Global Arenavirus Infections Treatment Market

Market Size in USD Billion

USD

1.25 Billion

USD

1.73 Billion

2025

2033

USD

1.25 Billion

USD

1.73 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.25 Billion | |

| USD 1.73 Billion | |

| % | |

|

Arenavirus Infections Treatment Market Size

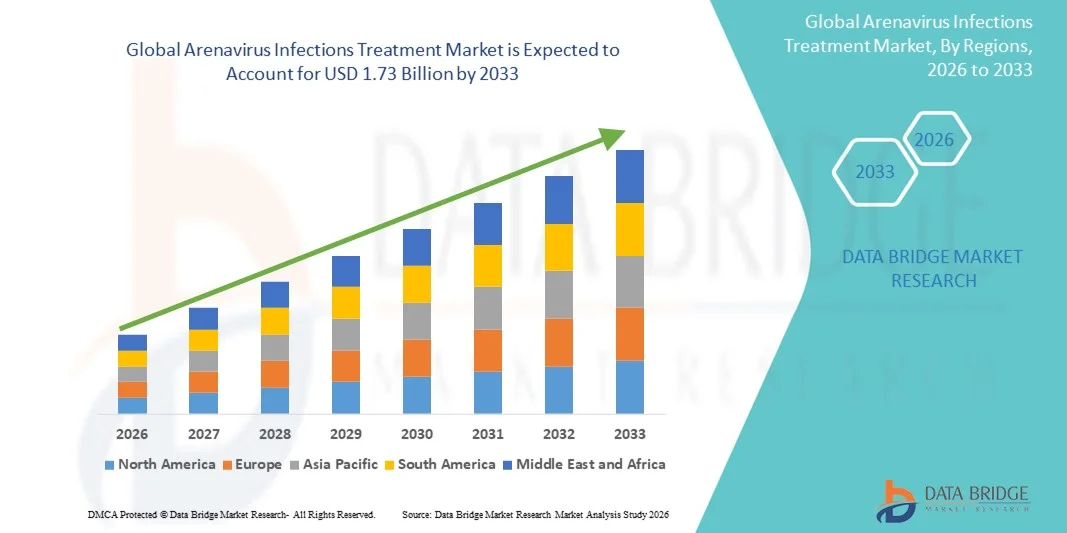

- The global arenavirus infections treatment market size was valued at USD 1.25 billion in 2025 and is expected to reach USD 1.73 billion by 2033, at a CAGR of 4.20% during the forecast period

- The market growth is largely driven by the rising prevalence of arenavirus-related diseases such as Lassa fever across endemic regions, coupled with increasing global focus on outbreak preparedness, antiviral development, and public health surveillance systems

- Furthermore, growing investment in advanced therapeutics, including broad-spectrum antivirals, immunotherapies, and supportive care solutions, is reinforcing the need for more effective treatment options. These converging factors are accelerating the adoption of arenavirus treatment modalities, thereby significantly boosting the industry’s growth

Arenavirus Infections Treatment Market Analysis

- Arenavirus infections treatment solutions, encompassing antivirals, supportive therapies, and symptomatic management, are becoming increasingly critical within global infectious disease control due to expanding endemic regions, rising viral spillover events, and the growing need for rapid-response treatments against pathogens such as Lassa virus and other hemorrhagic fever–causing arenaviruses

- The escalating demand for arenavirus treatments is primarily fueled by increasing outbreaks in West Africa, heightened global health security concerns, improved diagnostic capabilities, and a rising preference for therapeutic regimens that reduce fatality rates and enhance clinical outcomes

- North America dominated the arenavirus infections treatment market with the largest revenue share of 38.9% in 2025, supported by advanced R&D infrastructure, strong government funding for antiviral research, and active participation of biotech firms developing novel therapies, with the U.S. seeing increased clinical trials, vaccine innovation, and federal preparedness initiatives

- Asia-Pacific is expected to be the fastest-growing region in the arenavirus infections treatment market during the forecast period due to strengthened surveillance programs, rising healthcare expenditure, and increasing regional awareness of viral hemorrhagic fevers

- Ribavirin segment dominated the arenavirus infections treatment market with a market share of 41.7% in 2025, driven by its long-standing use as the primary therapeutic option for Lassa fever, established clinical effectiveness, and continued inclusion in treatment protocols across affected regions

Report Scope and Arenavirus Infections Treatment Market Segmentation

|

Attributes |

Arenavirus Infections Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Arenavirus Infections Treatment Market Trends

Advancements in Antiviral Innovation and AI-Assisted Disease Surveillance

- A significant and accelerating trend in the global arenavirus infections treatment market is the deepening integration of advanced antiviral research with AI-powered epidemic surveillance systems, enabling faster detection, improved prediction of outbreak patterns, and enhanced treatment responsiveness across endemic and non-endemic regions

- For instance, AI-enabled surveillance platforms used by institutions in West Africa and the U.S. help identify unusual fever clusters linked to Lassa virus transmission, enabling early deployment of medical resources and accelerating treatment interventions

- AI integration in arenavirus research enables capabilities such as modeling viral mutation pathways, improving antiviral candidate screening, and generating more accurate risk alerts based on real-time epidemiological data. For instance, several biotech firms use AI algorithms to optimize ribavirin dosing research and predict patient response patterns for severe arenavirus infections

- The seamless integration of antiviral development with digital monitoring systems supports centralized oversight of outbreak dynamics, treatment inventory, and clinical case management, allowing health agencies to coordinate diagnostics, therapeutics, and quarantine protocols through unified platforms

- This trend toward more intelligent, data-driven, and interconnected epidemic management systems is reshaping expectations for infectious disease preparedness. Consequently, companies and research groups such as CEPI are accelerating AI-assisted therapeutic development targeting Lassa virus and related arenaviruses

- The demand for arenavirus treatments supported by AI-enabled surveillance and early-warning systems is growing rapidly across both developed and developing regions, as healthcare systems seek improved preparedness and rapid-response capabilities

Arenavirus Infections Treatment Market Dynamics

Driver

Growing Need Due to Increasing Outbreak Frequency and Global Health Preparedness Efforts

- The rising prevalence of arenavirus outbreaks in endemic regions, coupled with growing global investment in pandemic preparedness initiatives, is a significant driver accelerating the demand for effective arenavirus infection treatments

- For instance, in March 2025, several public health agencies in Nigeria expanded Lassa fever treatment programs and partnered with research institutions to strengthen antiviral supply chains, supporting broader therapeutic adoption during peak transmission seasons

- As awareness increases regarding the severe complications of arenavirus infections, treatments such as ribavirin and supportive care protocols gain prominence due to their ability to reduce mortality when administered early in the infection cycle

- Furthermore, the global focus on emerging infectious diseases and the push for rapid-response healthcare capabilities are making arenavirus therapies a priority area, supported by international funding, clinical research collaborations, and accelerated regulatory pathways

- The availability of improved diagnostics, expanded hospital treatment capacities, and strengthened surveillance systems are key factors propelling broader adoption of arenavirus treatment protocols across Africa, North America, and parts of Asia

- The movement toward integrated epidemic preparedness initiatives and increased investment in antiviral development further contributes to steady market growth

Restraint/Challenge

Treatment Access Limitations and Regulatory Compliance Hurdles

- Challenges surrounding limited access to timely treatment in remote or resource-constrained regions, along with complex regulatory requirements for antiviral approvals, pose significant barriers to widespread arenavirus treatment adoption

- For instance, delayed reporting of suspected Lassa fever cases and constrained healthcare infrastructure in rural West Africa often lead to late treatment initiation, reducing therapeutic effectiveness and contributing to higher fatality rates

- Addressing these treatment accessibility issues through expanded diagnostic capacity, specialized training, and broader medicine distribution networks is crucial for improving patient outcomes. Several health programs emphasize early detection and rapid treatment initiation to mitigate disease severity

- In addition, the high cost of antiviral development and the stringent regulatory processes required for approval of therapies targeting high-risk pathogens can slow innovation and limit the availability of newer treatment options

- While global funding is increasing, many regions still face affordability challenges due to limited healthcare budgets, creating gaps in accessibility to advanced therapeutics and hospital-based care

- Overcoming these challenges through international funding support, accelerated approval pathways, improved supply chains, and greater investment in affordable treatment options will be vital for long-term market growth

Arenavirus Infections Treatment Market Scope

The market is segmented on the basis of treatment, dosage, route of administration, diagnosis, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the global arenavirus infections treatment market is segmented into ribavirin, antipyretic, anti-inflammatory, anticonvulsants, and others. The Ribavirin segment dominated the market with the largest market revenue share of 41.7% in 2025, driven by its long-standing clinical use and inclusion in most treatment protocols for severe arenavirus infections such as Lassa fever. Ribavirin’s established safety profile (when used under clinical supervision), widespread stockpiling by health authorities in endemic regions, and presence in national treatment guidelines make it the primary therapeutic choice in many settings. Hospitals and infectious disease centers often prioritize ribavirin for early intervention because timely administration has been associated with improved survival in observational studies. Strong supply-chain channels and existing generic manufacturing capacity also support ribavirin’s dominant market position. In addition, ribavirin’s oral and parenteral formulations allow flexible use across inpatient and emergency settings, reinforcing steady demand. Continued clinical familiarity among practitioners and inclusion in donor-funded treatment programs further sustain its market share.

The Others segment (comprising emerging broad-spectrum antivirals, monoclonal antibodies, and novel immunotherapies) is expected to witness the fastest CAGR of 22.3% from 2026 to 2033, fuelled by increased R&D investment and accelerated regulatory pathways for therapies addressing high-consequence pathogens. For instance, several biotech programs focused on pan-arenavirus candidates and antibody therapies are progressing through preclinical and early clinical stages, attracting public-private funding. The “Others” bucket benefits from technology advances (e.g., platform antiviral approaches) that enable faster lead identification and scalable production. Growing interest in stockpiling next-generation therapeutics for outbreak preparedness has incentivized developers to pursue licensure and emergency use pathways. Moreover, successful demonstration of improved efficacy or single-dose regimens would rapidly shift clinical practice, creating outsized growth relative to established drugs. Partnerships between global health agencies and industry to de-risk development also accelerate commercialization, making “Others” the fastest growing subsegment.

- By Dosage

On the basis of dosage, the market is segmented into tablet, capsule, solution, and others. The Solution dosage segment dominated the market with a revenue share of 46.2% in 2025, largely because many severe arenavirus cases present to hospitals where intravenous or parenteral solutions are standard for rapid drug delivery and supportive care. Solutions facilitate controlled dosing in critically ill patients, enable rapid onset of action, and are preferred during initial stabilization and intensive care management. Hospital formularies and emergency treatment protocols commonly stock solution formulations, which supports higher institutional purchasing volumes compared with outpatient forms. The need for injectable solutions is further driven by patients who cannot tolerate oral intake due to vomiting or altered consciousness during hemorrhagic presentations. Procurement through national health programs and international emergency stockpiles often targets solution formulations for frontline response. Clinical practice patterns that favor IV administration in severe disease thereby maintain the solution segment’s dominance.

The Tablet dosage segment is expected to register the fastest CAGR of 19.1% from 2026 to 2033, propelled by decentralization of care, improved outpatient diagnostic capacity, and the push to enable early oral treatment in remote or resource-limited settings. For instance, orally administered formulations that enable treatment initiation at peripheral clinics or via community health workers reduce time-to-treatment and hospital burden. Tablets simplify storage and distribution compared with cold-chain or parenteral requirements, making them attractive for large-scale prophylaxis or post-exposure use in outbreak scenarios. Pharmaceutical companies are also prioritizing oral formulations in development pipelines to increase accessibility and adherence. As point-of-care diagnostics improve, earlier case identification will shift some treatment to outpatient oral regimens, boosting tablet uptake. Increased acceptance of telemedicine and home therapy models further supports tablet growth.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, subcutaneous, and others. The Oral route dominated the market with a revenue share of 53.0% in 2025, reflecting the combined prevalence of oral antiviral regimens for mild to moderate cases, ease of distribution, and patient preference for non-invasive therapy. Oral administration enables outpatient management, reduces need for hospital beds, and lowers overall treatment costs—critical factors in regions with constrained inpatient capacity. Many national treatment guidelines and community health programs favor oral therapy when clinically appropriate, increasing procurement at the primary care level. Oral drugs also facilitate rapid scale-up during outbreaks because they do not require sterile administration or extensive clinical infrastructure. Patient adherence programs and simplified dosing schedules for oral medicines further bolster their market penetration. The convenience and logistical advantages of oral therapies make them the default route wherever clinical severity permits.

The Subcutaneous route is projected to be the fastest growing with a CAGR of 17.8% from 2026 to 2033, owing to the emergence of long-acting antibody and antiviral depot formulations that can be administered subcutaneously for prolonged protection or therapeutic effect. For instance, novel monoclonal antibodies designed for single-dose subcutaneous use offer outpatient delivery of potent neutralizing activity, reducing the need for IV infusions and inpatient care. Subcutaneous administration is also more feasible in field or community settings than IV therapy and can be performed by trained non-physician health workers, expanding access. Advances in formulation science that increase bioavailability and stability of subcutaneous products are accelerating clinical development. If long-acting subcutaneous options demonstrate durable protection or therapeutic benefit, adoption across prophylactic and treatment use cases will rise rapidly, driving this route’s growth.

- By Diagnosis

On the basis of diagnosis, the market is segmented into blood tests, laboratory tests, and others. The Laboratory Tests segment dominated the market with a share of 49.4% in 2025, driven by the central role of molecular diagnostics (PCR) and centralized laboratory confirmation in diagnosing arenavirus infections and guiding treatment decisions. Reference and regional labs perform confirmatory testing, viral load monitoring, and sequencing services that are critical for clinical management and surveillance. Health systems rely on laboratory infrastructure to differentiate arenaviruses from other febrile illnesses and to identify co-infections that affect therapeutic strategy. Investment in centralized diagnostic capacity by governments and international partners during outbreak responses sustains the laboratory tests segment. Laboratory confirmations are often required for reporting, case management, and eligibility for certain treatment programs or clinical trials, which further anchors demand. Quality control, accreditation, and cross-border sample referral networks also concentrate diagnostic spend in laboratory testing.

The Blood Tests segment (rapid point-of-care antigen and serology tests) is expected to be the fastest growing with a CAGR of 24.0% from 2026 to 2033, as technological advances produce faster, cheaper, and more accurate bedside diagnostics that enable immediate triage and early treatment initiation. For instance, validated rapid antigen kits allow clinicians in peripheral clinics to make treatment decisions within hours rather than days, improving outcomes. The expansion of decentralized testing, greater investment in point-of-care platforms, and integration of rapid tests into community surveillance programs drive adoption. Donor funding aimed at outbreak containment also prioritizes deployable blood-based rapid diagnostics, accelerating procurement. As sensitivity and specificity of point-of-care tests improve, clinicians will increasingly rely on them to initiate antiviral therapy earlier, favoring market growth in this subsegment.

- By End-Users

On the basis of end-users, the market is segmented into clinic, hospital, and others. The Hospital end-user segment dominated the market with a revenue share of 58.7% in 2025, reflecting that severe arenavirus cases require inpatient management, intensive supportive care, and parenteral therapy that are only available in hospital settings. Hospitals account for the bulk of high-value purchases (IV solutions, monitoring equipment, ICU beds) and are central to clinical trials and specialist care pathways for hemorrhagic presentations. Procurement contracts, government reimbursement schemes, and emergency stockpiles further channel major spending through hospitals. Referral systems in endemic regions concentrate complicated cases at tertiary hospitals, sustaining high volumes of hospital-based treatment. In addition, hospitals remain key hubs for training, protocol development, and stewardship programs that standardize use of antivirals and supportive therapies.

The Clinic segment is expected to witness the fastest CAGR of 20.5% from 2026 to 2033, driven by decentralization of care and efforts to expand early diagnosis and treatment at the primary care level to reduce delays in therapy. For instance, as rapid diagnostics and oral treatment options become more available, community clinics and outpatient centers will initiate treatment earlier and manage a higher share of mild-to-moderate cases. Strengthened primary healthcare networks, task-shifting to community health workers, and public health campaigns to increase care-seeking behavior all bolster clinic demand. Clinics also play a crucial role in post-discharge follow-up and surveillance, further increasing service volumes and associated procurement of outpatient formulations and diagnostics.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy channel dominated the market with a revenue share of 62.4% in 2025, as hospitals procure and dispense the majority of high-value therapeutics (IV formulations, specialty antivirals) and maintain emergency inventories for outbreak response. Hospital pharmacies are integrated with clinical care teams and directly support inpatient dosing, therapeutic drug monitoring, and stewardship activities. Bulk purchasing agreements, public health procurement, and donor supply chains often allocate stock to hospital pharmacies first to ensure readiness for severe case care. Hospital pharmacy distribution also handles complex cold-chain and controlled-substance logistics that retail channels may not support. The centrality of hospitals in treating severe arenavirus cases therefore keeps hospital pharmacies at the forefront of market share.

The Online Pharmacy channel is expected to be the fastest growing with a CAGR of 28.7% from 2026 to 2033, propelled by expanding e-commerce in healthcare, improved telemedicine links, and demand for home delivery of outpatient medicines and diagnostics. For instance, online pharmacies enable rapid replenishment of oral antivirals, symptom-management drugs, and self-test kits to patients in urban and peri-urban areas, reducing barriers to access. Regulatory modernization in some countries that permits online dispensing, combined with logistics partners able to reach remote areas, accelerates adoption. The convenience, price-comparison features, and integration with telehealth consultations make online channels an increasingly attractive option for outpatient management and prophylactic distribution, driving strong growth.

Arenavirus Infections Treatment Market Regional Analysis

- North America dominated the arenavirus infections treatment market with the largest revenue share of 38.9% in 2025, supported by advanced R&D infrastructure, strong government funding for antiviral research, and active participation of biotech firms developing novel therapies, with the U.S. seeing increased clinical trials, vaccine innovation, and federal preparedness initiatives

- The region’s leadership is supported by well-established healthcare infrastructure, strong R&D investments, and faster regulatory approvals, enabling timely availability of advanced diagnostic tools and treatment options

- In addition, high awareness of viral hemorrhagic fevers among clinicians, strong government preparedness programs, and increasing emphasis on early diagnosis and outbreak response have solidified North America’s position as the leading regional market for arenavirus infection treatment

U.S. Arenavirus Infections Treatment Market Insight

The U.S. arenavirus infections treatment market captured the largest revenue share of 82% in 2025 within North America, driven by well-established infectious disease surveillance systems and strong preparedness initiatives for viral hemorrhagic fevers. The rising focus on early diagnosis, rapid hospitalization, and access to antiviral therapies such as ribavirin continues to support market expansion. Growing investment in high-containment laboratories, coupled with continuous monitoring of imported cases from endemic regions, further fuels demand for advanced therapeutics. Moreover, the country’s leadership in vaccine R&D, integrated emergency response infrastructure, and accelerated regulatory pathways significantly bolster market growth.

Europe Arenavirus Infections Treatment Market Insight

The Europe arenavirus infections treatment market is projected to expand at a steady CAGR throughout the forecast period, supported by stringent infectious-disease control policies and an increasing emphasis on outbreak preparedness. Rising awareness among clinicians, improvements in laboratory diagnostic capabilities, and coordinated public health responses across EU member states are elevating treatment uptake. The region is witnessing growing adoption of antiviral medications, supportive care protocols, and rapid diagnostic tools across hospitals and emergency care settings. Enhanced government funding for zoonotic disease monitoring and increased focus on travel-related infection management are further contributing to market growth.

U.K. Arenavirus Infections Treatment Market Insight

The U.K. arenavirus infections treatment market is anticipated to grow at a noteworthy CAGR over the forecast period, driven by the increasing prioritization of viral hemorrhagic fever preparedness and robust infectious-disease management frameworks. Heightened concern over travel-associated arenavirus cases, especially among returning travelers from endemic regions, is encouraging wider availability of diagnostics and antiviral care pathways. The U.K.’s strong public health system, together with advanced laboratory networks and national response strategies, continues to support treatment adoption. In addition, ongoing investments in pathogen surveillance and emergency medical readiness are expected to propel future market expansion.

Germany Arenavirus Infections Treatment Market Insight

The Germany arenavirus infections treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing emphasis on biosafety measures and demand for advanced viral diagnostic capabilities. Germany’s highly developed healthcare infrastructure, including specialized isolation units and BSL-3/BSL-4 facilities, promotes swift intervention and effective treatment delivery. The nation’s commitment to medical innovation, strong pharmaceutical manufacturing capacity, and continuous investment in infectious-disease research contribute to greater accessibility of antiviral therapies and critical care solutions. Enhanced public awareness and rapid adoption of modern diagnostic platforms further support market growth.

Asia-Pacific Arenavirus Infections Treatment Market Insight

The Asia-Pacific arenavirus infections treatment market is poised to grow at the fastest CAGR of around 23% during 2026–2033, driven by rising healthcare modernization, improving diagnostic infrastructure, and increasing government attention to zoonotic and emerging viral diseases. Countries such as China, Japan, and India are rapidly upgrading laboratory networks and adopting advanced outbreak-response tools, which support broader treatment access. Growing medical tourism, rising investments in antiviral research, and expanding awareness among clinicians of rare viral fevers are amplifying regional growth. In addition, Asia-Pacific’s increasing role in pharmaceutical manufacturing continues to improve affordability and availability of treatment options.

Japan Arenavirus Infections Treatment Market Insight

The Japan arenavirus infections treatment market is gaining momentum due to the country’s strong infectious-disease management framework and high technological adoption in the healthcare sector. Japan places significant emphasis on early detection and rapid containment of viral pathogens, driving demand for advanced diagnostic tests and antiviral therapeutics. Integration of arenavirus diagnostics with hospital information systems, along with the rise of smart medical monitoring devices, is supporting better patient outcomes. Furthermore, the aging population and increasing focus on infection prevention within healthcare facilities are contributing to sustained market demand.

India Arenavirus Infections Treatment Market Insight

The India arenavirus infections treatment market accounted for the largest regional revenue share in Asia-Pacific in 2025, driven by rapid improvements in healthcare accessibility, expanding diagnostic coverage, and rising awareness of emerging infectious diseases. India’s growing urban population, increasing cases of travel-associated viral infections, and strengthening public health surveillance systems are accelerating the adoption of antiviral and supportive care therapies. Government initiatives to expand laboratory capacity, coupled with the presence of strong domestic pharmaceutical manufacturers, are significantly contributing to market expansion. In addition, increasing participation in clinical research collaborations is enhancing the country’s role in arenavirus treatment development.

Arenavirus Infections Treatment Market Share

The Arenavirus Infections Treatment industry is primarily led by well-established companies, including:

- Zalgen Labs (U.S.)

- Ridgeback Biotherapeutics (U.S.)

- Emergent BioSolutions (U.S.)

- SIGA Technologies (U.S.)

- Profectus BioSciences (U.S.)

- Dr. Reddy's Laboratories Ltd. (India)

- Natco Pharma Ltd. (India)

- Cipla Limited (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Hetero Labs Ltd. (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Viatris Inc. (U.S.)

- Glenmark Pharmaceuticals Ltd. (India)

- Abbott (U.S.)

- Roche (Switzerland)

- BIOMÉRIEUX (France)

- QIAGEN (Netherlands)

- Moderna, Inc. (U.S.)

- Pfizer Inc. (U.S.)

What are the Recent Developments in Global Arenavirus Infections Treatment Market?

- In December 2024, the U.S. CDC-led researchers demonstrated that an oral antiviral, 4′-fluorouridine (4′-FlU), was highly effective in animal models protecting guinea pigs from lethal Lassa virus (and Junín virus) even when treatment was delayed, suggesting strong potential for a broad-spectrum arenavirus therapeutic

- In May 2024, The Guardian reported that Nigeria initiated the first clinical trials for Lassa fever treatment in four decades, marking a historic turning point for arenavirus therapeutics. Led by the multinational INTEGRATE consortium, the trials aim to test multiple promising drug candidates including new antivirals and repurposed medications in regions where Lassa cases are endemic

- In August 2023, scientists at the University of Texas Medical Branch (UTMB), together with Zalgen Labs, announced a major milestone: Arevirumab-3, a monoclonal antibody cocktail, successfully cured Lassa-infected macaques even when given during advanced stages of illness

- In October 2022, the CDC published documented cases in Nigeria where two patients with confirmed Lassa fever were successfully treated using a combination of ribavirin and dexamethasone. The report noted that the addition of dexamethasone, typically used to control severe inflammatory responses, contributed to favorable clinical outcomes

- In March 2021, Kineta announced at the International Conference on Antiviral Research (ICAR) that its antiviral candidate LHF-535 demonstrated strong safety, tolerability, and predictable pharmacokinetics in healthy volunteers. This molecule is engineered to inhibit viral entry of arenaviruses such as Lassa virus, and the results strengthened its potential to advance into further clinical development

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.