Global Anti Uav Defence System Market

Market Size in USD Billion

USD

2.94 Billion

USD

21.07 Billion

2024

2032

USD

2.94 Billion

USD

21.07 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.94 Billion | |

| USD 21.07 Billion | |

| % | |

|

Anti Unmanned Aerial Vehicle (UAV) Defence System Market Size

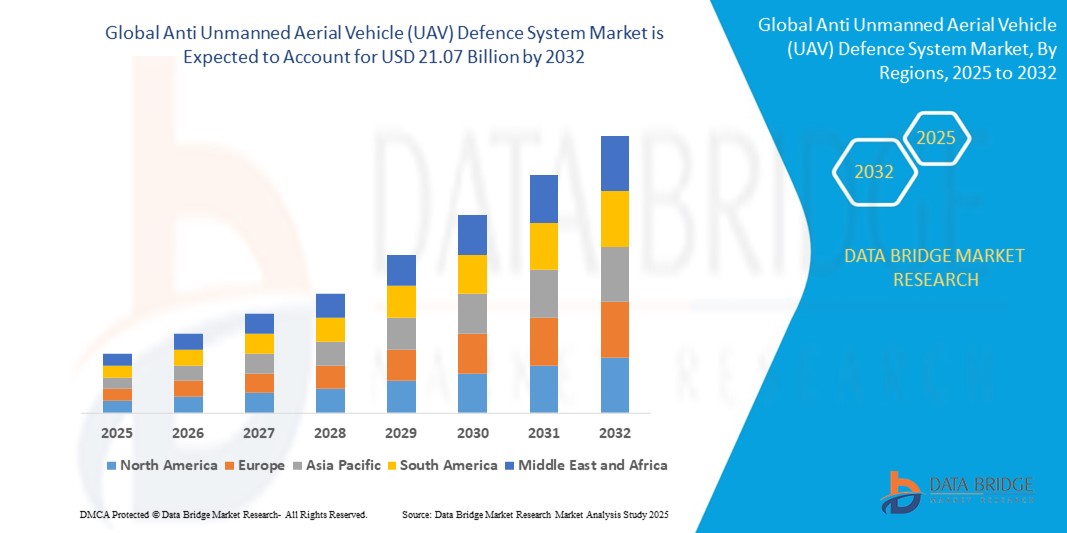

- The global anti unmanned aerial vehicle (UAV) defence system market size was valued at USD 2.94 billion in 2024 and is expected to reach USD 21.07 billion by 2032, at a CAGR of 27.9% during the forecast period

- The Market growth is primarily driven by the increasing proliferation of drones for both commercial and malicious purposes, raising security concerns across military, homeland security, and critical infrastructure sectors

- Rising government investments in advanced counter-UAV technologies and growing awareness of drone-related threats, such as espionage, smuggling, and terrorist activities, are further propelling market demand

Anti Unmanned Aerial Vehicle (UAV) Defence System Market Analysis

- The anti-UAV defence system market is experiencing robust growth due to the escalating use of drones in unauthorized and hostile activities, necessitating advanced countermeasures to ensure safety and security

- The demand for portable anti-drone solutions is increasing, particularly in law enforcement and civilian security applications, while vehicle-mounted systems are gaining traction for border security and military operations

- North America dominates the anti-UAV defence system market with the largest revenue share of 36.1% in 2024, driven by significant investments in counter-UAV technologies by the U.S. Department of Defense and a strong presence of key industry players

- Europe is projected to be the fastest-growing region during the forecast period, fueled by increasing defense budgets, growing adoption of advanced technologies, and rising concerns over drone-related security threats in countries such as Germany, France, and the U.K.

- The vehicle-mounted type segment held the largest market revenue share of 62.3% in 2024, driven by its widespread deployment in military and homeland security applications for securing borders, critical infrastructure, and sensitive locations

Report Scope and Anti Unmanned Aerial Vehicle (UAV) Defence System Market Segmentation

|

Attributes |

Anti Unmanned Aerial Vehicle (UAV) Defence System Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Anti Unmanned Aerial Vehicle (UAV) Defence System Market Trends

“Rising Adoption of Laser-Based Anti-UAV Systems”

- Laser-based anti-UAV systems are gaining traction due to their precision and ability to neutralize drones without physical projectiles, minimizing collateral damage

- These systems offer rapid response times and are effective against small, agile drones, making them ideal for protecting critical infrastructure and military installations

- In regions with high security concerns, such as North America and the Middle East, laser systems are increasingly deployed for their scalability and cost-effectiveness over time

- Defense contractors, such as Raytheon and Lockheed Martin, are investing in laser technology to enhance counter-UAV capabilities for military applications

- For instance, the U.S. Department of Defense has integrated laser-based systems such as the High Energy Laser Weapon System (HELWS) for UAV defense

- Governments and security agencies are offering contracts to include laser-based anti-UAV systems in homeland security operations, boosting market demand

Anti Unmanned Aerial Vehicle (UAV) Defence System Market Dynamics

Driver

“Increasing Threat of Unauthorized Drone Activities”

- Growing use of drones for illicit purposes, including espionage, smuggling, and potential terrorist attacks, is driving demand for robust anti-UAV defense systems

- These systems detect and neutralize unauthorized drones, protecting sensitive areas such as military bases, critical infrastructure, and public event

- In regions such as North America, where defense spending is high, and Europe, where security threats are rising, investments in anti-UAV technologies are accelerating

- For instance, the U.S. Department of Homeland Security has procured systems such as DroneSentry-X for on-the-move counter-UAV capabilities

- The rise of commercial drones, with over 1.7 million registered in the U.S. alone, has heightened the need for advanced detection and disruption systems to ensure airspace safety

Restraint/Challenge

“High Costs and Technological Limitations”

- he high cost of research, development, and deployment of advanced anti-UAV systems, particularly laser and electronic technologies, limits market accessibility for smaller organizations

- Laser-based systems, while effective, require significant investment in infrastructure and maintenance, posing challenges for widespread adoption

- Detection accuracy and range limitations, especially against low-observable or highly maneuverable drones, hinder system performance in complex environments

- Environmental factors, such as weather and terrain, can reduce the effectiveness of detection and disruption systems, impacting operational reliability

- Regulatory complexities surrounding the use of counter-UAV technologies, such as jamming, vary across countries, creating challenges for manufacturers and end-users

Anti Unmanned Aerial Vehicle (UAV) Defence System Market Scope

The market is segmented on the basis of product type, application, technology, type, and end user.

- By Product Type

On the basis of product type, the market is segmented into portable type and vehicle-mounted type. The vehicle-mounted type segment held the largest market revenue share of 62.3% in 2024, driven by its widespread deployment in military and homeland security applications for securing borders, critical infrastructure, and sensitive locations. Vehicle-mounted systems offer mobility, scalability, and robust detection and neutralization capabilities, making them ideal for large-scale operations.

The portable type segment is expected to witness the fastest growth rate of 28.5% from 2025 to 2032, fueled by increasing demand from law enforcement and civilian security applications. Portable anti-drone solutions provide flexibility and ease of deployment in dynamic environments such as public events, airports, and temporary security setups.

- By Application

On the basis of application, the market is segmented into civil and commercial and military. The military segment dominated the market with a revenue share of 68.7% in 2024, driven by the critical need to counter unauthorized or hostile drone activities in defense operations. Military applications leverage anti-UAV systems to protect bases, personnel, and strategic assets from drone-based threats, including surveillance, espionage, and attacks.

The civil and commercial segment is anticipated to experience the fastest growth rate from 2025 to 2032, propelled by the rising use of drones for commercial purposes such as aerial photography, delivery, and surveying. This has increased the need for anti-UAV systems to ensure safety at airports, stadiums, and critical infrastructure, addressing concerns over unauthorized drone intrusions.

- By Technology

On the basis of technology, the market is segmented into traditional kinetic systems, electronic, and laser systems. The electronic systems segment held the largest market revenue share of 55.8% in 2024, owing to their effectiveness in detecting and disrupting drones through radio frequency (RF) jamming and signal interference. These systems are widely adopted due to their non-destructive nature and ability to neutralize threats without collateral damage.

The laser system segment is projected to witness significant growth from 2025 to 2032, driven by advancements in directed energy weapons (DEWs) that offer precise targeting and minimal environmental impact. Laser systems are increasingly favored for their ability to neutralize drones at long ranges and in complex scenarios, particularly in military and homeland security applications.

- By Type

On the basis of type, the market is segmented into detection systems and detection and disruption systems. The detection and disruption systems segment accounted for the largest market revenue share of 70.4% in 2024, as these systems provide comprehensive solutions by combining real-time detection with active countermeasures such as jamming or neutralization. Their ability to address multi-drone threats and swarming scenarios drives their dominance.

The detection systems segment is expected to grow steadily from 2025 to 2032, supported by the increasing need for early warning and monitoring capabilities in both military and civilian sectors. Advanced radar, electro-optical sensors, and AI-based tracking systems enhance the effectiveness of detection-only solutions.

- By End User

On the basis of end user, the market is segmented into defense, homeland security, and others. The defense segment held the largest market revenue share of 60.2% in 2024, driven by significant government investments in counter-drone technologies to protect military installations and personnel from evolving UAV threats. The rise of drone-based warfare and asymmetric threats further fuels demand.

The homeland security segment is anticipated to witness the fastest growth rate of 29.1% from 2025 to 2032, driven by the need to safeguard critical infrastructure, public events, and urban areas from unauthorized drones. Increasing incidents of drone misuse, such as smuggling and surveillance, are prompting governments to deploy advanced anti-UAV systems.

Anti Unmanned Aerial Vehicle (UAV) Defence System Market Regional Analysis

- North America dominates the anti-UAV defence system market with the largest revenue share of 36.1% in 2024, driven by significant investments in counter-UAV technologies by the U.S. Department of Defense and a strong presence of key industry players

- Europe is projected to be the fastest-growing region during the forecast period, fueled by increasing defense budgets, growing adoption of advanced technologies, and rising concerns over drone-related security threats in countries such as Germany, France, and the U.K.

- The European Union’s focus on countering drone threats in urban environments and critical infrastructure, coupled with initiatives such as the EU’s counter-UAS programs, supports market expansion

U.S. Anti Unmanned Aerial Vehicle (UAV) Defence System Market Insight

The U.S. holds the largest share of the North American market and is expected to witness rapid growth from 2025 to 2032, driven by significant government spending on counter-drone technologies and rising incidents of unauthorized drone activities near military bases and critical infrastructure. The U.S. Department of Defense’s contracts, such as RTX’s $237 million deal for Ku-band Radio Frequency Sensors (KuRFS) and Coyote effectors, underscore the focus on advanced anti-UAV solutions.

Europe Anti Unmanned Aerial Vehicle (UAV) Defence System Market Insight

The European market is expected to experience robust growth, supported by regulatory mandates and increasing demand for counter-drone systems in military and civilian applications. Countries such as Germany and France are investing in multi-layered anti-UAV solutions to protect critical infrastructure and public spaces. The adoption of advanced technologies, such as AI-driven detection and laser systems, further accelerates market growth.

U.K. Anti Unmanned Aerial Vehicle (UAV) Defence System Market Insight

The U.K. market is anticipated to witness healthy growth, driven by a 300% increase in reported drone incidents over restricted areas such as airports and military installations in recent years. The U.K. Ministry of Defence and Civil Aviation Authority are prioritizing counter-UAS technologies, with companies such as BAE Systems leading innovation in radar and electronic systems to enhance airspace security.

Germany Anti Unmanned Aerial Vehicle (UAV) Defence System Market Insight

Germany is expected to see significant growth in the anti-UAV defence system market, driven by its advanced defense manufacturing sector and focus on technological innovation. The country’s emphasis on protecting critical infrastructure and public events from drone threats, combined with partnerships between defense contractors and emerging firms such as Dedrone, supports market expansion.

Asia-Pacific Anti Unmanned Aerial Vehicle (UAV) Defence System Market Insight

The Asia-Pacific region is expected to hold a significant market share, driven by rapid urbanization, increasing defense budgets, and growing drone usage in countries such as China, India, and Japan. Government initiatives to counter drone-based threats in military and civilian applications, along with advancements in AI and radar technologies, are boosting market growth.

Japan Anti Unmanned Aerial Vehicle (UAV) Defence System Market Insight

Japan’s anti-UAV defence system market is projected to witness robust growth, fueled by the country’s focus on technological innovation and national security. The increasing use of drones for commercial and recreational purposes has heightened the need for counter-drone solutions to protect airports, public events, and critical infrastructure.

China Anti Unmanned Aerial Vehicle (UAV) Defence System Market Insight

China holds the largest share of the Asia-Pacific anti-UAV defence system market, driven by rapid advancements in drone technology and growing security concerns. The country’s investments in AI-powered detection systems and laser technologies, coupled with its focus on protecting urban areas and military installations, support sustained market growth.

Anti Unmanned Aerial Vehicle (UAV) Defence System Market Share

The anti unmanned aerial vehicle (UAV) defence system industry is primarily led by well-established companies, including:

- Check Point Software Technologies Ltd. (Israel)

- Cisco Systems, Inc. (U.S.)

- Fortinet, Inc. (U.S.)

- Juniper Networks, Inc. (U.S.)

- Kaspersky Lab. (Russia)

- Trend Micro (Japan)

- Palo Alto Networks, Inc. (U.S.)

- WatchGuard Technologies, Inc. (U.S.)

- Raytheon Company (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Israel Aerospace Industries Ltd. (Israel)

- Thales Group (France)

- BAE Systems plc (U.K.)

- The Boeing Company (U.S.)

Latest Developments in Global Anti Unmanned Aerial Vehicle (UAV) Defence System Market

- In May 2024, HENSOLDT partnered with Singapore’s Home Team Science and Technology Agency (HTX) to develop Rapid Deployable Counter UAV Systems (CUAS) for urban environments. This collaboration integrates advanced detection and neutralization technologies to address UAV threats in densely populated areas, enhancing public safety and homeland security applications. The CUAS system incorporates HENSOLDT’s Z:ASSESS software and Multi-Sensor Data Fusion technology, providing real-time threat detection and mapping capabilities. The initiative strengthens HENSOLDT’s global presence in the counter-UAV market and was showcased at the Milipol Asia-Pacific–TechX Summit 2024

- In April 2024, Israel Aerospace Industries (IAI) and Aerotor Unmanned Systems signed a Memorandum of Understanding (MoU) to advance unmanned aerial system technologies, particularly in counter-UAV solutions. IAI brings its expertise in aviation and unmanned platforms, while Aerotor integrates its Apus multicopter, which features a heavy-fuel propulsion system and a variable-pitch mechanism for enhanced payload capacity and agility. This collaboration aims to develop innovative counter-UAV systems for defense and commercial applications, strengthening their competitive position in the global market

- In August 2023, Elbit Systems secured a $55 million contract to supply multi-layered ReDrone Counter Unmanned Aerial Systems (C-UAS) to the Netherlands. The ReDrone system integrates advanced detection, tracking, and neutralization capabilities, providing a comprehensive solution to counter unauthorized UAVs. The contract includes mobile, stationary, and deployed configurations of the ReDrone system, along with training and logistical support. The system features Elbit’s DAiR Radar, signal intelligence (SIGINT) sensors, and COAPS-L electro-optical payload, ensuring enhanced aerial surveillance and electronic attack capabilities. This agreement strengthens Elbit’s foothold in the European market and highlights its expertise in counter-UAV technologies for defense forces

- In April 2023, RTX secured a $237 million contract from the US Army to supply Ku-band Radio Frequency Sensors (KuRFS) and Coyote effectors for detecting and neutralizing unmanned aircraft systems. The contract includes both fixed and mobile systems, enhancing the Army’s operational capabilities in the US Central Command region. KuRFS provides advanced 360-degree threat detection, while Coyote effectors offer scalable counter-UAV solutions, including the ability to defeat drone swarms. This agreement reinforces RTX’s leadership in military defense technologies

- In March 2023, Blighter Surveillance Systems entered into a contract with Raytheon UK to supply its multi-mode A800 3D e-scan radars for a Laser Directed Energy Weapon (LDEW) system project. This initiative showcases Raytheon’s capability to neutralize small UAVs using advanced laser technology, with the A800 radars providing initial target detection and direction for the laser’s targeting system. The laser weapon system will be mounted on a vehicle, with ground-based A800 radars assisting in detection and designation. The collaboration strengthens the integration of radar and directed energy systems, positioning both companies as leaders in counter-UAV defense solutions for military applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Anti Uav Defence System Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Anti Uav Defence System Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Anti Uav Defence System Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.