Global Anti Fibrotic Drug Therapies Market

Market Size in USD Billion

USD

7.43 Billion

USD

18.92 Billion

2025

2033

USD

7.43 Billion

USD

18.92 Billion

2025

2033

| 2026 - 2033 | |

| USD 7.43 Billion | |

| USD 18.92 Billion | |

| % | |

|

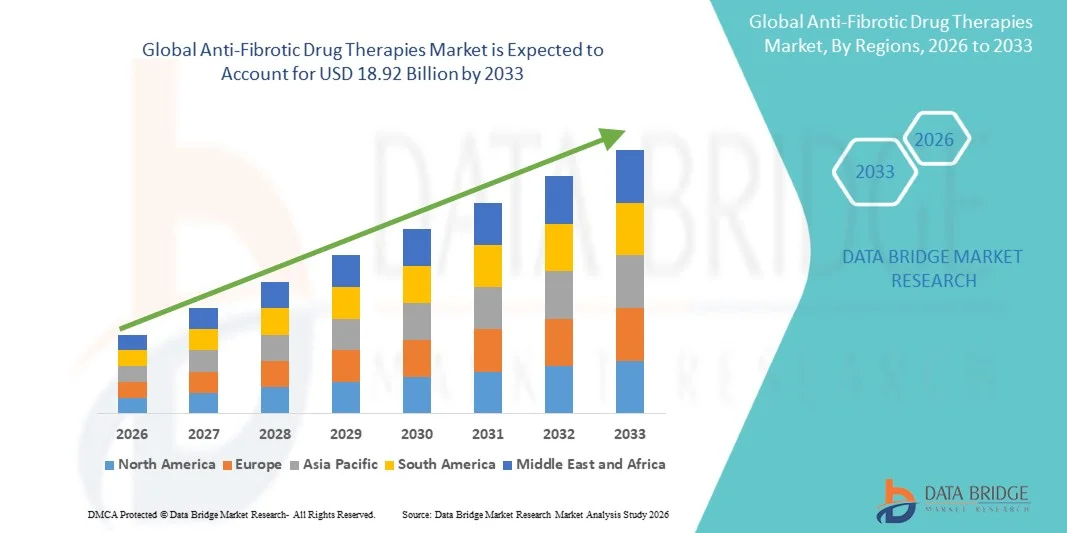

Anti-Fibrotic Drug Therapies Market Size

- The global anti-fibrotic drug therapies market size was valued at USD 7.43 billion in 2025 and is expected to reach USD 18.92 billion by 2033, at a CAGR of 12.40% during the forecast period

- The market growth is largely fueled by the increasing prevalence of fibrotic diseases, growing awareness about early diagnosis, and advancements in therapeutic research targeting fibrosis

- Furthermore, rising demand for effective and targeted treatment options, along with government initiatives to support drug development, is driving the adoption of Anti-Fibrotic Drug Therapies solutions, thereby significantly boosting the industry's growth

Anti-Fibrotic Drug Therapies Market Analysis

- Anti-Fibrotic Drug Therapies market growth is largely fueled by the increasing prevalence of fibrotic diseases, including pulmonary fibrosis, liver fibrosis, and kidney fibrosis, alongside rising awareness of early diagnosis and effective treatment options

- The escalating demand for Anti-Fibrotic Drug Therapies is primarily driven by advances in biologic and small-molecule therapies, growing investment in R&D, and an increasing focus on personalized medicine for patients with progressive fibrotic conditions

- North America dominated the anti-fibrotic drug therapies market with the largest revenue share of approximately 41.5% in 2025, supported by advanced healthcare infrastructure, strong R&D investments, and a high adoption rate of innovative therapeutics, with the U.S. leading market growth through extensive clinical trials and government-backed initiatives

- Asia-Pacific is expected to be the fastest-growing region in the anti-fibrotic drug therapies market during the forecast period, with a projected CAGR of 9.6%, driven by increasing healthcare spending, improving access to advanced therapeutics, and growing patient awareness in countries such as China and India

- The Pirfenidone segment dominated the largest revenue share of 45% in 2025, driven by its established efficacy in slowing the progression of idiopathic pulmonary fibrosis (IPF)

Report Scope and Anti-Fibrotic Drug Therapies Market Segmentation

|

Attributes |

Anti-Fibrotic Drug Therapies Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Boehringer Ingelheim (Germany) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Anti-Fibrotic Drug Therapies Market Trends

“Enhanced Research and Clinical Developments”

- A significant and accelerating trend in the global Anti-Fibrotic Drug Therapies market is the growing focus on advanced research and clinical development. Pharmaceutical and biotechnology companies are heavily investing in discovering new molecules and treatment mechanisms targeting fibrotic diseases affecting the lungs, liver, and kidneys

- This trend is encouraging collaborations between research institutions and commercial organizations to accelerate the translation of scientific discoveries into clinically effective therapies

- For instance, in June 2024, Galapagos NV reported positive Phase II clinical trial results for its anti-fibrotic candidate in patients with idiopathic pulmonary fibrosis (IPF), demonstrating significant improvement in lung function. Such clinical successes are motivating further investment and partnerships across multiple regions, accelerating the availability of novel anti-fibrotic therapies

- Increased clinical research also includes combination therapy studies and personalized treatment approaches based on patient-specific biomarkers. This enables healthcare providers to offer more targeted interventions, improving treatment efficacy and reducing adverse effects

- The expansion of global clinical trials across North America, Europe, and Asia-Pacific is also contributing to faster knowledge dissemination, regulatory approvals, and patient access

- In addition, the trend towards patient-centric drug development is influencing the formulation of orally administered and less invasive therapies, improving adherence and quality of life

- Biopharmaceutical companies are establishing specialized R&D centers in regions with strong scientific infrastructure, such as the U.S., Germany, and Japan, to focus on anti-fibrotic drug innovation

- The use of real-world evidence and post-marketing surveillance studies is supporting the validation of efficacy and safety of newly approved therapies

- Collaborations with healthcare providers and hospitals are enabling broader patient recruitment and better monitoring during clinical trials

- Strategic mergers and acquisitions are also facilitating technology and expertise transfer, helping companies rapidly expand their anti-fibrotic therapy portfolios

- Overall, the strong emphasis on research and clinical development is setting the foundation for a robust and diversified pipeline, ensuring long-term growth in the market

Anti-Fibrotic Drug Therapies Market Dynamics

Driver

“Rising Prevalence of Fibrotic Diseases and Unmet Medical Need”

- The growing prevalence of fibrotic diseases, such as IPF, liver cirrhosis, and NASH-related fibrosis, is the primary driver for the Anti-Fibrotic Drug Therapies market. Increasing patient awareness and early diagnosis are expanding the demand for effective treatment solutions

- For instance, in 2023, Intercept Pharmaceuticals expanded the distribution of its Ocaliva therapy to European markets to address the rising cases of NASH-induced fibrosis. Such strategic launches demonstrate the market’s response to rising disease burden and unmet medical needs

- Healthcare providers are actively seeking therapies that can halt or reverse disease progression, given the limited effectiveness of existing options

- Government and private payer reimbursement initiatives for anti-fibrotic drugs are improving accessibility and affordability

- The increase in chronic lifestyle-related diseases, such as obesity and metabolic syndrome, is driving fibrosis incidence, particularly in North America and Asia-Pacific

- Growing patient populations, combined with improved diagnostic capabilities, are further increasing the market potential

- Demand for innovative treatments that offer improved efficacy and reduced side effects is propelling research and commercial adoption

- The aging global population is contributing to higher prevalence of fibrotic diseases, especially IPF, which predominantly affects older adults

- Expansion of hospital and outpatient treatment centers is providing infrastructure for wider therapy adoption

- Investments in education and awareness programs by pharmaceutical companies and healthcare organizations are also driving patient engagement and therapy uptake

Restraint/Challenge

“High Drug Development Costs and Regulatory Complexity”

- One of the key challenges in the anti-fibrotic drug therapies market is the high cost of drug development, coupled with stringent regulatory requirements. Clinical trials for fibrosis therapies are often lengthy and expensive due to the chronic nature of the diseases

- For instance, several NASH-targeted therapies have faced delays in Phase III trials due to challenges in patient recruitment and meeting efficacy endpoints. Such delays increase financial risks and can impact smaller biotech firms disproportionately

- Regulatory approval processes require extensive clinical evidence on safety, efficacy, and long-term outcomes, making market entry time-consuming

- The relatively high cost of newly approved anti-fibrotic drugs can limit patient access, especially in developing regions

- Reimbursement limitations in certain countries can further restrict market adoption

- Market penetration is sometimes hampered by a lack of healthcare infrastructure and diagnostic facilities in emerging economies

- The complexity of combination therapy trials introduces additional operational and regulatory challenges

- Manufacturing scale-up for biologics and novel compounds can be expensive, affecting supply and pricing strategies

- Intellectual property disputes and patent expirations may pose challenges for long-term market stability

- Addressing these challenges requires strategic collaborations, efficient clinical trial designs, and robust regulatory engagement to ensure timely and cost-effective therapy availability

Anti-Fibrotic Drug Therapies Market Scope

The market is segmented on the basis of Drug Type and End User.

• By Drug Type

On the basis of drug type, the Anti-Fibrotic Drug Therapies market is segmented into Pirfenidone, Nintedanib, and other anti-fibrotic drugs. The Pirfenidone segment dominated the largest revenue share of 45% in 2025, driven by its established efficacy in slowing the progression of idiopathic pulmonary fibrosis (IPF). Hospitals and specialty clinics widely adopt Pirfenidone due to its proven clinical outcomes, favorable safety profile, and extensive regulatory approvals across major markets. The drug’s oral administration makes it convenient for both inpatient and outpatient care, supporting adherence and long-term therapy. Pharmaceutical companies actively promote Pirfenidone through awareness programs and partnerships with healthcare providers. Its inclusion in treatment guidelines and reimbursement schemes further strengthens adoption. Pirfenidone is compatible with combination therapies, expanding clinical applications. Patient preference for oral therapy and minimal monitoring requirements contribute to its dominance. Research institutions continue to evaluate Pirfenidone in clinical studies, reinforcing market confidence. Its widespread use in North America, Europe, and Asia-Pacific supports the segment’s leading market position. Overall, strong clinical evidence, accessibility, and physician trust ensure Pirfenidone remains the market leader.

The Nintedanib segment is expected to witness the fastest CAGR of 12.5% from 2026 to 2033, fueled by its efficacy across multiple fibrotic conditions, including IPF, systemic sclerosis-associated interstitial lung disease, and other progressive fibrosing interstitial lung diseases. Its multi-kinase inhibitor mechanism offers an alternative for patients intolerant to Pirfenidone or requiring combination therapy. Specialty clinics and hospitals increasingly prefer Nintedanib due to its effectiveness in slowing disease progression and improving patient outcomes. Adoption is rising in emerging markets as healthcare infrastructure improves and reimbursement schemes expand. Research institutes are exploring novel indications and combination therapies, supporting clinical adoption. Pharmaceutical innovations, such as sustained-release formulations and patient support programs, enhance usability and adherence. Physicians and patients value its ability to reduce hospitalizations and disease complications. Global awareness campaigns and increasing incidence of fibrotic diseases further drive growth. The segment benefits from strong pipeline developments, regulatory approvals, and growing physician familiarity. Convenience of oral dosing and safety monitoring compatibility make it highly adoptable. Overall, Nintedanib’s clinical versatility and emerging-market penetration support rapid revenue growth.

• By End-User

On the basis of end-user, the Anti-Fibrotic Drug Therapies market is segmented into hospitals, specialty clinics, home-care settings, and research institutes. Hospitals dominated the largest revenue share of 50% in 2025, driven by high patient volumes, integration into clinical protocols, and centralized administration of anti-fibrotic therapies. Hospitals benefit from established procurement channels, trained staff, and monitoring facilities required for safe therapy administration. Both inpatient and outpatient hospital setups provide convenient access to Pirfenidone, Nintedanib, and other therapies. Hospitals are also central to clinical trials and research, supporting widespread adoption. Regulatory compliance, reimbursement coverage, and treatment guideline inclusion further strengthen hospital demand. Pharmaceutical companies focus on hospital partnerships to ensure consistent supply and patient education. The segment includes tertiary care centers and academic hospitals, providing high exposure to new therapies. Ongoing awareness initiatives, training programs, and patient management systems reinforce dominance. Hospitals remain critical for effective disease management and therapy monitoring, maintaining leadership.

Home-care settings are expected to witness the fastest CAGR of 11.2% from 2026 to 2033, driven by increasing patient preference for self-administration of oral anti-fibrotic drugs, convenience, and remote healthcare adoption. Growth is supported by telemedicine, digital monitoring platforms, and patient support programs. Home-care adoption is rising in chronic disease management and elderly populations requiring long-term therapy. Pharmaceutical companies are providing pre-packaged, easy-to-use dosing systems for home use. Increasing awareness of disease progression and adherence programs ensures patient compliance. Specialty drugs with oral formulations enable patients to avoid frequent hospital visits. Rising prevalence of IPF and other fibrotic conditions accelerates demand in home-care. Government initiatives promoting home treatment and reducing hospital burden further support growth. Cost-effectiveness and patient comfort enhance segment adoption. Integration of mobile apps and reminder systems improves adherence and monitoring. Emerging markets are also contributing to faster adoption due to expanding home healthcare services. Overall, convenience, accessibility, and patient autonomy drive rapid growth in home-care settings.

Anti-Fibrotic Drug Therapies Market Regional Analysis

- North America dominated the anti-fibrotic drug therapies market with the largest revenue share of approximately 41.5% in 2025, supported by advanced healthcare infrastructure, strong R&D investments, and a high adoption rate of innovative therapeutics

- The market leads the market growth through extensive clinical trials, government-backed initiatives, and a robust network of hospitals and specialty clinics that facilitate rapid uptake of anti-fibrotic drugs

- The region benefits from well-established regulatory frameworks, increasing patient awareness, and the availability of insurance coverage, which collectively accelerate market expansion

U.S. Anti-Fibrotic Drug Therapies Market Insight

The U.S. anti-fibrotic drug therapies market captured the largest revenue share within North America in 2025, fueled by the increasing prevalence of fibrotic diseases such as idiopathic pulmonary fibrosis (IPF) and non-alcoholic steatohepatitis (NASH)-related fibrosis. The country’s advanced clinical research environment and availability of state-of-the-art healthcare facilities support early adoption of innovative therapeutics. Moreover, strong collaborations between biotechnology companies, research institutes, and hospitals are contributing to faster approvals and wider patient access to anti-fibrotic drugs.

Europe Anti-Fibrotic Drug Therapies Market Insight

The Europe anti-fibrotic drug therapies market is projected to expand at a substantial CAGR during the forecast period, primarily driven by the rising incidence of chronic fibrotic conditions and increasing healthcare expenditure. The presence of stringent regulatory standards ensures the development of safe and effective therapeutics. European countries such as Germany, France, and Italy are witnessing growing adoption of advanced anti-fibrotic drugs, supported by strong clinical research networks and reimbursement policies that facilitate patient access.

U.K. Anti-Fibrotic Drug Therapies Market Insight

The U.K. anti-fibrotic drug therapies market is expected to grow at a significant CAGR during the forecast period, driven by increasing patient awareness and rising demand for effective fibrosis management. National health programs and funding for clinical trials are supporting the introduction of innovative therapies. Furthermore, the U.K.’s well-developed healthcare infrastructure enables timely diagnosis and treatment of fibrotic diseases, contributing to market expansion.

Germany Anti-Fibrotic Drug Therapies Market Insight

The Germany anti-fibrotic drug therapies market is anticipated to expand at a considerable CAGR throughout the forecast period, supported by the country’s advanced healthcare system and emphasis on medical research. Germany’s strong pharmaceutical sector and focus on developing novel therapeutic options enhance the adoption of anti-fibrotic drugs in hospitals and specialized clinics. Patient awareness campaigns and government support further encourage early diagnosis and treatment.

Asia-Pacific Anti-Fibrotic Drug Therapies Market Insight

The Asia-Pacific anti-fibrotic drug therapies market is expected to be the fastest-growing region during the forecast period, with a projected CAGR of 9.6%, driven by increasing healthcare spending, improving access to advanced therapeutics, and growing patient awareness in countries such as China and India. Rapid urbanization, expanding healthcare infrastructure, and government initiatives promoting early disease management are contributing to higher adoption of anti-fibrotic therapies. Additionally, increasing local manufacturing and distribution networks are making advanced therapies more accessible to a wider population.

Japan Anti-Fibrotic Drug Therapies Market Insight

The Japan anti-fibrotic drug therapies market is gaining traction due to the country’s aging population, high healthcare standards, and strong focus on medical innovation. Rising incidence of age-related fibrotic conditions is driving demand for advanced therapeutics, while well-established clinical trial networks and healthcare delivery systems support faster adoption and accessibility of novel anti-fibrotic drugs.

China Anti-Fibrotic Drug Therapies Market Insight

The China anti-fibrotic drug therapies market accounted for the largest revenue share in Asia-Pacific in 2025, fueled by rising healthcare awareness, increasing prevalence of fibrotic diseases, and growing government support for early diagnosis and treatment. Expanding urban healthcare facilities, greater insurance coverage, and availability of locally produced innovative therapeutics are accelerating market adoption. The push for modern healthcare infrastructure and improved patient access is further propelling market growth in China.

Anti-Fibrotic Drug Therapies Market Share

The Anti-Fibrotic Drug Therapies industry is primarily led by well-established companies, including:

• Boehringer Ingelheim (Germany)

• Roche Holding AG (Switzerland)

• Bristol-Myers Squibb (U.S.)

• Gilead Sciences (U.S.)

• Johnson & Johnson (U.S.)

• Eli Lilly and Company (U.S.)

• Pfizer Inc. (U.S.)

• Novartis AG (Switzerland)

• AbbVie Inc. (U.S.)

• Shionogi & Co., Ltd. (Japan)

• Mitsubishi Tanabe Pharma Corporation (Japan)

• Galecto Biotech AB (Sweden)

• Kadmon Holdings, Inc. (U.S.)

• Promedior, Inc. (U.S.)

• Bellerophon Therapeutics (U.S.)

• Inventiva S.A. (France)

• Veracyte, Inc. (U.S.)

• MediciNova, Inc. (U.S.)

Latest Developments in Global Anti-Fibrotic Drug Therapies Market

- In May 2023, the Phase 3 ISABELA 1 and 2 clinical trials of ziritaxestat, a novel autotaxin inhibitor targeting idiopathic pulmonary fibrosis (IPF), were terminated early after failing to demonstrate significant clinical benefit in improving lung function, underscoring the challenges in developing new anti‑fibrotic drugs for IPF

- In March 2024, the first drug Rentosertib (ISM001‑055), an AI‑designed TNIK inhibitor developed using generative artificial intelligence for idiopathic pulmonary fibrosis, entered mid‑stage (Phase 2a) human clinical trials, representing a pioneering AI‑generated therapy targeting a novel biological pathway in fibrotic disease research

- In October 2024, Trevi Therapeutics provided updates on its clinical development program for Haduvio (oral nalbuphine ER), an investigational therapy aimed at treating chronic cough associated with idiopathic pulmonary fibrosis, reflecting continued innovation in symptom‑focused anti‑fibrotic treatment strategies

- In January 2025, Mediar Therapeutics announced a global licensing agreement with Eli Lilly & Company to advance MTX‑463, a first‑in‑class human IgG1 antibody designed to neutralize WISP1‑mediated fibrotic signaling, into Phase II clinical trials for idiopathic pulmonary fibrosis, marking a significant advancement in targeted anti‑fibrotic therapy development

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.