Global Assembly Trays Market

Market Size in USD Billion

USD

4.05 Billion

USD

6.02 Billion

2025

2033

USD

4.05 Billion

USD

6.02 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.05 Billion | |

| USD 6.02 Billion | |

| % | |

|

Assembly Trays Market Size

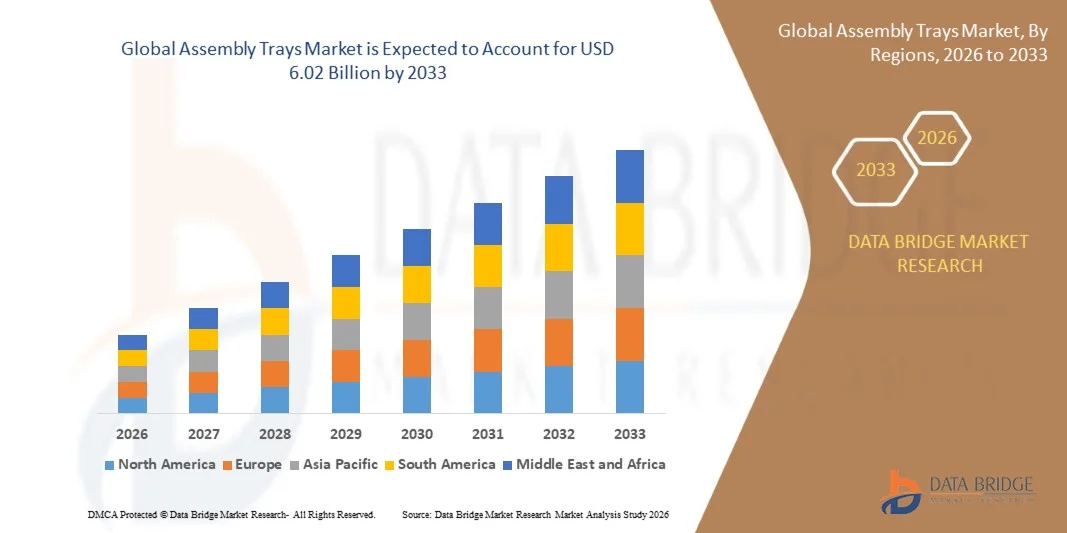

- The global assembly trays market size was valued at USD 4.05 billion in 2025 and is expected to reach USD 6.02 billion by 2033, at a CAGR of 5.10% during the forecast period

- The market growth is largely fuelled by the rising demand for efficient material handling and component organization solutions across automotive, electronics, aerospace, and industrial manufacturing sectors

- Increasing automation in assembly lines, coupled with the growing need for precision, productivity, and workflow optimization, is accelerating the adoption of durable and customizable assembly trays

Assembly Trays Market Analysis

- The market is witnessing steady growth due to increasing adoption of organized storage and transportation systems that improve operational efficiency, reduce assembly errors, and enhance productivity across manufacturing facilities

- Rising investments in advanced manufacturing processes, automation technologies, and sustainable reusable packaging solutions are strengthening market development, while expanding applications in electronics, medical devices, and precision engineering industries continue to create new growth opportunities

- North America dominated the assembly trays market with the largest revenue share in 2025, driven by the strong presence of advanced manufacturing industries, growing automation adoption, and increasing demand for efficient material handling solutions across automotive, aerospace, and electronics sectors

- Asia-Pacific region is expected to witness the highest growth rate in the global assembly trays market, driven by rapid industrial expansion, increasing automation in manufacturing facilities, strong growth in automotive, electronics, and healthcare sectors, and rising cost-effective production capabilities across emerging economies such as China, India, and Southeast Asia

- The plastic segment held the largest market revenue share in 2025 driven by its lightweight structure, cost efficiency, durability, and widespread applicability across manufacturing, electronics, healthcare, and logistics industries. Plastic assembly trays are highly preferred due to their corrosion resistance, easy customization, and compatibility with automated material handling systems. Their reusable nature and lower maintenance requirements further strengthen adoption across industrial production environments

Report Scope and Assembly Trays Market Segmentation

|

Attributes |

Assembly Trays Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Molded Fiber Glass Tray Company (U.S.) |

|

Market Opportunities |

• Rising Adoption Of Smart And Automated Material Handling Systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Assembly Trays Market Trends

“Rising Demand for Automated Material Handling and Lean Manufacturing Solutions”

• The growing focus on operational efficiency, precision manufacturing, and organized component management is significantly shaping the assembly trays market, as industries increasingly prioritize optimized workflows and reduced production errors. Assembly trays are gaining widespread traction due to their ability to streamline storage, transportation, and handling of components while improving assembly line productivity. This trend is strengthening their adoption across automotive, electronics, aerospace, medical devices, and industrial manufacturing sectors, encouraging manufacturers to develop advanced, durable, and customizable tray solutions

• Increasing industrial automation and the rapid implementation of lean manufacturing principles have accelerated the demand for assembly trays in production environments requiring efficient material flow and workspace organization. Manufacturers are actively seeking reusable, ergonomic, and high-performance tray systems that improve assembly speed, reduce labor inefficiencies, and support automated systems. This has also led to innovation in tray materials, modular designs, and smart tracking capabilities to enhance productivity and cost savings

• Sustainability and operational optimization trends are influencing purchasing decisions, with manufacturers emphasizing reusable tray systems, lightweight materials, and eco-friendly production practices. These factors are helping businesses reduce packaging waste, lower operational costs, and improve supply chain sustainability. Companies are increasingly promoting assembly trays as strategic tools for improving efficiency, inventory accuracy, and environmental performance in modern manufacturing ecosystems

• For instance, in 2024, automotive and electronics manufacturers in Germany and Japan expanded their use of advanced reusable assembly tray systems integrated with automation processes to improve component handling, reduce packaging waste, and optimize assembly efficiency. These initiatives were introduced in response to growing production complexity and increasing sustainability requirements, significantly improving workflow consistency and reducing operational expenses

• While demand for assembly trays is growing steadily, sustained market expansion depends on continuous product innovation, cost-effective manufacturing, and integration with evolving automation technologies. Manufacturers are also focusing on scalability, advanced material durability, and digital inventory management features to broaden adoption across multiple industrial applications

Assembly Trays Market Dynamics

Driver

“Growing Adoption of Automation and Lean Manufacturing Practices”

• Rising industrial demand for efficient, organized, and automated material handling systems is a major driver for the assembly trays market. Manufacturers are increasingly implementing assembly trays to optimize production workflows, improve component accessibility, and minimize assembly errors. This trend is also encouraging product innovation in smart trays, modular tray systems, and industry-specific customization to support diverse manufacturing requirements

• Expanding applications across automotive, aerospace, electronics, healthcare, and precision engineering industries are strongly influencing market growth. Assembly trays improve operational productivity by enhancing component organization, reducing manual handling inefficiencies, and supporting automated assembly systems. The increasing complexity of manufacturing processes globally further reinforces this trend

• Industrial manufacturers are actively promoting advanced tray solutions through process optimization strategies, sustainability initiatives, and automation investments. These efforts are supported by the growing demand for operational excellence, waste reduction, and cost efficiency. Strategic collaborations between tray manufacturers, industrial automation providers, and supply chain companies are also improving tray functionality and broader market penetration

• For instance, in 2023, electronics and automotive manufacturers in the U.S. and South Korea reported increased implementation of modular and reusable assembly tray systems to support precision manufacturing and reduce operational downtime. These expansions followed rising demand for production efficiency, improved quality control, and sustainable logistics, significantly enhancing manufacturing competitiveness

• Although automation and lean manufacturing trends strongly support growth, broader market adoption depends on production cost optimization, customization flexibility, and integration with next-generation manufacturing technologies. Investments in material innovation, supply chain scalability, and digitalization will be essential for sustaining long-term competitive advantage

Restraint/Challenge

“High Initial Costs and Limited Adoption Among Small-Scale Manufacturers”

• The relatively high upfront investment associated with advanced assembly tray systems compared to traditional storage and handling methods remains a key challenge, particularly for small and medium-sized manufacturers. Customization requirements, durable material costs, and automation compatibility can increase implementation expenses. In addition, fluctuating raw material prices may further affect affordability and market penetration

• Awareness and adoption remain uneven across developing industrial markets where conventional material handling systems continue to dominate. Limited understanding of long-term productivity benefits and return on investment can restrict broader implementation. This also contributes to slower adoption among smaller manufacturers with constrained capital budgets

• Supply chain and logistical complexities also impact market growth, as specialized assembly trays often require precise manufacturing standards, customized designs, and efficient distribution systems. Storage requirements, maintenance, and operational integration can increase costs for businesses transitioning from conventional systems. Manufacturers must also address scalability and compatibility with existing industrial infrastructure

• For instance, in 2024, small-scale manufacturers in Southeast Asia and Latin America reported slower adoption of advanced assembly tray systems due to higher implementation costs, limited customization budgets, and insufficient awareness of operational benefits. Budget limitations and infrastructure constraints were significant barriers to broader deployment

• Overcoming these challenges will require cost-efficient manufacturing, broader educational initiatives, scalable product offerings, and stronger collaboration between tray manufacturers and industrial users. Developing affordable, adaptable, and automation-compatible solutions will be essential for unlocking the long-term growth potential of the global assembly trays market while improving accessibility across diverse industrial sectors

Assembly Trays Market Scope

The market is segmented on the basis of product type, material type, load capacity, and end user.

• By Material Type

On the basis of material type, the assembly trays market is segmented into plastic, metal, fiber glass, and others. The plastic segment held the largest market revenue share in 2025 driven by its lightweight structure, cost efficiency, durability, and widespread applicability across manufacturing, electronics, healthcare, and logistics industries. Plastic assembly trays are highly preferred due to their corrosion resistance, easy customization, and compatibility with automated material handling systems. Their reusable nature and lower maintenance requirements further strengthen adoption across industrial production environments.

The fiber glass segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for high-strength, heat-resistant, and durable tray solutions across aerospace, defense, and precision manufacturing industries. Fiber glass trays are particularly valued for their superior structural integrity, resistance to harsh environments, and long operational lifespan, making them ideal for specialized industrial applications.

• By Material Type

On the basis of material type, the assembly trays market is segmented into plastic, metal, fiber glass, and others. The plastic segment held the largest market revenue share in 2025 driven by its lightweight structure, cost efficiency, durability, and widespread applicability across manufacturing, electronics, healthcare, and logistics industries. Plastic assembly trays are highly preferred due to their corrosion resistance, easy customization, and compatibility with automated material handling systems. Their reusable nature and lower maintenance requirements further strengthen adoption across industrial production environments.

The fiber glass segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for high-strength, heat-resistant, and durable tray solutions across aerospace, defense, and precision manufacturing industries. Fiber glass trays are particularly valued for their superior structural integrity, resistance to harsh environments, and long operational lifespan, making them ideal for specialized industrial applications.

• By Load Capacity

On the basis of load capacity, the assembly trays market is segmented into below 100 lb., 101-200 lb., 201-300 lb., and above 300 lb. The 101-200 lb. segment held the largest market revenue share in 2025 driven by its balanced load-bearing capability, versatility, and suitability for a broad range of industrial applications including automotive components, electronics, and manufacturing assemblies. This segment offers an optimal combination of strength, mobility, and operational efficiency, making it highly preferred across medium-duty industrial environments.

The above 300 lb. segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for heavy-duty assembly tray solutions in aerospace, defense, automotive manufacturing, and large-scale industrial production. These trays are increasingly utilized for handling larger components, improving safety, and supporting high-load automated systems. Expanding industrial complexity is further supporting this segment’s growth.

• By End User

On the basis of end user, the assembly trays market is segmented into electrical and electronics, manufacturing, automobile, aerospace, defense and military, healthcare, and others. The manufacturing segment held the largest market revenue share in 2025 driven by extensive adoption of assembly trays in production lines requiring efficient material organization, workflow optimization, and lean operational practices. Manufacturers increasingly rely on assembly trays to improve productivity, minimize assembly errors, and enhance process standardization. Growing automation and industrial modernization are further reinforcing segment dominance.

The healthcare segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing use of specialized assembly trays for medical device manufacturing, laboratory equipment organization, and sterile component handling. Rising healthcare infrastructure expansion, precision manufacturing requirements, and demand for hygienic reusable solutions are significantly accelerating adoption across healthcare and medical technology sectors.

Assembly Trays Market Regional Analysis

• North America dominated the assembly trays market with the largest revenue share in 2025, driven by the strong presence of advanced manufacturing industries, growing automation adoption, and increasing demand for efficient material handling solutions across automotive, aerospace, and electronics sectors

• Industries in the region highly value assembly trays for their durability, operational efficiency, and ability to streamline production workflows, reduce component damage, and improve organization across complex assembly environments

• This widespread adoption is further supported by technological advancements, high industrial productivity standards, and increasing investments in automated manufacturing systems, establishing assembly trays as essential components in industrial logistics and production operations

U.S. Assembly Trays Market Insight

The U.S. assembly trays market captured the largest revenue share in 2025 within North America, fueled by strong manufacturing infrastructure, expanding aerospace and defense industries, and rising adoption of automated assembly systems. Manufacturers are increasingly prioritizing productivity optimization, precision handling, and workflow efficiency, which is driving the use of advanced tray solutions. The growing focus on industrial automation, combined with robust investments in electronics, healthcare equipment, and automotive production, continues to propel market expansion.

Europe Assembly Trays Market Insight

The Europe assembly trays market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing industrial modernization, stringent manufacturing quality standards, and rising adoption of sustainable material handling systems. The expansion of automotive, aerospace, and precision engineering sectors is fostering demand for durable and reusable assembly trays. European industries are also emphasizing operational efficiency and sustainability, encouraging broader implementation across manufacturing facilities.

U.K. Assembly Trays Market Insight

The U.K. assembly trays market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing industrial automation, expansion of advanced manufacturing sectors, and growing investments in aerospace and electronics production. The country’s strong focus on operational efficiency, product quality, and supply chain optimization is accelerating demand for assembly trays across various industries.

Germany Assembly Trays Market Insight

The Germany assembly trays market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country’s robust automotive manufacturing base, engineering excellence, and increasing focus on industrial automation. Germany’s advanced production ecosystem, combined with high demand for precision material handling systems, promotes widespread adoption of assembly trays across automotive, aerospace, and industrial sectors. Sustainability initiatives are also encouraging the use of reusable and durable tray systems.

Asia-Pacific Assembly Trays Market Insight

The Asia-Pacific assembly trays market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, expanding manufacturing sectors, and rising investments in automotive, electronics, and healthcare production across countries such as China, Japan, and India. The region’s growing role as a global manufacturing hub, combined with increasing automation adoption and cost-effective production capabilities, significantly boosts market growth.

Japan Assembly Trays Market Insight

The Japan assembly trays market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s strong focus on technological innovation, precision manufacturing, and advanced industrial automation. Japan’s leadership in electronics, robotics, and automotive manufacturing supports increasing adoption of high-performance assembly trays designed for efficiency and quality assurance. The emphasis on streamlined operations and manufacturing excellence further accelerates market expansion.

China Assembly Trays Market Insight

The China assembly trays market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s extensive manufacturing ecosystem, rapid industrial growth, and expanding automotive, electronics, and healthcare industries. China’s role as a global production center, combined with rising automation investments and demand for cost-effective industrial solutions, significantly supports assembly tray adoption. Strong domestic production capabilities and increasing export activities further contribute to market leadership.

Assembly Trays Market Share

The Assembly Trays industry is primarily led by well-established companies, including:

• Molded Fiber Glass Tray Company (U.S.)

• Impala Plastics (U.S.)

• W.W. Grainger, Inc. (U.S.)

• Conductive Containers, Inc. (U.S.)

• LewisBins+ (U.S.)

• Gilmore Kramer Co. (U.S.)

• Z-Mar Technology, Inc. (U.S.)

• Regal Research and Mfg. Co. (U.S.)

• VALLEY PLASTICS (U.S.)

• Dunnage Engineering (U.S.)

• Robinson Industries, Inc. (U.S.)

• StockCap (U.S.)

• Engineered Components & Packaging, LLC (U.S.)

Latest Developments in Global Assembly Trays Market

- In March 2026, Uline (U.S.) introduced an expanded portfolio of customizable assembly trays designed for specialized industrial applications, enabling manufacturers to improve workflow efficiency, optimize storage, and address sector-specific handling needs. This development strengthens Uline’s competitive positioning by enhancing customer-centric offerings, increasing product versatility, and supporting broader adoption of tailored material handling solutions across diverse industries

- In October 2025, Apex Tool Group (U.S.) launched a new range of eco-friendly assembly trays manufactured using sustainable materials to address increasing environmental concerns and industrial sustainability goals. This initiative is expected to enhance the company’s brand value, attract environmentally conscious buyers, and accelerate the transition toward greener manufacturing practices within the global assembly trays market

- In August 2024, SSI Schaefer (Germany) formed a strategic partnership with an advanced automation technology provider to develop smart assembly trays integrated with IoT-enabled monitoring systems. This innovation improves real-time tracking, operational productivity, and process automation, positioning the company at the forefront of digital transformation while setting new performance standards in industrial material handling

- In February 2024, Conductive Containers, Inc. (U.S.) expanded its electrostatic discharge-safe assembly tray production capabilities to meet rising demand from electronics and semiconductor industries. This capacity enhancement supports precision manufacturing, improves product safety during component transportation, and strengthens the company’s presence in high-value electronics supply chains

- In June 2023, LewisBins+ (U.S.) launched advanced reusable plastic assembly trays with enhanced durability and ergonomic designs targeted at automotive and manufacturing sectors. This product innovation improves handling efficiency, reduces operational costs, and reinforces the shift toward long-term reusable solutions in industrial logistics systems

- In April 2022, Robinson Industries, Inc. (U.S.) invested in expanded manufacturing infrastructure to increase assembly tray production output and improve customization capabilities. This strategic expansion enhances supply chain responsiveness, supports growing industrial demand, and contributes to stronger market competitiveness through scalable production efficiency

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Assembly Trays Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Assembly Trays Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Assembly Trays Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.