Global Arachnoiditis Treatment Market

Market Size in USD Billion

USD

2.63 Billion

USD

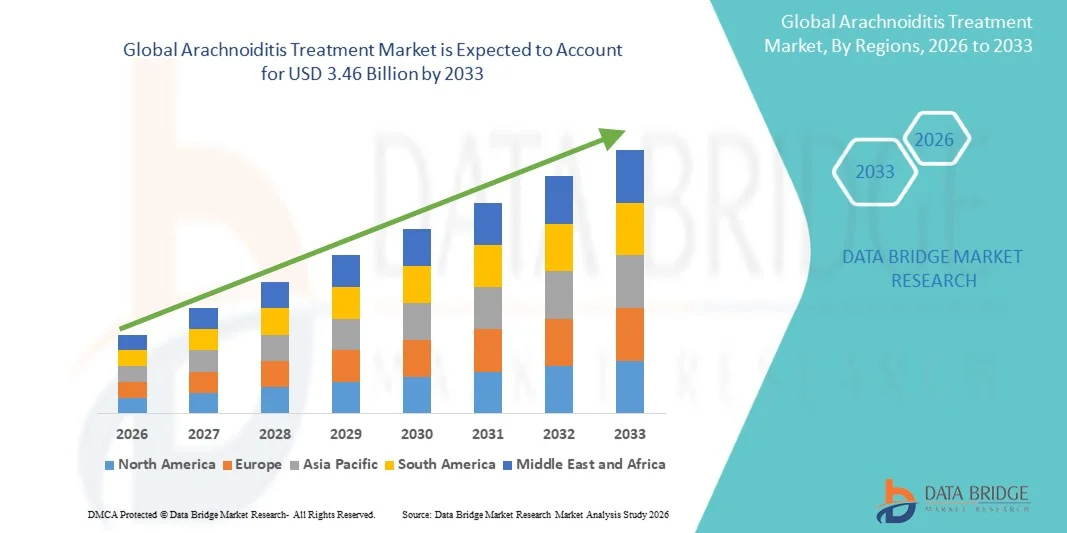

3.46 Billion

2025

2033

USD

2.63 Billion

USD

3.46 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.63 Billion | |

| USD 3.46 Billion | |

| % | |

|

Arachnoiditis Treatment Market Size

- The global arachnoiditis treatment market size was valued at USD 2.63 billion in 2025 and is expected to reach USD 3.46 billion by 2033, at a CAGR of 3.50% during the forecast period

- The market growth is primarily driven by the rising incidence of spinal surgeries, epidural procedures, and post-surgical complications, which are key contributors to arachnoiditis cases, along with increasing awareness of chronic neuropathic pain conditions and their long-term management needs

- Furthermore, growing demand for advanced pain management therapies, including anti-inflammatory drugs, neuro-modulatory treatments, and minimally invasive interventions, is strengthening the adoption of specialized treatment approaches, thereby supporting steady growth of the arachnoiditis treatment market

Arachnoiditis Treatment Market Analysis

- Arachnoiditis treatment market, focused on managing a rare and chronic inflammatory condition affecting the arachnoid membrane of the spinal cord and brain, is gaining clinical importance due to increasing post-surgical complications, infections, and trauma-related spinal injuries leading to long-term neuropathic pain and disability

- The escalating demand for treatment is primarily driven by rising incidence of spinal surgeries and epidural procedures, growing burden of chronic pain disorders, and increasing reliance on long-term symptom management using drug-based and supportive care approaches

- North America dominated the arachnoiditis treatment market with the largest revenue share of 41.6% in 2025, supported by advanced neurological care infrastructure, higher diagnosis rates, strong pain management specialist presence, and greater access to both pharmacological and interventional treatment options

- Asia-Pacific is expected to be the fastest growing region in the arachnoiditis treatment market during the forecast period due to improving healthcare access, rising awareness of rare neurological conditions, expanding hospital networks, and increasing investments in specialty care services

- Pain Management segment dominated the arachnoiditis treatment market in 2025 with a market share of 52.3%, driven by heavy reliance on NSAIDs, corticosteroids, anti-spasm drugs, and anti-convulsant drugs for controlling neuropathic pain, inflammation, and muscle spasms associated with the disease

Report Scope and Arachnoiditis Treatment Market Segmentation

|

Attributes |

Arachnoiditis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Arachnoiditis Treatment Market Trends

“Growing Shift Toward Multimodal Chronic Pain Management Approaches”

- A significant and evolving trend in the global arachnoiditis treatment market is the increasing adoption of multimodal treatment strategies combining pharmacological therapy, physiotherapy, and psychological support to improve long-term patient outcomes in chronic neuropathic pain management

- For instance, NSAIDs such as ibuprofen and naproxen are commonly used alongside corticosteroids and anti-convulsant drugs like gabapentin to simultaneously target inflammation, nerve irritation, and pain signaling pathways in arachnoiditis patients

- Integration of interventional pain management techniques with oral and parenteral drug therapies is improving symptom control, particularly in adhesive arachnoiditis cases where nerve root clumping leads to severe chronic pain and mobility limitations

- The growing use of personalized treatment planning based on disease type such as adhesive arachnoiditis, arachnoiditis ossificans, and neoplastic arachnoiditis is enabling more targeted and stage-specific therapeutic interventions across neurology clinics

- This shift toward integrated care models combining medication, rehabilitation, and psychological therapy is reshaping clinical expectations and improving quality of life outcomes for patients with long-term spinal inflammatory conditions

- The demand for coordinated treatment pathways is increasing across hospitals and specialty pain centers as clinicians focus more on functional improvement rather than symptom suppression alone

Arachnoiditis Treatment Market Dynamics

Driver

“Rising Burden of Spinal Procedures and Chronic Neuropathic Pain Conditions”

- The increasing incidence of spinal surgeries, epidural anesthesia procedures, and spinal infections is a key driver accelerating demand for arachnoiditis treatment due to higher risk of post-procedural inflammatory complications

- For instance, surgical interventions involving the spine often lead to adhesive arachnoiditis in rare cases, requiring long-term management using NSAIDs, corticosteroids, and anti-convulsant drugs to control persistent neuropathic pain

- Growing prevalence of chronic pain disorders and underdiagnosis of arachnoiditis is further increasing patient dependence on long-term pharmacological and rehabilitative care across neurology and pain management centers

- Furthermore, expanding access to specialized neurological care and improved imaging techniques such as MRI are enabling earlier detection and more effective disease management strategies in clinical practice

- Increasing awareness among healthcare providers regarding post-surgical inflammatory complications is encouraging early intervention and structured pain management protocols for affected patients

- Rising healthcare investments in neurological disorder treatment infrastructure are further supporting the expansion of advanced therapeutic options across both developed and emerging markets

Restraint/Challenge

“Limited Disease Awareness and Complex Clinical Diagnosis”

- A major challenge limiting the arachnoiditis treatment market is the low awareness and underdiagnosis of the condition due to its rarity and symptom overlap with other chronic spinal and neuropathic disorders

- For instance, patients often present with nonspecific symptoms such as chronic back pain and neurological deficits, making it difficult to differentiate arachnoiditis from conditions like spinal stenosis or disc disorders in early stages

- The absence of standardized treatment protocols and limited clinical guidelines creates variability in therapeutic approaches across healthcare providers, affecting treatment consistency and outcomes

- Furthermore, advanced diagnostic imaging requirements such as high-resolution MRI are not always readily accessible in developing regions, delaying accurate diagnosis and intervention

- The chronic and progressive nature of disease types such as adhesive arachnoiditis and arachnoiditis ossificans further complicates long-term management and reduces treatment predictability

- Limited availability of disease-specific clinical trials restricts the development of targeted therapies, slowing innovation in disease-modifying treatment options

- Overcoming these challenges through improved physician awareness, better diagnostic standardization, and expanded access to neurological imaging will be essential for improving market growth and patient outcomes

Arachnoiditis Treatment Market Scope

The market is segmented on the basis of drug class, disease type, treatment, route of administration, end-users, and distribution channel.

- By Drug Class

On the basis of drug class, the arachnoiditis treatment market is segmented into NSAIDs (non-steroidal anti-inflammatory drugs), corticosteroids, anti-spasm drugs, and anti-convulsant drugs. The NSAIDs segment dominated the market with the largest revenue share of 38.4% in 2025, driven by their wide availability, cost-effectiveness, and first-line use in managing inflammation and mild-to-moderate neuropathic pain associated with arachnoiditis. NSAIDs such as ibuprofen and naproxen are commonly prescribed in early-stage management to reduce spinal inflammation and improve patient mobility. Their extensive use in both hospital and outpatient settings further strengthens their dominance. In addition, NSAIDs are frequently combined with other drug classes for multimodal pain management, reinforcing their foundational role in treatment protocols.

The anti-convulsant drugs segment is anticipated to witness the fastest growth rate of 18.9% from 2026 to 2033, driven by increasing use in managing chronic neuropathic pain and nerve irritation associated with adhesive arachnoiditis. Drugs such as gabapentin and pregabalin are gaining strong adoption due to their effectiveness in targeting nerve-related pain pathways. Rising awareness among clinicians regarding neuropathic pain mechanisms is further supporting their uptake. In addition, growing preference for long-term oral therapy in chronic cases is contributing to sustained demand for anti-convulsant medications.

- By Disease Type

On the basis of disease type, the market is segmented into adhesive arachnoiditis, arachnoiditis ossificans, cerebral arachnoiditis, hereditary arachnoiditis, neoplastic arachnoiditis, and optochiasmatic arachnoiditis. The adhesive arachnoiditis segment dominated the market with the largest revenue share of 44.6% in 2025, owing to its higher prevalence as the most commonly diagnosed and clinically severe form of the disease. It is strongly associated with post-surgical spinal complications, infections, and epidural procedures leading to nerve root clumping and chronic debilitating pain. The condition requires long-term pain management and multidisciplinary care, significantly driving drug consumption and healthcare utilization. Increasing MRI-based diagnosis rates are further supporting the identification of adhesive cases.

The neoplastic arachnoiditis segment is anticipated to witness the fastest growth rate of 17.6% from 2026 to 2033, driven by rising incidence of cancer-related neurological complications and improved cancer survival rates leading to longer disease progression monitoring. Tumor-associated inflammation of the arachnoid membrane is increasingly recognized in oncology patients undergoing radiotherapy or chemotherapy. Growing integration of oncology and neurology care pathways is further enhancing diagnosis and treatment rates for this segment.

- By Treatment

On the basis of treatment, the market is segmented into pain management, physiotherapy, psychotherapy, and others. The pain management segment dominated the market with the largest revenue share of 52.3% in 2025, driven by the chronic and severe neuropathic pain nature of arachnoiditis requiring continuous pharmacological intervention. NSAIDs, corticosteroids, anti-convulsants, and anti-spasm drugs form the backbone of treatment protocols aimed at reducing inflammation and improving quality of life. High dependence on long-term medication use in both hospital and homecare settings further strengthens this segment’s dominance. In addition, pain management remains the primary clinically accessible approach due to limited curative options.

The physiotherapy segment is anticipated to witness the fastest growth rate of 19.2% from 2026 to 2033, driven by increasing recognition of its role in improving mobility, reducing stiffness, and enhancing functional recovery in chronic cases. Rehabilitation programs are increasingly being integrated into long-term care plans for adhesive arachnoiditis patients. Growing adoption of multidisciplinary treatment approaches in specialty clinics is further supporting segment growth. Specialty clinics are increasingly integrating physiotherapy into long-term care strategies.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral and parenteral. The oral segment dominated the market with the largest revenue share of 61.8% in 2025, driven by patient convenience, long-term treatment adherence, and widespread use of oral NSAIDs and anti-convulsant drugs. Oral medications are preferred for chronic outpatient management due to ease of administration and lower cost compared to injectable therapies. The availability of multiple oral formulations for neuropathic pain further supports their dominance. In addition, oral therapies are widely prescribed in homecare settings for sustained symptom control.

The parenteral segment is anticipated to witness the fastest growth rate of 16.4% from 2026 to 2033, driven by increasing use in hospital settings for severe acute pain episodes and advanced inflammatory cases. Corticosteroid injections and epidural administration routes are gaining traction for rapid symptom relief in refractory cases. Rising adoption of interventional pain management techniques is further contributing to segment expansion. Rising chronic disease burden is further accelerating growth.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market with the largest revenue share of 47.9% in 2025, driven by higher patient inflow for diagnosis, imaging, and initiation of complex pain management therapies. Hospitals serve as primary centers for spinal disorder diagnosis and multidisciplinary treatment planning. Availability of advanced neurological imaging and interventional procedures further strengthens hospital dominance. In addition, most severe and post-surgical arachnoiditis cases are managed in hospital settings.

The specialty clinics segment is anticipated to witness the fastest growth rate of 20.1% from 2026 to 2033, driven by increasing demand for focused chronic pain management services and neurological rehabilitation care. These clinics offer targeted treatment protocols combining pharmacological and non-pharmacological approaches. Rising patient preference for specialized long-term care is further boosting segment growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, online pharmacies, and others. The hospital pharmacy segment dominated the market with the largest revenue share of 49.5% in 2025, driven by direct dispensing of prescription drugs during hospital-based diagnosis and treatment initiation. Strong integration with inpatient and outpatient hospital services ensures consistent drug availability. High dependence on prescription-based therapies for arachnoiditis further supports hospital pharmacy dominance. In addition, hospital pharmacies play a critical role in managing complex medication regimens.

The online pharmacies segment is anticipated to witness the fastest growth rate of 22.3% from 2026 to 2033, driven by increasing digital healthcare adoption and convenience of home delivery for chronic disease medications. Expanding telemedicine services and rising smartphone penetration are further accelerating online drug procurement. The Patients with long-term treatment needs are increasingly shifting toward digital pharmacy platforms for cost and accessibility benefits. Cost advantages and accessibility are further driving growth.

Arachnoiditis Treatment Market Regional Analysis

- North America dominated the arachnoiditis treatment market with the largest revenue share of 41.6% in 2025, supported by advanced neurological care infrastructure, higher diagnosis rates, strong pain management specialist presence, and greater access to both pharmacological and interventional treatment options

- Patients and healthcare providers in the region benefit from strong availability of pain management specialists, MRI-based diagnostic capabilities, and established clinical protocols for chronic neuropathic pain conditions

- This widespread adoption is further supported by high healthcare expenditure, strong awareness of post-surgical spinal complications, and increasing use of multimodal treatment approaches including NSAIDs, corticosteroids, and anti-convulsant drugs, establishing North America as the leading region for arachnoiditis treatment demand

U.S. Arachnoiditis Treatment Market Insight

The U.S. arachnoiditis treatment market captured the largest revenue share of 81% in North America in 2025, driven by advanced neurology care systems and early adoption of innovative pain management therapies. Patients increasingly benefit from widespread availability of MRI diagnostics, interventional pain clinics, and specialized neurological treatment centers focusing on chronic spinal disorders. The growing preference for long-term multimodal therapy approaches, including pharmacological and physiotherapy-based care, is significantly supporting market expansion. Strong presence of leading pharmaceutical companies and advanced clinical research activities further enhances treatment accessibility and innovation in the country. Rising incidence of post-surgical spinal complications and epidural procedure-related inflammation is further fueling demand for arachnoiditis treatment in the U.S., along with increasing awareness of rare neurological conditions and improved insurance coverage for chronic pain management.

Europe Arachnoiditis Treatment Market Insight

The Europe arachnoiditis treatment market is projected to expand at a substantial CAGR during the forecast period, driven by growing awareness of rare neurological disorders and improving diagnostic capabilities. Increasing prevalence of spinal surgeries and degenerative spine conditions is contributing to higher cases requiring long-term pain management therapies. Patients in the region benefit from well-established public healthcare systems and broader access to neurological care services across hospitals and specialty clinics. The rising adoption of multidisciplinary treatment approaches, including physiotherapy and psychotherapy, is supporting improved patient outcomes, while growing focus on evidence-based treatment protocols and clinical research initiatives is further strengthening the regional market landscape. Expansion of rehabilitation centers and chronic pain management programs is also supporting sustained market growth across key European countries.

U.K. Arachnoiditis Treatment Market Insight

The U.K. arachnoiditis treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of chronic spinal inflammatory conditions and rising cases of post-surgical complications. Patients benefit from access to advanced NHS neurological care services and structured pain management pathways. Growing adoption of pharmacological therapies such as NSAIDs, corticosteroids, and anti-convulsants is supporting disease management, while increasing focus on early diagnosis and referral systems is improving treatment outcomes. In addition, expansion of specialist pain clinics is enhancing long-term care accessibility for patients.

Germany Arachnoiditis Treatment Market Insight

The Germany arachnoiditis treatment market is expected to expand at a considerable CAGR during the forecast period, driven by strong healthcare infrastructure and advanced neurological research capabilities. Increasing incidence of spinal disorders and surgical interventions is contributing to higher diagnosis rates of arachnoiditis. Patients benefit from widespread availability of MRI imaging and specialized neuro-rehabilitation services. Strong emphasis on precision medicine and evidence-based treatment protocols is supporting effective disease management, while growing integration of physiotherapy and pharmacological therapies is enhancing recovery outcomes in chronic cases. In addition, rising healthcare investments in neurological disorder treatment are strengthening market expansion.

Asia-Pacific Arachnoiditis Treatment Market Insight

The Asia-Pacific arachnoiditis treatment market is poised to grow at the fastest CAGR of 23.8% during 2026 to 2033, driven by rising healthcare access and increasing awareness of neurological disorders. Rapid urbanization and growing incidence of spinal surgeries are contributing to higher cases of chronic neuropathic pain conditions. Expanding healthcare infrastructure and government investments in specialty care are supporting market growth across the region, while increasing adoption of advanced diagnostic imaging technologies such as MRI is improving early detection rates. Growing availability of affordable generic drugs is enhancing treatment accessibility for a larger patient population, along with rising focus on chronic pain management programs accelerating adoption of multimodal treatment approaches.

Japan Arachnoiditis Treatment Market Insight

The Japan arachnoiditis treatment market is gaining momentum due to its advanced healthcare system and strong focus on neurological care innovation. High prevalence of aging-related spinal disorders is contributing to increased demand for chronic pain management therapies. Patients benefit from early diagnosis capabilities and widespread use of advanced imaging technologies. Integration of pharmacological treatment with rehabilitation therapy is improving long-term patient outcomes, while strong emphasis on minimally invasive treatment approaches is supporting better disease management. In addition, increasing healthcare R&D investments are driving improvements in neurological disorder treatment options.

India Arachnoiditis Treatment Market Insight

The India arachnoiditis treatment market accounted for the largest market revenue share in Asia Pacific in 2025, driven by rapid urbanization and expanding healthcare infrastructure. Increasing awareness of spinal disorders and rising number of surgical procedures are contributing to higher diagnosis rates. Patients are gaining improved access to affordable generic NSAIDs, corticosteroids, and anti-convulsant drugs. Expansion of specialty hospitals and neurology clinics is strengthening treatment availability across urban centers, while government initiatives supporting healthcare modernization and diagnostic accessibility are further boosting market growth. In addition, growing adoption of private healthcare services is enhancing overall treatment penetration in the country.

Arachnoiditis Treatment Market Share

The Arachnoiditis Treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Novartis AG (Switzerland)

- Sanofi (France)

- AstraZeneca (U.K.)

- GSK plc (U.K.)

- Bristol-Myers Squibb Company (U.S.)

- Eli Lilly and Company (U.S.)

- Teva Pharmaceutical Industries Ltd (Israel)

- Viatris Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd (India)

- Cipla Limited (India)

- Dr. Reddy’s Laboratories Limited (India)

- Abbott (U.S.)

- Boehringer Ingelheim International GmbH (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Hikma Pharmaceuticals PLC (U.K.)

- Mallinckrodt Pharmaceuticals (U.S.)

- Assertio Therapeutics, Inc. (U.S)

What are the Recent Developments in Global Arachnoiditis Treatment Market?

- In December 2025, Pain News Network reported evolving clinical updates on adhesive arachnoiditis treatment protocols, highlighting a structured multimodal approach combining anti-inflammatory therapy, neuro-regenerative support, and pain control strategies. The updated protocol emphasized corticosteroids, ketorolac, and opioid-based rescue therapy for severe cases while also integrating supportive lifestyle measures

- In November 2025, a large-scale cross-sectional AI-assisted study published on medRxiv analyzed over 1,100 arachnoiditis cases and highlighted increasing adoption of multimodal pain management strategies. The study found growing clinical reliance on combinations of pharmacological therapy, nerve modulation techniques, and rehabilitation-based care for symptom control

- In October 2025, the American Syringomyelia & Chiari Alliance Project hosted a clinical update presentation reviewing new insights into arachnoiditis disease biology and treatment limitations. Experts emphasized that while no curative therapy exists, interventional pain management such as spinal cord stimulation is being evaluated for neuropathic pain relief

- In March 2025, research published via Arachnoiditis Hope discussed findings from a “Stopping Deterioration Study” focused on adhesive arachnoiditis progression control strategies. The study explored inflammation suppression and nerve regeneration concepts as potential therapeutic directions to slow neurological decline. It highlighted the urgent need for disease-modifying approaches beyond symptomatic pain relief

- In December 2024, arXiv published research on non-invasive temporal interference (TI) electrical stimulation for spinal cord injury rehabilitation, indicating emerging interest in neuromodulation-based pain control strategies. The study demonstrated that targeted electrical stimulation may improve motor and sensory function while reducing pain symptoms, suggesting potential applicability for severe chronic spinal disorders like arachnoiditis in future clinical settings.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.