Global Antisense Oligonucleotide For Genetic And Rare Disorders Market

Market Size in USD Billion

USD

529.26 Billion

USD

1,563.55 Billion

2024

2032

USD

529.26 Billion

USD

1,563.55 Billion

2024

2032

Forecast Period |

2025 - 2032 |

Market Size (Base Year) |

USD 529.26 Billion |

Market Size (Forecast Year) |

USD 1,563.55 Billion |

CAGR |

% |

Major Markets Players |

|

Antisense Oligonucleotide for Genetic and Rare Disorders Market Size

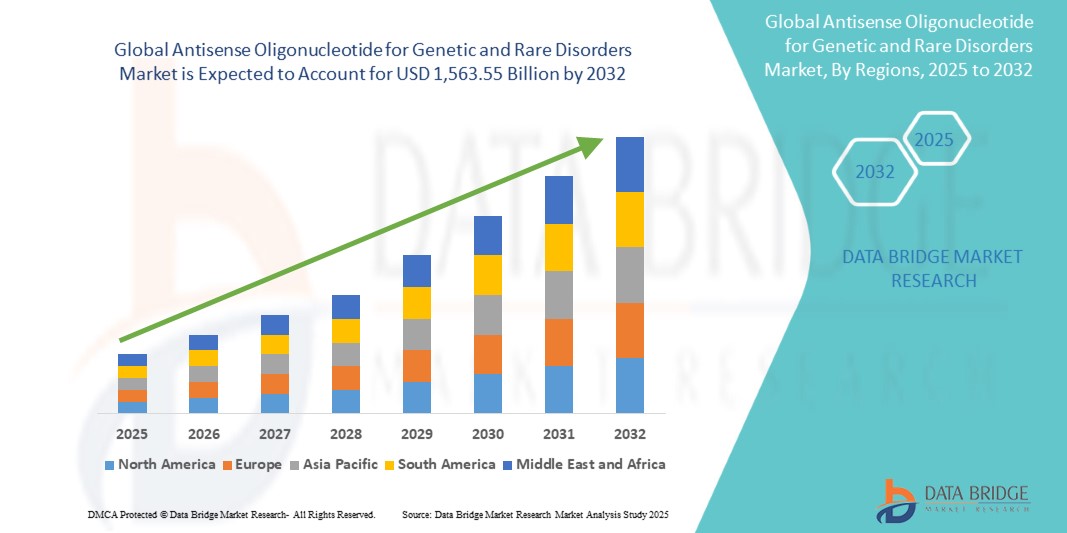

- The global antisense oligonucleotide for genetic and rare disorders market size was valued at USD 529.26 billion in 2024 and is expected to reach USD 1,563.55 billion by 2032, at a CAGR of 14.50% during the forecast period

- The market growth is largely fueled by the increasing adoption of antisense oligonucleotide (ASO) therapies for genetic and rare disorders, supported by advancements in precision medicine, targeted therapeutics, and molecular biology. Rising awareness of personalized treatment approaches and growing prevalence of rare genetic conditions are driving demand for ASO-based solutions

- Furthermore, increasing investments in research and development, coupled with technological progress in delivery systems, chemical modifications, and sequence design, are enabling more effective and safer ASO therapies. These factors are accelerating the uptake of antisense oligonucleotide treatments, thereby significantly boosting the overall growth of the market

Antisense Oligonucleotide for Genetic and Rare Disorders Market Analysis

- Antisense oligonucleotides (ASOs), offering targeted therapy for genetic and rare disorders, are increasingly vital components of modern precision medicine due to their ability to modulate gene expression, treat previously untreatable diseases, and integrate with personalized treatment plans

- The escalating demand for ASOs is primarily fueled by growing prevalence of rare and genetic disorders, increasing research and development activities, and rising awareness of gene-targeted therapies among healthcare providers and patients

- North America dominated the antisense oligonucleotide for genetic and rare disorders market with the largest revenue share of 43.2% in 2024, characterized by early adoption of advanced therapeutics, high healthcare expenditure, and a strong presence of key industry players, with the U.S. experiencing substantial growth in ASO treatments driven by innovations from both established pharmaceutical companies and biotech startups

- Asia-Pacific is expected to be the fastest-growing region in the antisense oligonucleotide for genetic and rare disorders market during the forecast period due to increasing healthcare infrastructure, rising disposable incomes, and growing investments in biotechnology and pharmaceutical research

- The Neurological Disorders segment dominated the antisense oligonucleotide for genetic and rare disorders market with the largest revenue share of 45% in 2024, supported by the growing prevalence of conditions such as spinal muscular atrophy, Huntington’s disease, and amyotrophic lateral sclerosis. These disorders have demonstrated strong responsiveness to ASO therapies, further driving adoption in clinical settings

Report Scope and Antisense Oligonucleotide for Genetic and Rare Disorders Market Segmentation

|

Attributes |

Antisense Oligonucleotide for Genetic and Rare Disorders Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Antisense Oligonucleotide for Genetic and Rare Disorders Market Trends

Enhanced Precision and Personalized Therapy Through AI and Advanced Analytics

- A significant and accelerating trend in the global antisense oligonucleotide (ASO) for genetic and rare disorders market is the deepening integration of artificial intelligence (AI) and advanced analytics into drug discovery, development, and patient management. This convergence is significantly enhancing the precision, efficiency, and personalization of ASO therapies

- AI-driven platforms are being utilized to design more effective antisense oligonucleotides by predicting optimal target sequences, improving binding affinity, and reducing off-target effects. For example, companies like Ionis Pharmaceuticals and Sarepta Therapeutics leverage AI algorithms to streamline the development of therapies for rare genetic conditions such as Duchenne muscular dystrophy and spinal muscular atrophy

- Advanced analytics and AI integration enable real-time monitoring of patient responses, allowing for data-driven adjustments to treatment regimens. This personalized approach helps maximize therapeutic outcomes while minimizing potential side effects. Some platforms can identify patterns in gene expression and suggest tailored ASO interventions for individual patients

- The combination of AI and big data also facilitates faster identification of potential candidates for clinical trials, optimizes dosing strategies, and predicts long-term efficacy, accelerating the overall development pipeline for rare disease therapies

- This trend towards intelligent, data-driven, and patient-centric ASO solutions is reshaping expectations for treatment of genetic and rare disorders. As a result, companies are increasingly focusing on AI-enabled design tools, predictive modeling, and real-world data integration to deliver safer and more effective therapies

- The demand for ASO therapies enhanced by AI and advanced analytics is growing rapidly across both developed and emerging markets, as healthcare providers and patients prioritize precision medicine, improved treatment outcomes, and individualized therapeutic strategies

Antisense Oligonucleotide for Genetic and Rare Disorders Market Dynamics

Driver

Rising Demand Driven by Advances in Genetic Therapeutics and Rare Disease Research

- The Asia-Pacific Antisense Oligonucleotide for Genetic and Rare Disorders market is witnessing strong growth, fueled by increasing prevalence of rare genetic disorders, rising awareness about personalized medicine, and the adoption of targeted genetic therapies. Patients and healthcare providers are seeking innovative solutions for conditions with limited treatment options, driving demand for antisense oligonucleotide (ASO) therapies

- In March 2024, Ionis Pharmaceuticals (U.S.) announced the expansion of its clinical trial pipeline for rare genetic disorders, incorporating novel antisense oligonucleotides aimed at neuromuscular and metabolic diseases. Such strategic initiatives by key companies are expected to significantly accelerate market growth during the forecast period

- Growing investments in research and development, coupled with government incentives for orphan drug programs, are enabling faster regulatory approvals and broader accessibility of ASO therapies. This is encouraging pharmaceutical and biotechnology companies to increase their focus on developing next-generation genetic therapies

- Advancements in delivery mechanisms—such as lipid nanoparticles, conjugates, and polymer-based carriers—are enhancing the efficacy and safety of antisense oligonucleotide therapies, further supporting adoption across neurological, cardiovascular, metabolic, and oncological indications

- The increasing emphasis on personalized medicine and patient-specific treatment strategies is driving collaborations between biotech firms, academic research institutions, and hospitals, fostering innovation in antisense oligonucleotide design, clinical trials, and patient monitoring

Restraint/Challenge

High Development Costs and Regulatory Complexities

- The development of antisense oligonucleotide therapies requires substantial investment in research, clinical trials, and specialized manufacturing processes, making the high cost of development a significant challenge for both new and established market players

- Regulatory complexities associated with rare disease therapies—including varying approval pathways across regions, stringent safety requirements, and long timelines for clinical validation—can delay product launches and affect market penetration

- Delivery challenges, such as ensuring tissue-specific targeting and minimizing off-target effects, add additional layers of technical complexity and cost, requiring advanced formulation strategies and extensive preclinical testing

- To overcome these challenges, leading companies are investing in platform technologies, strategic partnerships, and scalable manufacturing solutions to reduce development timelines, optimize costs, and facilitate regulatory compliance

- Initiatives such as early engagement with regulatory authorities and adoption of innovative clinical trial designs are helping mitigate risk and accelerate patient access to novel ASO therapies

Antisense Oligonucleotide for Genetic and Rare Disorders Market Scope

The market is segmented on the basis of type, delivery mechanism, mechanism of action, and application

• By Type

On the basis of type, the antisense oligonucleotide for genetic and rare disorders market is segmented into single-stranded oligonucleotides, double-stranded oligonucleotides, chemically modified oligonucleotides, gapmers, and others. The single-stranded oligonucleotides segment dominated the largest market revenue share of 42% in 2024, driven by their well-established effectiveness in targeting specific mRNA sequences for conditions such as Duchenne muscular dystrophy and spinal muscular atrophy. Their flexibility in design and ease of synthesis support strong adoption in both clinical trials and approved therapies.

The chemically modified oligonucleotides segment is anticipated to witness the fastest growth rate of 21% from 2025 to 2032, driven by innovations that enhance molecular stability, reduce off-target effects, and improve overall therapeutic efficacy. Chemical modifications, such as backbone, sugar, or base alterations, extend the in vivo half-life of oligonucleotides, enabling longer-lasting activity and more effective targeting of disease-related genes. These advancements are broadening the potential for treating complex genetic disorders, including rare inherited diseases and challenging conditions that were previously difficult to address with traditional nucleic acid therapies.

• By Delivery Mechanism

On the basis of delivery mechanism, the antisense oligonucleotide for genetic and rare disorders market is segmented into Lipid Nanoparticles, Conjugates, Viral Vectors, Polymer-Based Carriers, and Others. The Lipid Nanoparticles (LNPs) segment held the largest market revenue share of 39% in 2024, driven by their unique ability to protect oligonucleotides from enzymatic degradation during systemic delivery and facilitate efficient cellular uptake. LNPs are highly favored in both research and clinical applications due to their biocompatibility, low immunogenicity, and scalable manufacturing processes, making them ideal for large-scale therapeutic deployment. Their success in mRNA and ASO delivery has further validated their versatility and effectiveness in addressing complex genetic disorders.

The conjugates segment, including GalNAc-linked ASOs, is expected to register the fastest growth rate of 22% from 2025 to 2032, as these systems enable highly targeted delivery to specific tissues, such as the liver, thereby minimizing systemic exposure and potential side effects. Conjugate-based delivery enhances therapeutic safety, potency, and specificity, allowing lower dosing while achieving effective gene modulation. The growing adoption of conjugates is also fueled by advances in chemical linkage technologies, increasing clinical trial activity, and the expanding pipeline of ASO therapeutics targeting rare and genetic diseases, which require precise and controlled delivery for optimal efficacy.

• By Mechanism of Action

On the basis of mechanism of action, the antisense oligonucleotide for genetic and rare disorders market is segmented into RNase H-Mediated Degradation, Steric Blocking, RNA Interference, Splice Modulation, and Others. The RNase H-Mediated Degradation segment accounted for the largest market revenue share of 42% in 2024, driven by its well-established efficacy in selectively downregulating disease-causing mRNAs across a wide range of genetic disorders. This mechanism is widely adopted in both clinical and research applications due to its versatility, proven therapeutic outcomes, and applicability to multiple disease targets.

The splice modulation segment is projected to witness the fastest growth rate of 23% from 2025 to 2032, propelled by its unique ability to correct aberrant splicing events in conditions such as Duchenne muscular dystrophy and spinal muscular atrophy. Its highly targeted and personalized mode of action enables precise modulation of gene expression, making it an increasingly preferred approach in precision medicine and rare disease therapies.

• By Application

On the basis of application, the antisense oligonucleotide for genetic and rare disorders market is segmented into Neurological disorders, cardiovascular disorders, metabolic disorders, oncology, and other rare genetic disorders. The neurological disorders segment dominated the market with the largest revenue share of 45% in 2024, supported by the growing prevalence of conditions such as spinal muscular atrophy, Huntington’s disease, and amyotrophic lateral sclerosis. These disorders have demonstrated strong responsiveness to ASO therapies, further driving adoption in clinical settings.

The other rare genetic disorders segment is expected to register the fastest growth rate of 24% from 2025 to 2032, fueled by increasing investment in orphan drug development, favorable regulatory incentives, and an expanding focus on precision medicine approaches. The segment’s growth reflects the rising need for innovative therapies that can address previously untreatable genetic conditions, offering hope for highly targeted and effective treatment options.

Antisense Oligonucleotide for Genetic and Rare Disorders Market Regional Analysis

- North America dominated the antisense oligonucleotide for genetic and rare disorders market with the largest revenue share of 43.2% in 2024

- This strong position is characterized by early adoption of advanced therapeutics, high healthcare expenditure, and the presence of key pharmaceutical and biotechnology players. The U.S. accounted for the majority of regional revenue, driven by innovations from both established pharmaceutical companies and biotech startups focusing on rare genetic disorders

- Increasing clinical trials, growing awareness of personalized medicine, and favorable reimbursement policies are further boosting the uptake of ASO treatments across the region

U.S. Antisense Oligonucleotide for Genetic and Rare Disorders Market Insight

The U.S. antisense oligonucleotide for genetic and rare disorders market captured a substantial share of North America in 2024, fueled by rapid adoption of antisense oligonucleotide therapies for rare and genetic disorders. Advancements in delivery technologies, such as lipid nanoparticles and conjugates, and the development of novel therapies for neuromuscular, metabolic, and neurological disorders are driving market expansion. The country benefits from robust R&D infrastructure, strong private and public investments in biotech, and a growing pipeline of ASO treatments in clinical trials.

Europe Antisense Oligonucleotide for Genetic and Rare Disorders Market Insight

The Europe antisense oligonucleotide for genetic and rare disorders market is witnessing steady growth, supported by well-established healthcare infrastructure, rising government initiatives for rare diseases, and substantial R&D investments in biotechnology. Germany led the European market with a revenue share of 34.2% in 2024, fueled by its advanced pharmaceutical manufacturing infrastructure and strong regulatory frameworks that facilitate large-scale production of ASO intermediates. The U.K. is projected to register the fastest CAGR of 10.8%, driven by NHS-supported R&D programs, increasing investments in synthetic and biotech molecules, and growing demand for high-quality intermediates for both domestic and export-oriented pharmaceutical production.

Germany Antisense Oligonucleotide for Genetic and Rare Disorders Market Insight

The Germany antisense oligonucleotide for genetic and rare disorders market continues to hold a leadership position in Europe with a substantial share in 2024. This dominance is underpinned by Germany’s robust pharmaceutical manufacturing infrastructure, which supports large-scale production of high-quality antisense oligonucleotide (ASO) intermediates and finished therapies. The country is at the forefront of adopting advanced synthetic and biotech technologies, enabling precise, efficient, and scalable development of ASO treatments. Continuous investment in clinical research programs, alongside strategic collaborations between leading biotech firms, pharmaceutical companies, and academic institutions, is fostering innovation and accelerating the commercialization of novel antisense oligonucleotide therapies. Furthermore, Germany’s favorable regulatory environment facilitates streamlined approval pathways and compliance, providing an enabling ecosystem for both domestic and export-oriented ASO production.

U.K. Antisense Oligonucleotide for Genetic and Rare Disorders Market Insight

The U.K. antisense oligonucleotide for genetic and rare disorders market is expected to register a notable CAGR over the forecast period, reflecting strong growth prospects. This expansion is fueled by NHS-supported research and development initiatives aimed at rare genetic disorders, as well as increasing private and public investments in biotechnology and pharmaceutical innovation. The country is witnessing a rapidly growing pipeline of antisense oligonucleotide therapies targeting neuromuscular, metabolic, and neurological disorders, which is accelerating adoption in hospitals, research centers, and specialized treatment facilities. Additionally, the U.K.’s emphasis on fostering collaboration between biotech startups, academic institutions, and large pharmaceutical companies is driving technological advancements, enabling the development of more effective, targeted, and commercially viable ASO therapies for the European market.

Asia-Pacific Antisense Oligonucleotide for Genetic and Rare Disorders Market Insight

The Asia-Pacific antisense oligonucleotide for genetic and rare disorders market is expected to be the fastest-growing region in the Antisense Oligonucleotide for Genetic and Rare Disorders market during the forecast period. Growth is supported by increasing healthcare infrastructure, rising disposable incomes, and significant investments in biotechnology and pharmaceutical research. Countries such as China, Japan, and India are witnessing accelerated adoption of ASO therapies, driven by expanding clinical trial programs, government incentives for rare disease research, and improvements in manufacturing capabilities. China held the largest market revenue share in the region in 2024, supported by strong domestic pharmaceutical production, growing awareness of genetic therapies, and rising accessibility of advanced ASO treatments.

Japan Antisense Oligonucleotide for Genetic and Rare Disorders Market Insight:

The Japan antisense oligonucleotide for genetic and rare disorders market is steadily gaining momentum, driven by the country’s rapid advancements in biotechnology and substantial healthcare expenditure. Government initiatives supporting rare disease research and innovation are further propelling the development and adoption of antisense oligonucleotide (ASO) therapies. The increasing prevalence of genetic disorders, coupled with Japan’s aging population, is intensifying the demand for targeted and personalized ASO treatments across both clinical and research settings. Additionally, Japan’s well-established network of hospitals, research institutes, and biotechnology firms is facilitating efficient clinical trials, advanced therapeutic development, and the integration of ASO therapies into routine patient care, positioning the market for sustained growth in the coming years.

China Antisense Oligonucleotide for Genetic and Rare Disorders Market Insight:

The China antisense oligonucleotide for genetic and rare disorders market captured the largest share in the Asia-Pacific region in 2024, driven by a rapidly expanding middle-class population, increasing investments in pharmaceutical and biotechnology research, and robust government support for rare disease therapies. The country’s growing biotechnology sector, supported by domestic manufacturing capabilities, is enabling broader accessibility and faster distribution of antisense oligonucleotide treatments across hospitals, research institutions, and specialized care centers. Furthermore, the integration of advanced manufacturing technologies and strategic collaborations between local and international pharmaceutical companies is enhancing the production, quality, and affordability of ASO therapies, fueling China’s leadership in the regional market and supporting its role as a key hub for innovative rare disease therapeutics.

Antisense Oligonucleotide for Genetic and Rare Disorders Market Share

The antisense oligonucleotide for genetic and rare disorders industry is primarily led by well-established companies, including:

- Ionis Pharmaceuticals (U.S.)

- Sarepta Therapeutics (U.S.)

- Wave Life Sciences (U.S.)

- Biogen Inc. (U.S.)

- Stoke Therapeutics (U.S.)

- Regulus Therapeutics (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- GSK PLC (U.K.)

- Alnylam Pharmaceuticals (U.S.)

- ProQR Therapeutics (Netherlands)

- Cold Spring Harbor Laboratory (U.S.)

- Avidity Biosciences (U.S.)

- Arbutus Biopharma (Canada)

- SKIP Therapeutics (U.S.)

- Vico Therapeutics (Netherlands)

- EveryONE Medicines (U.S.)

- Secarna Pharmaceuticals (Germany)

- SpliSense (Israel)

- Arcturus Therapeutics (U.S.)

Latest Developments in Global Antisense Oligonucleotide for Genetic and Rare Disorders Market

- In February 2021, Sarepta Therapeutics received FDA approval for Amondys 45 (casimersen), an antisense oligonucleotide designed to treat Duchenne muscular dystrophy (DMD) in patients with a specific mutation amenable to exon 45 skipping. This marked a significant advancement in precision medicine for rare genetic disorders

- In December 2023, Ionis Pharmaceuticals and AstraZeneca announced the FDA approval of Eplontersen (Wainua), an antisense oligonucleotide therapy for hereditary transthyretin-mediated amyloidosis. This approval underscored the growing role of ASOs in treating complex genetic diseases

- In December 2024, Olezarsen (Tryngolza), an antisense oligonucleotide targeting apolipoprotein C-III, was approved by the FDA for the treatment of familial chylomicronemia syndrome. This first-in-class medication highlighted the expanding therapeutic applications of ASOs

- In June 2025 EveryONE Medicines, a Boston-based biotech startup, announced its initiative to develop personalized antisense oligonucleotide therapies for ultra-rare genetic disorders. This approach aims to accelerate drug development timelines and provide tailored treatments for individual patients

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.