Global Arnold Chiari Treatment Market

Market Size in USD Billion

USD

2.21 Billion

USD

3.64 Billion

2025

2033

USD

2.21 Billion

USD

3.64 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.21 Billion | |

| USD 3.64 Billion | |

| % | |

|

Arnold-Chiari Treatment Market Overview

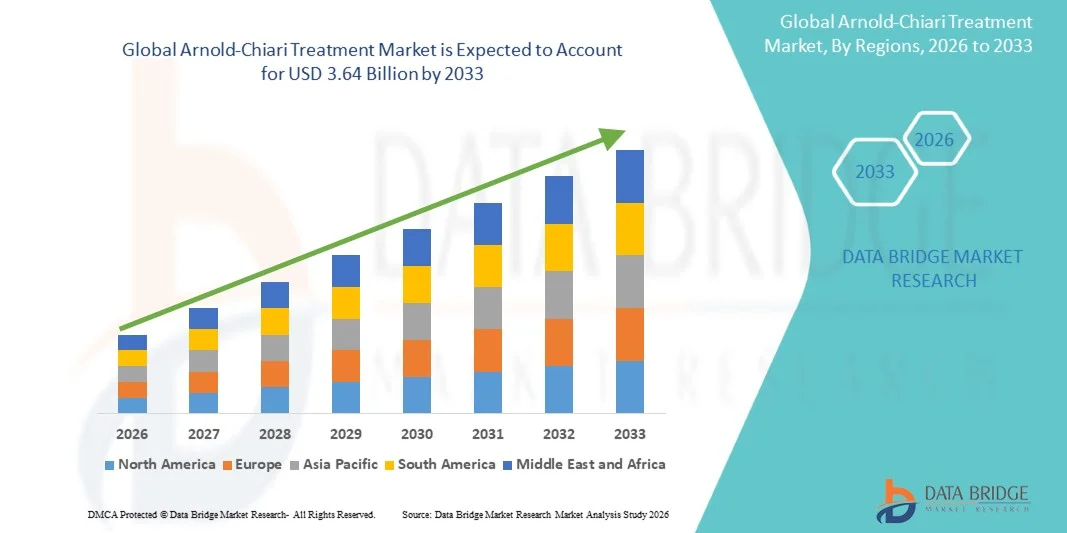

The Arnold-Chiari Treatment Market was valued at USD 2.21 billion in 2025 and is projected to reach USD 3.64 billion by 2033, growing at a CAGR of 6.45% from 2026 to 2033. The market is experiencing steady growth driven by increasing diagnosis rates of Arnold-Chiari malformation, improved access to advanced neuroimaging techniques such as MRI, and rising awareness of neurological disorders among patients and healthcare providers. The growing prevalence of congenital brain and spinal abnormalities, particularly Chiari Type I malformation, is further contributing to higher demand for timely and effective treatment options.

The increasing adoption of minimally invasive neurosurgical procedures, combined with advancements in surgical techniques such as posterior fossa decompression, is significantly improving patient outcomes and reducing postoperative complications. In addition, expanding healthcare infrastructure, rising neurosurgical expertise in emerging economies, and growing investments in neurological disorder research are supporting market expansion. Improved insurance coverage for complex neurosurgical treatments and increasing patient preference for early intervention are further accelerating adoption of advanced treatment approaches globally.

Key Market Trends & Insights

- North America dominated the Arnold-Chiari Treatment Market with the largest revenue share of 38.76% in 2025, driven by advanced neurosurgical infrastructure, high awareness and early diagnosis of Chiari malformations, strong availability of MRI-based diagnostic systems, and the presence of leading neurological care centers. Increasing adoption of minimally invasive decompression surgeries and improved access to specialized neurological care further support regional market growth.

- MRI dominates the market with a share of 71.34% in 2025 due to its superior ability to detect structural brain abnormalities and cerebrospinal fluid flow disruption.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by improving neurological healthcare infrastructure, rising awareness of congenital neurological disorders, increasing access to advanced imaging technologies, and growing healthcare expenditure across China, India, Japan, and Southeast Asia.

- MRI Diagnosis segment is projected to be the fastest-growing diagnostic category, registering a CAGR of 7.8%, due to its high accuracy in detecting cerebellar tonsillar herniation, spinal cord abnormalities, and associated syringomyelia without radiation exposure.

- Type I Arnold-Chiari malformation dominates the disease type segment with a 54.19% revenue share in 2025, as it is the most commonly diagnosed form, often detected incidentally or during evaluation of chronic headaches and neurological symptoms.

- Hospital End-Users accounted for 57.83% of the market in 2025, driven by high patient inflow, availability of advanced neurosurgical facilities, and increased preference for hospital-based diagnosis and surgical intervention.

Market Size & Forecast

- Global Market Value (2025): USD 2.21 Billion

- Expected Market Value (2033): USD 3.64 Billion

- Forecast CAGR (2026–2033): 6.45%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Arnold-Chiari Treatment Market Segmentation

|

Attributes |

Arnold-Chiari Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Abbott Laboratories (U.S.) |

|

Market Opportunities |

· Expansion of Minimally Invasive Neurosurgical Procedures · Rising Demand for Advanced Neuroimaging and Early Diagnosis · Growth in Post-Surgical Rehabilitation and Long-Term Care Services |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Arnold-Chiari Treatment Market Trends

Trend: Rising Adoption of Advanced Neuroimaging and Minimally Invasive Neurosurgical Techniques

The Arnold-Chiari Treatment market is witnessing a growing shift toward early and accurate diagnosis supported by high-resolution neuroimaging technologies such as MRI and CT scans. MRI remains the gold standard, with studies indicating diagnostic accuracy exceeding 90% in detecting cerebellar tonsillar herniation and associated syringomyelia. Increasing use of cine MRI to evaluate cerebrospinal fluid (CSF) flow dynamics is further improving clinical decision-making.

On the treatment side, there is a strong trend toward minimally invasive posterior fossa decompression surgeries, which reduce hospital stay, recovery time, and postoperative complications. According to neurosurgical clinical reports, minimally invasive techniques can reduce postoperative recovery time by up to 30–40% compared to traditional open procedures. Growing adoption of image-guided navigation and microsurgical tools is also improving surgical precision and patient outcomes globally.

Arnold-Chiari Treatment Market Dynamics

Key Market Driver: Rising Incidence and Improved Diagnosis of Congenital Neurological Disorders

The increasing detection of Arnold-Chiari malformations, particularly Type I, is a key driver of market growth. Improved access to MRI imaging and rising awareness among clinicians have led to higher diagnosis rates, especially in asymptomatic or mildly symptomatic patients. It is estimated that Chiari malformation affects approximately 1 in 1,000 individuals globally, though many cases remain undiagnosed.

In addition, growing prevalence of associated conditions such as syringomyelia, hydrocephalus, and spinal cord abnormalities is increasing demand for both diagnostic and surgical interventions. Expansion of specialized neurology and neurosurgery centers, along with improved healthcare infrastructure in emerging economies, is further driving market growth. Technological advancements in intraoperative imaging and neuro-navigation systems are also enhancing surgical precision and outcomes.

Key Restraint/Challenge: High Surgical Risk and Limited Access to Specialized Neurosurgical Care

A major challenge in the Arnold-Chiari Treatment market is the complexity and risk associated with neurosurgical procedures. Posterior fossa decompression surgery carries risks such as cerebrospinal fluid leakage, infection, and neurological complications, requiring highly skilled neurosurgeons and specialized hospital infrastructure.

In many low- and middle-income regions, limited access to advanced neuroimaging tools, trained neurosurgeons, and postoperative care facilities restricts treatment availability. Additionally, high surgical costs and variability in insurance coverage further limit patient access. Delayed diagnosis due to nonspecific symptoms such as headaches, dizziness, and balance disorders also contributes to under-treatment in several regions.

Key Market Opportunity: Expansion of AI-Assisted Diagnosis and Precision Neurosurgery

The integration of artificial intelligence and advanced imaging analytics presents a significant opportunity in the Arnold-Chiari Treatment market. AI-based image interpretation tools are increasingly being used to detect structural brain abnormalities earlier and more accurately, reducing diagnostic delays.

In addition, the adoption of robot-assisted neurosurgery and intraoperative MRI systems is improving surgical precision and reducing complication rates. Growing investments in neurology-focused healthcare infrastructure in Asia-Pacific and Latin America are expanding access to advanced treatment options. Collaborative research in genetic and congenital neurological disorders is also expected to enhance understanding of disease progression, enabling more personalized treatment approaches in the coming years.

Arnold-Chiari Treatment Market Scope

The Arnold-Chiari Treatment market is segmented on the basis of Type, Treatment, Diagnosis, End-Users, and Distribution Channel.

- By Type

On the basis of type, the Arnold-Chiari Treatment Market is segmented into Type 1, Type 2, Type 3, and Type 4. Type 1 dominates the market with a share of 62.18% in 2025, driven by its higher prevalence in adult populations and frequent incidental detection through MRI imaging. Type 2 is commonly associated with pediatric cases and spina bifida, requiring early medical intervention. Type 3 and Type 4 are rare but severe forms with high neurological complication risks. Rising awareness of congenital brain disorders is increasing diagnosis rates. Expanding access to advanced neuroimaging is improving early detection. Growing neurological disorder burden is increasing treatment demand. Rising neurosurgical procedures are supporting market growth. Increasing hospital neurology infrastructure is improving patient outcomes. Growing adoption of minimally invasive decompression surgery is enhancing recovery rates. Increasing government focus on rare disease management is boosting screening programs. Improved reimbursement frameworks are increasing treatment affordability. Expanding clinical research in Chiari malformations is strengthening disease understanding.

The Type 2 segment is expected to witness the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by rising pediatric diagnosis rates, increasing prenatal screening programs, and improved early detection of congenital neurological abnormalities. Expanding neonatal healthcare infrastructure is enabling timely intervention and treatment. Growing awareness among parents and healthcare providers is improving early consultation rates. Increasing availability of advanced MRI imaging in pediatric hospitals is enhancing diagnostic accuracy. Rising survival rates of infants with congenital disorders are increasing long-term treatment demand. Expanding government neonatal screening initiatives are supporting early disease identification. Growth in specialized pediatric neurology centers is improving access to expert care. Increasing adoption of minimally invasive pediatric neurosurgery is improving clinical outcomes. Rising healthcare expenditure on child neurology is strengthening treatment infrastructure. Technological advancements in fetal imaging are improving prenatal diagnosis capabilities. Increasing clinical trials focused on pediatric Chiari malformations are supporting innovation. Overall, Type 2 is emerging as the fastest-growing segment due to strong pediatric healthcare expansion.

- By Treatment

On the basis of treatment, the Arnold-Chiari Treatment Market is segmented into Medical Treatment and Surgical Treatment. Surgical Treatment dominates the market with a share of 68.45% in 2025 due to its high effectiveness in relieving cerebrospinal fluid obstruction through posterior fossa decompression surgery. Medical treatment is mainly used for symptom management in mild cases and includes pain relievers, muscle relaxants, and anti-inflammatory drugs. Rising prevalence of neurological symptoms is increasing surgical intervention rates. Growing adoption of minimally invasive neurosurgery is improving recovery outcomes. Increasing availability of advanced surgical tools is enhancing procedural precision. Expansion of neurosurgery departments in hospitals is improving access to care. Rising healthcare spending is supporting complex surgical procedures. Increasing clinical evidence supporting decompression surgery is strengthening adoption. Growing patient awareness of surgical benefits is increasing acceptance rates. Expansion of specialized neurosurgical centers is improving treatment availability. Rising use of neuronavigation systems is enhancing surgical accuracy. Increasing post-surgical rehabilitation services is improving long-term recovery. Overall, surgical procedures remain the dominant treatment approach globally.

The Surgical Treatment segment is expected to witness the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by increasing adoption of minimally invasive neurosurgical techniques and improved surgical success rates. Rising availability of advanced imaging-guided surgical systems is enhancing procedural accuracy. Growing preference for shorter hospital stays is supporting minimally invasive approaches. Increasing neurological disorder burden is driving higher surgical volumes. Expansion of specialized neurosurgery hospitals is improving access to treatment. Rising healthcare investments in advanced operating room technologies are supporting adoption. Increasing clinical training in complex cranial surgeries is improving surgeon expertise. Growing reimbursement support for surgical procedures is enhancing affordability. Rising awareness of early surgical intervention benefits is increasing patient acceptance. Expanding global neurosurgical infrastructure is improving treatment reach. Technological innovation in microsurgical tools is enhancing outcomes. Overall, surgical intervention is emerging as the fastest-growing treatment modality.

- By Diagnosis

On the basis of diagnosis, the Arnold-Chiari Treatment Market is segmented into X-Ray, CT-Scan, Sleep Study, Swallowing Study, Myelogram, and MRI. MRI dominates the market with a share of 71.34% in 2025 due to its superior ability to detect structural brain abnormalities and cerebrospinal fluid flow disruption. CT-Scan is widely used in emergency diagnostic settings for quick evaluation. Myelography is used when MRI is contraindicated. Sleep and swallowing studies help in assessing associated complications like apnea and dysphagia. Rising neurological disorder prevalence is increasing imaging demand. Expansion of diagnostic imaging infrastructure is improving accessibility. Increasing adoption of high-resolution MRI systems is enhancing diagnostic accuracy. Growth in hospital radiology departments is supporting early detection. Rising awareness among clinicians is improving diagnostic screening rates. Increasing AI integration in radiology is enhancing image interpretation. Government investments in diagnostic technologies are strengthening healthcare systems. Expanding neuroimaging centers are improving patient access. Overall, MRI remains the gold standard diagnostic modality.

The MRI segment is expected to witness the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by continuous advancements in high-field MRI systems and AI-powered imaging analysis. Rising adoption of 3T and 7T MRI scanners is improving diagnostic precision. Increasing focus on early neurological disease detection is driving imaging demand. Expanding hospital imaging infrastructure is supporting accessibility. Growing prevalence of congenital neurological disorders is increasing MRI utilization. Rising awareness among healthcare providers is improving screening rates. Increasing integration of AI-based image reconstruction is enhancing efficiency. Government funding for advanced imaging systems is accelerating adoption. Expanding neurological research is improving diagnostic protocols. Rising demand for non-invasive diagnostic methods is boosting MRI preference. Increasing pediatric imaging applications are expanding market scope. Overall, MRI is the fastest-growing diagnostic modality.

- By End-Users

On the basis of end-users, the Arnold-Chiari Treatment Market is segmented into Hospitals, Homecare, Specialty Clinics, and Others. Hospitals dominate the market with a share of 54.92% in 2025 due to advanced neurosurgical infrastructure and availability of multidisciplinary neurological care teams. Specialty clinics are growing due to rising outpatient consultations. Homecare services are expanding for long-term rehabilitation support. Increasing neurological disease burden is driving hospital admissions. Rising healthcare investments are strengthening neurology departments. Expansion of neurosurgical units is improving treatment access. Growing demand for postoperative care is supporting rehabilitation services. Increasing adoption of telemedicine is enhancing follow-up care. Rising awareness of brain malformations is improving diagnosis rates. Expansion of specialty neurology centers is improving care delivery. Government healthcare initiatives are strengthening hospital capacity. Increasing insurance coverage is improving affordability. Overall, hospitals remain the primary treatment centers globally.

The Specialty Clinics segment is expected to witness the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by increasing demand for specialized neurological consultations and outpatient-based care delivery. Rising preference for cost-effective treatment settings is supporting clinic adoption. Expanding availability of advanced diagnostic services in specialty centers is improving patient access. Growing neurological disease burden is increasing outpatient visits. Rising awareness of early diagnosis is boosting clinic consultations. Increasing adoption of advanced neuroimaging in clinics is improving detection rates. Expansion of neurology-focused specialty hospitals is supporting growth. Rising healthcare expenditure is improving access to specialist care. Increasing physician specialization in neurology is strengthening clinical expertise. Growth in ambulatory care services is supporting outpatient treatment models. Expanding urban healthcare infrastructure is improving accessibility. Overall, specialty clinics are emerging as the fastest-growing end-user segment.

- By Distribution Channel

On the basis of distribution channel, the Arnold-Chiari Treatment Market is segmented into Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy. Hospital Pharmacy dominates the market with a share of 63.27% in 2025 due to high dependency on inpatient medication dispensing and post-surgical drug administration. Retail pharmacies support long-term medication needs for chronic symptom management. Online pharmacies are expanding rapidly due to digital healthcare adoption. Increasing telemedicine consultations are driving online prescriptions. Rising neurological disorder prevalence is increasing drug demand. Expansion of hospital pharmacy networks is improving drug accessibility. Growth in e-prescription systems is supporting digital distribution. Increasing healthcare digitization is transforming pharmacy operations. Rising patient preference for home delivery is boosting online sales. Government support for digital health platforms is accelerating adoption. Expansion of retail pharmacy chains is improving availability. Increasing insurance coverage is enhancing affordability. Overall, hospital pharmacies remain the dominant distribution channel.

The Online Pharmacy segment is expected to witness the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by rapid digital transformation in healthcare systems and increasing adoption of telemedicine platforms. Rising smartphone penetration is enabling easy access to online prescriptions. Expanding e-pharmacy regulations are supporting market legitimacy. Increasing patient preference for home-based healthcare services is boosting demand. Growth in chronic neurological conditions is increasing long-term medication needs. Rising convenience of doorstep delivery is driving adoption. Expansion of digital health ecosystems is improving accessibility. Increasing integration of AI-driven prescription systems is enhancing efficiency. Government initiatives supporting digital healthcare are accelerating adoption. Rising urbanization is boosting online healthcare usage. Expanding healthcare startup ecosystem is supporting innovation. Overall, online pharmacy is emerging as the fastest-growing distribution channel.

Arnold-Chiari Treatment Market Regional Analysis

North America dominated the Arnold-Chiari Treatment market and accounted for the largest revenue share of 38.76% in 2025, driven by advanced neurosurgical infrastructure, high awareness and early diagnosis of Chiari malformations, strong availability of MRI-based diagnostic systems, and the presence of leading neurological care centers. The region also benefits from well-established healthcare reimbursement frameworks, high adoption of minimally invasive decompression procedures, and increasing access to specialized neurological care. Continuous technological advancements in neuroimaging and surgical navigation systems further strengthen regional market dominance.

U.S. Arnold-Chiari Treatment Market Insight

The U.S. Arnold-Chiari Treatment market is witnessing steady expansion due to rising incidence of congenital neurological disorders and strong adoption of advanced diagnostic imaging such as MRI and CT scans for early detection. Leading hospitals and neuroscience institutes are increasingly performing posterior fossa decompression surgeries using minimally invasive techniques, improving patient recovery outcomes. In addition, ongoing clinical research programs and growing investments by key players in neurology-focused therapeutics are supporting continuous innovation in treatment approaches.

Europe Arnold-Chiari Treatment Market Insight

The Europe Arnold-Chiari Treatment market remains a significant contributor to global revenue, supported by robust public healthcare systems, strong neurological research networks, and increasing access to advanced diagnostic services. Countries across the region are witnessing rising utilization of MRI-based screening for early-stage diagnosis of Chiari malformations. Furthermore, expansion of specialized neurosurgical centers and growing adoption of precision surgical planning tools are improving treatment success rates and supporting market growth.

U.K. Arnold-Chiari Treatment Market Insight

The U.K. market is experiencing steady growth driven by increased awareness of rare neurological disorders and expanding access to specialist neurology services through the National Health Service (NHS). Hospitals are increasingly adopting advanced neuroimaging and intraoperative navigation systems to improve surgical accuracy. Growing investment in neurological research and rehabilitation services is also contributing to improved long-term patient management outcomes.

Germany Arnold-Chiari Treatment Market Insight

Germany’s market is expanding due to its strong hospital infrastructure and leadership in medical technology innovation. High adoption of advanced MRI systems and neurosurgical planning software is enabling earlier and more accurate diagnosis of Arnold-Chiari malformations. German university hospitals and research institutes are also actively involved in developing improved decompression surgical techniques and post-operative rehabilitation protocols.

Asia-Pacific Arnold-Chiari Treatment Market Insight

The Asia-Pacific Arnold-Chiari Treatment market is expected to witness the fastest growth at a CAGR of 8.1% from 2026 to 2033, supported by improving neurological healthcare infrastructure, rising awareness of congenital neurological disorders, increasing access to advanced imaging technologies, and growing healthcare expenditure across emerging economies. Expansion of tertiary care hospitals and improved diagnostic penetration in rural and semi-urban regions are further accelerating regional market growth.

Japan Arnold-Chiari Treatment Market Insight

Japan is witnessing steady growth in the treatment market due to its highly advanced healthcare system and strong focus on early neurological diagnosis. Widespread availability of high-resolution MRI systems and skilled neurosurgeons enables accurate detection and management of Chiari malformations. Additionally, Japan’s emphasis on minimally invasive neurosurgical procedures and post-operative rehabilitation is improving long-term patient outcomes.

China Arnold-Chiari Treatment Market Insight

China’s market is growing rapidly due to expanding healthcare infrastructure, increasing neurological disorder awareness, and rising investments in advanced diagnostic imaging systems. Major hospitals in urban centers are increasingly adopting MRI-based screening for early diagnosis, while government healthcare reforms are improving access to specialized neurosurgical care. Continuous expansion of tertiary care networks and rising medical tourism are further supporting market growth across the country.

Arnold-Chiari Treatment Market Share

The Arnold-Chiari Treatment industry is primarily led by well-established companies, including:

- Abbott Laboratories (U.S.)

- Medtronic plc (Ireland)

- Johnson & Johnson (U.S.)

- Stryker Corporation (U.S.)

- Siemens Healthineers AG (Germany)

- GE HealthCare Technologies Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Boston Scientific Corporation (U.S.)

- B. Braun Melsungen AG (Germany)

- Karl Storz SE & Co. KG (Germany)

- Integra LifeSciences Holdings Corporation (U.S.)

- Medtronic Neurological Division (Ireland)

- Codman & Shurtleff (Integra LifeSciences) (U.S.)

- Elekta AB (Sweden)

- Zimmer Biomet Holdings Inc. (U.S.)

- Brainlab AG (Germany)

- Nihon Kohden Corporation (Japan)

- Fujifilm Holdings Corporation (Japan)

- Hitachi Medical Systems (Japan)

- Canon Medical Systems Corporation (Japan)

- Neuropace Inc. (U.S.)

- MicroPort Scientific Corporation (China)

- LivaNova PLC (U.K.)

- Penumbra Inc. (U.S.)

- Terumo Corporation (Japan)

- Cook Medical (U.S.)

- DePuy Synthes (Johnson & Johnson) (U.S.)

- ClearPoint Neuro Inc. (U.S.)

- Intra-Cellular Therapies Inc. (U.S.)

- Upsher-Smith Laboratories (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Lupin Limited (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Glenmark Pharmaceuticals Ltd. (India)

Latest Developments in Arnold-Chiari Treatment Market

- In January 2021, a comprehensive systematic review published in Acta Neurochirurgica analyzed posterior fossa decompression with and without duraplasty for Chiari I malformation, concluding that while decompression remains the gold-standard treatment, surgical technique variations significantly influence outcomes and complication rates. This study reinforced the growing clinical debate on optimal surgical approaches and highlighted the need for standardized treatment protocols in Chiari malformation management

- In March 2022, researchers published updated clinical evidence in Frontiers in Surgery emphasizing the lack of global consensus on Chiari I malformation management, noting that treatment decisions increasingly rely on individualized MRI-based assessment of cerebrospinal fluid (CSF) flow obstruction. The study highlighted the expanding role of advanced neuroimaging in pre-surgical planning and outcome prediction

- In August 2022, the World Federation of Neurosurgical Societies (WFNS) Spine Committee conducted consensus conferences in São Paulo and Porto to develop structured recommendations for Chiari malformation surgery. The resulting Delphi consensus supported posterior fossa decompression as the primary surgical option, with duraplasty recommended in adult patients and more conservative decompression in pediatric cases. This marked an important step toward global treatment standardization

- In September 2024, the Park-Reeves Syringomyelia Research Consortium (PRSRC) expanded its multi-center registry in the United States to collect large-scale clinical data on Chiari I malformation and syringomyelia patients. The initiative involves multiple academic neurosurgical centers and focuses on improving surgical outcome prediction and understanding cerebrospinal fluid dynamics, strengthening evidence-based surgical decision-making

- In April 2024, Children’s National Hospital launched a neurosurgical research initiative studying “tonsillar manipulation during Chiari I malformation surgery,” aiming to compare clinical outcomes and MRI-based structural changes in symptomatic versus incidental Chiari cases. The project reflects increasing focus on refining microsurgical techniques to improve post-operative neurological recovery

- In May 2025, a WFNS-linked surgical consensus publication reaffirmed that posterior fossa decompression remains the primary treatment approach for symptomatic Chiari malformation, but emphasized increasing use of minimally invasive decompression strategies and intraoperative dural assessment techniques to reduce complication rates such as CSF leakage and aseptic meningitis

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.