastest growing region in the anti-arrhythmic drugs market during the forecast period due to a rapidly aging population, increasing healthcare expenditure, improving access to cardiac care, and a rising burden of lifestyle-related cardiovascular diseases across emerging economies

- Beta-blockers segment dominated the anti-arrhythmic drugs market with a market share of 42.7% in 2025, driven by their widespread clinical use as first-line therapy for rate control in arrhythmias, proven efficacy, favorable safety profile, and broad availability in both branded and generic formulations

Report Scope and Anti Arrhythmic Drugs Market Segmentation

|

Attributes |

Anti Arrhythmic Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Anti Arrhythmic Drugs Market Trends

“Shift Toward Personalized and Precision-Based Cardiac Therapy”

- A significant and accelerating trend in the global anti-arrhythmic drugs market is the growing adoption of personalized and precision-based treatment approaches guided by genetic profiling, electrophysiological mapping, and advanced diagnostic tools, improving therapeutic outcomes and patient-specific drug selection

- For instance, the use of drugs such as flecainide and amiodarone is increasingly being optimized based on individual patient risk profiles and comorbidities, while clinical decision support systems help physicians tailor dosing and drug combinations more effectively

- Advances in pharmacogenomics are enabling better prediction of patient response and adverse reactions to anti-arrhythmic medications, helping reduce trial-and-error prescribing and minimizing the risk of pro-arrhythmic side effects. Furthermore, integration of digital health tools and remote monitoring devices allows continuous tracking of heart rhythm, enabling timely therapy adjustments and improved adherence

- The integration of wearable cardiac monitors and AI-driven diagnostic platforms with drug therapy is facilitating real-time monitoring of arrhythmias, supporting early intervention and more effective disease management through data-driven insights

- This trend toward more individualized, data-informed, and technology-supported treatment strategies is reshaping clinical expectations in cardiac care. Consequently, pharmaceutical companies and healthcare providers are increasingly focusing on combination approaches that align drug therapy with advanced diagnostics and patient-specific risk assessment

- The demand for precision-guided anti-arrhythmic therapies is growing rapidly across both developed and emerging markets, as clinicians and patients prioritize improved efficacy, safety, and long-term management of complex arrhythmia conditions

- Growing adoption of combination therapies involving anti-arrhythmic drugs with anticoagulants and rate-control agents is enhancing overall treatment effectiveness and reducing the risk of complications such as stroke in atrial fibrillation patients

Anti Arrhythmic Drugs Market Dynamics

Driver

“Rising Prevalence of Cardiovascular Diseases and Expanding Patient Pool”

- The increasing prevalence of cardiovascular diseases, coupled with a growing global burden of arrhythmias among aging populations, is a significant driver for the heightened demand for anti-arrhythmic drugs

- For instance, in May 2025, major cardiology associations reported a continued rise in atrial fibrillation cases globally, prompting healthcare systems to expand screening programs and treatment protocols for early detection and management of rhythm disorders

- As awareness of arrhythmia-related complications such as stroke, heart failure, and sudden cardiac death increases, healthcare providers are emphasizing early pharmacological intervention, boosting the adoption of anti-arrhythmic medications as a primary treatment option

- Furthermore, improvements in diagnostic technologies such as ECG monitoring, Holter devices, and implantable cardiac monitors are enabling earlier and more accurate detection of arrhythmias, contributing to a larger diagnosed patient pool requiring long-term drug therapy

- The availability of both branded and generic anti-arrhythmic drugs, combined with expanding healthcare access in emerging economies and increasing healthcare expenditure, is further accelerating market growth across residential and hospital care settings

- Rising investments in cardiovascular research and clinical trials are accelerating the development of advanced anti-arrhythmic therapies, improving treatment options and expanding the overall patient base eligible for pharmacological management

- Increasing hospitalization rates associated with cardiac arrhythmias are also driving higher prescription volumes of anti-arrhythmic drugs in acute care and emergency settings

Restraint/Challenge

“Safety Concerns and Adverse Effects Associated with Anti-Arrhythmic Therapies”

- Concerns regarding the safety profile and potential adverse effects of anti-arrhythmic drugs, including pro-arrhythmic risks and organ toxicity, pose a significant challenge to broader market adoption

- For instance, certain class I and class III anti-arrhythmic drugs have been associated with risks such as QT prolongation and ventricular arrhythmias, which require careful patient monitoring and limit their use in specific populations

- The narrow therapeutic index of several anti-arrhythmic agents necessitates close clinical supervision, regular dose adjustments, and frequent monitoring, which can increase treatment complexity and limit accessibility in resource-constrained settings

- In addition, long-term use of some drugs such as amiodarone has been linked to thyroid, pulmonary, and hepatic side effects, raising concerns among physicians and patients regarding sustained therapy and compliance

- While newer formulations and improved clinical guidelines aim to mitigate these risks, safety concerns remain a key barrier to widespread adoption, particularly in patients with comorbidities or those requiring long-term management

- Overcoming these challenges through the development of safer next-generation molecules, improved clinical monitoring protocols, and enhanced physician and patient education will be critical for sustained growth of the anti-arrhythmic drugs market

- Limited patient adherence due to the need for continuous monitoring and potential side effects further impacts long-term treatment effectiveness and market penetration

- Variability in regulatory approvals and stringent clinical requirements for anti-arrhythmic drugs can delay the introduction of new therapies, posing additional challenges for market expansion

Anti Arrhythmic Drugs Market Scope

The market is segmented on the basis of drug class, drugs, route of administration, end-users, and distribution channel.

- By Drug Class

On the basis of drug class, the anti-arrhythmic drugs market is segmented into beta blockers, calcium channel blockers, sodium channel blockers, and potassium channel blockers. The beta blockers segment dominated the market with the largest market revenue share of 42.7% in 2025, driven by their widespread use as first-line therapy for rate control in atrial fibrillation and other arrhythmias. Beta blockers are highly preferred due to their proven efficacy in reducing heart rate, lowering blood pressure, and improving survival outcomes in cardiovascular patients. Their broad availability in both branded and generic forms, along with well-established clinical guidelines supporting their use, further strengthens their dominant position across hospitals and outpatient settings. In addition, their relatively favorable safety profile compared to other anti-arrhythmic classes contributes to their extensive adoption in long-term management.

The sodium channel blockers segment is anticipated to witness the fastest growth rate during the forecast period, driven by increasing utilization in rhythm control strategies for specific arrhythmia conditions. These drugs are particularly effective in treating supraventricular arrhythmias and certain ventricular arrhythmias, making them important in specialized cardiac care. Growing clinical adoption of precision-based therapies and improved diagnostic capabilities are enabling better patient selection for sodium channel blockers. Furthermore, ongoing research and development activities aimed at improving the safety and efficacy of this drug class are supporting its expansion. Rising demand for targeted anti-arrhythmic therapies with rapid onset of action also contributes to the accelerating growth of this segment.

- By Drugs

On the basis of drugs, the anti-arrhythmic drugs market is segmented into amiodarone, flecainide, ibutilide, and others. The amiodarone segment dominated the market with the largest market revenue share of 38.9% in 2025, owing to its high effectiveness in treating a wide range of arrhythmias, including both atrial and ventricular types. Amiodarone is widely used in acute care and emergency settings due to its strong rhythm-control capabilities and versatility across different patient populations. Its long-standing presence in clinical practice and inclusion in major treatment guidelines further reinforce its dominant position. Despite known side effects, its high efficacy in complex and refractory cases ensures continued preference among clinicians, especially in hospital environments.

The flecainide segment is anticipated to witness the fastest growth rate during the forecast period, driven by its increasing use in selected patient groups with supraventricular arrhythmias, particularly atrial fibrillation. Flecainide is gaining traction due to its effectiveness in rhythm control and its suitability for “pill-in-the-pocket” therapy, which supports outpatient and home-based treatment approaches. Growing preference for personalized treatment regimens and outpatient management of arrhythmias is boosting its adoption. In addition, improved patient monitoring and better screening for contraindications are expanding its safe usage. Increasing awareness among clinicians regarding its efficacy in structurally normal hearts is further supporting segment growth.

- By Route of Administration

On the basis of route of administration, the anti-arrhythmic drugs market is segmented into oral and parenteral. The oral segment dominated the market with the largest market revenue share of 64.3% in 2025, driven by its convenience, ease of administration, and suitability for long-term management of chronic arrhythmias. Oral anti-arrhythmic drugs are widely prescribed for outpatient care, enabling patients to manage conditions such as atrial fibrillation without frequent hospital visits. The availability of multiple oral formulations across different drug classes, along with high patient compliance, further supports the dominance of this segment. In addition, the growing shift toward homecare and self-administration of medications contributes significantly to the widespread use of oral therapies.

The parenteral segment is anticipated to witness the fastest growth rate during the forecast period, driven by its critical role in emergency and acute care settings where rapid onset of action is required. Parenteral anti-arrhythmic drugs are commonly used in hospitals for the immediate management of life-threatening arrhythmias and during surgical or intensive care procedures. Increasing hospitalization rates due to cardiovascular emergencies and the need for intravenous administration in critical cases are fueling demand for this segment. Advancements in hospital infrastructure and emergency cardiac care capabilities are also supporting the adoption of parenteral formulations.

- By End-Users

On the basis of end-users, the anti-arrhythmic drugs market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market with the largest market revenue share of 51.6% in 2025, driven by the high volume of diagnosed arrhythmia cases requiring acute care, monitoring, and specialized treatment. Hospitals serve as primary centers for emergency interventions, cardiac diagnostics, and initiation of anti-arrhythmic therapy, making them the leading end-user segment. The availability of advanced medical infrastructure, skilled healthcare professionals, and continuous patient monitoring capabilities further reinforces hospital dominance. In addition, most intravenous and complex drug regimens are administered in hospital settings, contributing to higher utilization.

The homecare segment is anticipated to witness the fastest growth rate during the forecast period, driven by the increasing shift toward outpatient management and patient-centric care models. Growing availability of oral anti-arrhythmic drugs and wearable monitoring devices enables patients to manage arrhythmias from home with periodic medical supervision. Rising healthcare costs and the preference for cost-effective treatment options are also encouraging home-based care. Furthermore, advancements in telemedicine and remote patient monitoring technologies are supporting safe and effective drug administration outside traditional clinical environments.

- By Distribution Channel

On the basis of distribution channel, the anti-arrhythmic drugs market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with the largest market revenue share of 48.2% in 2025, driven by the high volume of prescriptions generated within hospital settings for both inpatient and outpatient care. Hospital pharmacies play a critical role in dispensing drugs used in emergency treatments, post-procedural care, and chronic disease management under medical supervision. The direct linkage between physicians and hospital pharmacies ensures timely availability of prescribed medications, particularly for parenteral and specialized therapies.

The online pharmacy segment is anticipated to witness the fastest growth rate during the forecast period, driven by increasing digitalization of healthcare services and growing consumer preference for convenient medication access. Online pharmacies offer home delivery, competitive pricing, and easy prescription management, making them attractive for chronic disease patients requiring long-term medication. The expansion of e-commerce platforms and regulatory support for digital health services are further accelerating adoption. In addition, increased internet penetration and smartphone usage are contributing to the rapid growth of this distribution channel across both developed and emerging markets.

Anti Arrhythmic Drugs Market Regional Analysis

- North America dominated the anti-arrhythmic drugs market with the largest revenue share of 38.5% in 2025, attributed to advanced healthcare infrastructure, high adoption of innovative therapies, strong presence of key pharmaceutical players

- Patients and healthcare providers in the region benefit from widespread access to advanced diagnostic tools, well-established clinical guidelines, and a strong presence of leading pharmaceutical companies, supporting effective arrhythmia management

- This widespread adoption is further supported by high healthcare expenditure, a well-developed insurance system, and increasing awareness regarding early diagnosis and treatment of cardiac arrhythmias, establishing anti-arrhythmic drugs as a key component of cardiovascular care in both hospital and outpatient settings

U.S. Anti Arrhythmic Drugs Market Insight

The U.S. anti-arrhythmic drugs market captured the largest revenue share within North America in 2025, fueled by the high prevalence of cardiovascular diseases and the strong presence of advanced healthcare infrastructure and specialized cardiac care facilities. Patients and healthcare providers in the country benefit from early diagnosis, widespread screening programs, and access to innovative and guideline-driven treatment options. The growing adoption of both branded and generic anti-arrhythmic drugs, combined with strong reimbursement frameworks and high healthcare spending, further propels market growth. Moreover, the increasing use of precision medicine approaches, remote cardiac monitoring, and integration of digital health tools is significantly contributing to the expansion of the market across hospital and outpatient settings

Europe Anti-Arrhythmic Drugs Market Insight

The Europe anti-arrhythmic drugs market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising burden of cardiovascular diseases and the increasing aging population across the region. Stringent regulatory frameworks and well-established healthcare systems are supporting the adoption of standardized treatment protocols for arrhythmia management. European consumers benefit from universal healthcare access, which facilitates early diagnosis and treatment, thereby boosting demand for anti-arrhythmic therapies. In addition, growing investments in clinical research, increasing awareness of cardiac health, and the expansion of specialized cardiology centers are contributing to steady market growth across both residential and hospital care segments.

U.K. Anti-Arrhythmic Drugs Market Insight

The U.K. anti-arrhythmic drugs market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing cases of atrial fibrillation and other rhythm disorders, along with a strong focus on preventive healthcare. The country’s National Health Service (NHS) plays a crucial role in providing widespread access to cardiac diagnostics and treatment, supporting early intervention and long-term disease management. In addition, rising awareness among patients regarding heart health, coupled with the availability of advanced monitoring technologies and guideline-based therapies, is encouraging the adoption of anti-arrhythmic drugs. The emphasis on cost-effective treatment options and increasing use of generic medications further supports market expansion.

Germany Anti-Arrhythmic Drugs Market Insight

The Germany anti-arrhythmic drugs market is expected to expand at a considerable CAGR during the forecast period, fueled by a strong healthcare infrastructure, high levels of medical innovation, and a growing elderly population. Germany’s focus on advanced diagnostics and precision medicine supports effective management of arrhythmias through targeted drug therapies. The country’s well-established hospital networks and emphasis on quality healthcare encourage the adoption of both acute and long-term anti-arrhythmic treatments. Furthermore, increasing awareness of cardiovascular diseases, combined with government support for healthcare research and digitalization in medical services, is driving the integration of modern therapeutic approaches within clinical practice.

Asia-Pacific Anti-Arrhythmic Drugs Market Insight

The Asia-Pacific anti-arrhythmic drugs market is poised to grow at the fastest CAGR during the forecast period, driven by a rapidly aging population, increasing prevalence of cardiovascular diseases, and improving healthcare infrastructure across emerging economies. Rising healthcare expenditure, expanding access to diagnostic services, and growing awareness of heart rhythm disorders are significantly contributing to market expansion. Countries in the region are witnessing increased adoption of both branded and generic anti-arrhythmic drugs due to affordability and availability. In addition, government initiatives aimed at strengthening healthcare systems and the growing penetration of health insurance are supporting wider access to treatment, making the region a key growth hub for the market.

Japan Anti-Arrhythmic Drugs Market Insight

The Japan anti-arrhythmic drugs market is gaining momentum due to the country’s rapidly aging population, advanced healthcare system, and high prevalence of cardiovascular conditions. Japan places a strong emphasis on early diagnosis and preventive care, which supports the timely use of anti-arrhythmic therapies. The integration of advanced diagnostic technologies, along with widespread hospital access, enables effective management of complex arrhythmias. In addition, the country’s focus on innovation in pharmaceuticals and clinical research contributes to the availability of advanced treatment options. Increasing use of minimally invasive procedures combined with pharmacological therapies is further supporting the demand for anti-arrhythmic drugs in both hospital and outpatient settings.

India Anti-Arrhythmic Drugs Market Insight

The India anti-arrhythmic drugs market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large population base, rising burden of cardiovascular diseases, and improving access to healthcare services. Rapid urbanization, changing lifestyles, and increasing incidence of risk factors such as hypertension and diabetes are contributing to a growing patient pool requiring arrhythmia management. The expansion of healthcare infrastructure, along with increasing availability of affordable generic medications, is making treatment more accessible across urban and rural areas. In addition, government initiatives focused on improving healthcare delivery and growing awareness of cardiac health are further driving the adoption of anti-arrhythmic drugs in India.

Anti Arrhythmic Drugs Market Share

The Anti Arrhythmic Drugs industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Sanofi (France)

- Bristol-Myers Squibb Company (U.S.)

- GSK plc (U.K.)

- Viatris Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Abbott (U.S.)

- AstraZeneca (U.K.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Fresenius Kabi AG (Germany)

- Bayer AG (Germany)

- Sun Pharmaceutical Industries Ltd. (India)

- Lupin Limited (India)

- Glenmark Pharmaceuticals Ltd. (India)

- Amneal Pharmaceuticals Inc. (U.S.)

- Mayne Pharma Group Limited (Australia)

- Upsher-Smith Laboratories, LLC (U.S.)

- Amomed Pharma GmbH (Austria)

- Dr. Reddy’s Laboratories Ltd. (India)

What are the Recent Developments in Global Anti Arrhythmic Drugs Market?

- In March 2026, Everest Medicines entered an asset purchase agreement with Corxel Pharmaceuticals to develop and commercialize CARDAMYST™ (etripamil) nasal spray in Greater China, expanding the geographic reach and commercial development of this novel anti-arrhythmic therapy

- In December 2025, the U.S. Food and Drug Administration (FDA) approved CARDAMYST™ (etripamil) nasal spray, marking the first self-administered, rapid-acting treatment for paroxysmal supraventricular tachycardia (PSVT) that patients can use outside hospital settings, potentially transforming acute arrhythmia management

- In July 2025, Everest Medicines announced updated positive results from the ongoing Phase 1b/2a clinical trial of EVER001 (a novel BTK inhibitor), with data showing strong efficacy and tolerability in reducing key biomarkers in autoimmune disease highlighting potential crossover interest in arrhythmia-related immune pathways and novel small molecule therapies

- In March 2025, Milestone Pharmaceuticals received a complete response letter from the U.S. FDA, declining approval of its heart-rhythm nasal spray (Cardamyst) and requesting additional manufacturing data, reflecting regulatory challenges and ongoing refinement in anti-arrhythmic drug development

- In October 2023, Pfizer presented new data on arrhythmia-related drugs including amiodarone and flecainide at a major scientific meeting, underscoring ongoing clinical research and continued evaluation of established anti-arrhythmic agents in broader therapeutic contexts

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.