Global Anti Scratch Film Market

Market Size in USD Billion

USD

9.20 Billion

USD

14.44 Billion

2025

2033

USD

9.20 Billion

USD

14.44 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.20 Billion | |

| USD 14.44 Billion | |

| % | |

|

Anti Scratch Film Market Overview

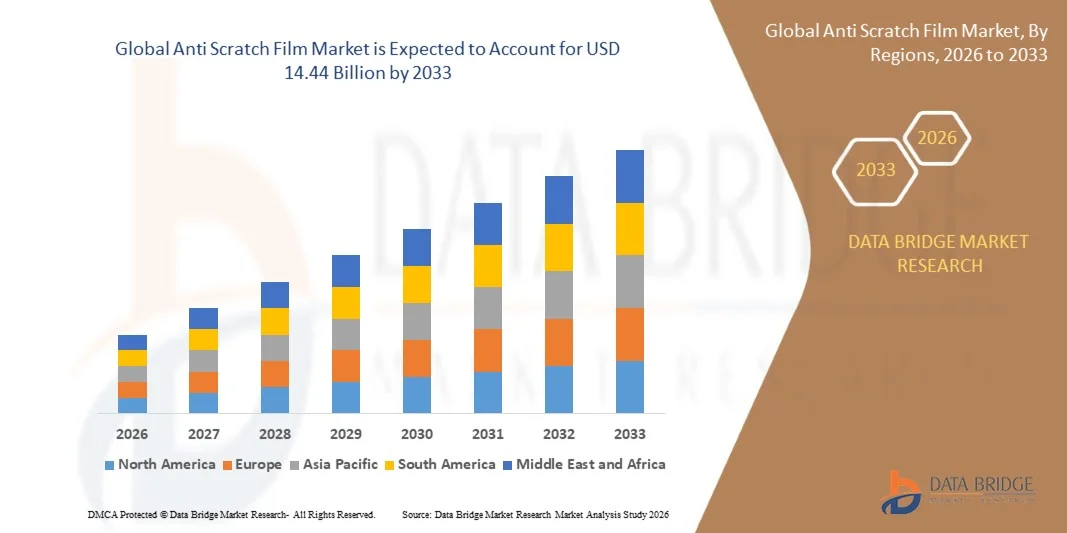

The Anti Scratch Film Market was valued at USD 9.2 Billion in 2025 and is projected to reach USD 14.44 Billion by 2033, growing at a CAGR of 5.8% from 2026 to 2033. The market is experiencing consistent growth driven by increasing demand for surface protection solutions across automotive, electronics, construction, and industrial applications. Rising adoption of premium consumer electronics, growing vehicle production, and expanding use of scratch-resistant materials in architectural surfaces are supporting market expansion. Advancements in coating technologies, self-healing films, and high-performance protective materials are further contributing to market growth across developed and emerging economies.

The growing focus on enhancing product durability, maintaining aesthetic appeal, and reducing maintenance costs is encouraging manufacturers to adopt advanced anti scratch film solutions across a wide range of applications. Anti scratch films are increasingly used to protect displays, vehicle surfaces, glass panels, and industrial equipment from abrasion, wear, and surface damage while extending product lifespan. In addition, rising consumer preference for premium-quality products, coupled with continuous innovation in transparent and high-performance protective films, is accelerating adoption and supporting long-term market development.

Key Market Trends & Insights

- Asia-Pacific dominated the Anti Scratch Film Market with the largest revenue share of 46.40% in 2025, supported by strong manufacturing activity, expanding consumer electronics production, and rising automotive industry demand across major economies

- The stretch film segment led the market with a 61.4% share in 2025, driven by its extensive use in protecting delicate surfaces during transportation, storage, and manufacturing processes

- North America is expected to be the fastest-growing region at a CAGR of 5.9% from 2026 to 2033, fueled by increasing demand for premium consumer electronics, advanced automotive technologies, and durable surface protection solutions

- Glass is the fastest-growing application type, projected to register a CAGR of 9.4% from 2026 to 2033, supported by increasing installation of glass surfaces in commercial buildings, residential projects, and consumer electronics

- The 20 to 25 Micron segment dominated the thickness category with a 38.2% revenue share in 2025, led by its optimal balance between flexibility, durability, and cost-effectiveness

- Polyester accounted for 34.8% of the market in 2025, preferred by its superior scratch resistance, optical clarity, and durability across a wide range of industrial and consumer applications

- The more than 30 Micron segment is the fastest-growing thickness category, with a CAGR of 9.1% from 2026 to 2033, driven by increasing demand for heavy-duty surface protection in high-impact environments

Market Size & Forecast

- Global Market Value (2025): USD 9.2 Billion

- Expected Market Value (2033): USD 14.44 Billion

- Forecast CAGR (2026–2033): 5.8%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Report Scope and Anti Scratch Film Market Segmentation

|

Attributes |

Anti Scratch Film Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· 3M (U.S.) · TEKRA, LLC. (U.S.) · POLIFILM (Germany) · Synpack (India) · Specialty Polyfilms India Pvt. Ltd. (India) · tesa Tapes (India) Private Limited (India) · Intertape Polymer Group (Canada) · LINTEC Corporation (Japan) · Nitto Denko Corporation (Japan) · DuPont (U.S.) · Scapa Group Ltd (U.K.) · Saint-Gobain Performance Plastics (France) · ECHOtape (Canada) · ECOPLAST LTD. (India) · Avery Dennison Corporation (U.S.) · Chargeurs (France) · Tredegar Corporation (U.S.) · Polifilm GmbH (Germany) · Bischof + Klein SE & Co. KG (Germany) · Aristo Flexi Pack (India) · Dute Industries Group (China) |

|

Market Opportunities |

· Growth of Self-Healing Film Technologies · Rising Adoption in Electric Vehicles · Expanding Use in Architectural Glass Applications |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Anti Scratch Film Market Trends

Trend: Rising Use of Anti Scratch Films in Consumer Electronics

The growing penetration of smartphones, tablets, laptops, wearable devices, and premium display technologies is significantly increasing demand for anti scratch films across the consumer electronics industry. Manufacturers are increasingly integrating advanced protective films to improve device durability, maintain display clarity, and enhance user experience. The trend is further supported by rising consumer preference for premium electronic products with extended product life and improved surface protection. Continuous advancements in thin-film coatings, self-healing technologies, and optical-grade protective materials are accelerating product adoption across global electronics markets.

Companies such as Apple and Samsung continue to incorporate advanced scratch-resistant materials and protective surface technologies in their flagship devices, while Corning’s Gorilla Glass solutions have become a benchmark for enhanced scratch protection across smartphones and consumer electronics, highlighting the growing emphasis on surface durability.

Anti Scratch Film Market Dynamics

Key Market Driver: Growing Demand for Surface Protection in Automotive Applications

The increasing production of passenger vehicles, luxury automobiles, and electric vehicles is a major factor driving demand for anti scratch films globally. Automotive manufacturers are increasingly utilizing protective films on exterior painted surfaces, infotainment displays, interior trims, door panels, and high-contact components to preserve appearance and reduce maintenance costs. Rising consumer spending on vehicle protection and customization solutions is further supporting market expansion. Growing adoption of paint protection films (PPF) and advanced surface protection technologies is creating sustained demand across the automotive sector.

Major industry participants such as 3M and Avery Dennison have expanded their paint protection film portfolios to address increasing demand for durable and scratch-resistant automotive surface solutions, reflecting the growing importance of protective films in modern vehicle manufacturing and aftermarket applications.

Key Restraint/Challenge: Fluctuating Raw Material Costs

A major challenge for the Anti Scratch Film market is the volatility in prices of key raw materials such as polyester, polypropylene, polyethylene, specialty resins, and coating chemicals. Changes in crude oil prices, supply chain disruptions, and fluctuations in petrochemical feedstock costs can significantly impact manufacturing expenses and profit margins. Manufacturers often face challenges in maintaining competitive pricing while investing in advanced coating technologies and product innovation. In addition, rising energy and transportation costs further increase production expenditures across the value chain.

For instance, fluctuations in global petrochemical prices during recent years have affected film manufacturers worldwide, prompting companies such as DuPont and POLIFILM to focus on operational efficiency and material optimization strategies to manage cost pressures while maintaining product quality.

Key Market Opportunity: Expanding Use in Architectural Glass Applications

The increasing adoption of architectural glass in commercial buildings, residential projects, airports, shopping centers, and smart infrastructure is creating significant growth opportunities for the Anti Scratch Film market. Protective films are increasingly being used to preserve glass clarity, reduce surface damage, and improve the lifespan of high-value architectural installations. Growing investments in modern infrastructure development and premium building materials are further supporting demand for advanced protective film solutions. Rising deployment of smart glass and decorative glass technologies is also expanding application opportunities for anti scratch films.

Companies such as Saint-Gobain and tesa are actively developing advanced surface protection solutions for construction and architectural applications, supporting the growing use of protective films in modern building projects and high-performance glass installations worldwide.

Anti Scratch Film Market Scope

The anti scratch film market is segmented on the basis of material, product type, thickness, application, and end-use.

- By Material

On the basis of material, the Anti Scratch Film Market is segmented into Polyethylene, Linear Low Density Polyethylene (LLDPE), Low Density Polyethylene (LDPE), High Density Polyethylene (HDPE), Polyester, Polypropylene, Biaxial Oriented Polypropylene (BOPP), Cast Polypropylene (CPP), and Others. The Polyester segment dominated the market with the largest share of 34.8% in 2025, driven by its superior scratch resistance, optical clarity, and durability across a wide range of industrial and consumer applications. Polyester-based films provide excellent surface protection while maintaining transparency, making them highly suitable for automotive, electronics, and architectural surfaces. Manufacturers increasingly prefer polyester films due to their high tensile strength and long-term performance under demanding operating conditions. Growing demand for premium protective solutions in display panels and vehicle components continues to support segment growth. Continuous product innovation and enhanced coating technologies further reinforce its leading position.

The Biaxial Oriented Polypropylene (BOPP) segment is projected to register the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by increasing demand for lightweight, cost-effective, and high-performance protective films. BOPP films offer excellent surface smoothness, moisture resistance, and mechanical strength, making them attractive for electronics and packaging-related applications. Advancements in film orientation and coating technologies are improving scratch resistance while maintaining affordability. Rising adoption in consumer electronics and decorative surface protection applications is further accelerating demand. Expanding industrial production and growing preference for recyclable film materials continue to support rapid segment expansion.

- By Product Type

On the basis of product type, the Anti Scratch Film Market is segmented into Shrink Film and Stretch Film. The Stretch Film segment dominated the market with a share of 61.4% in 2025, supported by its extensive use in protecting delicate surfaces during transportation, storage, and manufacturing processes. Stretch films provide superior conformability and surface coverage, enabling effective protection against scratches, abrasions, and dust. Industries increasingly utilize stretch films due to their flexibility and ability to secure products of varying shapes and sizes. Growing logistics activities and rising demand for damage-free product handling are strengthening adoption across multiple sectors. The segment also benefits from ongoing improvements in film strength and durability.

The Shrink Film segment is projected to register the fastest growth at a CAGR of 8.3% from 2026 to 2033, driven by increasing demand for tamper-resistant and tightly fitted protective packaging solutions. Shrink films offer enhanced product appearance and secure coverage, making them suitable for consumer goods and industrial components. Advancements in heat-shrink technologies are improving film performance while reducing material consumption. Rising demand for premium packaging and protective surface applications is creating significant growth opportunities. Expanding manufacturing activities across emerging economies are further supporting segment development.

- By Thickness

On the basis of thickness, the Anti Scratch Film Market is segmented into Less than 20 Micron, 20 to 25 Micron, 26 to 30 Micron, and More than 30 Micron. The 20 to 25 Micron segment dominated the market with the largest share of 38.2% in 2025, driven by its optimal balance between flexibility, durability, and cost-effectiveness. Films within this thickness range provide adequate protection against scratches while maintaining transparency and ease of application. Manufacturers widely utilize these films across automotive, electronics, and construction applications due to their versatile performance characteristics. Growing demand for reliable yet economical protective solutions continues to strengthen segment adoption. Consistent usage across both industrial and consumer applications further supports market leadership.

The More than 30 Micron segment is projected to register the fastest growth at a CAGR of 9.1% from 2026 to 2033, driven by increasing demand for heavy-duty surface protection in high-impact environments. Thicker films provide enhanced resistance against abrasion, mechanical damage, and harsh operating conditions. Industries such as automotive, construction, and industrial equipment manufacturing are increasingly adopting thicker protective films to extend product lifespan. Continuous improvements in film durability and coating technologies are supporting wider deployment. Rising investments in premium protection solutions are expected to accelerate segment growth throughout the forecast period.

- By Application

On the basis of application, the Anti Scratch Film Market is segmented into Glass, Panels, Frames, Handles, Doors, Vehicle, and Flooring. The Vehicle segment dominated the market with the largest share of 32.9% in 2025, driven by growing demand for surface protection across automotive interiors and exteriors. Anti scratch films help preserve vehicle aesthetics by protecting painted surfaces, displays, trims, and high-contact components from daily wear and tear. Increasing production of passenger and luxury vehicles is contributing significantly to segment demand. Automotive manufacturers are also focusing on enhancing product durability and customer satisfaction through advanced protective solutions. Rising consumer preference for maintaining vehicle appearance further reinforces market dominance.

The Glass segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by increasing installation of glass surfaces in commercial buildings, residential projects, and consumer electronics. Anti scratch films improve durability and visual quality while protecting glass against minor abrasions and surface damage. Growing adoption of large display screens and smart glass technologies is creating new growth opportunities. Advancements in transparent protective coatings are enhancing film performance without affecting visibility. Expanding infrastructure development and modernization projects continue to support strong segment expansion.

- By End-Use

On the basis of end-use, the Anti Scratch Film Market is segmented into Food and Beverages, Automotive, Electric and Electronics, Pharmaceutical and Health Care, Cosmetics and Personal Care, and Others. The Electric and Electronics segment dominated the market with a share of 36.7% in 2025, supported by increasing demand for protective solutions for displays, touchscreens, panels, and electronic components. Anti scratch films play a critical role in maintaining product appearance and functionality while extending device lifespan. Growing production of smartphones, tablets, laptops, and consumer electronics is significantly driving demand. Manufacturers are increasingly integrating advanced protective films to enhance product quality and user experience. Continuous innovation in display technologies further strengthens segment leadership.

The Automotive segment is projected to register the fastest growth at a CAGR of 9.8% from 2026 to 2033, driven by rising vehicle production and increasing adoption of advanced surface protection technologies. Automotive manufacturers are focusing on improving durability and preserving vehicle aesthetics throughout the product lifecycle. Growing demand for premium and electric vehicles is accelerating the use of anti scratch films across both interior and exterior components. Technological advancements in self-healing and high-performance protective films are supporting wider adoption. Increasing consumer awareness regarding vehicle maintenance and protection is expected to fuel sustained growth during the forecast period.

Anti Scratch Film Market Regional Analysis

Asia-Pacific dominated the anti scratch film market and accounted for the largest revenue share of 46.40% in 2025, supported by strong manufacturing activity, expanding consumer electronics production, and rising automotive industry demand across major economies. The region benefits from extensive industrialization, cost-effective production capabilities, and growing investments in advanced protective film technologies. Increasing demand for scratch-resistant surfaces in smartphones, displays, vehicles, and construction materials is accelerating market expansion. Rapid urbanization and rising adoption of premium consumer products are further supporting regional growth.

China Anti Scratch Film Market Insight

China held the largest share in the Asia-Pacific Anti Scratch Film market in 2025, supported by its dominant position in electronics manufacturing, automotive production, and industrial processing activities. The country has a well-established supply chain for specialty films and protective coating materials that enables large-scale production and distribution. Strong demand from smartphone manufacturers, display panel producers, and automotive OEMs is further strengthening market growth. In addition, increasing exports of electronic devices and industrial components are reinforcing China's leadership in the regional market.

India Anti Scratch Film Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by expanding electronics manufacturing, rising vehicle production, and increasing infrastructure development activities. Growing demand for protective films across consumer electronics, architectural glass, and automotive applications is significantly supporting market expansion. The country is benefiting from rising investments in domestic manufacturing and favorable government initiatives promoting industrial growth. In addition, increasing consumer preference for durable and aesthetically appealing products is accelerating long-term market development.

Europe Anti Scratch Film Market Insight

The Europe Anti Scratch Film market is expanding steadily, supported by increasing demand for advanced surface protection solutions across automotive, electronics, and construction industries. Manufacturers are increasingly adopting anti scratch films to enhance product durability, improve aesthetics, and reduce maintenance requirements. Strong focus on premium materials, technological innovation, and sustainable manufacturing practices is contributing to market growth. In addition, rising adoption of high-performance protective films in luxury vehicles and architectural applications is supporting regional expansion.

Germany Anti Scratch Film Market Insight

Germany accounted for the largest share in the Europe Anti Scratch Film market in 2025, driven by its strong automotive manufacturing sector and extensive use of advanced materials in industrial applications. The country has a well-developed production ecosystem that supports continuous innovation in protective film technologies. Rising demand for scratch-resistant coatings and films in premium vehicles, electronic devices, and industrial equipment is further strengthening market growth. In addition, increasing investments in advanced manufacturing and surface protection technologies are reinforcing Germany’s leading position.

U.K. Anti Scratch Film Market Insight

The U.K. market is supported by growing demand for protective films across consumer electronics, automotive components, and commercial construction applications. Increasing focus on maintaining product appearance and extending asset lifespan is driving adoption of anti scratch solutions across various industries. The country is also witnessing rising utilization of protective films in smart devices, display panels, and architectural glass installations. In addition, growing investments in modern infrastructure projects and premium building materials are supporting market expansion.

North America Anti Scratch Film Market Insight

North America is projected to grow at the fastest CAGR of 5.9% from 2026 to 2033, driven by increasing demand for premium consumer electronics, advanced automotive technologies, and durable surface protection solutions. Rising awareness regarding product longevity and maintenance reduction is significantly supporting market expansion across the region. Strong adoption of anti scratch films in display screens, automotive interiors, and commercial infrastructure projects is further accelerating demand. In addition, continuous technological advancements in self-healing and high-performance films are boosting regional market growth.

U.S. Anti Scratch Film Market Insight

The U.S. accounted for the largest share in the North America Anti Scratch Film market in 2025, supported by strong demand from automotive, electronics, aerospace, and construction industries. The country benefits from extensive adoption of advanced protective materials across consumer and industrial applications. Growing utilization of anti scratch films in smartphones, tablets, vehicle surfaces, and architectural installations is further strengthening market growth. In addition, increasing investments in innovative coating technologies and premium product development are reinforcing the U.S. leadership position in the regional market.

Anti Scratch Film Market Share

The anti scratch film industry is primarily led by well-established companies, including:

- 3M (U.S.)

- TEKRA, LLC. (U.S.)

- POLIFILM (Germany)

- Synpack (India)

- Specialty Polyfilms India Pvt. Ltd. (India)

- tesa Tapes (India) Private Limited (India)

- Intertape Polymer Group (Canada)

- LINTEC Corporation (Japan)

- Nitto Denko Corporation (Japan)

- DuPont (U.S.)

- Scapa Group Ltd (U.K.)

- Saint-Gobain Performance Plastics (France)

- ECHOtape (Canada)

- ECOPLAST LTD. (India)

- Avery Dennison Corporation (U.S.)

- Chargeurs (France)

- Tredegar Corporation (U.S.)

- Polifilm GmbH (Germany)

- Bischof + Klein SE & Co. KG (Germany)

- Aristo Flexi Pack (India)

- Dute Industries Group (China)

Latest Developments in Anti Scratch Film Market

- In May 2026, ORAFOL Group acquired Maxpro Manufacturing LLC, a U.S.-based producer of protective and window films, to strengthen its presence in the North American market and expand its functional film portfolio. The acquisition enhances ORAFOL’s manufacturing capacity, technological expertise, and distribution network for protective surface solutions. It is expected to support the growing demand for anti-scratch films across automotive, architectural, and industrial applications while improving the company’s ability to deliver advanced protective film products to a broader customer base

- In September 2025, Inozetek launched its next-generation paint protection film portfolio, including InoClear, InoClear+, InoMatte, and InoColor, aimed at providing superior scratch resistance, durability, and aesthetic enhancement for vehicle surfaces. The launch expands the company's product offerings in the premium protection segment and addresses increasing consumer demand for long-lasting surface protection solutions. The new films are expected to strengthen market competition and drive innovation in advanced anti-scratch film technologies

- In September 2025, ORAFOL Group completed the acquisition of South Korea-based Reflomax Co., Ltd. to enhance its specialty film technology capabilities and strengthen its footprint in the Asia-Pacific region. The acquisition provides access to advanced manufacturing technologies and specialized film solutions that can be utilized in protective and anti-scratch film applications. This strategic move supports the company’s expansion into high-growth markets and reinforces its position in the global protective films industry

- In June 2025, Covestro introduced new Makrofol® film solutions for automotive head-up display applications featuring enhanced optical clarity, UV resistance, durability, and scratch-resistant performance. These advanced films are designed to meet the growing requirements of modern vehicle display systems while ensuring long-term surface protection. The development supports increasing adoption of premium interior display technologies and highlights the rising importance of high-performance anti-scratch materials in the automotive sector

- In October 2024, ORAFOL Group acquired a stake in Belgian specialty film manufacturer Group M.A.M. to gain access to advanced sputtering and coating technologies used in high-performance film production. The investment strengthens the company’s research and development capabilities and expands opportunities for creating innovative protective film solutions with enhanced scratch resistance and durability. The partnership is expected to accelerate technological advancements and support growing demand for premium surface protection products across multiple industries

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Anti Scratch Film Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Anti Scratch Film Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Anti Scratch Film Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.