Global Anti Cathepsin B Market

Market Size in USD Million

USD

199.70 Million

USD

256.93 Million

2025

2033

USD

199.70 Million

USD

256.93 Million

2025

2033

| 2026 - 2033 | |

| USD 199.70 Million | |

| USD 256.93 Million | |

| % | |

|

Anti-cathepsin B Market Size

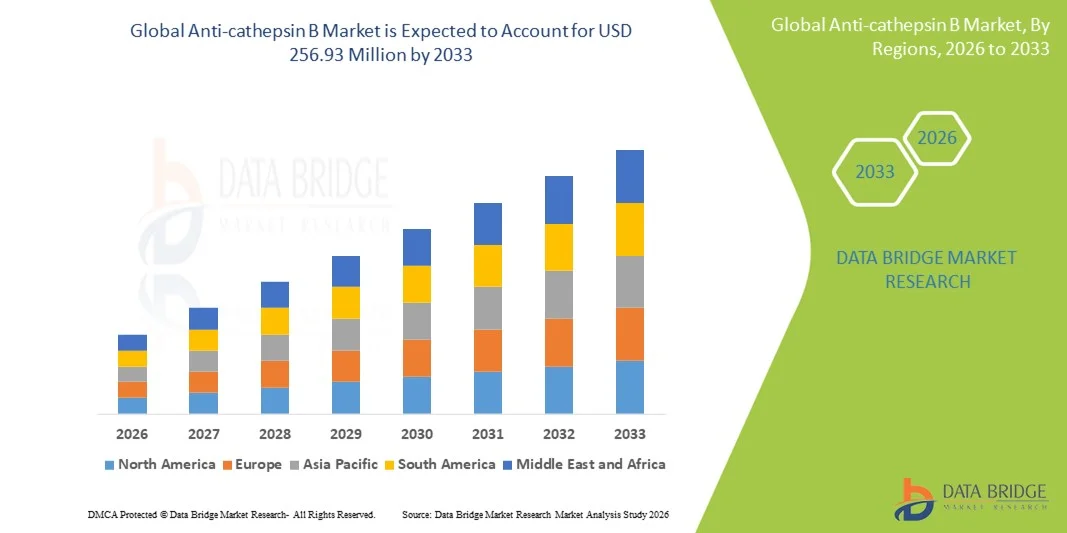

- The global anti-Cathepsin B market size was valued at USD 199.70 million in 2025 and is expected to reach USD 256.93 million by 2033, at a CAGR of 3.2% during the forecast period

- The market growth is largely fueled by increasing research and development of targeted therapies, growing prevalence of diseases such as cancer and neurodegenerative disorders, and technological advancements in protease inhibitors, leading to expanded applications in both therapeutic and research settings

- Furthermore, rising demand for effective, specific, and safe anti-Cathepsin B therapies is establishing these inhibitors as a key strategy in precision medicine. These converging factors are accelerating the uptake of anti-Cathepsin B solutions, thereby significantly boosting the industry's growth

Anti-cathepsin B Market Analysis

- Anti-Cathepsin B inhibitors, targeting the protease Cathepsin B involved in cancer, neurodegenerative, and inflammatory diseases, are increasingly important in therapeutic development and research applications due to their potential for precise disease modulation and integration into combination therapies

- The escalating demand for anti-Cathepsin B therapies is primarily fueled by rising prevalence of cancer and chronic diseases, increasing investment in targeted drug development, and growing focus on precision medicine for improved efficacy and safety profiles

- North America dominated the anti-Cathepsin B market with the largest revenue share of 39% in 2025, driven by strong R&D infrastructure, high healthcare expenditure, and the presence of leading biotechnology and pharmaceutical companies actively developing Cathepsin B inhibitors

- Asia-Pacific is expected to be the fastest growing region in the anti-Cathepsin B market during the forecast period due to expanding pharmaceutical research, increasing incidence of target diseases, and growing investment in biologics and advanced therapies

- Primary antibodies segment dominated the anti-Cathepsin B market with a market share of 42.8% in 2025, driven by their high specificity, efficacy in research and therapeutic applications, and wide use across techniques such as immunohistochemistry, Western blotting, ELISA, and flow cytometry

Report Scope and Anti-cathepsin B Market Segmentation

|

Attributes |

Anti-cathepsin B Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Anti-cathepsin B Market Trends

Advancements in Targeted Therapeutics and Research Applications

- A significant and accelerating trend in the global anti-Cathepsin B market is the increasing development of targeted therapies and research tools, enabling precise disease modulation and integration into multi-modal treatment strategies

- For instance, Primabio’s anti-Cathepsin B antibodies are being used in preclinical studies to enhance therapeutic efficacy in cancer and neurodegenerative disease models

- Integration with advanced techniques such as immunohistochemistry, ELISA, and flow cytometry is improving assay sensitivity and reproducibility, allowing researchers to detect and quantify Cathepsin B with greater accuracy

- The growing use of anti-Cathepsin B proteins and peptides in diagnostic and therapeutic research facilitates the development of personalized medicine approaches and combination therapy strategies

- This trend towards more precise, efficient, and multifunctional Cathepsin B inhibitors is fundamentally reshaping research and therapeutic expectations, prompting companies such as Abcam and Thermo Fisher to expand their product offerings with advanced antibody and protein solutions

- The demand for anti-Cathepsin B products that offer enhanced specificity and versatility is growing rapidly across pharmaceutical, academic, and clinical research sectors, as researchers increasingly prioritize high-quality, reproducible reagents

Anti-cathepsin B Market Dynamics

Driver

Rising Prevalence of Target Diseases and Precision Medicine Focus

- The increasing prevalence of cancer, neurodegenerative disorders, and inflammatory diseases, coupled with the growing emphasis on precision medicine, is a significant driver for the heightened demand for anti-Cathepsin B products

- For instance, in March 2025, Abcam launched a new line of high-affinity Cathepsin B primary antibodies to support preclinical research in oncology and neurodegeneration, highlighting the growing investment in targeted therapeutic research

- As researchers and clinicians seek highly specific inhibitors and detection tools, anti-Cathepsin B products provide critical solutions for understanding disease mechanisms and optimizing treatment strategies

- Furthermore, the expanding adoption of advanced laboratory techniques and standardized research protocols is making Cathepsin B inhibitors and antibodies an essential component of therapeutic discovery and biomarker studies

- The proven effectiveness of Cathepsin B inhibition in modulating disease progression and the increasing integration into combination therapy studies are key factors propelling market adoption in both academic and pharmaceutical sectors

- The ongoing focus on personalized medicine and biomarker-driven research, along with increasing funding for therapeutic R&D, further contributes to sustained market growth

Restraint/Challenge

High Cost and Technical Complexity of Cathepsin B Products

- Concerns surrounding the high cost and technical complexity of anti-Cathepsin B antibodies, proteins, and peptides pose a significant challenge to broader market penetration

- For instance, premium monoclonal antibodies with high specificity for Cathepsin B are priced significantly higher than general-purpose research antibodies, limiting adoption in smaller laboratories and developing regions

- Handling and application of these products require trained personnel and advanced laboratory infrastructure, which can restrict widespread utilization, particularly in resource-limited settings

- Furthermore, variability in reagent quality across different suppliers can impact reproducibility and data reliability, making some researchers hesitant to adopt certain products

- While initiatives for improving accessibility and standardization are underway, the perceived complexity and cost barrier still hinder broader adoption, especially among emerging research institutions or cost-sensitive pharmaceutical R&D projects

- Overcoming these challenges through enhanced affordability, robust product validation, and comprehensive technical support will be vital for sustained growth and wider adoption of anti-Cathepsin B solutions

Anti-cathepsin B Market Scope

The market is segmented on the basis of product type, application, technique, end-users, and distribution channel.

- By Product Type

On the basis of product type, the anti-Cathepsin B market is segmented into primary antibodies, proteins and peptides, and lysates. The primary antibodies segment dominated the market with the largest revenue share of 42.8% in 2025, driven by their high specificity, reproducibility, and critical role in both research and therapeutic development. Researchers prefer primary antibodies for detecting Cathepsin B across multiple techniques such as immunohistochemistry, Western blotting, and ELISA, making them highly versatile. The market also sees strong demand due to the availability of validated and high-affinity antibodies from leading suppliers, ensuring consistent experimental results. Pharmaceutical companies leverage these antibodies for preclinical and clinical studies, further solidifying market dominance. In addition, primary antibodies are widely used in combination with secondary antibodies to enhance signal detection and accuracy in diagnostic research. Their role in precision medicine research, especially in oncology and neurodegenerative diseases, continues to drive adoption and revenue growth.

The proteins and peptides segment is anticipated to witness the fastest growth rate of 19.8% from 2026 to 2033, fueled by increasing use in diagnostic assays and therapeutic research. Proteins and peptides allow researchers to study enzyme-substrate interactions and Cathepsin B activity in more physiologically relevant settings. Their applications in combination therapies and targeted inhibitor development provide high-value opportunities for pharmaceutical R&D. In addition, advancements in recombinant peptide synthesis and protein engineering are enhancing their stability and specificity, encouraging broader adoption. Proteins and peptides are increasingly integrated into multiplex assays for biomarker discovery, supporting personalized medicine initiatives. The rising demand for high-quality, application-ready peptide reagents in both academic and industrial research further contributes to market acceleration.

- By Application

On the basis of application, the anti-Cathepsin B market is segmented into cancer, traumatic brain injury, Ebola infection, fertility treatment, and others. The cancer segment dominated the market with a revenue share of 46.5% in 2025, due to the well-established role of Cathepsin B in tumor progression, invasion, and metastasis. Anti-Cathepsin B inhibitors and antibodies are widely used in preclinical cancer models and translational research to evaluate therapeutic efficacy. Pharmaceutical companies are increasingly incorporating Cathepsin B inhibition into combination therapy strategies for precision oncology. The segment’s dominance is further supported by robust funding for cancer research and growing awareness of protease-targeted therapies. Academic researchers extensively use Cathepsin B reagents to study tumor microenvironments and metastatic mechanisms. In addition, the development of predictive biomarkers involving Cathepsin B has increased the clinical research applications of this segment, driving continuous revenue growth.

The traumatic brain injury (TBI) segment is expected to witness the fastest growth rate of 17.4% from 2026 to 2033, driven by rising research on Cathepsin B’s role in neuroinflammation and neuronal damage. Anti-Cathepsin B products are increasingly employed to explore therapeutic strategies for TBI, providing opportunities for novel intervention studies. Advances in in vitro and in vivo models have enabled more precise evaluation of Cathepsin B activity in brain injury, expanding product demand. The growth is also supported by collaborations between pharmaceutical companies and academic institutions focusing on neurodegenerative and injury-related disorders. TBI research is gaining attention due to increased prevalence and awareness, encouraging investments in Cathepsin B-targeted studies. Moreover, integration of these products into multiplex neurobiological assays enhances the reliability of experimental outcomes, further accelerating adoption.

- By Technique

On the basis of technique, the market is segmented into immunohistochemistry, immunofluorescence, Western blotting, ELISA, flow cytometry, and others. The immunohistochemistry segment dominated the market with a share of 40.8% in 2025, due to its widespread use in visualizing Cathepsin B expression in tissue samples. Researchers rely on immunohistochemistry for spatial localization and quantification of Cathepsin B, supporting cancer and neurodegenerative disease studies. The segment benefits from standardized protocols, commercial antibody availability, and ease of integration into preclinical workflows. Pharmaceutical and academic researchers prefer immunohistochemistry to validate target engagement of Cathepsin B inhibitors. In addition, advancements in automated staining platforms and imaging software enhance the reproducibility and efficiency of experiments. Its critical role in translational research ensures sustained market dominance.

The ELISA segment is expected to witness the fastest growth rate of 18.6% from 2026 to 2033, driven by high demand for quantitative measurement of Cathepsin B in biological fluids and cell lysates. ELISA assays are widely applied in drug screening, biomarker validation, and therapeutic monitoring. The growing adoption of high-throughput and multiplex ELISA formats enhances data accuracy and throughput. Pharmaceutical companies and clinical laboratories increasingly employ ELISA kits for evaluating treatment efficacy and monitoring disease progression. In addition, ELISA’s compatibility with standardized laboratory equipment makes it accessible for both academic and industrial researchers. Advances in assay sensitivity and kit availability further contribute to the rapid expansion of this segment.

- By End-Users

On the basis of end-users, the market is segmented into pharmaceutical companies and academic and research institutes. The pharmaceutical companies segment dominated the market with a share of 52.1% in 2025, owing to their extensive use of anti-Cathepsin B products in drug discovery, preclinical studies, and therapeutic development. Leading biotech and pharma companies invest heavily in Cathepsin B-targeted research to develop novel inhibitors for cancer and neurodegenerative diseases. The segment’s dominance is also driven by large-scale adoption of validated antibodies, proteins, and lysates in high-throughput R&D workflows. Pharmaceutical researchers rely on these products for combination therapy evaluation and biomarker discovery. Strategic collaborations with academic institutions further support the development of novel therapeutics, reinforcing market share.

The academic and research institutes segment is expected to witness the fastest growth rate of 16.9% from 2026 to 2033, fueled by increasing research initiatives, grants, and funding for Cathepsin B studies. Universities and independent research organizations are expanding preclinical and translational studies, driving demand for antibodies, peptides, and lysates. Integration of Cathepsin B research into educational programs and collaborative projects with pharmaceutical companies further boosts product utilization. The growth is also supported by rising awareness of Cathepsin B’s role in disease mechanisms and biomarker studies. Academic adoption is expected to increase as research techniques become more standardized and reagent availability improves, creating significant market opportunities.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The online pharmacy segment dominated the market with a share of 44.7% in 2025, driven by ease of access, wider product availability, and growing adoption of digital procurement platforms by researchers and institutions. Online distribution allows academic and pharmaceutical customers to conveniently source anti-Cathepsin B antibodies, proteins, and lysates from global suppliers. The segment also benefits from faster delivery, bulk ordering options, and detailed product information available on e-commerce portals. Online platforms increasingly provide validated and application-ready products, enhancing customer confidence and repeat purchases. Ease of comparison and reviews also drives adoption among cost-conscious buyers.

The hospital pharmacy segment is expected to witness the fastest growth rate of 15.8% from 2026 to 2033, fueled by increasing in-house research initiatives and clinical studies involving Cathepsin B. Hospitals are expanding translational research programs and personalized medicine initiatives, requiring direct procurement of high-quality anti-Cathepsin B products. Collaboration with academic institutes and pharmaceutical partners further supports adoption. Hospital pharmacies prefer sourcing validated reagents for diagnostics, biomarker studies, and therapeutic monitoring. Rising investment in clinical research infrastructure across hospitals enhances access to these products, accelerating segment growth.

Anti-cathepsin B Market Regional Analysis

- North America dominated the anti-Cathepsin B market with the largest revenue share of 39% in 2025, driven by strong R&D infrastructure, high healthcare expenditure, and the presence of leading biotechnology and pharmaceutical companies actively developing Cathepsin B inhibitors

- Researchers and pharmaceutical companies in the region highly value the specificity, reproducibility, and versatility offered by anti-Cathepsin B products across applications such as cancer, neurodegenerative disorders, and inflammatory diseases

- This widespread adoption is further supported by strong funding for preclinical and translational research, advanced laboratory infrastructure, and collaborations between academic institutions and industry, establishing anti-Cathepsin B reagents as essential tools in both research and therapeutic development

U.S. Anti-cathepsin B Market Insight

The U.S. anti-Cathepsin B market captured the largest revenue share of 82% in 2025 within North America, fueled by strong investment in pharmaceutical R&D, extensive preclinical studies, and the growing focus on precision medicine. Researchers and pharmaceutical companies are increasingly prioritizing Cathepsin B-targeted therapies for cancer, neurodegenerative, and inflammatory diseases. The robust infrastructure for laboratory research, combined with widespread adoption of advanced techniques such as immunohistochemistry and ELISA, further propels the market. Moreover, collaborations between biotech firms and academic institutions are accelerating product development and clinical applications, significantly contributing to market growth.

Europe Anti-Cathepsin B Market Insight

The Europe anti-Cathepsin B market is projected to expand at a substantial CAGR throughout the forecast period, driven by growing funding for biomedical research, regulatory support for therapeutic innovation, and increasing adoption of targeted inhibitors. Rising incidence of cancers and chronic diseases, coupled with a strong academic research ecosystem, is fostering the uptake of anti-Cathepsin B products. European researchers and pharmaceutical companies are increasingly incorporating these reagents into translational and preclinical studies. In addition, the demand for high-quality, validated antibodies and proteins across diagnostic and therapeutic applications is contributing to significant market growth in the region.

U.K. Anti-Cathepsin B Market Insight

The U.K. anti-Cathepsin B market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing R&D investment in oncology and neurodegenerative disorders and the adoption of advanced research reagents. Rising awareness of Cathepsin B’s role in disease progression is encouraging both academic and pharmaceutical sectors to integrate these products into experimental workflows. The U.K.’s strong biotech and pharmaceutical infrastructure, alongside robust funding for translational medicine, is expected to continue stimulating market expansion. Collaborative research programs and availability of high-quality antibodies, proteins, and peptides further support growth.

Germany Anti-Cathepsin B Market Insight

The Germany anti-Cathepsin B market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing biomedical research initiatives and a strong focus on innovative therapeutic solutions. Germany’s well-developed research infrastructure, combined with government incentives for pharmaceutical innovation, promotes the adoption of Cathepsin B inhibitors in both preclinical and translational studies. Researchers increasingly leverage these products in cancer, neurodegeneration, and biomarker discovery studies. Furthermore, collaborations between universities and biotech companies are enhancing product utilization, with an emphasis on reproducibility, high specificity, and quality assurance.

Asia-Pacific Anti-Cathepsin B Market Insight

The Asia-Pacific anti-Cathepsin B market is poised to grow at the fastest CAGR of 22% during the forecast period of 2026 to 2033, driven by expanding pharmaceutical R&D, rising prevalence of cancers and chronic diseases, and increasing government support for biomedical research in countries such as China, Japan, and India. The growing adoption of advanced laboratory techniques and the establishment of new research centers are driving market expansion. Furthermore, Asia-Pacific is emerging as a hub for antibody and protein manufacturing, increasing accessibility and affordability of anti-Cathepsin B products to a wider research and pharmaceutical customer base.

Japan Anti-Cathepsin B Market Insight

The Japan anti-Cathepsin B market is gaining momentum due to the country’s strong focus on biotechnology, advanced research infrastructure, and the increasing number of preclinical and translational studies. Japanese researchers place significant emphasis on developing targeted therapies for cancer and neurodegenerative diseases. Integration of Cathepsin B inhibitors into combination therapy research and diagnostic applications is fueling growth. Moreover, collaborations between pharmaceutical companies and academic institutions, along with government support for precision medicine initiatives, are expected to drive demand for high-quality antibodies, proteins, and peptides in both research and clinical applications.

India Anti-Cathepsin B Market Insight

The India anti-Cathepsin B market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s rapidly growing biomedical research sector, increasing incidence of target diseases, and rising investment in preclinical studies. India is becoming an important hub for research reagent production, making antibodies, proteins, and peptides more accessible and affordable. The expansion of academic research programs, collaborations with global pharmaceutical companies, and government initiatives supporting biotechnology and precision medicine are key factors propelling market growth in India.

Anti-cathepsin B Market Share

The Anti-cathepsin B industry is primarily led by well-established companies, including:

- Merck KGaA, (Germany)

- Eli Lilly and Company (U.S.)

- Boehringer Ingelheim International GmbH (Germany)

- Bio Techne Corporation (U.S.)

- AddLife AB (Sweden)

- BioVision, Inc. (U.S.)

- R&D Systems, Inc. (U.S.)

- Cayman Chemical Company, Inc. (U.S.)

- Selleck Chemicals LLC (U.S.)

- Santa Cruz Biotechnology, Inc. (U.S.)

- Tocris Bioscience (U.K.)

- ViroBay, Inc. (U.S.)

- MedChemExpress (U.S.)

- BOC Sciences (U.S.)

- Biorbyt Ltd (U.K.)

- GlpBio Technology LLC (U.S.)

- Echelon Biosciences (U.S.)

- AG Scientific (U.S.)

- ApexBio Technology (U.S.)

- OXiGENE, Inc. (U.S.)

What are the Recent Developments in Global Anti-cathepsin B Market?

- In April 2025, A study published in Aging Cell discovered that inhibiting Cathepsin B in mice can increase ovarian (oocyte) reserve by preventing IGF1R degradation, thereby enhancing mitophagy and mitochondrial health. They showed that Cathepsin B inhibition leads to a rise in IGF1R levels, which in turn activates AKT–mTOR signaling and promotes mitochondrial biogenesis

- In April 2025, Scientists at Konkuk University developed a novel peptide‑based nano‑sized Cathepsin B inhibitor (an RR–BA conjugate), which self‑assembles into nanoparticles and showed strong Cathepsin B inhibition and anticancer efficacy (colorectal cancer) in vitro and in mice, with low toxicity

- In December 2023, A proteomics study published in Brain found that levels of Cathepsin B in extracellular vesicles (from CSF and plasma) change during Alzheimer’s disease (ATN staging), suggesting Cathepsin B could serve as a biomarker and potential therapeutic target in Alzheimer’s pathology

- In August 2023, A study in Acta Neuropathologica Communications reported that Cathepsin B is more abundant and active in microglia in Alzheimer’s disease and Down syndrome brains, implicating its role in neuroinflammation and neurodegeneration

- In March 2023, Researchers developed theranostic nanoparticles (TNPs) for glioblastoma (GBM) that are cleaved by Cathepsin B to selectively release the cytotoxin MMAE, while the nanoparticle core (ferumoxytol) allows MRI tracking of drug delivery. These dual-function nanoparticles combine therapy (via release of MMAE only in Cathepsin B-rich tumor environments) with noninvasive imaging, enabling clinicians to monitor drug delivery in real time

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.