Global Antivenom Drugs Market

Market Size in USD Billion

USD

1.13 Billion

USD

1.60 Billion

2025

2033

USD

1.13 Billion

USD

1.60 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.13 Billion | |

| USD 1.60 Billion | |

| % | |

|

Antivenom Drugs Market Overview

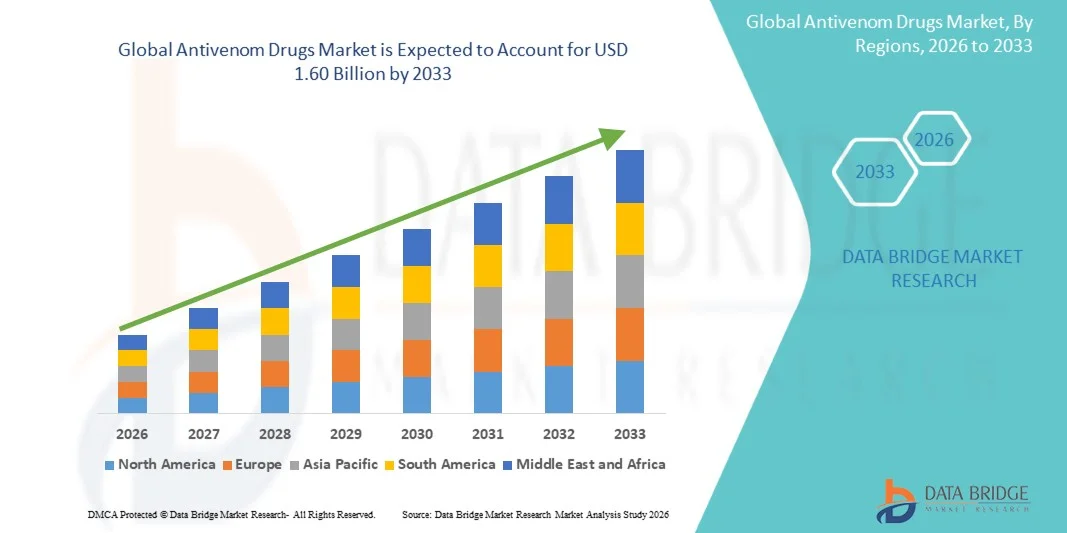

The Antivenom Drugs Market was valued at USD 1.13 billion in 2025 and is projected to reach USD 1.60 billion by 2033, growing at a CAGR of 4.50% from 2026 to 2033. The Antivenom Drugs market is experiencing steady growth driven by the increasing incidence of venomous animal bites and rising public health awareness regarding timely and effective treatment of envenomation cases. Growing prevalence of snakebites, scorpion stings, and spider bites—particularly in tropical and rural regions across Asia-Pacific, Africa, and Latin America—is significantly increasing demand for life-saving antivenom therapies. Governments and healthcare organizations are strengthening emergency care infrastructure and stockpiling antivenom products in high-risk regions to reduce mortality rates associated with envenomation.

In addition, advancements in biotechnology and plasma fractionation techniques are improving the safety, efficacy, and specificity of antivenom formulations. The development of recombinant and monoclonal antibody-based antivenoms is reducing adverse reactions compared to traditional equine-derived products. Expanding access to hospital emergency care, improved distribution networks, and increased inclusion of antivenoms in essential medicines lists by global health authorities are further supporting market growth. Rising investments in public health programs, particularly in endemic regions, are also accelerating adoption of antivenom therapies for rapid and effective treatment outcomes.

Key Market Trends & Insights

- North America dominated the Antivenom Drugs Market with the largest revenue share of 33.84% in 2025, supported by strong hospital infrastructure, advanced emergency care systems, and well-established government procurement programs for critical antivenom stockpiles and toxicology treatment protocols.

- The Snakes segment dominated the market with a share of 63% in 2025, due to the high global incidence of snakebite envenomation, particularly in Asia-Pacific and Africa. Snakebites account for the majority of envenomation-related mortality cases worldwide.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by high incidence of snakebite cases, expanding rural healthcare access, government-supported antivenom distribution programs, and increasing investment in emergency medical infrastructure across India, China, and Southeast Asia.

- Snake segment dominated the market with a 73.12% revenue share in 2025, due to the high global burden of snakebite envenomation, particularly in agricultural regions and tropical countries with limited immediate access to emergency care.

- The Neurotoxic antivenom segment accounted for the largest share of 35.64% in 2025, driven by the prevalence of highly venomous neurotoxic species such as cobras and kraits, especially across Asia-Pacific regions.

Market Size & Forecast

- Global Market Value (2025): USD 1.13 Billion

- Expected Market Value (2033): USD 1.60 Billion

- Forecast CAGR (2026–2033): 4.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Antivenom Drugs Market Segmentation

|

Attributes |

Antivenom Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• CSL Limited (Australia) |

|

Market Opportunities |

· Expansion of Antivenom Access in High-Burden Regions · Development of Recombinant and Next-Generation Antivenoms · Public Health Initiatives and Strategic Antivenom Stockpiling Programs |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Antivenom Drugs Market Trends

Trend: Increasing Focus on Snakebite Envenomation Management and Rapid Response Antivenom Deployment

The Antivenom Drugs Market is witnessing a strong shift toward improving rapid access to life-saving antivenom therapies, particularly in rural and high-risk regions where venomous snakebites are most prevalent. According to the World Health Organization (WHO), snakebite envenomation affects approximately 1.8–2.7 million people annually, resulting in up to 138,000 deaths per year, with millions more suffering long-term disabilities such as amputations and neurological complications.

To address this burden, governments in countries such as India, Brazil, and several Sub-Saharan African nations are expanding national antivenom stockpiling programs, improving cold-chain distribution systems, and increasing rural hospital preparedness. Hospitals are increasingly adopting polyvalent antivenoms as first-line treatment to ensure rapid intervention when the venomous species is unknown. In addition, improvements in toxin mapping and venom profiling technologies are helping manufacturers develop more effective and region-specific antivenoms.

Antivenom Drugs Market Dynamics

Key Market Driver: Rising Global Burden of Venomous Animal Bites and Improved Emergency Care Infrastructure

The primary driver of the antivenom drugs market is the growing incidence of venomous animal bites, particularly snakebites in tropical and subtropical regions. WHO classifies snakebite envenomation as a neglected tropical disease, with the highest burden observed in Asia-Pacific and Sub-Saharan Africa.

India alone reports over 50,000 snakebite deaths annually (estimated burden range varies by study), making it one of the most affected countries globally. Increasing agricultural activity, deforestation, and rural population exposure are major contributing factors. In response, healthcare systems are strengthening emergency care infrastructure, expanding access to intensive care units (ICUs), and improving physician training in toxinology. Pharmaceutical companies and public health agencies are also investing in improved plasma-derived and immunoglobulin-based antivenoms, enhancing treatment efficacy and survival rates.

Key Restraint/Challenge: High Production Complexity and Limited Antivenom Availability

A major challenge in the antivenom market is the complex and costly production process, which involves venom extraction, immunization of horses or other host animals, plasma purification, and strict quality control. These processes make manufacturing expensive and limit the number of global suppliers.

In addition, species-specific antivenom limitations often require region-specific production, which reduces scalability. Many low-income countries face frequent shortages due to weak cold-chain infrastructure, inconsistent procurement systems, and reliance on imports. Adverse reactions such as serum sickness and allergic responses also require careful clinical monitoring, increasing treatment complexity.

Key Market Opportunity: Development of Recombinant and Next-Generation Antivenoms

The market presents significant opportunities through the development of recombinant antivenoms and monoclonal antibody-based therapies, which aim to replace traditional animal-derived products. Research supported by organizations such as the World Health Organization (WHO) and global toxinology institutes is focusing on designing broad-spectrum antivenoms that can neutralize multiple venom toxins more safely and effectively.

Advancements in proteomics and venom characterization are enabling region-specific precision antivenom design, while biotechnology firms are exploring synthetic antibody platforms to reduce immunogenic side effects. Increasing funding for neglected tropical disease programs and government-led initiatives in countries like India, Mexico, and Brazil are expected to significantly improve accessibility and affordability of antivenom therapies over the coming years.

Antivenom Drugs Market Scope

The Antivenom Drugs market is segmented on the basis of Type, Treatment, Animal, Mode of Action, End User, and Distribution Channel.

- By Type

On the basis of type, the Antivenom Drugs Market is segmented into Monovalent Antivenom and Polyvalent Antivenom. The Monovalent Antivenom segment dominated the market with a share of 54.12% in 2025, owing to its high specificity, targeted action against single venom species, and improved clinical effectiveness in region-specific envenomation cases. These antivenoms are widely used in areas with well-identified snake species distribution, enabling faster neutralization and reduced adverse reactions. Hospitals in rural and tropical regions increasingly rely on monovalent formulations for emergency care due to their precision and lower dosage requirements. Government health programs in Asia-Pacific and Africa are further strengthening availability in endemic zones. In addition, improved cold-chain logistics and public health procurement initiatives are supporting broader adoption. However, limited applicability across multiple venom types restricts their universal usage. Increasing clinical preference for species-specific treatment protocols continues to drive segment demand. Pharmaceutical companies are investing in refining antibody purification techniques to improve efficacy and safety profiles. The segment also benefits from growing awareness programs on snakebite management. Overall, monovalent antivenoms remain critical in targeted treatment strategies across endemic regions.

The Polyvalent Antivenom segment is expected to witness the fastest growth with a CAGR of 6.8% from 2026 to 2033, driven by increasing demand in regions where multiple venomous species coexist and species identification is difficult during emergencies. These broad-spectrum antivenoms provide rapid treatment without requiring precise identification of the biting organism, making them highly suitable for rural and emergency care settings. Rising snakebite incidence in tropical countries is significantly boosting adoption. Hospitals are increasingly stocking polyvalent formulations for emergency preparedness. Improvements in antibody engineering are enhancing cross-neutralization efficiency. Government healthcare programs are prioritizing polyvalent antivenoms due to their versatility. Expanding emergency healthcare infrastructure in emerging economies is further supporting demand. Increasing WHO initiatives for snakebite management are accelerating procurement. Cost-effectiveness compared to multiple monovalent doses is also a key factor. Growing clinical preference for rapid-response treatment is strengthening adoption. Overall, polyvalent antivenoms are expected to dominate future emergency treatment strategies.

- By Treatment

On the basis of treatment, the Antivenom Drugs Market is segmented into Vaccines and Hyper Immune Serums. The Hyper Immune Serums segment dominated the market with a share of 72.45% in 2025, due to their direct neutralization capability against circulating venoms and established clinical effectiveness in acute envenomation cases. These serums are widely used in emergency hospital settings where rapid toxin neutralization is critical. Equine-derived immunoglobulin therapies remain the most common form due to large-scale production capabilities. Increasing hospital admissions for snakebite cases in rural regions is supporting demand. Improved purification and fractionation techniques are reducing adverse immune reactions. Government-supported production facilities in emerging economies are enhancing supply availability. Rising investments in plasma-derived therapies are strengthening manufacturing capacity. Clinical guidelines continue to recommend hyperimmune serums as first-line treatment. Expanding distribution networks in endemic regions are improving accessibility. Overall, hyperimmune therapies remain the backbone of antivenom treatment protocols globally.

The Vaccines segment is expected to witness the fastest growth with a CAGR of 7.2% from 2026 to 2033, driven by increasing research into preventive immunization approaches for high-risk populations. Although still in early stages, venom-based vaccine development is gaining momentum in biotechnology research. Rising focus on preventive healthcare strategies is supporting innovation. Academic and clinical collaborations are exploring recombinant venom antigens. Government funding for neglected tropical diseases is accelerating research activity. Advances in molecular biology are enabling safer vaccine candidates. Increasing awareness in endemic regions is driving preventive healthcare demand. Long-term goal of reducing snakebite mortality is supporting investment. Pharmaceutical companies are expanding R&D pipelines in immunization technologies. Growing interest in prophylactic protection for high-risk workers is emerging. Overall, venom vaccines represent a high-potential future segment in antivenom therapeutics.

- By Animal

On the basis of animal type, the Antivenom Drugs Market is segmented into Snakes, Spiders, Scorpions, and Others. The Snakes segment dominated the market with a share of 78.63% in 2025, due to the high global incidence of snakebite envenomation, particularly in Asia-Pacific and Africa. Snakebites account for the majority of envenomation-related mortality cases worldwide. Widely distributed venomous species such as cobras, vipers, and kraits drive strong demand for antivenom products. Government health agencies maintain dedicated snakebite treatment programs in endemic countries. Increased rural exposure and agricultural activities further contribute to cases. Hospitals prioritize stocking snake-specific antivenoms due to high emergency admission rates. WHO classification of snakebite as a neglected tropical disease is improving funding allocation. Awareness campaigns are increasing early treatment seeking behavior. Improvements in diagnostic protocols are enhancing treatment outcomes. Overall, snake envenomation remains the dominant clinical indication globally.

The Scorpions segment is expected to witness the fastest growth with a CAGR of 6.5% from 2026 to 2033, driven by rising incidence of scorpion stings in Middle Eastern, African, and Latin American regions. Increasing urban expansion into desert and semi-arid ecosystems is raising exposure risk. Pediatric cases are significantly contributing to treatment demand. Hospitals are increasing procurement of scorpion-specific antivenoms. Improved clinical awareness is reducing mortality rates but increasing diagnosis rates. Government emergency response systems are strengthening distribution networks. Pharmaceutical companies are expanding regional antivenom production. Climate change-related habitat shifts are increasing scorpion-human interaction. Emergency healthcare infrastructure expansion is improving treatment access. Rising rural healthcare investments are supporting growth. Overall, scorpion antivenoms are gaining importance in regional emergency medicine.

- By Mode of Action

On the basis of mode of action, the Antivenom Drugs Market is segmented into Cytotoxic, Neurotoxic, Haemotoxic, Cardiotoxic, Myotoxic, and Others. The Neurotoxic segment dominated the market with a share of 36.84% in 2025, due to the high prevalence of neurotoxic snake species such as cobras and kraits, particularly in Asia. Neurotoxic venoms affect the nervous system rapidly, requiring immediate antivenom administration. High mortality rates associated with respiratory paralysis drive urgent treatment demand. Hospitals prioritize neurotoxic antivenoms in emergency care units. Clinical guidelines emphasize early intervention for neurotoxic bites. Increasing rural healthcare access is improving survival outcomes. Government procurement programs focus heavily on neurotoxic antivenoms. Advancements in antibody formulation are improving reversal of neurotoxic effects. Rising awareness among healthcare workers is improving diagnosis speed. Overall, neurotoxic antivenoms remain the most critical life-saving segment.

The Haemotoxic segment is expected to witness the fastest growth with a CAGR of 6.9% from 2026 to 2033, driven by increasing cases of venom-induced coagulopathy and internal bleeding complications. Haemotoxic bites are commonly associated with vipers, which are widely distributed across multiple regions. Improved diagnostic capabilities are increasing detection rates. Hospitals are adopting rapid coagulation monitoring systems. Growing clinical focus on clotting disorders is supporting demand. Emergency care protocols are expanding haemotoxic treatment coverage. Rising rural exposure is increasing case incidence. Government healthcare programs are strengthening availability in endemic zones. Advancements in antivenom purification are improving efficacy. Increased research into clotting pathway neutralization is accelerating innovation. Overall, haemotoxic antivenoms are gaining rapid clinical importance.

- By End User

On the basis of end user, the Antivenom Drugs Market is segmented into Hospital/Clinical Laboratories, Physician Offices, Reference Laboratories, and Other End Users. The Hospital/Clinical Laboratories segment dominated the market with a share of 64.29% in 2025, due to the high volume of emergency envenomation cases treated in hospital settings. Hospitals serve as the primary point of care for snakebite and scorpion sting management. Availability of critical care infrastructure enables rapid administration of antivenom therapy. Increasing emergency admissions in rural and semi-urban hospitals is driving demand. Government funding for public hospitals is strengthening treatment capacity. Expansion of emergency medicine departments is improving response time. Clinical laboratories support diagnostic confirmation of venom type. Rising healthcare infrastructure investments in developing regions are boosting access. Standardized treatment protocols are widely implemented in hospitals. Overall, hospitals remain the central hub for antivenom administration globally.

The Reference Laboratories segment is expected to witness the fastest growth with a CAGR of 6.7% from 2026 to 2033, driven by increasing demand for accurate venom identification and diagnostic confirmation. Advanced immunoassay and molecular diagnostic techniques are improving testing precision. Rising need for species-specific treatment guidance is supporting laboratory utilization. Expansion of diagnostic networks in emerging economies is accelerating growth. Government initiatives for venom surveillance are strengthening laboratory infrastructure. Increased research into regional venom variations is driving demand. Clinical collaborations with research institutions are expanding. Improvements in laboratory automation are enhancing efficiency. Growing focus on personalized treatment approaches is supporting adoption. Overall, reference laboratories are becoming critical for precision antivenom therapy.

- By Distribution Channel

On the basis of distribution channel, the Antivenom Drugs Market is segmented into Direct Tender, Retail Sales, and Other Channels. The Direct Tender segment dominated the market with a share of 61.38% in 2025, due to large-scale procurement by governments, public hospitals, and international health organizations. Centralized purchasing ensures cost-effective supply of antivenom in high-burden regions. National healthcare programs heavily rely on tender-based distribution systems. WHO-supported initiatives are strengthening procurement mechanisms. Bulk purchasing improves affordability and accessibility in rural areas. Emergency preparedness programs maintain strategic stockpiles. Public healthcare systems prioritize direct supplier agreements. Increasing government focus on snakebite mortality reduction is supporting demand. Stable supply contracts with manufacturers ensure consistent availability. Overall, direct tender remains the backbone of global distribution systems.

The Retail Sales segment is expected to witness the fastest growth with a CAGR of 6.6% from 2026 to 2033, driven by expanding private healthcare access and improving pharmaceutical retail networks in emerging economies. Increasing availability of antivenoms in private pharmacies is enhancing accessibility. Growing awareness of emergency treatment is driving demand in retail settings. Expansion of rural pharmacy networks is improving drug availability. Rising private healthcare spending is supporting market growth. Improved cold-chain logistics are enabling wider distribution. Pharmaceutical companies are expanding retail partnerships. Government policies supporting decentralized healthcare access are boosting sales. Increasing emergency preparedness in remote areas is contributing to demand. Overall, retail channels are becoming increasingly important for last-mile accessibility.

Antivenom Drugs Market Regional Analysis

The North America Antivenom Drugs market accounted for the largest revenue share of 33.84% in 2025, driven by strong hospital infrastructure, advanced emergency care systems, and well-established toxicology treatment protocols. The region benefits from efficient emergency response networks, high availability of hospital-based antivenom stockpiles, and robust government-supported procurement systems for critical care medicines. Increasing incidences of venomous animal exposures, particularly snake and spider bites in certain regions of the U.S., along with rapid access to intensive care units and poison control centers, continue to support market dominance.

U.S. Antivenom Drugs Market Insight

The U.S. Antivenom Drugs market is witnessing steady growth due to strong clinical infrastructure, widespread availability of FDA-approved antivenoms, and the presence of specialized poison control centers. Hospitals across rural and urban areas maintain strategic antivenom inventories to manage emergency cases involving snakebites and other envenomations. In addition, increasing awareness programs and rapid emergency response systems are improving patient survival rates and supporting demand for antivenom therapies.

Europe Antivenom Drugs Market Insight

The Europe Antivenom Drugs market holds a significant share of global revenue, supported by advanced healthcare systems, strong regulatory frameworks, and coordinated emergency medical services. Countries across the region maintain structured toxicology treatment protocols and centralized poison information services, ensuring timely administration of antivenom therapies. Rising cases of imported venomous species exposures and occupational risks in rural and agricultural areas further contribute to steady market growth.

U.K. Antivenom Drugs Market Insight

The U.K. Antivenom Drugs market is growing steadily, supported by the National Health Service (NHS), which ensures centralized access to critical care medicines including antivenoms. Specialist toxicology units and poison information services play a key role in managing envenomation cases. Increasing awareness among healthcare professionals and continuous updates in clinical treatment guidelines are improving response times and treatment outcomes.

Germany Antivenom Drugs Market Insight

The Germany Antivenom Drugs market is expanding due to strong hospital infrastructure, advanced emergency care capabilities, and efficient pharmaceutical distribution networks. The country maintains well-developed clinical toxicology services and emergency protocols for managing snakebite and arthropod envenomation cases. Continuous investment in hospital preparedness and critical care medicine availability further supports market stability.

Asia-Pacific Antivenom Drugs Market Insight

The Asia-Pacific Antivenom Drugs market is expected to be the fastest-growing region, with a CAGR of 7.6% from 2026 to 2033, driven by high incidence of snakebite cases, expanding rural healthcare infrastructure, and government-supported antivenom distribution programs. Countries such as India, China, Bangladesh, and Indonesia face significant public health burdens from venomous bites, increasing demand for affordable and widely accessible antivenom therapies. Expanding emergency care systems and improving healthcare access in rural regions are further accelerating regional market growth.

Japan Antivenom Drugs Market Insight

The Japan Antivenom Drugs market is witnessing stable growth, supported by advanced healthcare infrastructure, strong emergency medical response systems, and low but well-managed incidence of venomous bites. The country maintains highly regulated clinical protocols and ensures rapid access to antivenom treatments in hospital settings. Continuous improvements in emergency medicine and toxicology care contribute to consistent market performance.

China Antivenom Drugs Market Insight

The China Antivenom Drugs market is growing steadily due to increasing rural healthcare expansion, rising awareness of snakebite management, and government-led initiatives to improve emergency medical access. Large rural populations in certain provinces face higher exposure risks to venomous animals, driving demand for antivenom availability in regional hospitals. Strengthening of healthcare infrastructure and expansion of emergency response networks are further supporting market growth across the country.

Antivenom Drugs Market Share

The Antivenom Drugs industry is primarily led by well-established companies, including:

- CSL Limited (Australia)

- Sanofi (France)

- Serum Institute of India Pvt. Ltd. (India)

- Merck KGaA (Germany)

- Pfizer Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Grifols S.A. (Spain)

- Bioclon Institute (Mexico)

- Instituto Clodomiro Picado (Costa Rica)

- Instituto Butantan (Brazil)

- Bharat Serums and Vaccines Limited (India)

- Haffkine Bio-Pharmaceutical Corporation Ltd. (India)

- Vins Bioproducts Ltd. (India)

- Incepta Pharmaceuticals Ltd. (Bangladesh)

- BTG Specialty Pharmaceuticals (UK)

- MicroPharm Ltd. (UK)

- Pfizer Animal Health / Zoetis Inc. (U.S.)

- Emergent BioSolutions Inc. (U.S.)

- Sanofi Pasteur (France)

- Bayer AG (Germany)

- Kedrion Biopharma (Italy)

- Kamada Ltd. (Israel)

Latest Developments in Antivenom Drugs Market

- In April 2021, Rare Disease Therapeutics, Inc. announced FDA approval for the expanded indication of its equine-derived antivenom ANAVIP. The updated formulation broadened its coverage to include additional North American pit viper species such as rattlesnakes and copperheads, improving clinical effectiveness for multi-species envenomation cases and enhancing treatment duration due to its extended half-life

- In September 2021, the World Health Organization (WHO) continued strengthening its Snakebite Envenoming Strategy, expanding global coordination efforts to improve access to safe and effective antivenoms in high-burden regions such as Sub-Saharan Africa and South Asia. The initiative emphasized quality control reforms, improved regulatory oversight, and scaling up production of WHO-prequalified antivenom products to address global shortages and inconsistent product efficacy

- In May 2022, international public health programs under WHO-supported initiatives intensified antivenom accessibility projects in Asia and Africa, focusing on strengthening rural healthcare supply chains and improving emergency treatment protocols for snakebite management. These efforts aimed to reduce mortality rates by improving timely administration of antivenom in primary healthcare centers and district hospitals

- In March 2023, researchers and biotechnology companies advanced recombinant and monoclonal antibody-based antivenom development, shifting away from traditional horse-serum production methods. These next-generation approaches focused on improving safety profiles, reducing allergic reactions, and expanding cross-species venom neutralization capabilities, marking a significant innovation trend in antivenom therapeutics

- In June 2024, global health agencies and pharmaceutical developers increased clinical research efforts on broad-spectrum and recombinant antivenom therapies, including nanobody-based treatments capable of targeting multiple snake species. These innovations demonstrated improved stability and broader venom coverage, particularly for African elapid species, representing a major step toward next-generation universal antivenom solutions

- In October 2024, ongoing WHO-led regulatory strengthening programs emphasized the need for improved quality control frameworks for antivenom manufacturing and distribution. Several countries updated national guidelines to enhance production standards, improve cold-chain logistics, and ensure better access to antivenom in rural and high-risk regions, particularly across Asia-Pacific

- In February 2025, breakthrough research in human-derived antibody antivenom development gained momentum, with experimental therapies showing potential for broad protection against multiple venomous snake species. These developments are part of a growing global trend toward “universal antivenom” research aimed at overcoming limitations of species-specific treatments and improving affordability and scalability

- In May 2025, WHO-aligned global health discussions highlighted snakebite envenoming as a continued neglected tropical disease priority, reinforcing funding and innovation pipelines for next-generation antivenoms. Focus areas included recombinant antivenoms, synthetic antibodies, and improved regional manufacturing capacity to reduce dependency on imports in high-burden countries

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.