Global Antibody Fragment Therapeutics Market

Market Size in USD Billion

USD

9.28 Billion

USD

18.62 Billion

2025

2033

USD

9.28 Billion

USD

18.62 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.28 Billion | |

| USD 18.62 Billion | |

| % | |

|

Antibody Fragment Therapeutics Market Overview

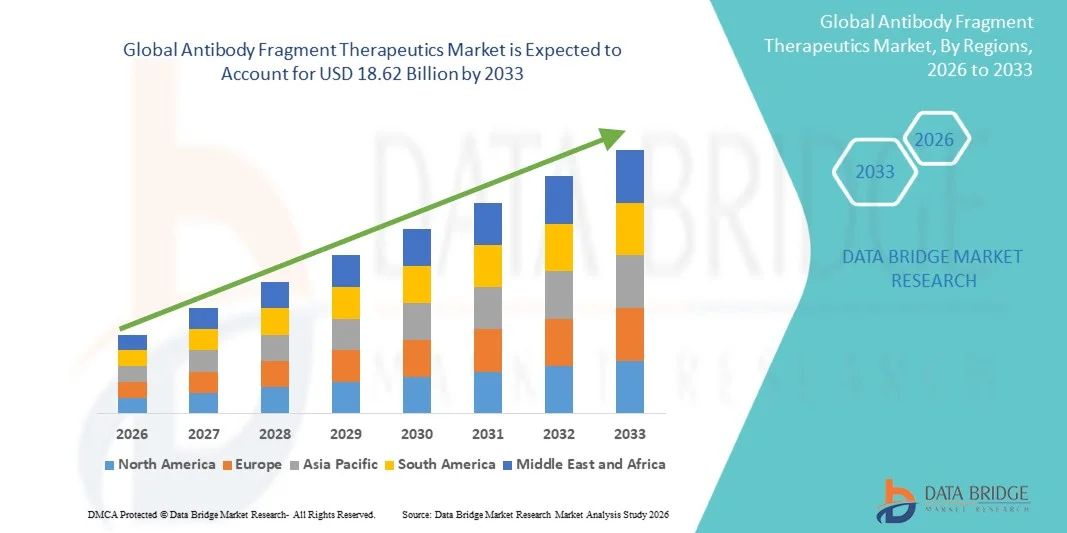

As per Data Bridge Market Research analysis, the antibody fragment therapeutics market was valued at USD 9.28 billion in 2025 and is projected to reach USD 18.62 billion by 2033, growing at a CAGR of 9.10% from 2026 to 2033. The market is experiencing consistent growth driven by the increasing prevalence of chronic diseases, rising demand for targeted biologics with superior tissue penetration and reduced immunogenicity, and the expanding pipeline of fragment-based therapeutics across oncology, autoimmune, and metabolic disorders.

The growing adoption of fab fragments, nanobodies, and single-chain variable fragments (scFvs) in therapeutic applications, together with advancements in AI-directed phage display, cell-free synthesis, and fragment-drug conjugate technologies, is accelerating innovation across the market. Increasing regulatory support for novel antibody formats, expanding investments in fragment-specific manufacturing, and broader use of antibody fragments in molecular imaging and targeted drug delivery are further strengthening market growth by improving therapeutic precision, development efficiency, and clinical outcomes.

Market Size & Forecast

- Global Market Value (2025): USD 9.28 Billion

- Expected Market Value (2033): USD 18.62 Billion

- Forecast CAGR (2026–2033): 9.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the antibody fragment therapeutics market with the largest revenue share of 46.2% in 2025, supported by strong biologics R&D, high adoption of targeted therapies, and a favorable regulatory environment

- The fab segment led the market with a 44.4% share in 2025, driven by its established clinical success, broad regulatory acceptance, and extensive use in approved antibody fragment therapeutics

- Asia-Pacific is expected to be the fastest-growing regional market, registering a CAGR of 8.3% from 2026 to 2033, fueled by increasing investments in fragment-specific manufacturing capacity, expanding biopharmaceutical industries, and regulatory harmonization

- scFv are the fastest-growing fragment type, projected to register a CAGR of 10.8%, reflecting the surge in compact structure, engineering flexibility, and expanding use in next-generation immunotherapies

- The bacterial segment dominated the production method category with a 39.6% revenue share in 2025, led by its cost-effective manufacturing capabilities, rapid production cycles, and widespread use in recombinant antibody fragment production

- Monoclonal antibodies accounted for 58.7% of the market, preferred by extensive clinical utilization, strong regulatory support, and widespread adoption across multiple therapeutic areas

- The drug delivery & conjugates segment is the fastest-growing application category, with a CAGR of 12.1%, driven by increasing development of antibody fragment-drug conjugates and targeted payload delivery systems

Report Scope and Antibody Fragment Therapeutics Market Segmentation

|

Attributes |

Antibody Fragment Therapeutics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Antibody Fragment Therapeutics Market Trends

Trend: Growing Development of Nanobody Antibody Fragment Therapeutics

Antibody fragment therapeutics are increasingly being developed in the form of nanobodies, single-chain variable fragments (scFvs), and bispecific antibody fragments owing to their small size, enhanced tissue penetration, and ability to access difficult-to-reach targets. Advances in protein engineering and antibody discovery technologies are accelerating the development of next-generation fragment-based therapies across oncology, autoimmune disorders, and rare diseases. For instance, in April 2025, the U.S. FDA approved the prefilled syringe (PFS) version of Vyvgart Hytrulo developed by argenx for adults with generalized myasthenia gravis (gMG) and chronic inflammatory demyelinating polyneuropathy (CIDP), enabling at-home self-administration and expanding patient access, further strengthening the commercial adoption of Fc-fragment-based therapeutics.

The growing success of nanobody and Fc-fragment-based therapies is accelerating innovation and expanding the role of antibody fragments in modern biologic drug development.

Antibody Fragment Therapeutics Market Dynamics

Key Market Driver: Rising Demand for Targeted Biologics with Enhanced Tissue Penetration

The increasing burden of cancer, autoimmune diseases, and rare disorders is driving demand for highly targeted biologics capable of achieving improved tissue penetration and reduced off-target effects. Antibody fragments offer advantages over conventional monoclonal antibodies through better tissue accessibility and rapid target engagement, supporting their growing adoption in precision medicine. For instance, in September 2021, the U.S. FDA approved Byooviz (ranibizumab-nuna), the first biosimilar to Genentech's Lucentis (ranibizumab), for the treatment of neovascular (wet) age-related macular degeneration (AMD), macular edema following retinal vein occlusion (RVO), myopic choroidal neovascularization (mCNV), and diabetic macular edema (DME), highlighting the established clinical value and expanding adoption of ranibizumab, an anti-VEGF antibody fragment, in retinal disease management.

The ability of antibody fragments to provide precise targeting while maintaining favorable efficacy profiles remains a major driver supporting market expansion.

Key Restraint/Challenge: Manufacturing Complexity and Short Biological Half-Life

Despite their therapeutic advantages, antibody fragments often exhibit shorter serum half-lives than full-length monoclonal antibodies because they lack Fc-mediated recycling mechanisms. As a result, developers frequently require additional engineering approaches such as PEGylation, albumin binding, or Fc fusion, increasing development complexity and production costs. For instance, in January 2023, an article published in Bioengineering titled "Bioengineering of Antibody Fragments: Challenges and Opportunities" highlighted that antibody fragments experience rapid blood clearance because of their small size and lack of an Fc domain, requiring half-life extension strategies such as PEGylation, albumin conjugation, or Fc fusion, which increase development complexity and manufacturing challenges.

Pharmacokinetic limitations and the need for advanced engineering strategies continue to represent important barriers to broader market adoption.

Key Market Opportunity: Expansion of Antibody Fragment-Drug Conjugates and Molecular Imaging Applications

The use of antibody fragments in targeted drug delivery, molecular imaging, and theranostics is creating significant growth opportunities. Their small molecular size enables rapid tissue penetration and efficient delivery of imaging agents, radionuclides, and therapeutic payloads, supporting the advancement of precision medicine. For instance, in August 2024, the National Medical Products Administration approved Envafolimab (Envida), the world's first subcutaneously administered anti-PD-L1 single-domain antibody (nanobody), for the treatment of patients with MSI-H/dMMR advanced solid tumors. The approval demonstrated growing pharmaceutical investment and confidence in nanobody-based antibody fragment therapeutics, creating significant opportunities for expanding fragment-based targeted therapies and precision oncology.

Expanding use of antibody fragments in theranostics, molecular imaging, and targeted drug conjugates is expected to unlock substantial long-term market opportunities.

Antibody Fragment Therapeutics Market Scope

The antibody fragment therapeutics market is segmented on the basis of fragment type, production method, format, and application.

- By Fragment Type

On the basis of fragment type, the antibody fragment therapeutics market is segmented into fab, scfv, dual-fragment formats, and more. The fab segment dominated the market with an estimated 44.4% share in 2025, owing to its established clinical success, broad regulatory acceptance, and extensive use in approved antibody fragment therapeutics. Fab fragments offer high antigen specificity while maintaining a smaller molecular size than full-length antibodies, enabling improved tissue penetration. Their proven efficacy in ophthalmology and autoimmune disease applications has strengthened physician confidence and commercial adoption. Pharmaceutical companies continue to invest in Fab-based therapies due to their validated manufacturing processes and clinical track record. The segment also benefits from growing demand for targeted biologics with favorable safety profiles. Continuous expansion of precision medicine approaches further supports its market leadership.

The scFv segment is projected to register the fastest growth at a CAGR of 10.8% from 2026 to 2033, driven by its compact structure, engineering flexibility, and expanding use in next-generation immunotherapies. Single-chain variable fragments are increasingly utilized in CAR-T cell therapies, bispecific constructs, and targeted drug delivery platforms. Their ability to bind specific antigens while maintaining low production costs makes them attractive for biopharmaceutical developers. Growing investment in cancer immunotherapy research is accelerating clinical development activities. Advances in protein engineering and antibody optimization technologies are further improving their therapeutic potential. Increasing adoption in innovative biologic platforms is expected to fuel strong future growth.

- By Production Method

On the basis of production method, the antibody fragment therapeutics market is segmented into bacterial, yeast, mammalian, and more. The bacterial segment accounted for the largest market share of 39.6% in 2025, supported by its cost-effective manufacturing capabilities, rapid production cycles, and widespread use in recombinant antibody fragment production. Bacterial expression systems enable efficient large-scale manufacturing of antibody fragments with relatively low operational costs. Their established infrastructure and extensive industrial experience have encouraged broad adoption across pharmaceutical and biotechnology companies. The segment also benefits from shorter development timelines and simplified production processes. Continuous improvements in expression technologies are enhancing protein yield and quality. These advantages continue to position bacterial systems as the preferred production method.

The mammalian segment is expected to witness the fastest growth at a CAGR of 11.2% from 2026 to 2033, due to its ability to produce complex biologics with superior protein folding and post-translational modifications. Mammalian expression systems are increasingly preferred for advanced antibody fragment formats requiring high biological activity and stability. Growing development of sophisticated therapeutic candidates is driving demand for these platforms. Pharmaceutical companies are investing heavily in mammalian manufacturing facilities to support expanding biologics pipelines. Improvements in cell line engineering and bioprocess optimization are enhancing production efficiency. The increasing focus on high-quality biologic therapeutics is expected to accelerate segment growth.

- By Format

On the basis of format, the antibody fragment therapeutics market is segmented into monoclonal antibodies, polyclonal antibodies, bispecific antibodies, and other novel antibody therapies. The monoclonal antibodies segment led the market with an estimated 58.7% share in 2025, driven by extensive clinical utilization, strong regulatory support, and widespread adoption across multiple therapeutic areas. Monoclonal antibody technologies provide highly specific targeting and have established a robust commercial ecosystem. Significant investments in biologics research and development continue to expand treatment options and improve patient outcomes. The segment benefits from a large number of approved products and advanced clinical-stage candidates. Continuous innovation in antibody engineering is further strengthening therapeutic effectiveness. Strong physician familiarity and reimbursement support continue to drive market dominance.

The bispecific antibodies segment is anticipated to register the fastest growth at a CAGR of 12.4% from 2026 to 2033, owing to its ability to simultaneously engage two distinct biological targets. This dual-targeting capability enhances therapeutic efficacy and supports novel treatment approaches in oncology and immune-mediated diseases. Growing success of bispecific antibody products is increasing industry investment and clinical development activity. Technological advancements are improving safety profiles and manufacturing feasibility. Pharmaceutical companies are actively expanding their bispecific pipelines to address unmet medical needs. The segment's potential to deliver superior clinical outcomes is expected to drive rapid expansion.

- By Application

On the basis of application, the antibody fragment therapeutics market is segmented into therapeutics, diagnostics & imaging, research reagents, drug delivery & conjugates, and biosensors. The therapeutics segment dominated the market with an estimated 69.5% share in 2025, driven by increasing use of antibody fragments in oncology, autoimmune disorders, ophthalmology, and rare disease treatment. Antibody fragments offer enhanced tissue penetration and target accessibility, making them highly suitable for precision medicine applications. Rising prevalence of chronic diseases is increasing demand for targeted biologic therapies. Expanding clinical pipelines and growing regulatory approvals are further supporting segment growth. Pharmaceutical companies continue to invest heavily in fragment-based therapeutic development. These factors collectively reinforce the segment's leading market position.

The drug delivery & conjugates segment is projected to be the fastest-growing application, registering a CAGR of 12.1% from 2026 to 2033, fueled by increasing development of antibody fragment-drug conjugates and targeted payload delivery systems. Antibody fragments enable precise delivery of therapeutic agents while minimizing systemic toxicity and off-target effects. Growing investment in precision oncology is driving innovation in conjugate technologies. Advances in linker chemistry and payload engineering are improving treatment efficacy and safety. Pharmaceutical companies are increasingly exploring fragment-based conjugates for complex and difficult-to-treat diseases. Their ability to enhance therapeutic outcomes is expected to accelerate future adoption and market growth.

Antibody Fragment Therapeutics Market Regional Analysis

North America dominated the antibody fragment therapeutics market with the largest revenue share of 46.2% in 2024, supported by strong biologics R&D, high adoption of targeted therapies, and a favorable regulatory environment. The region benefits from advanced healthcare infrastructure, high adoption of targeted biologics, and favorable regulatory pathways for innovative antibody-based therapies. Growing clinical research activities in oncology, autoimmune diseases, and rare disorders are further accelerating market expansion. Increasing investments in next-generation antibody engineering technologies, including nanobodies and bispecific constructs, continue to support innovation. The presence of major biotechnology companies and extensive funding for biologics research further strengthens regional market leadership. Continuous regulatory approvals and commercialization of novel antibody fragment therapeutics are expected to sustain North America's dominant position in the global market.

U.S. Antibody Fragment Therapeutics Market Insight

The U.S. antibody fragment therapeutics market is witnessing strong growth due to rising investments in biologics research, increasing adoption of precision medicine, and a robust pipeline of antibody fragment-based therapies targeting oncology, autoimmune diseases, and rare disorders. The country's advanced biotechnology ecosystem, strong venture capital funding, and favorable regulatory environment continue to support innovation and commercialization activities. In addition, growing demand for targeted therapies with improved tissue penetration and reduced immunogenicity is accelerating market expansion. In April 2025, the U.S. FDA approved the prefilled syringe version of Vyvgart Hytrulo (efgartigimod alfa and hyaluronidase-qvfc) developed by argenx for generalized myasthenia gravis and chronic inflammatory demyelinating polyneuropathy, further expanding patient access to an Fc-fragment-based therapy.

Europe Antibody Fragment Therapeutics Market Insight

The Europe antibody fragment therapeutics market remains a major contributor to global revenue, driven by a strong biotechnology sector, extensive clinical research activities, and favorable support for innovative biologic therapies. The region benefits from increasing investment in antibody engineering technologies and the presence of leading developers specializing in nanobodies and antibody fragments. Growing adoption of targeted therapeutics for cancer and autoimmune diseases continues to support market growth. Belgium-based argenx reported global Vyvgart sales exceeding USD 2.2 billion in 2024, highlighting Europe's important role in the development and commercialization of antibody fragment-based therapies.

U.K. Antibody Fragment Therapeutics Market Insight

The U.K. antibody fragment therapeutics market is experiencing steady growth, supported by world-class biomedical research institutions, strong government support for life sciences innovation, and increasing investment in next-generation biologics. The country continues to play an important role in antibody engineering, translational research, and clinical development activities. Growing collaboration between academic institutions and biotechnology companies is further supporting market expansion. Researchers at the University of Oxford have continued to advance nanobody and antibody engineering research programs aimed at developing highly targeted therapies for cancer and infectious diseases, reinforcing the U.K.'s position in biologics innovation.

Germany Antibody Fragment Therapeutics Market Insight

The Germany antibody fragment therapeutics market is expanding steadily due to the country's strong pharmaceutical manufacturing base, advanced biotechnology capabilities, and increasing focus on precision medicine. German research institutes and pharmaceutical companies are actively involved in the development of novel antibody-based therapies and biomanufacturing technologies. Rising investments in oncology research and biologics production continue to support market growth. Germany remains one of Europe's largest biotechnology markets, with numerous antibody-focused research collaborations supported through federal innovation and life science funding programs.

Asia-Pacific Antibody Fragment Therapeutics Market Insight

The Asia-Pacific antibody fragment therapeutics market is expected to witness rapid growth, driven by expanding biopharmaceutical manufacturing capabilities, rising healthcare expenditures, and increasing investment in innovative biologics across China, Japan, South Korea, and India. Growing demand for targeted therapies and increasing participation in global clinical trials are accelerating regional market development. In addition, favorable government initiatives supporting biotechnology innovation are contributing to market expansion. Aaccording to the International Trade Administration, China continues to prioritize biotechnology as a strategic industry under national development plans, supporting significant investment in biologics and antibody-based therapeutics.

Japan Antibody Fragment Therapeutics Market Insight

The Japan antibody fragment therapeutics market is witnessing consistent growth due to strong investment in advanced biologics research, increasing adoption of precision medicine, and growing demand for targeted oncology therapies. The country has a well-established pharmaceutical industry and a supportive regulatory framework for innovative therapies. Japanese companies are actively investing in antibody engineering technologies and novel biologic drug development. Japan has been among the leading markets for approved biologics and antibody-based therapies, supported by the Pharmaceuticals and Medical Devices Agency's accelerated pathways for innovative treatments.

China Antibody Fragment Therapeutics Market Insight

The China antibody fragment therapeutics market is growing rapidly, driven by expanding biotechnology infrastructure, increasing R&D expenditure, and strong government support for innovative biologics development. The country has become a major hub for antibody drug discovery, clinical development, and manufacturing activities. Rising cancer incidence and growing demand for advanced targeted therapies are significantly boosting market demand. In November 2021, China's National Medical Products Administration approved Envafolimab (Enweida/KN035), the world's first subcutaneously administered anti-PD-L1 single-domain antibody (nanobody), for patients with MSI-H/dMMR advanced solid tumors, highlighting the country's growing leadership in antibody fragment innovation.

Antibody Fragment Therapeutics Market Share

The antibody fragment therapeutics industry is primarily led by well-established companies, including:

- argenx (Netherlands)

- AbbVie (U.S.)

- Amgen Inc. (U.S.)

- AstraZeneca (U.K.)

- Genentech, Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Novo Nordisk A/S (Denmark)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Sanofi (France)

- Eli Lilly and Company (U.S.)

- Bristol Myers Squibb (U.S.)

- Merck & Co., Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Genmab A/S (Denmark)

- Xencor, Inc. (U.S.)

- Harbour BioMed (Cayman Islands)

- Cartesian Therapeutics, Inc. (U.S.)

- MindWalk Holdings Corp (Canada)

- Inhibrx Biosciences, Inc. (U.S.)

Latest Developments in Antibody Fragment Therapeutics Market

- In April 2025, argenx announced that the U.S. FDA approved the prefilled syringe version of Vyvgart Hytrulo for adults with generalized myasthenia gravis (gMG) and chronic inflammatory demyelinating polyneuropathy (CIDP). The approval enables at-home self-administration, improves patient convenience, and expands access to one of the leading Fc-fragment-based therapeutics

- In November 2024, Zai Lab and argenx announced that China's National Medical Products Administration (NMPA) approved Vyvgart Hytrulo for chronic inflammatory demyelinating polyneuropathy (CIDP). It became the first and only approved treatment for CIDP in China, marking a significant expansion of the antibody fragment therapeutic franchise

- In June 2024, argenx announced that the U.S. FDA approved Vyvgart Hytrulo for adults with chronic inflammatory demyelinating polyneuropathy (CIDP). The product became the first and only FcRn blocker approved for CIDP, expanding the clinical applications of antibody fragment therapeutics in autoimmune neurology

- In November 2021, Alphamab Oncology and 3D Medicines announced that China's NMPA approved Envafolimab (ENWEIDA/KN035), the world's first subcutaneously administered anti-PD-L1 single-domain antibody (nanobody), for adults with MSI-H/dMMR advanced solid tumors. This represented the first commercial launch of a subcutaneous nanobody checkpoint inhibitor and a major milestone for antibody fragment therapeutics

- In October 2021, researchers published pivotal Phase II clinical trial results in the Journal of Hematology & Oncology demonstrating that subcutaneous Envafolimab showed durable antitumor activity and a favorable safety profile in patients with previously treated MSI-H/dMMR advanced solid tumors. These data directly supported the subsequent regulatory approval and reinforced the clinical potential of single-domain antibody therapeutics

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.