Global Artery Stenosis Drug Market

Market Size in USD Billion

USD

2.60 Billion

USD

4.11 Billion

2025

2033

USD

2.60 Billion

USD

4.11 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.60 Billion | |

| USD 4.11 Billion | |

| % | |

|

Artery Stenosis Drug Market Size

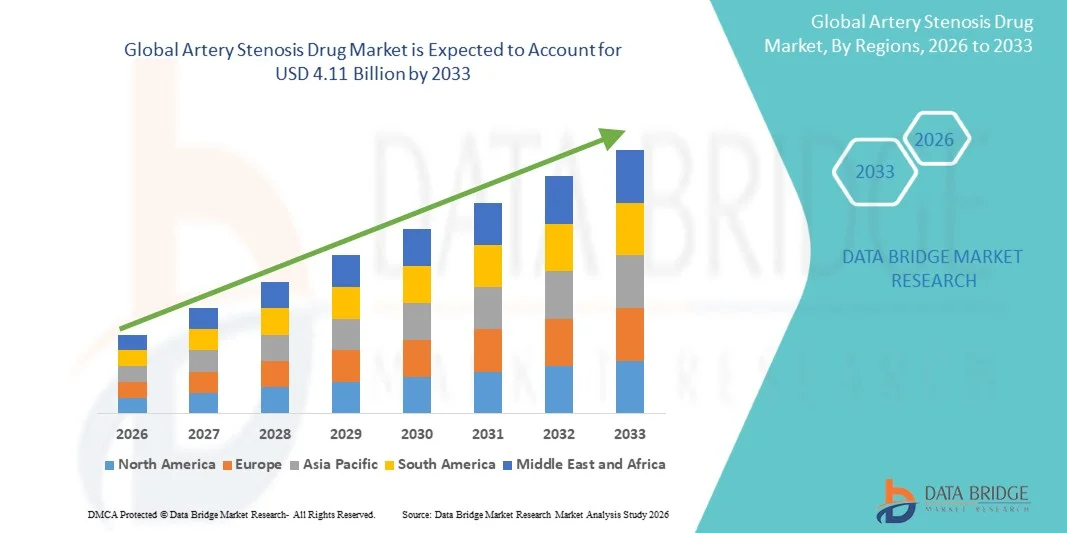

- The global artery stenosis drug market size was valued at USD 2.60 billion in 2025 and is expected to reach USD 4.11 billion by 2033, at a CAGR of 5.90% during the forecast period

- The market growth is largely driven by the increasing prevalence of cardiovascular diseases, particularly artery stenosis, along with the rising aging population that is more susceptible to such conditions, leading to greater demand for effective drug therapies

- Furthermore, advancements in pharmaceutical research and the development of targeted drug therapies are enhancing treatment outcomes and patient compliance. Growing awareness regarding early diagnosis and treatment, coupled with improved healthcare infrastructure, is positioning artery stenosis drugs as a critical component in cardiovascular disease management. These factors are collectively accelerating the adoption of artery stenosis drug solutions, thereby significantly boosting market growth

Artery Stenosis Drug Market Analysis

- Artery stenosis drugs, used to manage and treat the narrowing of arteries by improving blood flow and preventing complications such as heart attacks and strokes, are becoming increasingly essential in cardiovascular care across both hospital and outpatient settings due to their effectiveness in long-term disease management

- The rising demand for artery stenosis drugs is primarily driven by the growing global burden of cardiovascular diseases, increasing geriatric population, and heightened awareness regarding early diagnosis and preventive treatment, along with a shift toward minimally invasive and drug-based management approaches

- North America dominated the artery stenosis drug market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, and strong presence of leading pharmaceutical companies, with the U.S. witnessing significant adoption of novel and combination drug therapies for artery stenosis management

- Asia-Pacific is expected to be the fastest-growing region in the artery stenosis drug market during the forecast period, driven by rapid urbanization, improving healthcare access, rising disposable incomes, and an increasing prevalence of lifestyle-related cardiovascular disorders in countries such as China and India

- The oral segment held the largest market share of 66.7% in 2025, driven by its convenience, ease of administration, and high patient compliance

Report Scope and Artery Stenosis Drug Market Segmentation

|

Attributes |

Artery Stenosis Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Artery Stenosis Drug Market Trends

“Advancements in Minimally Invasive Therapies and Personalized Treatment Approaches”

- A significant and accelerating trend in the global artery stenosis drug market is the increasing focus on minimally invasive treatment options and the adoption of personalized medicine approaches. These advancements are significantly improving patient outcomes and enhancing overall treatment efficiency

- For instance, newer drug formulations and combination therapies are being developed to complement minimally invasive procedures such as angioplasty, ensuring better management of arterial blockages. In addition, targeted drug therapies are being tailored to individual patient profiles, improving efficacy and reducing adverse effects

- The integration of advanced diagnostics and precision medicine enables healthcare providers to identify the most effective drug regimens based on genetic, lifestyle, and clinical factors. This has led to improved treatment success rates and reduced recurrence of arterial narrowing

- Furthermore, the growing use of combination therapies, including antiplatelet agents, anticoagulants, and lipid-lowering drugs, allows for comprehensive disease management. These therapies work synergistically to prevent clot formation, reduce plaque buildup, and improve blood flow

- The shift toward patient-centric treatment and continuous innovation in drug development is transforming the management of artery stenosis. Consequently, pharmaceutical companies are focusing on developing advanced therapeutics with improved safety profiles and long-term effectiveness

- The demand for effective and targeted artery stenosis drugs is rising across both developed and developing regions, as healthcare systems increasingly prioritize early diagnosis, prevention, and long-term disease management

Artery Stenosis Drug Market Dynamics

Driver

“Rising Prevalence of Cardiovascular Diseases and Aging Population”

- The increasing prevalence of cardiovascular diseases, along with a rapidly aging global population, is a significant driver for the heightened demand for artery stenosis drugs

- For instance, the growing incidence of conditions such as atherosclerosis, hypertension, and coronary artery disease has led to a higher need for effective pharmacological interventions to manage arterial blockages

- As lifestyle-related risk factors such as poor diet, lack of physical activity, smoking, and obesity continue to rise, the burden of artery-related diseases is increasing globally, driving the demand for therapeutic solutions

- Furthermore, advancements in diagnostic technologies and increased awareness about early disease detection are encouraging timely treatment, thereby boosting drug adoption

- The availability of a wide range of medications, including statins, antiplatelet drugs, and vasodilators, along with improved healthcare infrastructure, is further supporting market growth

- The increasing focus on preventive healthcare and long-term disease management is also contributing to the sustained demand for artery stenosis drugs across both hospital and outpatient settings

Restraint/Challenge

“High Treatment Costs and Potential Side Effects of Drug Therapies”

- High treatment costs associated with long-term drug therapy and advanced treatment options pose a significant challenge to the growth of the artery stenosis drug market

- Many patients require prolonged or lifelong medication, which can lead to substantial financial burden, particularly in low- and middle-income regions

- For instance, In addition, certain artery stenosis drugs may cause side effects such as bleeding complications, liver dysfunction, or muscle-related issues, which can impact patient compliance and treatment continuity

- Concerns regarding adverse drug reactions and interactions, especially in elderly patients with multiple comorbidities, further complicate treatment strategies

- Addressing these challenges requires continuous research and development to create safer and more cost-effective drug options, along with improved patient monitoring and management practices

- While efforts are being made to reduce costs and enhance drug safety, these factors continue to limit widespread adoption, particularly among cost-sensitive populations

- Overcoming these barriers through innovation, affordability initiatives, and enhanced patient education will be crucial for ensuring sustained market growth

Artery Stenosis Drug Market Scope

The market is segmented on the basis of indication type, treatment, drugs, route of administration, distribution channel, and end-users.

• By Indication Type

On the basis of indication type, the Artery Stenosis Drug market is segmented into carotid artery stenosis, renal artery stenosis, peripheral artery stenosis, coronary artery stenosis, and others. The coronary artery stenosis segment dominated the largest market revenue share of approximately 38.6% in 2025, driven by the high global prevalence of cardiovascular diseases and increasing incidences of atherosclerosis. Coronary artery stenosis is one of the leading causes of heart attacks, making its treatment a top priority in healthcare systems worldwide. The rising geriatric population, coupled with unhealthy lifestyles such as poor diet, smoking, and lack of physical activity, significantly contributes to the dominance of this segment. In addition, advancements in diagnostic technologies and early detection methods have improved treatment rates. Government initiatives and awareness programs promoting cardiovascular health further support segment growth. The availability of a wide range of treatment options, including medications and surgical interventions, also strengthens its market position. Hospitals and specialty clinics heavily focus on coronary conditions, increasing drug demand. Continuous R&D investments by pharmaceutical companies in cardiovascular drugs further drive this segment. Increasing healthcare expenditure in both developed and developing regions also plays a crucial role.

The peripheral artery stenosis segment is expected to witness the fastest CAGR of 7.9% from 2026 to 2033, driven by the growing prevalence of diabetes and obesity, which are major risk factors for peripheral arterial diseases. Increasing awareness regarding early diagnosis and treatment of peripheral vascular conditions is boosting segment growth. Technological advancements in non-invasive diagnostic tools are making detection easier and more accessible. Rising demand for minimally invasive treatment options is also contributing to growth. In addition, the expanding geriatric population is highly susceptible to peripheral artery diseases, further accelerating demand. Healthcare providers are increasingly focusing on preventive care and early-stage treatment, supporting drug adoption. Improved access to healthcare services in emerging economies is another key driver. Pharmaceutical companies are investing in targeted therapies for peripheral conditions, enhancing treatment outcomes. The segment is also benefiting from growing clinical research activities. Furthermore, lifestyle changes and increasing screening programs are expected to sustain long-term growth.

• By Treatment

On the basis of treatment, the market is segmented into medication and surgery. The medication segment held the largest market revenue share of around 61.4% in 2025, driven by its non-invasive nature and widespread use as the first line of treatment. Medications such as statins, anticoagulants, and antihypertensives are commonly prescribed to manage artery stenosis effectively. The growing preference for conservative treatment approaches among patients and healthcare providers significantly contributes to this dominance. Medications help in slowing disease progression and reducing complications without requiring surgical intervention. Increased awareness regarding early-stage management of artery stenosis further fuels demand. In addition, the affordability and accessibility of drugs compared to surgical procedures make them a preferred option. Continuous advancements in pharmaceutical formulations are improving drug efficacy and safety profiles. The rising burden of chronic diseases also increases long-term medication usage. Favorable reimbursement policies in developed regions further support this segment. Pharmaceutical companies are focusing on developing combination therapies, enhancing treatment effectiveness.

The surgery segment is projected to grow at the fastest CAGR of 8.5% from 2026 to 2033, driven by the increasing demand for advanced and minimally invasive surgical procedures. Surgical treatments such as angioplasty and stenting are gaining popularity due to their effectiveness in severe cases. Technological advancements in surgical equipment and techniques are improving patient outcomes and reducing recovery times. Growing awareness regarding the benefits of early surgical intervention is also boosting demand. Increasing healthcare infrastructure development, especially in emerging markets, supports segment growth. In addition, the rising number of specialized surgeons and healthcare facilities contributes to adoption. Government initiatives to improve surgical care accessibility further enhance growth prospects. The increasing incidence of critical artery blockage cases necessitates surgical intervention. Higher success rates and reduced complications associated with modern procedures also attract patients. The segment is expected to witness sustained growth due to continuous innovation in surgical technologies.

• By Drugs

On the basis of drugs, the market is segmented into atorvastatin, fluvastatin, heparin, minoxidil, aspirin, and others. The atorvastatin segment dominated the market with a revenue share of approximately 29.8% in 2025, driven by its widespread use in lowering cholesterol levels and preventing cardiovascular complications. Atorvastatin is highly effective in reducing LDL cholesterol, making it a preferred choice among healthcare professionals. The increasing prevalence of hyperlipidemia and cardiovascular diseases significantly supports its demand. In addition, strong clinical evidence supporting its efficacy and safety enhances its adoption. The availability of generic versions has made it more affordable and accessible globally. Growing awareness about cholesterol management further boosts usage. Pharmaceutical companies continue to promote statins as a preventive therapy. The drug is widely prescribed for long-term treatment, ensuring consistent demand. Favorable reimbursement policies in developed regions also contribute to its dominance. Increasing screening for cholesterol-related conditions further strengthens market growth.

The heparin segment is expected to witness the fastest CAGR of 8.2% from 2026 to 2033, driven by its critical role as an anticoagulant in preventing blood clots. Heparin is widely used in both surgical and non-surgical settings, especially in patients at high risk of thrombosis. The rising number of surgical procedures globally significantly increases its demand. In addition, its rapid action and effectiveness in emergency situations make it indispensable in clinical practice. Growing awareness about clot prevention and management further supports segment growth. Increasing hospital admissions for cardiovascular conditions also boost usage. Advancements in drug formulations are improving safety and reducing side effects. The expansion of healthcare infrastructure in emerging economies enhances accessibility. Moreover, ongoing research into improved anticoagulant therapies is expected to sustain growth. The segment benefits from increasing demand in critical care and intensive care units.

• By Route of Administration

On the basis of route of administration, the market is segmented into oral and intravenous. The oral segment held the largest market share of 66.7% in 2025, driven by its convenience, ease of administration, and high patient compliance. Oral medications are widely preferred for long-term management of artery stenosis due to their non-invasive nature. Patients find oral drugs more convenient compared to injectable alternatives, leading to higher adherence rates. The availability of a wide range of oral drugs further supports segment growth. In addition, oral medications are cost-effective and easily accessible through retail pharmacies. Increasing awareness about preventive healthcare also boosts demand for oral drugs. Pharmaceutical companies focus heavily on developing oral formulations, enhancing availability. The segment benefits from the growing prevalence of chronic cardiovascular conditions requiring long-term treatment. Favorable regulatory approvals for oral drugs further contribute to growth.

The intravenous segment is expected to grow at the fastest CAGR of 7.6% from 2026 to 2033, driven by its rapid onset of action and effectiveness in acute conditions. Intravenous administration is commonly used in hospitals and emergency settings where immediate drug action is required. Increasing hospital admissions for severe cardiovascular conditions support segment growth. In addition, advancements in infusion technologies improve safety and efficiency. Healthcare professionals prefer IV drugs for critically ill patients, boosting demand. The rising number of surgical procedures also contributes to increased usage. Expanding healthcare infrastructure in developing regions enhances accessibility to IV treatments. The segment is further supported by growing investments in hospital facilities. Continuous innovation in injectable drug formulations is expected to sustain growth.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with a share of 47.9% in 2025, driven by the high volume of prescriptions generated in hospital settings. Patients undergoing treatment for artery stenosis often rely on hospital pharmacies for immediate access to medications. The presence of skilled healthcare professionals ensures accurate drug dispensing, enhancing trust. In addition, hospital pharmacies are well-equipped to handle critical medications, including injectables. Increasing hospital admissions for cardiovascular conditions further support growth. Strong supply chain networks ensure drug availability in hospitals. Government funding and investments in healthcare infrastructure also contribute to segment dominance.

The online pharmacy segment is expected to witness the fastest CAGR of 9.1% from 2026 to 2033, driven by the growing adoption of e-commerce in healthcare. Increasing internet penetration and smartphone usage support the shift toward online platforms. Patients prefer online pharmacies for convenience, home delivery, and competitive pricing. The COVID-19 pandemic further accelerated online drug purchases. In addition, digital health platforms are integrating pharmacy services, boosting growth. Improved regulatory frameworks for online pharmacies enhance consumer trust. The segment is expected to grow significantly with advancements in digital healthcare.

• By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment held the largest market share of 52.3% in 2025, driven by the high number of patients receiving treatment in hospital settings. Hospitals are equipped with advanced diagnostic and treatment facilities, making them the primary choice for artery stenosis management. The availability of specialized healthcare professionals further supports segment growth. Increasing hospital admissions for cardiovascular diseases significantly boosts demand. In addition, hospitals provide both medication and surgical treatment options, ensuring comprehensive care. Government investments in hospital infrastructure further strengthen the segment.

The homecare segment is projected to grow at the fastest CAGR of 8.8% from 2026 to 2033, driven by the increasing preference for home-based treatment and monitoring. Patients with chronic conditions prefer homecare for convenience and cost-effectiveness. Advancements in telemedicine and remote monitoring technologies support this trend. In addition, the aging population drives demand for home healthcare services. Increasing awareness about self-care and preventive healthcare further boosts growth. The segment is expected to expand rapidly due to rising healthcare costs and the shift toward patient-centric care models.

Artery Stenosis Drug Market Regional Analysis

- North America dominated the artery stenosis drug market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, and the strong presence of leading pharmaceutical companies

- The region benefits from widespread awareness regarding cardiovascular diseases and early diagnosis, which drives the demand for effective treatment options

- Patients and healthcare providers in the region increasingly prefer advanced and combination drug therapies for effective management of artery stenosis, contributing to improved clinical outcomes. In addition, favorable reimbursement policies, ongoing clinical research, and rapid adoption of innovative therapeutics further strengthen market growth across North America

U.S. Artery Stenosis Drug Market Insight

The U.S. artery stenosis drug market captured the largest revenue share within North America in 2025, driven by the high prevalence of cardiovascular diseases and strong adoption of novel and combination drug therapies. The country’s well-established healthcare system, coupled with significant investments in research and development, supports the introduction of advanced treatment options. Moreover, increasing focus on preventive care, early diagnosis, and personalized medicine is further propelling market expansion in the United States.

Europe Artery Stenosis Drug Market Insight

The Europe artery stenosis drug market is projected to expand at a substantial CAGR during the forecast period, primarily driven by the rising burden of cardiovascular diseases and supportive government healthcare policies. The presence of well-developed healthcare systems and growing awareness regarding early treatment contribute to increased drug adoption. In addition, continuous advancements in pharmaceutical research and increasing geriatric population are key factors fostering market growth across the region.

U.K. Artery Stenosis Drug Market Insight

The U.K. artery stenosis drug market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by increasing healthcare awareness and a rising prevalence of lifestyle-related cardiovascular conditions. Government initiatives aimed at improving cardiac care, along with enhanced screening programs, are encouraging early diagnosis and treatment. Furthermore, the availability of advanced therapies and strong healthcare infrastructure are contributing to sustained market growth in the U.K.

Germany Artery Stenosis Drug Market Insight

The Germany artery stenosis drug market is expected to expand at a considerable CAGR, driven by the country’s robust healthcare system and strong focus on medical innovation. Increasing investment in pharmaceutical research, coupled with a high demand for effective cardiovascular treatments, is boosting market development. Germany’s emphasis on quality healthcare services and access to advanced therapies supports the widespread adoption of artery stenosis drugs.

Asia-Pacific Artery Stenosis Drug Market Insight

The Asia-Pacific artery stenosis drug market is expected to grow at the fastest CAGR during the forecast period, driven by rapid urbanization, improving healthcare access, and rising disposable incomes. The increasing prevalence of lifestyle-related cardiovascular disorders, particularly in countries such as China and India, is significantly boosting demand for effective treatment solutions. In addition, government initiatives to strengthen healthcare infrastructure and growing awareness about heart health are accelerating market expansion across the region.

Japan Artery Stenosis Drug Market Insight

The Japan artery stenosis drug market is gaining momentum due to its advanced healthcare system, aging population, and high prevalence of cardiovascular diseases. The country places strong emphasis on early diagnosis and preventive care, which drives the demand for effective drug therapies. Moreover, ongoing innovations in pharmaceutical treatments and increasing adoption of combination therapies are contributing to market growth in Japan.

China Artery Stenosis Drug Market Insight

The China artery stenosis drug market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s large patient population, rising middle class, and rapid improvements in healthcare infrastructure. Increasing awareness regarding cardiovascular health, along with government efforts to expand healthcare access, is driving drug adoption. Furthermore, the growing presence of domestic pharmaceutical manufacturers and expanding availability of cost-effective treatment options are key factors propelling market growth in China.

Artery Stenosis Drug Market Share

The Artery Stenosis Drug industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Roche Holding AG (Switzerland)

- Sanofi (France)

- GSK plc (U.K.)

- Johnson & Johnson (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Merck & Co., Inc. (U.S.)

- AstraZeneca plc (U.K.)

- Abbott Laboratories (U.S.)

- Bayer AG (Germany)

- Amgen Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Dr. Reddy’s Laboratories Ltd. (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Cipla Ltd. (India)

- Lupin Limited (India)

- Aurobindo Pharma Ltd. (India)

- Zydus Lifesciences Ltd. (India)

Latest Developments in Global Artery Stenosis Drug Market

- In March 2024, Boston Scientific, a leading medical device and cardiovascular therapy company, announced that the U.S. Food and Drug Administration (FDA) approved its Agent™ drug-coated balloon (DCB) for the treatment of coronary in-stent restenosis (ISR). This marked the first drug-coated balloon approved in the United States for coronary ISR, delivering paclitaxel directly to artery walls to prevent re-narrowing. The approval was supported by the AGENT IDE trial, demonstrating significantly reduced target lesion failure compared to standard balloon angioplasty, highlighting a major advancement in minimally invasive artery stenosis treatment

- In October 2024, UPMC (University of Pittsburgh Medical Center) announced the clinical adoption of newly FDA-approved drug-coated balloon therapy for patients with recurrent artery blockage following stent placement. This therapy enables localized drug delivery without leaving a permanent implant, offering a less invasive alternative to repeat stenting or radiation therapy and improving outcomes for patients with coronary artery stenosis complications

- In September 2024, GE HealthCare announced that the FDA approved Flyrcado™ (flurpiridaz F-18), a novel PET imaging diagnostic drug for detecting coronary artery disease (CAD). The drug enables high-resolution 3D imaging of blood flow in narrowed arteries and demonstrated 74–89% diagnostic accuracy in clinical studies, significantly improving early detection and treatment planning for artery stenosis

- In February 2025, Mayo Clinic researchers (with prior involvement from Sanofi) reported promising clinical trial results for ataciguat, an experimental drug targeting aortic valve stenosis. The therapy demonstrated nearly a 70% reduction in calcification progression over six months, indicating its potential to delay disease progression and reduce the need for surgical valve replacement, representing a breakthrough in pharmacological management of stenosis

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.