Global Antifibrinolytic Market

Market Size in USD Billion

CAGR :

%

USD

18.23 Billion

USD

26.93 Billion

2025

2033

USD

18.23 Billion

USD

26.93 Billion

2025

2033

| 2026 –2033 | |

| USD 18.23 Billion | |

| USD 26.93 Billion | |

| % | |

|

Antifibrinolytic Market Size

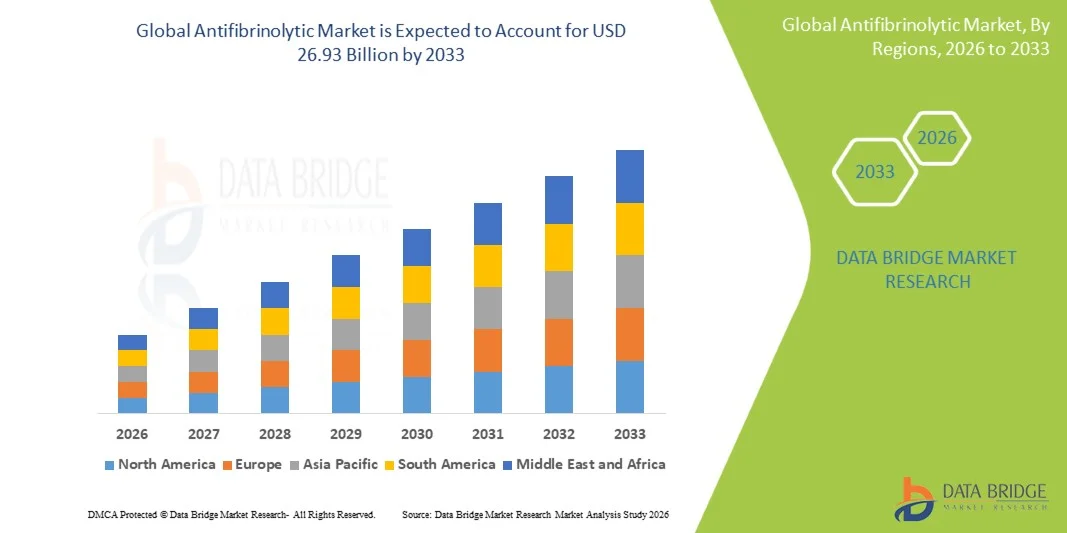

- The global antifibrinolytic market size was valued at USD 18.23 billion in 2025 and is expected to reach USD 26.93 billion by 2033, at a CAGR of 5.00% during the forecast period

- The market growth is largely driven by the increasing prevalence of surgical procedures, trauma cases, and chronic conditions such as cardiovascular diseases and bleeding disorders, which necessitate effective blood loss management and hemostatic control

- Furthermore, rising demand for cost-effective and efficient therapies in perioperative care, along with growing awareness regarding patient blood management (PBM) strategies across hospitals and healthcare systems, is positioning antifibrinolytic agents as essential components in modern clinical practice. These combined factors are significantly accelerating the adoption of antifibrinolytic therapies, thereby boosting overall market growth

Antifibrinolytic Market Analysis

- Antifibrinolytic agents, which help prevent excessive bleeding by inhibiting the breakdown of blood clots, are increasingly critical in modern healthcare settings, particularly in surgical procedures, trauma care, and the management of bleeding disorders, due to their effectiveness in reducing blood loss and minimizing the need for transfusions

- The rising demand for antifibrinolytics is primarily driven by the growing volume of surgeries worldwide, increasing incidence of trauma injuries, and heightened focus on patient blood management (PBM) practices, along with expanding applications in obstetrics, orthopedics, and cardiac surgeries

- North America dominated the antifibrinolytic market with the largest revenue share of 41.3% in 2025, supported by advanced healthcare infrastructure, high surgical procedure volumes, and strong adoption of evidence-based blood management protocols, with the U.S. witnessing significant usage of antifibrinolytic drugs across hospitals and ambulatory surgical centers

- Asia-Pacific is expected to be the fastest growing region in the antifibrinolytic market during the forecast period due to improving healthcare infrastructure, rising healthcare expenditure, and increasing awareness regarding effective bleeding management in emerging economies

- Tranexamic acid segment dominated the antifibrinolytic market with a market share of 45.7% in 2025, driven by its widespread clinical use, cost-effectiveness, and strong efficacy profile across a broad range of surgical and trauma-related applications

Report Scope and Antifibrinolytic Market Segmentation

|

Attributes |

Antifibrinolytic Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Antifibrinolytic Market Trends

“Expanding Clinical Adoption Driven by Evidence-Based Outcomes”

- A significant and accelerating trend in the global antifibrinolytic market is the increasing integration of evidence-based clinical protocols and guidelines supporting the routine use of antifibrinolytic agents across multiple surgical and therapeutic areas. This alignment with standardized care pathways is significantly improving patient outcomes and reducing perioperative risks

- For instance, tranexamic acid is widely incorporated into clinical guidelines for orthopedic and cardiac surgeries, where it is routinely administered to minimize intraoperative and postoperative blood loss. Similarly, its use in trauma protocols has been endorsed following large-scale clinical trials demonstrating survival benefits

- Clinical integration of antifibrinolytics enables features such as standardized dosing regimens, improved surgical efficiency, and reduced dependency on blood transfusions. For instance, hospitals adopting patient blood management (PBM) programs utilize antifibrinolytics to optimize hemostasis and lower transfusion-related complications. Furthermore, these agents support faster recovery times and reduced hospital stays by limiting excessive bleeding during procedures

- The seamless incorporation of antifibrinolytics into hospital treatment protocols facilitates coordinated care across departments such as surgery, emergency medicine, and obstetrics. Through unified clinical pathways, healthcare providers can ensure consistent and effective bleeding management, enhancing overall treatment efficiency and patient safety

- This trend towards more standardized, outcome-driven, and protocol-based usage is fundamentally reshaping treatment approaches in bleeding management. Consequently, companies such as Pfizer and Sun Pharmaceutical Industries are focusing on expanding clinical indications and improving formulation accessibility to align with evolving medical guidelines

- The demand for antifibrinolytics that offer proven clinical efficacy and broad applicability is growing rapidly across hospitals and surgical centers, as healthcare systems increasingly prioritize cost-effective and evidence-based treatment solutions

- Growing adoption of antifibrinolytics in emerging applications such as oncology-related bleeding and minimally invasive procedures is expanding the scope of these agents beyond traditional surgical use

Antifibrinolytic Market Dynamics

Driver

“Growing Need Due to Rising Surgical Volume and Focus on Blood Management”

- The increasing volume of surgical procedures worldwide, coupled with the growing emphasis on patient blood management (PBM) strategies, is a significant driver for the heightened demand for antifibrinolytic agents

- For instance, in March 2025, a leading healthcare provider network expanded its PBM program across multiple hospitals, incorporating antifibrinolytic therapies as a standard protocol to reduce transfusion rates. Such strategies by key healthcare institutions are expected to drive the antifibrinolytic market growth in the forecast period

- As healthcare providers aim to minimize blood loss and reduce reliance on donor blood, antifibrinolytics offer proven benefits such as decreased transfusion requirements, lower complication rates, and improved surgical outcomes, making them an essential component of modern perioperative care

- Furthermore, the increasing incidence of trauma cases, postpartum hemorrhage, and chronic conditions requiring surgical intervention is driving the adoption of antifibrinolytics across diverse medical specialties, including orthopedics, cardiology, and obstetrics

- The cost-effectiveness of antifibrinolytic therapies, combined with their ability to improve clinical efficiency and patient safety, is encouraging widespread adoption in both developed and emerging healthcare markets. The expansion of healthcare infrastructure and access to essential medicines further supports market growth

- Rising government and institutional initiatives promoting blood conservation strategies are further accelerating the integration of antifibrinolytics into standard treatment protocols across public healthcare systems

- Increasing awareness among healthcare professionals regarding the long-term benefits of reduced transfusion dependency is further strengthening the adoption of antifibrinolytic therapies globally

Restraint/Challenge

“Risk of Adverse Effects and Regulatory Compliance Hurdles”

- Concerns surrounding potential adverse effects and safety considerations associated with antifibrinolytic use, including thromboembolic complications, pose a significant challenge to broader market adoption. As these agents influence clot stability, careful patient selection and monitoring are required

- For instance, regulatory authorities have issued precautionary guidelines on antifibrinolytic usage in high-risk patients, leading to cautious adoption among healthcare providers in certain clinical scenarios

- Addressing these safety concerns through robust clinical data, updated treatment guidelines, and physician education is crucial for ensuring appropriate use. Companies such as F. Hoffmann-La Roche Ltd and Cipla Ltd emphasize safety profiles and adherence to regulatory standards in their product development and commercialization strategies. In addition, variability in regulatory approvals and labeling across regions can create barriers to uniform market penetration

- While antifibrinolytics are generally cost-effective, limited awareness in some developing regions and inconsistent access to healthcare facilities can hinder their optimal utilization, particularly in rural or under-resourced settings

- Overcoming these challenges through enhanced clinical research, harmonized regulatory frameworks, and improved access to healthcare services will be vital for sustaining long-term market growth

- Stringent regulatory requirements for drug approval and post-market surveillance can delay product launches and increase compliance costs for manufacturers operating in multiple regions

- Potential drug interactions and contraindications in patients with complex medical histories may limit widespread usage, necessitating careful clinical evaluation and restricting adoption in certain high-risk populations

Antifibrinolytic Market Scope

The market is segmented on the basis of drugs, indication, route of administration, end-users, and distribution channel.

- By Drugs

On the basis of drugs, the antifibrinolytic market is segmented into aminocaproic acid, tranexamic acid, and others. The tranexamic acid segment dominated the market with the largest market revenue share of 45.7% in 2025, driven by its extensive clinical adoption across a wide range of indications including trauma, surgeries, and obstetric bleeding. Its strong efficacy profile, affordability, and inclusion in essential medicine lists across multiple countries have significantly contributed to its widespread usage. In addition, the growing emphasis on patient blood management (PBM) practices has further strengthened its position in hospital protocols. The availability of multiple formulations such as oral and injectable forms enhances its accessibility and clinical flexibility. Increasing clinical evidence supporting its safety and effectiveness is also reinforcing its dominance. The drug’s role in reducing mortality in trauma cases further accelerates its global demand.

The aminocaproic acid segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its increasing use in specific surgical procedures and bleeding disorders where targeted fibrinolysis inhibition is required. Its application in cardiac surgeries and dental procedures for high-risk patients is gaining traction among healthcare providers. Growing awareness regarding alternative antifibrinolytic options is also supporting its adoption in niche therapeutic areas. The drug is particularly useful in patients who may not tolerate other antifibrinolytics, thereby expanding its clinical relevance. Rising healthcare access in emerging markets is contributing to increased utilization. In addition, ongoing research exploring new indications is expected to create further growth opportunities for this segment.

- By Indication

On the basis of indication, the antifibrinolytic market is segmented into gynecology, gastrointestinal bleeding, hereditary angioedema, hemorrhage, surgeries, and others. The surgeries segment dominated the market with the largest revenue share in 2025, driven by the high volume of surgical procedures globally and the critical need to manage intraoperative and postoperative blood loss. Antifibrinolytics are widely used in orthopedic, cardiac, and transplant surgeries to improve patient outcomes and reduce transfusion requirements. The growing adoption of minimally invasive surgeries is also contributing to the use of these agents for enhanced recovery. Hospitals increasingly rely on standardized bleeding management protocols, further boosting demand. In addition, cost savings associated with reduced blood transfusions are encouraging widespread usage. The consistent rise in elective and emergency surgeries globally supports sustained dominance of this segment.

The hemorrhage segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing cases of trauma injuries and postpartum hemorrhage worldwide. Antifibrinolytics play a crucial role in emergency settings by rapidly controlling excessive bleeding and improving survival rates. Growing awareness among healthcare professionals regarding early intervention in hemorrhagic conditions is supporting market expansion. The integration of antifibrinolytics into emergency care protocols is further accelerating adoption. Rising investments in emergency healthcare infrastructure, particularly in developing regions, are also contributing to growth. Furthermore, global health initiatives targeting maternal mortality reduction are boosting demand in this segment.

- By Route of Administration

On the basis of route of administration, the antifibrinolytic market is segmented into oral, injectable, and others. The injectable segment dominated the market with the largest revenue share in 2025, driven by its rapid onset of action and high effectiveness in critical care and surgical settings. Injectable antifibrinolytics are preferred in hospitals for managing acute bleeding and during major surgical procedures where immediate results are required. Their precise dosing and controlled administration make them suitable for emergency and intensive care applications. The widespread availability of injectable formulations in hospitals further strengthens this segment. In addition, their use in trauma and perioperative care continues to expand globally. The increasing number of hospital-based treatments reinforces their dominant position.

The oral segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its convenience, ease of administration, and suitability for long-term or outpatient treatment. Oral antifibrinolytics are increasingly prescribed for conditions such as heavy menstrual bleeding and hereditary angioedema. The growing preference for home-based care and reduced hospital visits is supporting the adoption of oral formulations. Improved patient compliance and lower administration costs are also key growth drivers. Pharmaceutical advancements in oral drug formulations are enhancing bioavailability and effectiveness. In addition, increasing awareness among patients and physicians is further boosting segment growth.

- By End-Users

On the basis of end-users, the antifibrinolytic market is segmented into hospitals, homecare, speciality centres, and others. The hospitals segment dominated the market with the largest revenue share in 2025, driven by the high volume of surgeries and emergency treatments performed in these settings. Hospitals serve as primary centers for administering antifibrinolytics, particularly in critical care, trauma, and surgical departments. The presence of skilled healthcare professionals and advanced infrastructure supports the effective use of these drugs. In addition, hospitals are key adopters of patient blood management programs, further driving demand. The increasing number of hospital admissions globally contributes to sustained growth. Furthermore, reimbursement support and standardized treatment protocols enhance segment dominance.

The homecare segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the rising trend toward decentralized healthcare and outpatient treatment. Patients with chronic conditions requiring antifibrinolytic therapy are increasingly opting for home-based care solutions. The convenience and cost-effectiveness of homecare settings are encouraging adoption. Technological advancements in drug delivery and telehealth support are further enabling this shift. Growing awareness and patient preference for personalized care also contribute to segment expansion. In addition, healthcare systems aiming to reduce hospital burden are promoting homecare services.

- By Distribution Channel

On the basis of distribution channel, the antifibrinolytic market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the market with the largest revenue share in 2025, driven by the high demand for antifibrinolytics in inpatient and surgical settings. Hospital pharmacies ensure the availability of essential drugs for immediate use in critical procedures and emergency care. The direct procurement and controlled distribution within hospitals enhance supply chain efficiency. In addition, strong coordination between healthcare providers and hospital pharmacies supports timely drug administration. The increasing number of surgical procedures further boosts demand through this channel. Furthermore, institutional purchasing agreements contribute to its dominant position.

The online pharmacy segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rapid digitalization of healthcare services and increasing consumer preference for convenient medication access. Online platforms offer ease of ordering, home delivery, and competitive pricing, attracting a growing patient base. The expansion of e-commerce infrastructure in healthcare is further supporting this trend. Increased internet penetration and smartphone usage are also driving adoption. Regulatory support for online pharmaceutical sales in several regions is enabling market growth. In addition, the shift toward outpatient care is boosting demand through online channels.

Antifibrinolytic Market Regional Analysis

- North America dominated the antifibrinolytic market with the largest revenue share of 41.3% in 2025, supported by advanced healthcare infrastructure, high surgical procedure volumes, and strong adoption of evidence-based blood management protocols

- Healthcare providers in the region highly value the clinical efficacy, cost-effectiveness, and rapid action offered by antifibrinolytic agents across surgical, trauma, and obstetric applications

- This widespread adoption is further supported by advanced healthcare infrastructure, strong reimbursement frameworks, and the presence of leading pharmaceutical companies, establishing antifibrinolytics as a standard component in modern treatment protocols across hospitals and specialty care settings

U.S. Antifibrinolytic Market Insight

The U.S. antifibrinolytic market captured the largest revenue share of 80% in 2025 within North America, fueled by the high volume of surgical procedures and the expanding adoption of patient blood management (PBM) programs. Healthcare providers are increasingly prioritizing the reduction of blood loss and transfusion dependency through effective pharmacological interventions. The growing preference for evidence-based treatment protocols, combined with strong demand for cost-effective therapies and improved clinical outcomes, further propels the antifibrinolytic market. Moreover, the increasing integration of antifibrinolytics into trauma care guidelines and surgical practices is significantly contributing to the market's expansion. The presence of leading pharmaceutical companies and continuous clinical research activities further strengthen market growth. In addition, favorable reimbursement policies and advanced hospital infrastructure support widespread adoption across healthcare facilities.

Europe Antifibrinolytic Market Insight

The Europe antifibrinolytic market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent clinical guidelines and the escalating need for effective bleeding management in hospitals and surgical centers. The increase in aging population, coupled with the rising number of surgeries, is fostering the adoption of antifibrinolytic therapies. European healthcare providers are also drawn to the clinical efficiency and cost savings these drugs offer. The region is experiencing significant growth across orthopedic, cardiac, and obstetric applications, with antifibrinolytics being incorporated into both routine and complex medical procedures. Government support for improving surgical outcomes and reducing healthcare costs further accelerates market expansion. In addition, increasing awareness among healthcare professionals regarding advanced treatment protocols is boosting demand.

U.K. Antifibrinolytic Market Insight

The U.K. antifibrinolytic market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing focus on improving surgical outcomes and reducing healthcare costs. In addition, concerns regarding blood shortages and transfusion-related risks are encouraging hospitals to adopt antifibrinolytic therapies. The UK’s emphasis on standardized treatment pathways, alongside its strong public healthcare system, is expected to continue to stimulate market growth. Rising investments in healthcare infrastructure and surgical advancements are also supporting adoption. Furthermore, increasing awareness of patient safety and efficiency in perioperative care is driving the use of antifibrinolytics. The growing number of elective and emergency surgeries further contributes to sustained market growth.

Germany Antifibrinolytic Market Insight

The Germany antifibrinolytic market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of advanced bleeding management solutions and the demand for high-quality, evidence-based therapies. Germany’s well-developed healthcare infrastructure, combined with its emphasis on clinical research and innovation, promotes the adoption of antifibrinolytics, particularly in surgical and critical care settings. The integration of these therapies into hospital protocols is also becoming increasingly prevalent, with a strong preference for safe and effective treatment options aligning with regional healthcare standards. Increasing collaborations between research institutions and pharmaceutical companies are further enhancing product development. In addition, the rising geriatric population and surgical demand are contributing to market growth.

Asia-Pacific Antifibrinolytic Market Insight

The Asia-Pacific antifibrinolytic market is poised to grow at the fastest CAGR of 24% during the forecast period of 2026 to 2033, driven by increasing healthcare expenditure, rising surgical volumes, and improving access to medical treatments in countries such as China, Japan, and India. The region's growing focus on strengthening healthcare systems, supported by government initiatives promoting better clinical outcomes, is driving the adoption of antifibrinolytics. Furthermore, as APAC emerges as a key market for generic drug production, the affordability and accessibility of antifibrinolytic therapies are expanding to a wider patient population. Rapid urbanization and increasing awareness about advanced medical treatments are also contributing to growth. In addition, improvements in emergency care infrastructure are boosting demand for bleeding management solutions.

Japan Antifibrinolytic Market Insight

The Japan antifibrinolytic market is gaining momentum due to the country’s advanced healthcare system, aging population, and demand for high-quality medical care. The Japanese market places a significant emphasis on patient safety, and the adoption of antifibrinolytics is driven by the increasing number of surgical procedures and chronic disease cases. The integration of these drugs into clinical guidelines, along with their use in specialized treatments such as cardiac and orthopedic surgeries, is fueling growth. Moreover, Japan's aging demographic is likely to spur demand for effective bleeding management solutions in both hospital and outpatient settings. Continuous technological advancements in healthcare delivery are also supporting market expansion. In addition, strong regulatory frameworks ensure the availability of safe and effective therapies.

India Antifibrinolytic Market Insight

The India antifibrinolytic market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country's expanding healthcare infrastructure, rising population, and increasing awareness of cost-effective treatment options. India stands as one of the fastest-growing markets for generic pharmaceuticals, and antifibrinolytics are becoming increasingly popular in hospitals and emergency care settings. The push towards improving maternal healthcare and trauma care services, alongside the availability of affordable drug options and strong domestic manufacturers, are key factors propelling the market in India. Government initiatives to enhance healthcare access and reduce mortality rates are further supporting adoption. In addition, the increasing number of private hospitals and surgical centers is contributing to sustained market growth.

Antifibrinolytic Market Share

The Antifibrinolytic industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Sanofi (France)

- Takeda Pharmaceutical Company Limited (Japan)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Zydus Lifesciences Limited (India)

- Hikma Pharmaceuticals PLC (U.K.)

- Amneal Pharmaceuticals, Inc. (U.S.)

- Cipla Limited (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Lupin Limited (India)

- Aurobindo Pharma Limited (India)

- Glenmark Pharmaceuticals Limited (India)

- Intas Pharmaceuticals Ltd. (India)

- Alkem Laboratories Ltd. (India)

- Abbott (U.S.)

- Baxter (U.S.)

- Fresenius Kabi AG (Germany)

What are the Recent Developments in Global Antifibrinolytic Market?

- In October 2025, the U.S. Food and Drug Administration (FDA) announced mandatory labeling updates for tranexamic acid injection, including the addition of a boxed warning to prevent incorrect spinal administration. The update was issued after identifying medication errors linked to improper administration routes. This regulatory action underscores the growing focus on drug safety and proper usage of antifibrinolytic therapies in clinical settings, ensuring safer adoption across hospitals and surgical environments

- In September 2025, researchers published a clinical study evaluating the combined use of tranexamic acid with anticoagulants in joint replacement surgeries, demonstrating effective reduction in postoperative complications such as deep vein thrombosis. The findings support the expanding clinical application of antifibrinolytics in orthopedic procedures and reinforce their role in improving surgical outcomes. This development highlights ongoing research efforts to optimize antifibrinolytic usage across complex treatment protocols

- In March 2025, Nexus Pharmaceuticals, LLC, announced the launch of its Tranexamic Acid injection, expanding its portfolio of life-saving hospital drugs. The product is designed to support bleeding management in surgical and emergency settings, ensuring availability of critical antifibrinolytic therapy. This development highlights the growing importance of ready-to-use antifibrinolytics in operating rooms and acute care environments, while also strengthening supply reliability across healthcare facilities

- In June 2024, Avenacy, announced the U.S. launch of its FDA-approved Tranexamic Acid Injection, USP, a therapeutic generic version used to prevent or reduce bleeding in patients, particularly during dental procedures in hemophilia cases. The launch emphasizes increasing availability of cost-effective antifibrinolytic therapies and supports broader adoption in hospitals. This development reflects the rising focus on generic drug penetration to improve accessibility and affordability in bleeding management treatments

- In November 2023, Bio-Technology researchers (ASH publication) reported the discovery of a novel antifibrinolytic candidate, BT-114143, demonstrating potent inhibition of fibrinolysis with potential for improved efficacy over existing therapies. The compound showed promising preclinical results and was being prepared for clinical trial evaluation. This development highlights ongoing innovation in next-generation antifibrinolytics aimed at enhancing treatment outcomes and expanding therapeutic options beyond traditional agents such as tranexamic acid

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.