Global Aortic Coarctation Market

Market Size in USD Billion

USD

1.22 Billion

USD

1.57 Billion

2025

2033

USD

1.22 Billion

USD

1.57 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 1.22 Billion |

Market Size (Forecast Year) |

USD 1.57 Billion |

CAGR |

% |

Major Markets Players |

|

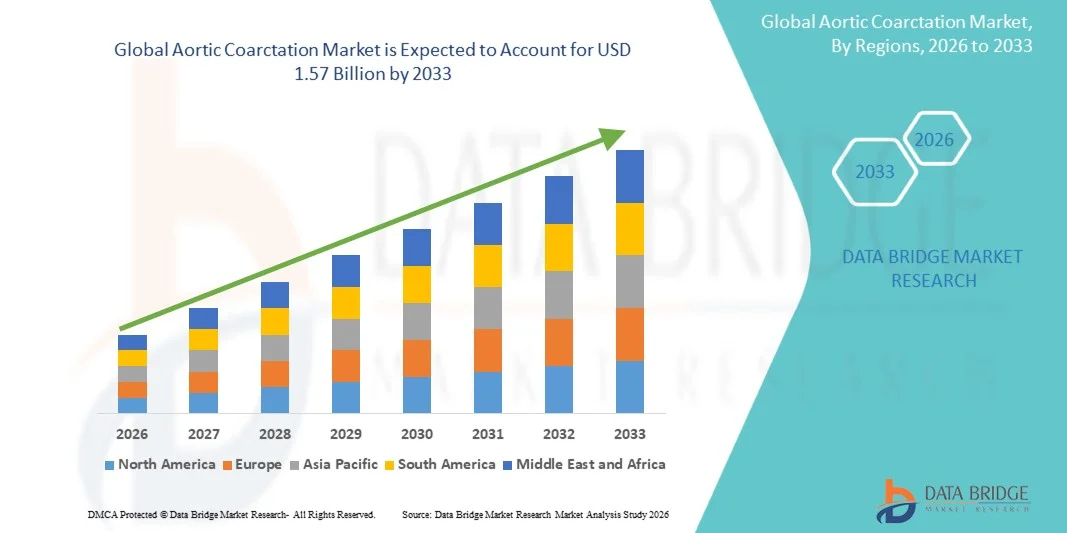

Aortic Coarctation Market Size

- The global aortic coarctation market size was valued at USD 1.22 billion in 2025 and is expected to reach USD 1.57 billion by 2033, at a CAGR of 3.22% during the forecast period

- The market growth is largely fueled by advancements in surgical and minimally invasive treatment techniques, rising awareness and early diagnosis of congenital heart defects, and increasing prevalence of aortic coarctation across populations

- Furthermore, growing healthcare infrastructure development, supportive government initiatives, and demand for improved access control in clinical care settings are driving the adoption of effective treatment solutions, establishing aortic coarctation interventions as essential components of cardiovascular care. These converging factors are accelerating the uptake of innovative therapies, thereby significantly boosting industry expansion

Aortic Coarctation Market Analysis

- Aortic coarctation, including interventions such as balloon angioplasty, patch aortoplasty, subclavian flap aortoplasty, and other surgical procedures, is increasingly a vital focus in cardiovascular care for both pediatric and adult patients due to its ability to restore normal blood flow, prevent complications, and improve long-term health outcomes

- The escalating demand for aortic coarctation interventions is primarily fueled by advancements in minimally invasive procedures, increased awareness and early diagnosis of congenital heart defects, and growing patient preference for safer, less invasive treatment options

- North America dominated the aortic coarctation market with the largest revenue share of 42.5% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative cardiovascular treatments, and the presence of key medical device and surgical solution providers, with the U.S. experiencing substantial growth in procedure volumes due to improved screening programs and technological innovations

- Asia-Pacific is expected to be the fastest-growing region in the aortic coarctation market during the forecast period due to increasing healthcare infrastructure investments, rising awareness of congenital heart disease, and growing availability of minimally invasive cardiovascular interventions

- The balloon angioplasty segment dominated the aortic coarctation market by treatment in 2025 with a market share of 47.8%, driven by its established efficacy, lower procedural risks, and growing preference among clinicians for catheter-based solutions over traditional open-heart surgery

Report Scope and Aortic Coarctation Market Segmentation

|

Attributes |

Aortic Coarctation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Aortic Coarctation Market Trends

“Advancements in Minimally Invasive Interventions”

- A significant and accelerating trend in the global aortic coarctation market is the increasing adoption of minimally invasive procedures, including balloon angioplasty and stenting, which reduce recovery times and procedural risks compared to traditional open-heart surgery

- For instance, catheter-based stent implantation allows physicians to treat coarctation with smaller incisions, enabling faster patient recovery and lower complication rates, making it a preferred option in specialized cardiac centers

- Technological improvements, such as drug-eluting stents and 3D imaging guidance, are enhancing procedural precision, reducing restenosis rates, and improving long-term patient outcomes

- The integration of imaging modalities and real-time monitoring during interventions is facilitating better procedural planning and post-operative management, improving overall clinical efficiency

- This trend towards safer, less invasive, and more precise interventions is reshaping treatment protocols, prompting device manufacturers and hospitals to focus on advanced stents and catheter systems

- The demand for minimally invasive and precision-guided aortic coarctation interventions is growing rapidly across pediatric and adult populations, as healthcare providers increasingly prioritize patient safety and procedural efficacy

- Growing patient preference for outpatient or short-stay procedures is encouraging healthcare providers to adopt catheter-based interventions over traditional surgical repair

Aortic Coarctation Market Dynamics

Driver

“Increasing Prevalence of Congenital Heart Defects and Early Diagnosis”

- The rising prevalence of congenital heart defects, including aortic coarctation, coupled with the growing focus on early diagnosis, is a significant driver for increased demand for effective treatment interventions

- For instance, newborn screening programs and echocardiography-based early detection in high-risk populations are enabling timely interventions, reducing complications, and improving survival rates

- Improved awareness among healthcare providers and parents regarding long-term cardiovascular risks associated with untreated coarctation is further propelling the adoption of corrective procedures

- Furthermore, the expanding availability of specialized cardiac centers and advanced surgical infrastructure is making aortic coarctation interventions more accessible to patients in both urban and semi-urban regions

- The ability to deliver patient-specific treatment plans using advanced imaging and intervention techniques is enhancing treatment outcomes and driving market growth

- Increasing healthcare spending, technological advancements, and the rising number of diagnosed cases are collectively creating robust opportunities for the aortic coarctation market

- Rising adoption of telemedicine and remote monitoring for pre- and post-procedure care is facilitating early intervention and better patient management

- Growing investment in pediatric cardiology infrastructure and specialized centers is increasing treatment accessibility and supporting market expansion

Restraint/Challenge

“Procedural Risks and Limited Access to Specialized Care”

- Concerns surrounding procedural complications, such as restenosis, aneurysm formation, or post-surgical hypertension, pose a significant challenge to broader adoption of aortic coarctation interventions

- For instance, complications following surgical repair or balloon angioplasty can require repeat interventions, leading to increased patient anxiety and additional healthcare costs

- Limited access to specialized cardiac centers and trained interventional cardiologists in emerging markets restricts the availability of advanced aortic coarctation treatments

- High costs associated with minimally invasive stents and specialized surgical procedures can also be a barrier to adoption, particularly in developing regions with constrained healthcare budgets

- Addressing these challenges through improved procedural safety, expanded cardiac infrastructure, and training programs for healthcare professionals is crucial for market growth

- While technological advancements continue to reduce risks, overcoming cost and access barriers remains essential for wider adoption of aortic coarctation interventions globally

- Variations in healthcare regulations and insurance coverage across countries can delay adoption of advanced treatment options

- Patient hesitation due to fear of complications or lack of awareness about minimally invasive options continues to limit market penetration in certain regions

Aortic Coarctation Market Scope

The market is segmented on the basis of treatment and end-user.

- By Treatment

On the basis of treatment, the aortic coarctation market is segmented into balloon angioplasty, patch aortoplasty, subclavian flap aortoplasty, and others. The balloon angioplasty segment dominated the market with the largest revenue share of 47.8% in 2025, driven by its minimally invasive nature and established clinical efficacy. Balloon angioplasty allows cardiologists to widen the narrowed aorta using a catheter-based approach, significantly reducing recovery times compared to traditional surgical repair. Patients and clinicians often prefer this treatment due to its lower procedural risks and shorter hospital stays. Technological advancements such as drug-eluting balloons and precision imaging guidance have further enhanced its safety and long-term outcomes. The segment’s dominance is also supported by increasing awareness of congenital heart defects and early diagnosis programs, which often lead to timely intervention with balloon angioplasty. Hospitals and cardiac institutes frequently adopt this procedure for pediatric and adult patients due to its high success rates and reduced need for intensive post-operative care.

The patch aortoplasty segment is anticipated to witness the fastest growth at a CAGR of 6.5% from 2026 to 2035, fueled by increasing adoption in complex coarctation cases that are unsuitable for balloon angioplasty. Patch aortoplasty involves surgical reconstruction of the aortic segment using a synthetic or autologous patch, offering a reliable solution for severe or recurrent narrowing. Rising investments in cardiovascular surgical infrastructure, particularly in emerging markets, are expanding the availability of this procedure. The technique’s ability to address extensive coarctation and associated complications makes it a preferred choice among cardiac surgeons for select patients. In addition, advancements in patch materials and minimally invasive surgical approaches are improving patient outcomes and recovery times. Increasing training and expertise among cardiothoracic surgeons are also supporting wider adoption of patch aortoplasty globally.

- By End User

On the basis of end user, the market is segmented on the basis of end users including hospitals, clinics, cardiac institutes, and others. The hospitals segment dominated the market with a share of 51% in 2025, owing to their advanced surgical facilities, availability of specialized cardiac teams, and capability to manage complex congenital heart cases. Hospitals are the primary setting for both minimally invasive and surgical aortic coarctation interventions, particularly for pediatric patients requiring continuous monitoring and post-operative care. Large hospitals with dedicated cardiology and cardiothoracic departments also offer a broad range of treatment options, including balloon angioplasty and patch aortoplasty. The presence of experienced surgeons and interventional cardiologists in hospitals ensures higher success rates and patient confidence. Furthermore, hospitals often collaborate with medical device manufacturers to trial and implement innovative stent and catheter technologies, further reinforcing their dominance. Growing awareness and accessibility of hospital-based cardiovascular care continue to drive patient preference toward this end-user segment.

The cardiac institutes segment is expected to witness the fastest growth with a CAGR of 7.1% from 2026 to 2035, fueled by increasing specialization in congenital and adult cardiac care. Cardiac institutes often focus exclusively on complex cardiovascular cases, offering high-end diagnostic tools, minimally invasive interventions, and follow-up care tailored to individual patient needs. Rising investments in specialized cardiac centers, particularly in urban regions of emerging markets, are expanding treatment accessibility. Institutes provide a concentrated expertise pool for procedures such as balloon angioplasty and patch aortoplasty, enhancing outcomes for high-risk patients. In addition, partnerships with research organizations and adoption of advanced imaging and intervention technologies are further accelerating the growth of this segment. Increasing patient awareness of dedicated cardiac care centers is also contributing to higher adoption rates in this segment.

Aortic Coarctation Market Regional Analysis

- North America dominated the aortic coarctation market with the largest revenue share of 42.5% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative cardiovascular treatments, and the presence of key medical device and surgical solution providers

- Patients and healthcare providers in the region highly value minimally invasive interventions such as balloon angioplasty and stenting, which offer shorter recovery times, lower procedural risks, and improved long-term outcomes compared to traditional surgical repair

- This widespread adoption is further supported by the presence of specialized cardiac centers, experienced interventional cardiologists, and high healthcare spending, establishing North America as the preferred region for both pediatric and adult aortic coarctation interventions

U.S. Aortic Coarctation Market Insight

The U.S. aortic coarctation market captured the largest revenue share of 44% in 2025 within North America, fueled by the widespread adoption of minimally invasive interventions such as balloon angioplasty and stenting. Patients and clinicians increasingly prioritize procedures with shorter recovery times, lower risks, and improved long-term outcomes. The presence of specialized cardiac centers, skilled interventional cardiologists, and advanced imaging technologies further supports market growth. Growing awareness of congenital heart defects and early diagnosis programs is also driving demand. In addition, high healthcare spending and strong infrastructure for cardiovascular care are accelerating the adoption of aortic coarctation treatments across both pediatric and adult populations.

Europe Aortic Coarctation Market Insight

The Europe aortic coarctation market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising awareness of congenital heart disease and investments in advanced cardiovascular care facilities. Increasing urbanization, coupled with higher healthcare spending, is fostering the adoption of minimally invasive and surgical interventions. European patients are increasingly opting for precise, safe, and effective procedures, supported by technologically advanced hospitals and cardiac institutes. The region is experiencing significant growth across pediatric and adult care segments, with treatments being incorporated into both new hospital programs and specialized cardiac centers. Furthermore, stringent healthcare regulations and government initiatives to improve cardiac outcomes are contributing to market expansion.

U.K. Aortic Coarctation Market Insight

The U.K. aortic coarctation market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of congenital heart defects and a desire for improved procedural safety. Rising demand for minimally invasive interventions, such as balloon angioplasty, and enhanced follow-up care are encouraging both hospitals and cardiac institutes to adopt advanced treatment options. In addition, early screening programs, specialized cardiac centers, and robust healthcare infrastructure are expected to continue supporting market growth. The U.K.’s emphasis on quality care and patient safety is fostering greater adoption of corrective interventions across both pediatric and adult populations.

Germany Aortic Coarctation Market Insight

The Germany aortic coarctation market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of congenital heart conditions and technological advancements in cardiovascular care. Germany’s advanced healthcare infrastructure, coupled with an emphasis on precision and safety in medical procedures, promotes the adoption of both minimally invasive and surgical interventions. Integration of advanced imaging systems and catheter-based solutions enhances procedural outcomes, while specialized cardiac centers ensure access to expert care. The demand for patient-specific interventions and improved post-operative care continues to drive growth in the region.

Asia-Pacific Aortic Coarctation Market Insight

The Asia-Pacific aortic coarctation market is poised to grow at the fastest CAGR of 7.5% from 2026 to 2035, driven by increasing healthcare infrastructure investments, rising awareness of congenital heart disease, and growing availability of minimally invasive cardiovascular interventions. Countries such as China, Japan, and India are witnessing rapid adoption of balloon angioplasty and stent procedures due to their safety and efficacy. Government initiatives promoting early diagnosis and specialized cardiac centers are also supporting market growth. Furthermore, increasing healthcare spending and urbanization are improving access to advanced cardiac care across the region.

Japan Aortic Coarctation Market Insight

The Japan aortic coarctation market is gaining momentum due to the country’s advanced healthcare system, high awareness of congenital heart defects, and increasing adoption of minimally invasive interventions. Growing numbers of specialized cardiac centers and skilled interventional cardiologists enable effective treatment of both pediatric and adult patients. Integration of advanced imaging and catheter-based procedures is improving procedural success rates. In addition, the aging population and rising demand for patient-friendly interventions are driving market expansion in both residential and hospital-based care settings.

India Aortic Coarctation Market Insight

The India aortic coarctation market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding healthcare infrastructure, growing awareness of congenital heart disease, and rising adoption of minimally invasive procedures. India is becoming a key hub for cardiac care, with specialized hospitals and cardiac institutes offering balloon angioplasty, patch aortoplasty, and stenting procedures. Government initiatives for early screening, urbanization, and increasing healthcare spending are supporting market growth. In addition, increasing availability of skilled cardiologists and advanced intervention technologies is further propelling adoption across pediatric and adult populations.

Aortic Coarctation Market Share

The Aortic Coarctation industry is primarily led by well-established companies, including:

- Renata Medical, Inc. (U.S.)

- Boston Scientific Corporation (U.S.)

- Medtronic (Ireland)

- Abbott (U.S.)

- Cook (U.S.)

- B. Braun SE (U.S.)

- Terumo Corporation (Japan)

- MicroPort Scientific Corporation (China)

- OrbusNeich Medical Group Holdings Limited (Hong Kong)

- Biotronik SE & Co. KG (Germany)

- W. L. Gore & Associates, Inc. (U.S.)

- Endologix, Inc. (U.S.)

- Lombard Medical, Inc. (U.S.)

- CryoLife, Inc. (U.S.)

- Cordis Corporation (U.S.)

- Lepu Medical Technology (Beijing) Co., Ltd. (China)

- Braile Biomédica (Brazil)

- Getinge AB (Sweden)

- iVascular (Spain)

- Artivion Inc. (U.S.)

What are the Recent Developments in Global Aortic Coarctation Market?

- In September 2025, Arkansas Children’s Heart Institute announced successful implantation of a Renata Minima aortic stent in the smallest baby to ever receive it, demonstrating the expanding application of this pediatric stent technology for treating coarctation of the aorta in extremely low‑weight infants

- In August 2025, Nicklaus Children’s Heart Institute became the first hospital in South Florida to offer the innovative Minima Stent for growing pediatric patients, providing a new treatment alternative that helps avoid repeated open‑heart surgeries in infants with aortic coarctation and related conditions

- In September 2024, Renata Medical announced the first successful implantation of the commercially available Minima Growth Stent in a young child following FDA approval, marking a significant real‑world clinical achievement and expanding treatment options for pediatric patients with congenital vascular narrowing

- In August 2024, the U.S. Food and Drug Administration (FDA) approved the Minima Growth Stent, a first‑of‑its‑kind balloon‑expandable stent designed specifically to treat aortic coarctation and pulmonary artery stenosis in neonates, infants, and children; this device can be expanded as the child grows, representing a significant advancement in minimally invasive congenital heart defect care

- In January 2023, the American College of Cardiology (ACC) reported data from the IMPACT Registry showing catheter‑based interventions (including stenting) are safe and highly effective for native aortic coarctation in older children and adults, substantiating the growing clinical adoption of less invasive treatments over traditional surgical repair

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.