Global Anti Metabolite Drugs Market

Market Size in USD Billion

USD

6.37 Billion

USD

11.45 Billion

2025

2033

USD

6.37 Billion

USD

11.45 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.37 Billion | |

| USD 11.45 Billion | |

| % | |

|

Anti-Metabolite Drugs Market Overview

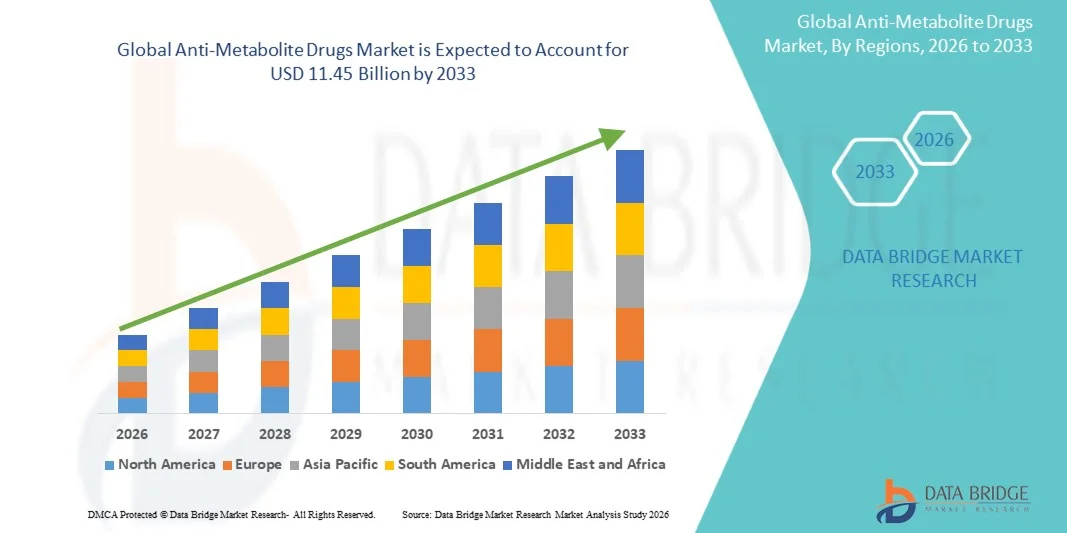

The Anti-Metabolite Drugs Market was valued at USD 6.37 billion in 2025 and is projected to reach USD 11.45 billion by 2033, growing at a CAGR of 7.60% from 2026 to 2033. Market growth is supported by rising prevalence of cancer worldwide, increasing adoption of chemotherapy regimens incorporating anti-metabolite agents, and expanding therapeutic applications across oncology, autoimmune diseases, and infectious conditions.

The efficacy of anti-metabolite drugs in disrupting DNA and RNA synthesis within rapidly dividing cancer cells, combined with their established role in first-line and combination chemotherapy protocols, continues to drive widespread clinical utilization. Ongoing advancements in drug formulation technologies, including novel delivery systems and prodrug approaches, are improving bioavailability, reducing toxicity profiles, and expanding patient eligibility for anti-metabolite therapy. In addition, growing healthcare infrastructure investments in emerging markets and increasing access to essential oncology medications are creating new opportunities for stakeholders across the forecast period.

Key Market Trends & Insights

- North America dominated the Anti-Metabolite Drugs Market with the largest revenue share of 38.7% in 2025, supported by high cancer incidence rates, advanced oncology treatment infrastructure, strong reimbursement frameworks, and the presence of leading pharmaceutical companies.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 9.45% from 2026 to 2033, driven by expanding healthcare infrastructure, rising cancer prevalence, increasing healthcare expenditure, and improving access to essential oncology medications.

- The Pyrimidine Analogues segment led the market with a 48.2% market share in 2025, reflecting the widespread utilization of agents such as 5-fluorouracil, capecitabine, and gemcitabine across multiple solid tumor indications including colorectal, breast, pancreatic, and non-small cell lung cancers.

- The Purine Analogues segment is anticipated to be the fastest-growing type category, driven by expanding applications in hematological malignancies, increasing adoption of fludarabine and cladribine in lymphoproliferative disorders, and ongoing clinical development of next-generation purine-based agents.

- The Cancer Therapeutics segment dominated the application category with a 72.5% market share in 2025, supported by the central role of anti-metabolite agents in standard chemotherapy regimens across solid tumors and hematological malignancies.

- The Hospital segment dominated the end-user category with a 65.8% market share in 2025, supported by access to comprehensive oncology services, multidisciplinary care teams, and specialized infusion infrastructure required for anti-metabolite drug administration.

- The Hospital Pharmacy segment dominated the distribution channel category with a 58.4% market share in 2025, driven by centralized procurement, specialized handling requirements for cytotoxic agents, and integrated medication management within inpatient oncology settings.

Market Size & Forecast

- Global Market Value (2025): USD 6.37 Billion

- Expected Market Value (2033): USD 11.45 Billion

- Forecast CAGR (2026–2033): 7.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Anti-Metabolite Drugs Market Segmentation

|

Attributes |

Anti-Metabolite Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Lilly USA, LLC (U.S.) · Pfizer Inc. (U.S.) · Teva Pharmaceutical Industries Ltd. (Israel) · Mylan N.V. (U.S.) · Fresenius Kabi AG (Germany) · Hikma Pharmaceuticals PLC (U.K.) · Sun Pharmaceutical Industries Ltd. (India) · Accord Healthcare Ltd. (U.K.) · Sagent Pharmaceuticals Inc. (U.S.) · Novartis AG (Switzerland) · F. Hoffmann-La Roche Ltd. (Switzerland) · Sanofi S.A. (France) |

|

Market Opportunities |

· Expansion of anti-metabolite drug accessibility into emerging markets with growing oncology treatment infrastructure and increasing cancer diagnosis rates · Development of novel drug delivery systems and prodrug formulations enabling improved bioavailability, reduced toxicity, and enhanced patient compliance |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Anti-Metabolite Drugs Market Trends

Trend: Advancements in Drug Delivery Systems and Combination Therapy Protocols

Clinical adoption of anti-metabolite drugs continues to evolve as pharmaceutical companies invest in advanced drug delivery technologies and combination therapy approaches. Novel formulations including liposomal encapsulation, nanoparticle-based delivery, and oral prodrug development are improving drug bioavailability, extending plasma half-life, and reducing systemic toxicity associated with conventional anti-metabolite administration. Integration of anti-metabolite agents with targeted therapies and immunotherapies is expanding treatment options and improving clinical outcomes across multiple cancer types.

For instance,

The development of oral capecitabine as a prodrug of 5-fluorouracil has significantly improved patient convenience and compliance compared to intravenous infusion regimens, enabling outpatient chemotherapy administration while maintaining therapeutic efficacy in colorectal and breast cancer treatment protocols.

In addition, research demonstrates that combination regimens incorporating anti-metabolites with immune checkpoint inhibitors are showing promising results in clinical trials, supporting broader adoption of synergistic treatment approaches across solid tumor and hematological malignancy indications. These advancements in drug delivery and combination protocols are expected to strengthen market growth and expand therapeutic applications throughout the forecast period.

Anti-Metabolite Drugs Market Dynamics

Key Market Driver: Rising Global Cancer Incidence and Expanding Chemotherapy Utilization

The growing global burden of cancer is a primary driver of market growth. Anti-metabolite drugs remain foundational components of standard chemotherapy regimens across multiple malignancies, including colorectal cancer, breast cancer, pancreatic cancer, acute leukemias, and non-Hodgkin lymphoma. The increasing prevalence of cancer due to aging populations, lifestyle factors, and improved diagnostic capabilities is expanding the patient population requiring anti-metabolite therapy.

For instance,

According to the World Health Organization, global cancer incidence is projected to increase significantly over the coming decades, with approximately 35 million new cancer cases expected annually by 2050, representing a substantial increase from current levels. Rising cancer diagnosis rates, particularly in emerging markets with improving healthcare access, are expected to strengthen demand for anti-metabolite chemotherapy agents globally.

Key Restraint/Challenge: Treatment-Related Toxicities and Adverse Effect Profiles

The significant toxicity profiles associated with anti-metabolite drugs, including myelosuppression, mucositis, hepatotoxicity, and gastrointestinal adverse effects, present challenges for patient tolerability and treatment adherence. Dose-limiting toxicities may require treatment interruption, dose reduction, or discontinuation, potentially compromising therapeutic outcomes. Managing adverse effects requires comprehensive supportive care infrastructure and specialized oncology expertise.

For instance,

Clinical studies demonstrate that 5-fluorouracil-based regimens are associated with significant rates of grade 3-4 adverse events including neutropenia, diarrhea, and hand-foot syndrome, requiring careful patient monitoring and supportive care interventions. Treatment-related toxicities may limit utilization in certain patient populations and constrain market expansion, particularly among elderly patients with comorbidities.

Key Market Opportunity: Expansion of Oncology Infrastructure in Emerging Markets

The development of comprehensive oncology treatment capabilities in emerging markets is creating significant opportunities for anti-metabolite drug adoption. Healthcare infrastructure investments in Asia-Pacific, Latin America, and the Middle East are expanding access to essential chemotherapy agents and improving cancer care delivery. Generic drug availability is improving affordability, enabling broader patient access to established anti-metabolite therapies in previously underserved markets.

For instance,

The global oncology drugs market is projected to experience substantial growth driven by increasing cancer prevalence and expanding treatment access in emerging economies. Healthcare modernization initiatives and essential medicines programs in countries including China, India, and Brazil are improving anti-metabolite drug availability and affordability. Expansion of oncology infrastructure in emerging markets represents a significant opportunity for market stakeholders throughout the forecast period.

Anti-Metabolite Drugs Market Scope

The anti-metabolite drugs market is segmented on the basis of type, application, demographic, dosage form, route of administration, end-users, and distribution channel.

By Type

On the basis of type, the Anti-Metabolite Drugs Market is segmented into folic acid analogues, pyrimidine analogues, and purine analogues. The Pyrimidine Analogues segment dominated the market with a 48.2% market share in 2025, reflecting the widespread utilization of agents including 5-fluorouracil, capecitabine, gemcitabine, and cytarabine across multiple solid tumor and hematological malignancy indications. Strong clinical evidence supporting efficacy in colorectal, breast, pancreatic, and non-small cell lung cancers drives high prescription volumes and segment leadership. The established role of pyrimidine analogues in first-line and adjuvant chemotherapy regimens contributes to dominant market positioning.

The Purine Analogues segment is expected to witness the fastest growth from 2026 to 2033, driven by expanding applications in hematological malignancies including chronic lymphocytic leukemia, hairy cell leukemia, and acute lymphoblastic leukemia. Increasing adoption of fludarabine, cladribine, and clofarabine in lymphoproliferative disorders and ongoing clinical development of next-generation purine-based agents support segment expansion. The Purine Analogues segment is anticipated to grow at a CAGR of 9.15% during the forecast period.

By Application

On the basis of application, the Anti-Metabolite Drugs Market is segmented into cancer therapeutics, antibiotics, and others. The Cancer Therapeutics segment dominated the market with a 72.5% market share in 2025, supported by the central role of anti-metabolite agents in standard chemotherapy regimens across solid tumors and hematological malignancies. The established efficacy of 5-fluorouracil, gemcitabine, methotrexate, and cytarabine in first-line, adjuvant, and palliative treatment protocols drives high utilization rates. Rising global cancer incidence and expanding access to oncology care contribute to segment leadership.

The Antibiotics segment is anticipated to be the fastest-growing application category in the Anti-Metabolite Drugs Market, registering a CAGR of 8.75% during the forecast period. Growth is driven by increasing research into the use of anti-metabolite agents as potential solutions in antimicrobial resistance management. Their role in disrupting bacterial metabolic pathways is gaining attention, particularly in combination antibiotic therapy approaches aimed at improving treatment efficacy. In addition, rising global concerns over drug-resistant infections and ongoing pharmaceutical innovation are expected to support the development and adoption of novel anti-metabolite-based antimicrobial strategies.

By Demographic

On the basis of demographic, the Anti-Metabolite Drugs Market is segmented into adult, geriatric, and others. The Adult segment dominated the market with a 52.4% market share in 2025, reflecting the high incidence of solid tumors and hematological malignancies requiring anti-metabolite therapy among adult populations. Standard chemotherapy protocols across colorectal, breast, pancreatic, and lung cancers drive substantial utilization in the 18-65 age demographic. Strong tolerability profiles and established dosing guidelines contribute to segment leadership.

The Geriatric segment is anticipated to be the fastest-growing demographic category in the Anti-Metabolite Drugs Market, registering a CAGR of 8.95% during the forecast period. Growth is primarily driven by the rapidly aging global population, which is leading to a higher prevalence of cancer and other chronic conditions among elderly individuals. Improved diagnostic rates, expanded access to oncology care, and advancements in treatment tolerance are further supporting adoption in this group. In addition, increasing focus on age-appropriate cancer therapies and supportive care is expected to drive sustained segment growth.

By Dosage Form

On the basis of dosage form, the Anti-Metabolite Drugs Market is segmented into injection, creams, tablets, and others. The Injection segment dominated the market with a 58.6% market share in 2025, reflecting the predominant utilization of intravenous anti-metabolite formulations in hospital-based oncology settings. Injectable formulations including 5-fluorouracil, gemcitabine, and cytarabine remain standard of care for multiple cancer indications requiring controlled infusion administration. Hospital-based infusion infrastructure and specialized handling requirements for cytotoxic agents support segment leadership.

The Tablets segment held a 32.8% market share in 2025, supported by the widespread utilization of oral anti-metabolite formulations including capecitabine and oral methotrexate. The convenience of oral administration enables outpatient treatment and improves patient compliance compared to intravenous regimens. The Tablets segment is anticipated to be the fastest-growing dosage form category at a CAGR of 9.25% during the forecast period, driven by patient preference for oral therapies and ongoing development of novel oral anti-metabolite formulations.

By Route of Administration

On the basis of route of administration, the Anti-Metabolite Drugs Market is segmented into oral, topical, intravenous push, intravenous infusion, and continuous infusion. The Intravenous Infusion segment dominated the market with a 38.5% market share in 2025, reflecting the standard utilization of controlled infusion administration for agents including gemcitabine and cytarabine in hospital-based oncology settings. Precise dose delivery and pharmacokinetic optimization through infusion protocols support segment leadership.

The Oral segment is anticipated to be the fastest-growing route of administration category in the Anti-Metabolite Drugs Market, registering a CAGR of 9.35% during the forecast period. Growth is primarily driven by strong patient preference for oral therapies due to their convenience, ease of administration, and reduced need for frequent hospital visits. The expanding development and approval of oral anti-metabolite drugs are further supporting adoption across various oncology indications. In addition, improved treatment adherence, enhanced quality of life, and the growing shift toward outpatient cancer care are expected to contribute significantly to segment growth.

By End-Users

On the basis of end-users, the Anti-Metabolite Drugs Market is segmented into clinic, hospital, and others. The Hospital segment dominated the market with a 65.8% market share in 2025, supported by access to comprehensive oncology services, multidisciplinary care teams, specialized infusion infrastructure, and comprehensive supportive care capabilities required for anti-metabolite drug administration. Hospitals serve as primary centers for complex chemotherapy regimens requiring inpatient monitoring, specialized handling of cytotoxic agents, and management of treatment-related adverse effects. High procedure volumes and integrated oncology programs contribute to segment leadership.

The Clinic segment is anticipated to be the fastest-growing end-user category in the Anti-Metabolite Drugs Market, registering a CAGR of 9.05% during the forecast period. Growth is being driven by healthcare system initiatives to transition suitable oncology treatments from inpatient hospitals to outpatient clinic settings, improving both cost efficiency and patient convenience. Clinics are increasingly equipped to administer anti-metabolite therapies, monitor treatment responses, and manage adverse effects through specialized oncology services. In addition, rising cancer prevalence, expanding outpatient infrastructure, and growing demand for accessible, high-quality cancer care are expected to further accelerate segment growth.

By Distribution Channel

On the basis of distribution channel, the Anti-Metabolite Drugs Market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the market with a 58.4% market share in 2025, driven by centralized procurement, specialized handling requirements for cytotoxic agents, and integrated medication management within inpatient oncology settings. Hospital pharmacies provide comprehensive compounding services, dose verification, and safe handling protocols essential for injectable anti-metabolite drug preparation and dispensing. High-volume oncology programs and specialized oncology pharmacy expertise contribute to segment leadership.

The Online Pharmacy segment is anticipated to be the fastest-growing distribution channel category at a CAGR of 10.25% during the forecast period. Digital pharmacy platforms are expanding access to oral anti-metabolite medications through convenient home delivery services, medication management tools, and enhanced patient support programs. Increasing adoption of digital healthcare services and expanding regulatory frameworks for online pharmacy operations support segment growth.

Anti-Metabolite Drugs Market Regional Analysis

North America dominated the anti-metabolite drugs market with a revenue share of 38.7% in 2025, supported by high cancer incidence rates, advanced oncology treatment infrastructure, strong reimbursement frameworks, and the presence of leading pharmaceutical companies. Favorable regulatory pathways, robust clinical research capabilities, and extensive oncology clinical trial activity contribute to regional market leadership.

U.S. Anti-Metabolite Drugs Market Insight

The U.S. anti-metabolite drugs market held a dominant share of 78.5% within North America in 2025, benefiting from the highest cancer treatment expenditure globally, comprehensive insurance coverage for oncology therapies, and extensive oncology treatment infrastructure. Academic medical centers, comprehensive cancer centers, and community oncology practices provide widespread access to anti-metabolite chemotherapy across the country. Strong clinical trial activity and ongoing pharmaceutical research support continued market leadership.

Europe Anti-Metabolite Drugs Market Insight

The Europe anti-metabolite drugs market remains a major contributor, with strong oncology treatment programs across Germany, France, the U.K., Italy, and Spain. Comprehensive cancer care networks, established chemotherapy protocols, and robust generic drug availability ensure widespread patient access to anti-metabolite therapies. Cross-disciplinary guidelines and quality assurance programs standardize oncology care delivery across public and private healthcare systems.

U.K. Anti-Metabolite Drugs Market Insight

The U.K. anti-metabolite drugs market held a dominant share of 18.2% within Europe in 2025, characterized by comprehensive NHS cancer treatment programs and expanding access to essential oncology medications. Investment in oncology infrastructure and chemotherapy services improves patient access and reduces treatment waiting times across the country.

Germany Anti-Metabolite Drugs Market Insight

Germany's robust healthcare infrastructure and advanced oncology capabilities support comprehensive chemotherapy programs utilizing anti-metabolite agents. Strong clinical research networks and favorable reimbursement frameworks contribute to high treatment volumes and continued market growth.

Asia-Pacific Anti-Metabolite Drugs Market Insight

The Asia-Pacific anti-metabolite drugs market is poised for rapid growth with a CAGR of 9.45% during the forecast period, driven by expanding healthcare infrastructure, rising cancer prevalence, increasing healthcare expenditure, and improving access to essential oncology medications. Healthcare modernization initiatives across China, Japan, India, and South Korea are strengthening oncology treatment capabilities and expanding patient access to anti-metabolite chemotherapy.

Japan Anti-Metabolite Drugs Market Insight

The Japan anti-metabolite drugs market held a dominant share of 24.8% within Asia-Pacific in 2025, benefiting from advanced healthcare infrastructure, strong oncology expertise, and comprehensive reimbursement for cancer treatment. High cancer incidence among aging populations and established chemotherapy protocols drive substantial anti-metabolite drug utilization.

China Anti-Metabolite Drugs Market Insight

The China anti-metabolite drugs market is experiencing rapid growth at a CAGR of 10.85% during the forecast period, driven by healthcare modernization initiatives, expanding oncology treatment capabilities, and increasing access to essential cancer medications. Government programs improving drug affordability and availability are supporting market expansion across urban and rural healthcare systems.

Anti-Metabolite Drugs Market Share

The anti-metabolite drugs industry is primarily led by well-established companies, including:

- Lilly USA, LLC (U.S.)

- Pfizer Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Mylan N.V. (U.S.)

- Fresenius Kabi AG (Germany)

- Hikma Pharmaceuticals PLC (U.K.)

- Sun Pharmaceutical Industries Ltd. (India)

- Accord Healthcare Ltd. (U.K.)

- Sagent Pharmaceuticals Inc. (U.S.)

- Novartis AG (Switzerland)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Sanofi S.A. (France)

Latest Developments in Anti-Metabolite Drugs Market

- In March 2026, Eli Lilly and Company announced the completion of its expanded manufacturing facility dedicated to oncology drug production, including anti-metabolite agents. The investment supports increased production capacity and supply chain resilience for essential chemotherapy medications globally.

- In January 2026, Fresenius Kabi AG received FDA approval for its generic gemcitabine injection product, expanding affordable access to this essential anti-metabolite agent for cancer patients in the United States. The approval reinforces the company's commitment to oncology generic drug development.

- In November 2025, Teva Pharmaceutical Industries Ltd. announced the launch of its generic capecitabine tablets in multiple European markets, providing cost-effective access to oral anti-metabolite therapy for colorectal and breast cancer patients across the region.

- In September 2025, Sun Pharmaceutical Industries Ltd. expanded its oncology portfolio with the introduction of generic pemetrexed injection in emerging markets across Asia-Pacific and Latin America, improving access to essential anti-metabolite therapy for non-small cell lung cancer patients.

- In July 2025, Pfizer Inc. announced positive results from a Phase III clinical trial evaluating a novel anti-metabolite combination regimen in metastatic pancreatic cancer, demonstrating improved progression-free survival compared to standard gemcitabine monotherapy.

- In April 2025, Hikma Pharmaceuticals PLC received FDA approval for its generic cytarabine liposomal injection, expanding therapeutic options for patients with lymphomatous meningitis requiring intrathecal anti-metabolite therapy.

- In February 2025, Novartis AG announced strategic investments in oncology manufacturing capabilities, including expanded production of anti-metabolite active pharmaceutical ingredients to support global supply chain stability.

- In December 2024, Accord Healthcare Ltd. launched generic methotrexate injection products in multiple formulations across European markets, improving affordable access to essential anti-metabolite therapy for oncology and autoimmune disease patients.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.