Global Antibody Drug Conjugates Contract Manufacturing Market

Market Size in USD Billion

USD

10.06 Billion

USD

15.15 Billion

2025

2033

USD

10.06 Billion

USD

15.15 Billion

2025

2033

| 2026 - 2033 | |

| USD 10.06 Billion | |

| USD 15.15 Billion | |

| % | |

|

Antibody Drug Conjugates Contract Manufacturing Market Overview

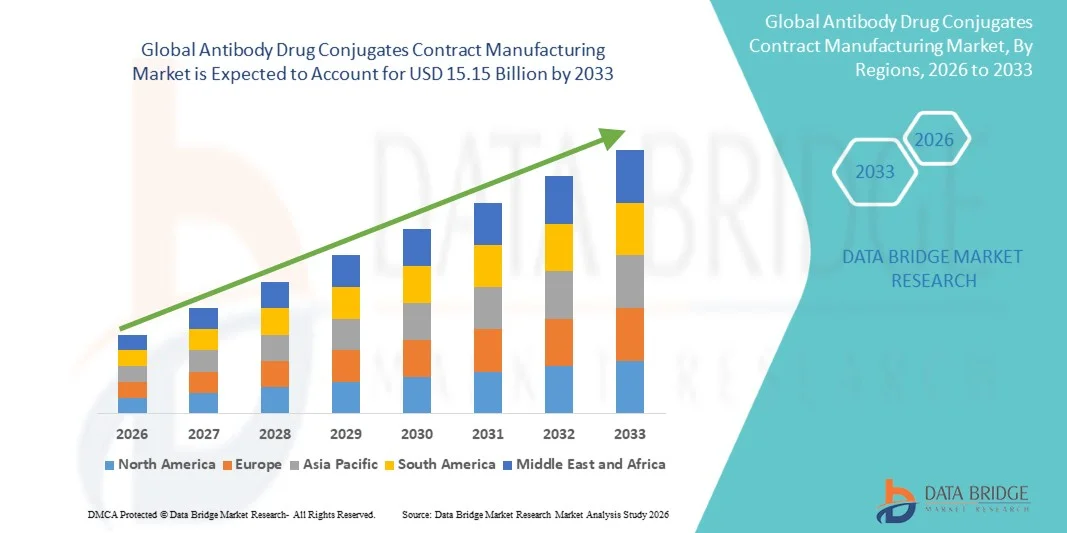

The global antibody drug conjugates (ADC) contract manufacturing market was valued at USD 10.06 billion in 2025 and is projected to reach USD 15.15 billion by 2033, growing at a CAGR of 5.25% from 2026 to 2033. Market growth is driven by an expanding global pipeline of ADC therapies, the complexity and capital intensity of ADC production, and an increasing preference among biopharmaceutical companies to outsource manufacturing to specialized contract development and manufacturing organizations (CDMOs).

Rising cancer incidence, regulatory advancements, and the commercial success of approved ADCs such as Enhertu and Padcev are further accelerating demand for contract manufacturing services. Investments in bioconjugation capabilities, linker-payload chemistry expertise, and compliance with stringent regulatory standards are shaping the competitive landscape. Additionally, the proliferation of novel ADC candidates entering clinical trials is creating robust opportunities for CDMOs across North America, Europe, and Asia-Pacific, supporting sustained market expansion over the forecast period.

Key Market Trends & Insights

- North America dominated the Antibody Drug Conjugates Contract Manufacturing Market with the largest revenue share of 42.6% in 2025, supported by a concentrated base of leading CDMOs, robust R&D investment, and proximity to major pharmaceutical sponsors.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.8% from 2026 to 2033, driven by expanding CDMO capacity, cost advantages, and increasing partnerships between regional players and global pharma companies.

- The Cleavable Linker segment led the market with a 68.4% market share in 2025, reflecting its broad applicability, enhanced payload release, and widespread adoption in approved and pipeline ADCs.

- The Breast Cancer segment dominated the condition category with a 38.2% market share in 2025, propelled by the commercial success of HER2-targeted ADCs and ongoing innovation in triple-negative breast cancer therapies.

- The Commercial stage segment held the largest share of the stage of development category with a 44.7% market share in 2025, driven by manufacturing scale-up requirements for approved ADC products and expanding indications.

- The Phase III segment is anticipated to be the fastest-growing stage of development category, fueled by a surge in late-stage clinical candidates and growing sponsor demand for large-scale, GMP-compliant manufacturing.

Market Size & Forecast

- Global Market Value (2025): USD 10.06 Billion

- Expected Market Value (2033): USD 15.15 Billion

- Forecast CAGR (2026–2033): 5.25%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Antibody Drug Conjugates Contract Manufacturing Market Segmentation

|

Attributes |

Antibody Drug Conjugates Contract Manufacturing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Lonza Group AG (Switzerland) · Samsung Biologics Co., Ltd. (South Korea) · WuXi Biologics (China) · Catalent, Inc. (U.S.) · Siegfried Holding AG (Switzerland) · Piramal Pharma Solutions (India) · Novasep Holding SAS (France) · FUJIFILM Diosynth Biotechnologies (Japan) · Almac Group (U.K.) · Cytovance Biologics, Inc. (U.S.) · AGC Biologics (U.S.) · Cerbios-Pharma SA (Switzerland) · Abzena Ltd. (U.K.) · Goodwin Biotechnology, Inc. (U.S.) · Avid Bioservices, Inc. (U.S.) |

|

Market Opportunities |

· Expansion of CDMO capacity in Asia-Pacific to meet rising global demand and cost optimization strategies · Growth in novel payload-linker platforms and site-specific conjugation technologies requiring specialized manufacturing expertise |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Antibody Drug Conjugates Contract Manufacturing Market Trends

Trend: Expansion of Bioconjugation and Payload Manufacturing Capabilities

CDMOs are investing heavily in bioconjugation suites, highly potent active pharmaceutical ingredient (HPAPI) handling, and site-specific conjugation technologies to address the growing complexity of next-generation ADCs. Strategic expansions include the addition of contained manufacturing lines, advanced analytical capabilities, and flexible scale-up infrastructure to accommodate both clinical and commercial batches. Regulatory harmonization efforts are encouraging CDMOs to standardize quality systems, supporting cross-border partnerships and accelerating time-to-market for ADC sponsors.

For instance,

Leading CDMOs have announced multi-million-dollar investments in new bioconjugation facilities across North America and Europe to serve the expanding global ADC pipeline.

In addition, partnerships between CDMOs and technology licensors are enabling broader access to proprietary linker-payload platforms, supporting innovation and diversification in ADC manufacturing.

Antibody Drug Conjugates Contract Manufacturing Market Dynamics

Key Market Driver: Rising Pipeline of ADC Therapies and Commercial Approvals

The global ADC pipeline has expanded rapidly, with more than 100 candidates in active clinical development as of 2025. The commercial success of recently approved ADCs, including Enhertu and Padcev, has demonstrated the therapeutic and commercial potential of this modality, prompting sponsors to scale manufacturing through outsourcing. CDMOs with established bioconjugation expertise, regulatory track records, and flexible capacity are well-positioned to capture this demand.

Key Restraint/Challenge: Manufacturing Complexity and Regulatory Stringency

ADC production involves intricate bioconjugation processes, handling of highly potent payloads, and stringent regulatory requirements for quality and containment. These factors increase capital and operational costs, limit the number of qualified CDMOs, and create bottlenecks in capacity. Variability in linker-payload stability and analytical method validation further complicate technology transfer and scale-up.

For instance,

Regulatory agencies require comprehensive data on conjugation efficiency, payload distribution, and product stability, necessitating advanced analytical infrastructure and process validation expertise. These manufacturing and regulatory complexities can constrain production scalability, increase development timelines, and create capacity limitations, potentially slowing market expansion despite growing demand for antibody-drug conjugates.

Key Market Opportunity: Growth of Outsourcing by Emerging Biotech Sponsors

Small and mid-sized biotechnology companies, which represent a significant share of the ADC pipeline, increasingly rely on CDMOs for end-to-end manufacturing services. This trend is driving demand for integrated offerings that span process development, clinical supply, and commercial production, creating opportunities for CDMOs to expand service portfolios and build long-term partnerships.

Antibody Drug Conjugates Contract Manufacturing Market Scope

The antibody drug conjugates contract manufacturing market is segmented on the basis of linker, condition, and stage of development.

By Linker

On the basis of linker, the Antibody Drug Conjugates Contract Manufacturing Market is segmented into cleavable linker and non-cleavable. The cleavable linker segment dominated the market with a 68.4% market share in 2025, supported by its broad applicability across diverse ADC platforms, enhanced intracellular payload release, and adoption in the majority of approved and late-stage pipeline ADCs. Cleavable linkers are favored for their ability to optimize therapeutic index and are compatible with a wide range of cytotoxic payloads, making them the preferred choice for sponsors and CDMOs alike.

The non-cleavable segment is expected to witness steady growth, driven by applications in specific indications requiring stable systemic circulation and controlled release profiles. Non-cleavable linkers offer advantages in minimizing off-target toxicity and are increasingly explored in next-generation ADC designs.

By Condition

On the basis of condition, the Antibody Drug Conjugates Contract Manufacturing Market is segmented into myeloma, lymphoma, breast cancer, and others. The breast cancer segment dominated the market with a market share of 38.2% in 2025, driven by the commercial success of HER2-targeted ADCs, expanding indications in triple-negative breast cancer, and a robust pipeline of next-generation therapies. High patient volumes, favorable reimbursement, and strong clinical outcomes have reinforced sponsor investment in breast cancer-focused ADC development and manufacturing.

The breast cancer segment is also expected to register the highest CAGR during the forecast period in the global antibody-drug conjugates (ADC) contract manufacturing market. Growth is driven by the expanding pipeline of HER2-targeted and novel ADC therapies, increasing regulatory approvals, rising prevalence of breast cancer, and growing demand for large-scale commercial manufacturing of complex ADC products, creating substantial opportunities for specialized contract manufacturing organizations.

By Stage of Development

On the basis of stage of development, the Antibody Drug Conjugates Contract Manufacturing Market is segmented into Phase I, Phase II, Phase III, and commercial. The commercial segment dominated the market with a market share of 44.7% in 2025, reflecting the scale-up requirements for approved ADC products, expanding indications, and growing demand for large-scale, GMP-compliant manufacturing. Commercial manufacturing generates the highest revenue per project and requires sustained CDMO capacity and quality assurance infrastructure.

The Phase III segment is expected to be the fastest-growing category in the global antibody-drug conjugates contract manufacturing market during the forecast period, driven by a growing number of ADC candidates advancing into late-stage clinical trials and approaching commercialization. Increasing demand for large-scale manufacturing, process validation, regulatory compliance, and commercial supply readiness is prompting biopharmaceutical companies to partner with specialized CDMOs possessing advanced conjugation, analytical, and high-potency manufacturing capabilities.

Antibody Drug Conjugates Contract Manufacturing Market Regional Analysis

North America dominated the antibody drug conjugates contract manufacturing market with a revenue share of 42.6% in 2025, supported by a concentrated base of leading CDMOs, robust R&D investment, proximity to major pharmaceutical sponsors, and advanced regulatory infrastructure. The presence of key industry players and strong demand from both large pharma and emerging biotech sponsors reinforces North America's leadership position.

U.S. Antibody Drug Conjugates Contract Manufacturing Market Insight

The U.S. antibody drug conjugates contract manufacturing market benefits from a mature CDMO ecosystem, high sponsor investment in ADC development, and a favorable regulatory environment. Major CDMOs have expanded bioconjugation capacity and established partnerships with leading ADC developers, enabling rapid scale-up and commercialization. The U.S. market is further supported by strong intellectual property protections and access to capital for capacity expansion.

Europe Antibody Drug Conjugates Contract Manufacturing Market Insight

The Europe antibody drug conjugates contract manufacturing market remains a major contributor, with established CDMOs in Switzerland, Germany, France, and the U.K. offering advanced bioconjugation and HPAPI handling capabilities. European sponsors and CDMOs benefit from harmonized regulatory pathways and cross-border collaboration, supporting efficient technology transfer and clinical supply. Investment in containment infrastructure and process automation is driving operational efficiency and quality improvements.

U.K. Antibody Drug Conjugates Contract Manufacturing Market Insight

The U.K. antibody drug conjugates contract manufacturing market is characterized by strong academic-industry collaboration, a skilled workforce, and access to global pharma sponsors. CDMOs in the U.K. are expanding capacity to serve both domestic and international clients, with a focus on clinical and commercial-stage manufacturing.

Germany Antibody Drug Conjugates Contract Manufacturing Market Insight

The Germany antibody drug conjugates contract manufacturing market benefits from a robust pharmaceutical manufacturing base, advanced engineering capabilities, and strong regulatory compliance. German CDMOs are increasingly investing in bioconjugation and HPAPI infrastructure to capture growing demand from European and global ADC sponsors.

Asia-Pacific Antibody Drug Conjugates Contract Manufacturing Market Insight

The Asia-Pacific antibody drug conjugates contract manufacturing market is poised for rapid growth with a CAGR of 7.8% during the forecast period, driven by expanding CDMO capacity, cost advantages, and increasing partnerships between regional players and global pharma companies. China, South Korea, and India are emerging as key manufacturing hubs, supported by government incentives and a growing talent pool in biopharmaceutical manufacturing.

Japan Antibody Drug Conjugates Contract Manufacturing Market Insight

The Japan antibody drug conjugates contract manufacturing market benefits from advanced biotechnology infrastructure, strong regulatory standards, and established partnerships with global ADC developers. Japanese CDMOs are investing in next-generation bioconjugation platforms and expanding capacity to serve both domestic and international sponsors.

China Antibody Drug Conjugates Contract Manufacturing Market Insight

The China antibody drug conjugates contract manufacturing market is experiencing rapid growth, driven by large-scale CDMO investments, competitive pricing, and increasing integration into global supply chains. Chinese CDMOs are enhancing quality systems and regulatory compliance to meet the requirements of international sponsors and support export-oriented manufacturing.

Antibody Drug Conjugates Contract Manufacturing Market Share

The antibody drug conjugates contract manufacturing industry is primarily led by well-established companies, including:

- Lonza Group AG (Switzerland)

- Samsung Biologics Co., Ltd. (South Korea)

- WuXi Biologics (China)

- Catalent, Inc. (U.S.)

- Siegfried Holding AG (Switzerland)

- Piramal Pharma Solutions (India)

- Novasep Holding SAS (France)

- FUJIFILM Diosynth Biotechnologies (Japan)

- Almac Group (U.K.)

- Cytovance Biologics, Inc. (U.S.)

- AGC Biologics (U.S.)

- Cerbios-Pharma SA (Switzerland)

- Abzena Ltd. (U.K.)

- Goodwin Biotechnology, Inc. (U.S.)

- Avid Bioservices, Inc. (U.S.)

Latest Developments in Antibody Drug Conjugates Contract Manufacturing Market

- In February 2026, Lonza announced the expansion of its bioconjugation manufacturing capabilities at its Visp, Switzerland facility to support increasing global demand for antibody-drug conjugates. The investment added commercial-scale conjugation suites, advanced containment systems, and analytical capabilities, strengthening Lonza’s position as a leading ADC contract manufacturing partner.

- In October 2025, Piramal Pharma Solutions completed a major expansion of its ADC manufacturing facility in Grangemouth, U.K. The project increased payload-linker production capacity and enhanced high-potency API manufacturing capabilities, enabling the company to support a growing pipeline of clinical and commercial ADC programs.

- In June 2025, Samsung Biologics announced the launch of integrated ADC development and manufacturing services, combining antibody production, conjugation, and aseptic fill-finish capabilities within a single platform. The initiative was designed to provide end-to-end solutions for biopharmaceutical companies developing next-generation ADC therapies.

- In April 2024, WuXi Biologics launched its comprehensive ADC Contract Development and Manufacturing Organization (CDMO) platform, integrating monoclonal antibody development, linker-payload manufacturing, bioconjugation, and fill-finish services. The expansion aimed to accelerate ADC development timelines and support increasing global demand for outsourced manufacturing.

- In March 2024, MilliporeSigma (the U.S. and Canada life science business of Merck KGaA, Darmstadt, Germany) announced the commercial readiness of its newly expanded ADC manufacturing facility in St. Louis, Missouri. The investment enhanced the company's ability to provide end-to-end CDMO services for highly potent ADC therapies.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.