Global Anxiety Disorder Market

Market Size in USD Million

USD

13.37 Million

USD

19.75 Million

2025

2033

USD

13.37 Million

USD

19.75 Million

2025

2033

| 2026 - 2033 | |

| USD 13.37 Million | |

| USD 19.75 Million | |

| % | |

|

Anxiety Disorder Market Overview

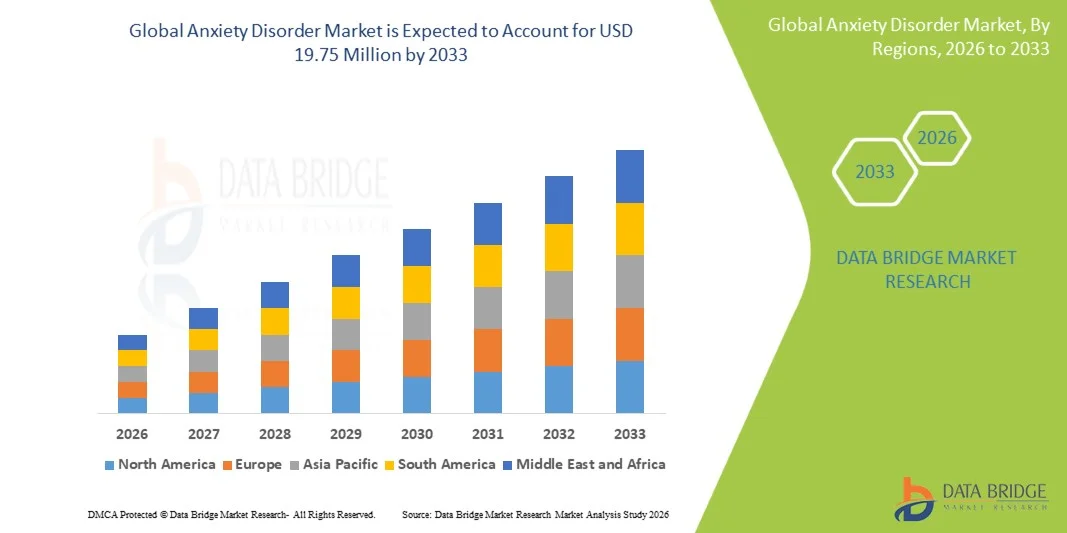

The Anxiety Disorder Market was valued at USD 13.37 Million in 2025 and is projected to reach USD 19.75 Million by 2033, growing at a CAGR of 5.00% from 2026 to 2033. The Anxiety Disorder Market is experiencing consistent growth driven by the rising prevalence of anxiety disorders worldwide, increasing awareness of mental health conditions, and expanding access to psychological and pharmacological treatments. Growing stress levels due to urbanization, workload pressure, social media influence, and changing lifestyles are significantly contributing to the increasing incidence of generalized anxiety disorder (GAD), panic disorder, and social anxiety disorder across all age groups.

The increasing recognition of mental health as a critical component of overall healthcare, combined with improved diagnosis rates and reduced stigma, is encouraging more patients to seek treatment. Healthcare providers, psychiatric clinics, and telehealth platforms are increasingly adopting evidence-based therapies, including cognitive behavioral therapy (CBT), antidepressants, and anxiolytic medications, to manage anxiety disorders effectively

Key Market Trends & Insights

- North America dominated the Anxiety Disorder Market with the largest revenue share of 6% in 2025, supported by high prevalence of anxiety disorders, advanced mental healthcare infrastructure, strong access to psychiatric services, and widespread adoption of pharmacological and psychotherapy-based treatments. The region also benefits from favorable reimbursement systems, high mental health awareness, and growing integration of digital mental health platforms such as telepsychiatry and AI-based therapy tools.

- The oral segment dominated the market with approximately 91.2% share in 2025, due to widespread use of oral antidepressants and anxiolytics as first-line therapy.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 3% from 2026 to 2033, fueled by increasing awareness of mental health conditions, rising healthcare expenditure, expanding psychiatric care infrastructure, and improving access to diagnosis and treatment in countries such as China, India, and Japan. Government initiatives to reduce mental health stigma and expand behavioral healthcare services are further accelerating regional growth.

- The Medications segment dominated the treatment category with 55.4% revenue share in 2025, supported by widespread use of SSRIs, SNRIs, benzodiazepines, and other anxiolytic drugs as first-line treatment options. Increasing prescription rates and improved access to psychiatric medications continue to drive segment leadership.

- The Outpatient segment led the patient category with share in 2025, due to the preference for long-term management of anxiety disorders through outpatient psychiatric consultations, therapy sessions, and medication management rather than inpatient hospitalization.

- The Oral route of administration segment dominated the market with share in 2025, driven by the widespread use of oral antidepressants and anxiolytic medications, which remain the most convenient and commonly prescribed treatment form.

- The Specialty Clinics segment dominated the end-user category with revenue share in 2025, supported by increasing availability of dedicated mental health clinics offering counseling, psychotherapy, and structured anxiety disorder management programs.

Market Size & Forecast

- Global Market Value (2025): USD 13.37 Million

- Expected Market Value (2033): USD 19.75 Million

- Forecast CAGR (2026–2033): 5.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Anxiety Disorder Market Segmentation

|

Attributes |

Anxiety Disorder Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Pfizer Inc. (U.S.) |

|

Market Opportunities |

· Expansion of Digital Mental Health and Telepsychiatry Platforms · Growing Demand for Novel and Personalized Pharmacological Therapies · Rising Awareness and Early Diagnosis of Mental Health Disorders |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Anxiety Disorder Market Trends

Trend: Rising Integration of Digital Mental Health Solutions and Expanding Access to Behavioral Therapy

The Anxiety Disorder Market is witnessing a strong shift toward digital mental health platforms, telepsychiatry, and AI-enabled behavioral therapy solutions, driven by increasing prevalence of anxiety disorders and growing demand for accessible, stigma-free treatment options. Anxiety disorders—including generalized anxiety disorder, panic disorder, social anxiety disorder, and phobias—are among the most common mental health conditions globally, affecting an estimated hundreds of millions of individuals worldwide, according to global psychiatric health assessments. The adoption of Cognitive Behavioral Therapy (CBT) delivered through digital platforms and mobile applications is increasing significantly, particularly in urban populations where stress, work pressure, and lifestyle changes are major contributors to mental health challenges. During and after the COVID-19 pandemic, demand for virtual mental health services surged, with telepsychiatry consultations becoming a mainstream care option in countries such as the United States, the United Kingdom, and parts of Europe. In addition, wearable devices and AI-based mental wellness applications are increasingly being used to monitor stress levels, sleep patterns, and physiological indicators linked to anxiety. These tools are enabling early intervention and continuous mental health monitoring, improving patient outcomes and expanding access to care.

Anxiety Disorder Market Dynamics

Key Market Driver: Rising Prevalence of Anxiety Disorders and Expanding Access to Mental Healthcare Services

The increasing global burden of anxiety disorders is a primary driver of market growth. According to the World Health Organization (WHO), mental health conditions, including anxiety and depression, represent a significant share of global disability burden, with anxiety disorders being among the most frequently diagnosed psychiatric conditions. Rising stress levels due to urbanization, academic pressure, workplace burnout, financial uncertainty, and social isolation are contributing to higher diagnosis rates. Improved awareness and reduced stigma around mental health are also encouraging more individuals to seek treatment. Pharmacological treatments such as selective serotonin reuptake inhibitors (SSRIs), serotonin-norepinephrine reuptake inhibitors (SNRIs), and benzodiazepines remain widely used, while non-pharmacological approaches such as psychotherapy and CBT are gaining strong adoption. The expansion of mental health infrastructure in North America and Europe, along with growing investments in psychiatric services in Asia-Pacific—particularly in countries such as India and China—is further accelerating market growth.

Large-scale initiatives such as national mental health programs and workplace wellness campaigns are also improving early diagnosis and treatment rates. The increasing integration of mental health services into primary healthcare systems is further supporting sustained market expansion.

Key Restraint/Challenge: Limited Access to Mental Healthcare and Stigma in Emerging Economies

A key challenge in the Anxiety Disorder Market is the limited access to mental healthcare services and persistent social stigma, particularly in low- and middle-income countries. Despite rising prevalence, a significant proportion of individuals with anxiety disorders remain undiagnosed or untreated due to lack of awareness, inadequate psychiatric infrastructure, and shortage of trained mental health professionals. In many developing regions, mental health services are concentrated in urban areas, leaving rural populations with limited access to diagnosis and treatment. In addition, cultural stigma surrounding mental illness often discourages individuals from seeking professional help, resulting in delayed intervention and worsening symptoms. Cost barriers also remain significant, as long-term therapy sessions and psychiatric medications may not be fully covered under public healthcare systems in several countries. The shortage of psychiatrists and psychologists further limits treatment capacity in high-demand regions. Addressing these challenges requires expansion of community-based mental health programs, integration of psychiatric care into primary healthcare systems, and increased adoption of digital mental health solutions to improve accessibility and affordability.

Key Market Opportunity: Expansion of Digital Therapeutics, AI-Based Mental Health Monitoring, and Personalized Treatment Models

The integration of artificial intelligence, digital therapeutics, and personalized mental healthcare solutions presents a major growth opportunity for the Anxiety Disorder market. AI-powered platforms are increasingly being used to analyze behavioral patterns, speech, and physiological data to detect early signs of anxiety and recommend personalized interventions. Digital Cognitive Behavioral Therapy (dCBT) platforms are gaining traction as scalable, cost-effective alternatives to traditional therapy, particularly in regions with limited access to mental health professionals. Mobile applications offering guided meditation, stress tracking, and mood monitoring are also expanding rapidly. Telepsychiatry adoption continues to grow globally, with healthcare systems increasingly incorporating virtual consultations into routine mental healthcare delivery. For example, in the United States, telehealth mental health visits increased significantly post-pandemic, becoming a standard component of psychiatric care delivery. In addition, workplace mental health programs and insurance-backed behavioral health initiatives are expanding across corporate sectors, particularly in North America and Europe. Growing investments in Asia-Pacific, including India’s digital health ecosystem and China’s mental wellness platforms, are expected to further accelerate market expansion through 2033.

Anxiety Disorder Market Scope

The Anxiety Disorder market is segmented on the basis of type, treatment, patient type, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the Anxiety Disorder Market is segmented into panic disorder, agoraphobia, generalized anxiety disorder, social anxiety disorder, specific phobia, and others. The Generalized Anxiety Disorder (GAD) segment dominated the market with approximately 34.8% share in 2025, owing to its high global prevalence, chronic progression pattern, and frequent coexistence with depression, insomnia, and stress-related conditions. GAD represents one of the most commonly diagnosed anxiety conditions across primary care and psychiatric settings, significantly contributing to prescription volume and therapy adoption. Increasing awareness, improved diagnostic screening tools, and integration of mental health assessments into routine healthcare visits are further strengthening its dominance. Rising urban stress, workload pressure, and lifestyle-related psychological disorders are also key contributors. Strong adoption of SSRIs, SNRIs, and cognitive behavioral therapy (CBT) as first-line treatment continues to support steady demand. Hospitals and specialty clinics increasingly prioritize early intervention strategies for GAD patients. Digital mental health platforms are also improving diagnosis rates globally. The segment benefits from continuous clinical research and improved disease classification standards.

The Social Anxiety Disorder segment is expected to witness the fastest growth with a CAGR of 9.6% from 2026 to 2033, driven by increasing psychological awareness, particularly among younger populations and urban working professionals. Rising social media exposure, academic pressure, and workplace competition are contributing significantly to the disorder’s incidence. Improved mental health literacy and reduced stigma around psychiatric consultations are supporting early diagnosis. Telepsychiatry platforms are enabling easier access to therapy and counseling services, especially in emerging economies. Digital CBT programs and AI-based mental health applications are increasingly used for treatment. Schools and universities are integrating mental wellness programs, further boosting early identification. Pharmaceutical companies are also expanding drug development pipelines targeting anxiety spectrum disorders. Growth in outpatient psychiatric consultations is accelerating segment expansion. Online therapy platforms are playing a crucial role in improving accessibility. Rising demand for non-invasive treatments is further strengthening adoption globally.

- By Treatment

On the basis of treatment, the market is segmented into medications, therapy, and others. The medications segment dominated the market with approximately 52.3% share in 2025, supported by widespread global prescription of antidepressants, including SSRIs, SNRIs, benzodiazepines (short-term), and beta-blockers for symptom control. Pharmacological intervention remains the most commonly prescribed and accessible treatment option across both developed and emerging healthcare systems. High patient dependency on long-term medication management is a key contributor. Hospitals and outpatient clinics prefer standardized drug-based protocols for moderate to severe anxiety cases. Increasing availability of generic drugs has improved affordability and access. Strong pharmaceutical pipelines and approvals of next-generation anxiolytics are supporting segment stability. Continuous physician preference for medication-first treatment approaches also drives demand. Combination therapies with psychotherapy are increasingly common. Insurance reimbursement systems strongly support pharmacological treatment. Medication adherence programs are further enhancing treatment continuity.

The therapy segment is expected to register the fastest CAGR of 10.1% from 2026 to 2033, driven by growing acceptance of cognitive behavioral therapy (CBT), exposure therapy, mindfulness-based therapy, and group counseling programs. Increasing preference for non-drug interventions due to reduced side effects is accelerating demand. Mental health awareness campaigns are improving therapy adoption globally. Teletherapy platforms and mobile mental health applications are expanding access significantly. Employers are increasingly offering mental wellness programs that include structured therapy sessions. Rising integration of digital CBT tools is improving scalability of therapy services. Patients are showing stronger preference for personalized psychological interventions. Governments are funding mental health counseling infrastructure expansion. Hybrid therapy models combining digital and in-person sessions are gaining traction. Growing shortage of psychiatrists is also driving digital therapy adoption.

- By Patients

On the basis of patient type, the market is segmented into inpatients and outpatients. The outpatient segment dominated the market with approximately 78.6% share in 2025, due to the chronic and manageable nature of anxiety disorders that typically do not require hospitalization. Most patients receive treatment through regular psychiatric consultations, therapy sessions, and prescription-based medication management. Increasing availability of outpatient psychiatric clinics is a major growth driver. Telemedicine platforms are further expanding outpatient accessibility. Patients prefer outpatient care due to lower costs and flexibility. Hospitals increasingly shift stable patients to outpatient monitoring programs. Community-based mental health initiatives are strengthening outpatient care delivery. Digital monitoring tools are improving long-term follow-up efficiency. Early diagnosis programs are increasing outpatient treatment initiation. Insurance coverage strongly supports outpatient psychiatric services.

The inpatient segment is expected to grow at a CAGR of 8.4% from 2026 to 2033, driven by increasing severe anxiety cases, comorbid psychiatric disorders, and acute crisis episodes requiring hospitalization. Rising cases of panic attacks with complications and suicidal ideation are increasing inpatient admissions. Psychiatric emergency units are expanding across hospitals. Government investments in mental health infrastructure are improving inpatient capacity. Specialized mental health hospitals are increasing globally. Integration of intensive behavioral therapy in inpatient settings is improving outcomes. Increasing awareness among families about severe anxiety conditions is driving admissions. Co-occurrence with depression and substance abuse is also contributing. Insurance coverage expansion is supporting inpatient affordability. Growth in urban psychiatric hospitals is further strengthening this segment.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral and others. The oral segment dominated the market with approximately 91.2% share in 2025, due to widespread use of oral antidepressants and anxiolytics as first-line therapy. Oral medications are easy to administer, cost-effective, and suitable for long-term use. High patient compliance supports their dominance globally. Physicians prefer oral SSRIs and SNRIs for chronic anxiety management. Availability of generic oral formulations has increased accessibility. Strong distribution networks support oral drug availability. Oral administration is suitable for both outpatient and homecare settings. Long-term safety profile supports continued usage. Pharmaceutical companies focus heavily on oral drug innovation. Patient preference for non-invasive treatment further strengthens adoption.

The other routes segment is expected to grow at a CAGR of 8.9% from 2026 to 2033, driven by advancements in rapid-acting formulations, injectable therapies for acute anxiety episodes, and emerging transdermal drug delivery systems. Research into fast-onset anti-anxiety treatments is increasing. Hospitals are adopting injectable formulations for emergency psychiatric care. Novel drug delivery technologies are improving bioavailability and response time. Increasing clinical trials in neuropsychiatry are supporting innovation. Demand for personalized medicine is also driving development of alternative routes. Biotechnology advancements are enabling targeted delivery systems. Growth in acute care psychiatry units is supporting adoption. Pharmaceutical R&D investments in novel formulations are rising. Improved patient outcomes are reinforcing segment expansion.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market with approximately 44.1% share in 2025, driven by strong psychiatric infrastructure, emergency mental health services, and integrated care pathways for moderate to severe anxiety disorders. Hospitals serve as primary diagnosis and treatment centers. Availability of psychiatrists and multidisciplinary teams supports dominance. Emergency psychiatric care demand is increasing globally. Hospitals also manage comorbid mental health conditions. Government healthcare funding supports hospital-based mental health services. Strong diagnostic and monitoring capabilities strengthen this segment. Insurance reimbursement favors hospital treatment pathways. Increasing inpatient psychiatric units are expanding capacity. Hospital-based outpatient departments contribute significantly to patient flow.

The homecare segment is expected to register the fastest CAGR of 10.3% from 2026 to 2033, driven by rising adoption of telepsychiatry, digital therapy platforms, and remote counseling services. Patients increasingly prefer home-based treatment due to convenience and reduced stigma. Mental health mobile applications are expanding rapidly. AI-driven therapy bots and virtual counseling platforms are gaining traction. Post-pandemic behavioral shift toward remote care is continuing. Homecare reduces healthcare system burden significantly. Governments are supporting digital mental health initiatives. Employers are offering home-based wellness programs. Remote monitoring tools improve treatment adherence. Increasing smartphone penetration is accelerating adoption globally.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the market with approximately 48.5% share in 2025, due to high prescription volume from psychiatric departments and controlled dispensing of antidepressants and anxiolytics. Hospitals remain the primary source of regulated mental health medications. Strong integration with inpatient and outpatient services supports dominance. Hospital pharmacies ensure compliance and monitoring. Physicians prefer hospital-based dispensing for severe cases. Institutional procurement systems support stable supply chains. Insurance-linked drug distribution is centered in hospitals. Emergency psychiatric care relies heavily on hospital pharmacies. Strong regulatory oversight ensures controlled access. Bulk procurement by hospitals strengthens market share.

The online pharmacy segment is expected to grow at the fastest CAGR of 11.2% from 2026 to 2033, driven by rising telemedicine adoption, e-prescriptions, and demand for discreet medication purchasing. Patients prefer online channels due to convenience and privacy. Digital healthcare ecosystems are expanding rapidly. Regulatory approvals for online drug delivery are increasing. Smartphone penetration is enabling easy access to pharmacy platforms. Subscription-based medication delivery models are gaining traction. Integration with telepsychiatry services is strengthening demand. AI-based prescription management systems are improving accuracy. Rural access to medications is improving significantly. Growth in digital health startups is accelerating expansion.

Anxiety Disorder Market Regional Analysis

North America dominated the Anxiety Disorder Market with the largest revenue share of approximately 41.6% in 2025, supported by high prevalence of anxiety disorders, advanced mental healthcare infrastructure, strong access to psychiatric services, and widespread adoption of pharmacological and psychotherapy-based treatments. The region also benefits from favorable reimbursement systems, high mental health awareness, and growing integration of digital mental health platforms such as telepsychiatry, AI-based therapy tools, and mobile behavioral health applications. The increasing burden of stress-related disorders, workplace burnout, and lifestyle-driven mental health conditions continues to drive demand for early diagnosis and long-term treatment solutions. In addition, strong healthcare spending and expanding insurance coverage for mental health services are further strengthening regional market growth.

U.S. Anxiety Disorder Market Insight

The U.S. Anxiety Disorder market is witnessing strong growth due to rising diagnosis rates, high awareness of mental health conditions, and increasing access to psychiatric care and behavioral therapy services. The country’s advanced healthcare infrastructure, strong presence of mental health professionals, and widespread insurance coverage for psychiatric treatment are supporting market expansion. Growing adoption of SSRIs, SNRIs, and cognitive behavioral therapy (CBT) remains central to treatment approaches, while digital mental health platforms and telepsychiatry services are increasingly improving access to care. Rising stress levels linked to work pressure, academic demands, and social factors are further contributing to higher treatment demand across outpatient and specialty care settings.

Europe Anxiety Disorder Market Insight

The Europe Anxiety Disorder market remains a major contributor to global revenue, driven by strong public healthcare systems, increasing mental health awareness, and expanding access to psychiatric services. The region benefits from structured mental healthcare frameworks, government-funded treatment programs, and growing adoption of psychotherapy and pharmacological interventions. Rising prevalence of anxiety disorders due to urban stress, aging populations, and socioeconomic pressures is supporting market growth. In addition, increasing integration of digital mental health services, including online therapy platforms and AI-assisted psychological support tools, is enhancing accessibility and treatment outcomes across European countries.

U.K. Anxiety Disorder Market Insight

The U.K. Anxiety Disorder market is experiencing steady growth, supported by strong mental health initiatives, increasing NHS-backed psychological services, and rising adoption of digital mental health platforms. The country has seen significant expansion of talking therapies and early intervention programs aimed at reducing long-term psychiatric burden. Growing awareness campaigns, improved access to Cognitive Behavioral Therapy (CBT), and increasing use of telepsychiatry are supporting early diagnosis and treatment. In addition, workplace mental health programs and government-led initiatives are further strengthening market adoption.

Germany Anxiety Disorder Market Insight

The Germany Anxiety Disorder market is expanding steadily due to strong healthcare infrastructure, increasing mental health awareness, and rising availability of psychiatric care services. Germany’s well-developed hospital network and outpatient mental health services are supporting widespread diagnosis and treatment. Growing adoption of antidepressants and structured psychotherapy programs is contributing to market growth. Additionally, increasing focus on workplace mental health, stress management programs, and integration of digital mental health tools is further enhancing access to care.

Asia-Pacific Anxiety Disorder Market Insight

The Asia-Pacific Anxiety Disorder market is expected to witness the fastest growth globally, registering a CAGR of approximately 9.3% from 2026 to 2033, driven by increasing awareness of mental health conditions, rising healthcare expenditure, expanding psychiatric care infrastructure, and improving access to diagnosis and treatment in countries such as China, India, and Japan. Government initiatives aimed at reducing mental health stigma, expanding behavioral healthcare services, and integrating mental health into primary care systems are significantly supporting regional market expansion. Increasing urbanization, changing lifestyles, and rising academic and workplace stress are also contributing to higher diagnosis rates.

Japan Anxiety Disorder Market Insight

The Japan Anxiety Disorder market is witnessing consistent growth due to increasing awareness of mental health conditions, aging population-related stress factors, and strong healthcare infrastructure. The country’s focus on workplace mental health and preventive care is supporting early diagnosis and treatment. Growing adoption of antidepressant medications, counseling services, and digital mental health platforms is improving access to care. Additionally, increasing integration of AI-enabled mental wellness applications and telepsychiatry services is enhancing treatment accessibility and patient monitoring.

China Anxiety Disorder Market Insight

The China Anxiety Disorder market is growing rapidly, driven by increasing urbanization, expanding transportation infrastructure, and rising government focus on road safety and professional driver education. Growing adoption of AI-enabled and VR/AR-based simulation platforms across commercial, automotive, and defense sectors is significantly boosting market demand. In addition, rising investments in automotive R&D, increasing awareness regarding safe driving practices, and rapid technological advancements are positioning China as one of the fastest-growing markets for Anxiety Disorder globally.

Anxiety Disorder Market Share

The Anxiety Disorder industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- GlaxoSmithKline plc (U.K.)

- Johnson & Johnson (U.S.)

- AstraZeneca plc (U.K.)

- Novartis AG (Switzerland)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Sanofi S.A. (France)

- Merck & Co., Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Bristol Myers Squibb (U.S.)

- Lundbeck A/S (Denmark)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Cipla Ltd. (India)

- Viatris Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- H. Lundbeck India (India)

- Alkermes plc (Ireland)

- Neuronetics, Inc. (U.S.)

- Neurocrine Biosciences, Inc. (U.S.)

- Acadia Pharmaceuticals Inc. (U.S.)

- Sage Therapeutics, Inc. (U.S.)

- H. Lundbeck A/S (Denmark)

- Talkspace Inc. (U.S.)

- Teladoc Health, Inc. (U.S.)

- BetterHelp (U.S.)

- Headspace Health (U.S.)

- Calm.com, Inc. (U.S.)

- Lyra Health, Inc. (U.S.)

- Spring Health (U.S.)

- Mindstrong Health (U.S.)

- Big Health Ltd. (U.K.)

- Ginger (Headspace Health) (U.S.)

Latest Developments in Anxiety Disorder Market

- In June 2021, AstraZeneca announced continued clinical advancement of its neuropsychiatric pipeline, including ongoing studies evaluating novel mechanisms for anxiety and related disorders such as GABAergic modulation therapies. The company emphasized expanding CNS research programs targeting generalized anxiety disorder (GAD), reflecting growing industry investment in non-benzodiazepine treatment approaches. This reinforced pharmaceutical focus on safer long-term anxiety treatments beyond traditional SSRIs and benzodiazepines

- In March 2022, Biogen and Sage Therapeutics reported progress in the clinical development of zuranolone, a neuroactive steroid targeting GABA-A receptors, being evaluated for mood and anxiety-related disorders. While primarily focused on major depressive disorder, the drug’s mechanism strengthened broader pipeline interest in rapid-acting GABAergic therapies with potential relevance for anxiety disorders. This highlighted a shift toward fast-onset CNS therapeutics in psychiatric care

- In August 2023, the U.S. FDA approved Johnson & Johnson’s SPRAVATO (esketamine) nasal spray label expansion for treatment-resistant depression with acute suicidal ideation, reinforcing the broader neuromodulation-based psychiatric treatment market. Although not exclusively indicated for anxiety, its rapid-acting antidepressant mechanism significantly influenced comorbid anxiety treatment strategies, expanding clinical adoption of NMDA receptor–targeted therapies in severe psychiatric conditions

- In December 2023, MindMed announced positive topline results from its Phase 2b clinical trial of MM-120 (lysergide d-tartrate) for generalized anxiety disorder (GAD), demonstrating statistically significant improvements in Hamilton Anxiety Rating Scale (HAM-A) scores compared to placebo. The study reported a 21.3-point reduction in anxiety severity at week 4 and strong response rates, marking one of the most notable psychedelic-assisted therapy breakthroughs in the anxiety disorder pipeline. This development accelerated investor and regulatory interest in psychedelic-based anxiolytics

- In March 2024, MindMed received FDA Breakthrough Therapy Designation for MM-120 for the treatment of generalized anxiety disorder following promising Phase 2b results. The designation was granted due to strong clinical efficacy signals, including a 65% response rate and 48% remission rate at 12 weeks. This milestone significantly advanced psychedelic-assisted therapy toward late-stage clinical development and potential commercialization

- In August 2024, MindMed announced preparations to initiate Phase 3 clinical trials for MM-120 in generalized anxiety disorder, marking the transition from mid-stage to late-stage development. The program included large-scale randomized studies expected to enroll hundreds of participants, reflecting increased regulatory momentum and commercialization readiness for psychedelic-based anxiety therapeutics. This development represented a key inflection point in next-generation psychiatric drug development

- In November 2025, Johnson & Johnson announced expanded FDA approval of Caplyta (lumateperone) as an adjunctive treatment for major depressive disorder, further strengthening the broader neuropsychiatric treatment market. While primarily indicated for depression, the drug’s anxiolytic effects in clinical populations contributed to its relevance in treating anxiety symptoms associated with mood disorders. The approval reinforced continued expansion of atypical antipsychotics in psychiatric care

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.