Global Assistive Technology In Down Syndrome Market

Market Size in USD Billion

USD

2.57 Billion

USD

4.68 Billion

2025

2033

USD

2.57 Billion

USD

4.68 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.57 Billion | |

| USD 4.68 Billion | |

| % | |

|

Assistive Technology in Down Syndrome Market Size

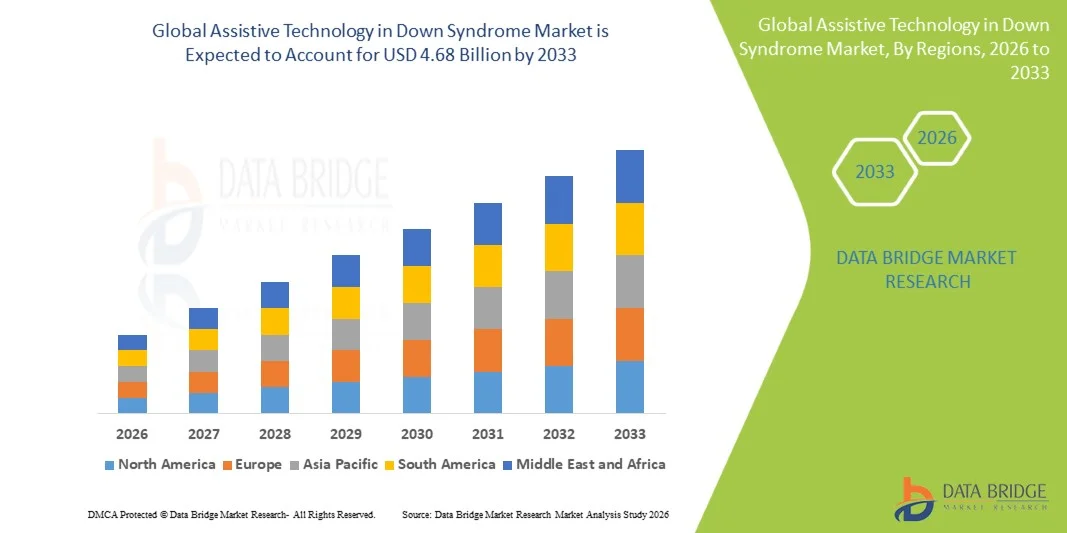

- The global assistive technology in down syndrome market size was valued at USD 2.57 billion in 2025and is expected to reach USD 4.68 billion by 2033, at a CAGR of 7.80% during the forecast period

- The market growth is largely driven by increasing awareness and early diagnosis of Down syndrome, coupled with the rising emphasis on inclusive education and developmental support, which is boosting the adoption of assistive technologies such as speech therapy tools, communication devices, and cognitive learning aids

- Furthermore, advancements in digital health, AI-powered learning applications, and personalized assistive devices are enhancing accessibility, independence, and quality of life for individuals with Down syndrome, thereby accelerating the demand and expansion of the assistive technology in Down syndrome market

Assistive Technology in Down Syndrome Market Analysis

- The Assistive Technology in Down Syndrome market, encompassing communication aids, speech and language therapy tools, cognitive development applications, wearable assistive devices, and adaptive learning platforms, is becoming increasingly essential in improving independence, learning outcomes, and daily functioning for individuals with Down syndrome, driven by the rapid integration of digital health solutions and AI-enabled personalized support systems

- The escalating demand for assistive technologies in down syndrome care is primarily fueled by rising global awareness, increased early diagnosis rates, expansion of special education programs, and growing preference for inclusive learning environments supported by AAC (Augmentative and Alternative Communication) devices, mobile-based learning applications, and sensor-based assistive tools that enhance communication and cognitive development

- North America dominated the Assistive Technology in Down Syndrome market with the largest revenue share of approximately 38% in 2025, supported by advanced healthcare infrastructure, strong adoption of digital therapeutics, high awareness of developmental disorders, and the presence of leading assistive technology providers, with the U.S. witnessing significant uptake of AI-powered speech therapy apps and communication devices in both educational and home-care settings

- Asia-Pacific is expected to be the fastest growing region in the Assistive Technology in Down Syndrome market during the forecast period, driven by improving healthcare access, increasing government initiatives for special needs education, rising disposable incomes, and growing penetration of affordable mobile-based assistive applications across countries such as India, China, and Southeast Asian nations

- The Trisomy 21 segment dominated the largest market revenue share of 94.8% in 2025, driven by its very high prevalence, accounting for the vast majority of Down Syndrome cases worldwide

Report Scope and Assistive Technology in Down Syndrome Market Segmentation

|

Attributes |

Assistive Technology in Down Syndrome Key Market Insights |

|

Segments Covered |

· By Disease Type: Trisomy 21, Translocation Down Syndrome, Mosaic Down Syndrome, and Others · By Treatment: Diagnosis, Therapy, Early Intervention Programs, and Supportive Care Solutions · By End User: Hospitals, Clinics, Homecare Settings, Therapy Centers, Special Education Institutions, and Others · By Distribution Channel: Direct Tender, Retail Sales, Online Platforms, Institutional Procurement, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Medtronic (Ireland) · Sonova Group (Switzerland) · Tobii Dynavox (Sweden) · OrCam Technologies (Israel) · Widex (Denmark) · GN Store Nord (Denmark) · Cochlear Limited (Australia) · Jabbla (Belgium) · AbleNet Inc. (U.S.) · Attainment Company (U.S.) · Lingraphica (U.S.) · Smartbox Assistive Technology (U.K.) · PRC-Saltillo (U.S.) · LeapFrog Enterprises (U.S.) · Sensory Software International (U.K.) · Rehadapt Engineering (Germany) · Freedom Scientific (U.S.) · Don Johnston Inc. (U.S.) · Inclusive Technology (U.K.) · Komodo OpenLab (U.S.) |

|

Market Opportunities |

· Expansion of AI-powered personalized learning and communication tools · Growing adoption in homecare and remote therapy solutions |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Assistive Technology in Down Syndrome Market Trends

“Enhanced Convenience Through AI and Voice Integration in Assistive Technology for Down Syndrome”

- A significant and accelerating trend in the global Assistive Technology in Down Syndrome market is the integration of artificial intelligence (AI) and voice-enabled technologies into communication, learning, and daily living support tools. These advancements are enhancing independence, communication ability, and accessibility for individuals with Down syndrome

- For instance, AI-powered augmentative and alternative communication (AAC) solutions such as Proloquo2Go enable users with speech difficulties to communicate through predictive text, symbol-based input, and synthesized speech output, improving real-time interaction capabilities

- Similarly, integration with voice assistants such as Google Assistant and other smart ecosystem tools allows users to perform everyday tasks using voice commands, supporting cognitive and speech development through interactive engagement

- AI is increasingly being used in adaptive learning platforms and speech therapy applications to personalize learning pathways based on user progress, attention span, and comprehension levels. These systems can adjust difficulty, repetition, and pacing to better suit individual developmental needs

- Wearable assistive devices and smart communication tools are also incorporating AI-based emotion recognition and behavioral tracking to help caregivers and therapists better understand user needs and emotional states, enabling more targeted interventions

- The growing interoperability between assistive devices, mobile applications, and cloud-based platforms is enabling a more connected and supportive ecosystem for individuals with Down syndrome, improving continuity of care across home, school, and therapy environments

Assistive Technology in Down Syndrome Market Dynamics

Driver

“Rising Demand for Early Intervention, Inclusive Education, and Digital Therapeutics”

- The increasing global focus on early intervention and inclusive education is a major driver supporting the growth of the Assistive Technology in Down Syndrome market. Parents, educators, and healthcare professionals are increasingly adopting digital tools to improve communication, cognitive development, and social integration outcomes

- Governments and non-profit organizations are expanding funding and support programs for special education technologies, encouraging wider adoption of AAC devices, speech therapy apps, and learning support platforms in schools and therapy centers

- For instance, schools and rehabilitation centers are increasingly incorporating AI-based learning applications and tablet-based communication tools to support personalized education plans for children with Down syndrome

- The rising prevalence of developmental disorder awareness campaigns has improved early diagnosis rates, leading to earlier adoption of assistive technologies that significantly improve long-term developmental outcomes

- In addition, advancements in digital therapeutics and mobile health applications are enabling continuous monitoring and structured skill development outside clinical settings, increasing accessibility and affordability of care solutions

Restraint/Challenge

“High Cost of Advanced Solutions, Limited Awareness, and Data Privacy Concerns”

- The high cost of advanced assistive technologies, including AI-enabled communication devices and specialized learning platforms, remains a significant barrier to adoption, particularly in low- and middle-income regions

- Limited awareness among caregivers and educators regarding the availability and benefits of modern assistive solutions continues to restrict market penetration, especially in rural and underdeveloped areas

- For instance, in several emerging markets, schools often continue relying on traditional teaching aids due to lack of exposure and training on AAC devices and digital learning platforms designed for individuals with Down syndrome

- A shortage of trained professionals capable of effectively implementing and customizing assistive technology solutions further limits their optimal utilization in educational and clinical settings

- Data privacy and security concerns associated with cloud-based communication tools and AI-driven monitoring systems also pose challenges, as these platforms often process sensitive behavioral and health-related information

- While technological advancements are gradually reducing costs and improving usability, ensuring affordability, building awareness, and strengthening data protection frameworks will be critical for sustained market expansion

Assistive Technology in Down Syndrome Market Scope

The market is segmented on the basis of disease type, treatment, end user, and distribution channel.

- By Disease Type

On the basis of disease type, the Assistive Technology in Down Syndrome market is segmented into Trisomy 21, Translocation Down Syndrome, and Mosaic Down Syndrome. The Trisomy 21 segment dominated the largest market revenue share of 94.8% in 2025, driven by its very high prevalence, accounting for the vast majority of Down Syndrome cases worldwide. Individuals with Trisomy 21 require continuous developmental, cognitive, and communication support, significantly increasing demand for assistive technologies. Rising awareness and early screening programs are further strengthening adoption. The segment benefits from strong integration of AI-enabled learning tools and adaptive communication devices. Expanding inclusive education systems and rehabilitation programs are also contributing to growth. Government and NGO support initiatives further enhance accessibility of assistive solutions. High demand for long-term care and structured intervention programs continues to reinforce dominance. Continuous innovation in personalized assistive platforms is improving outcomes. Overall, Trisomy 21 remains the most commercially significant segment in 2025.

The Mosaic Down Syndrome segment is expected to witness the fastest growth rate with a CAGR of 10.8% from 2026 to 2033, driven by improved diagnostic accuracy and rising awareness of milder and variable symptom profiles. Although it represents a smaller patient population, demand for highly customized assistive technologies is increasing rapidly. Individuals with Mosaic Down Syndrome often require adaptive and flexible support systems rather than standardized solutions. Growing use of AI-based behavioral and learning assessment tools is enhancing personalized intervention strategies. Expansion of home-based therapy and digital learning platforms is accelerating adoption. Increased parental awareness and early intervention programs are improving diagnosis rates. Healthcare providers are increasingly focusing on individualized care models. Technological advancements in communication aids and cognitive support tools are also boosting adoption. Supportive education policies are further encouraging inclusive learning environments. These factors collectively position Mosaic Down Syndrome as the fastest-growing disease type segment.

- By Treatment

On the basis of treatment, the market is segmented into Diagnosis and Therapy. The Diagnosis segment held the largest market share of 57.6% in 2025, driven by rising adoption of prenatal screening, genetic testing, and newborn diagnostic programs. Early diagnosis plays a critical role in enabling timely intervention and long-term developmental support. Increasing awareness among parents and healthcare professionals is boosting diagnostic uptake. Hospitals and diagnostic centers are increasingly integrating advanced genetic testing technologies. Government-led screening initiatives are further strengthening early detection rates. Insurance coverage for diagnostic procedures is also supporting market expansion. AI-powered diagnostic tools are improving accuracy and efficiency. Expansion of healthcare infrastructure in developing regions is further driving growth. Early identification increases demand for downstream assistive technologies. Overall, diagnosis remains the foundational driver of the market.

The Therapy segment is anticipated to witness the fastest growth rate with a CAGR of 11.5% from 2026 to 2033, driven by rising demand for long-term developmental support services. Speech therapy, occupational therapy, and behavioral therapy are increasingly supported by digital and AI-enabled platforms. Growing adoption of tele-therapy and remote rehabilitation solutions is expanding access to care. Families are increasingly preferring continuous home-based therapy programs. Gamified learning and interactive therapy tools are improving engagement and outcomes. Integration of assistive communication technologies is enhancing therapeutic effectiveness. Rising investment in specialized therapy centers is also supporting growth. Government and NGO initiatives promoting early intervention are contributing significantly. Increasing awareness of developmental care is driving consistent demand. These factors collectively make Therapy the fastest-growing treatment segment.

- By End User

On the basis of end user, the market is segmented into Hospitals, Clinics, Homecare Settings, Therapy Centers, and Others. The Hospital segment accounted for the largest market revenue share of 41.3% in 2025, driven by advanced diagnostic infrastructure and multidisciplinary care capabilities. Hospitals act as the primary point for diagnosis, early intervention, and treatment planning. High patient inflow and access to specialized professionals support strong adoption of assistive technologies. Integration of digital health systems and AI-based monitoring tools enhances care efficiency. Government healthcare funding and insurance support further strengthen hospital dominance. Hospitals also play a key role in therapy referrals and assistive device recommendations. Expansion of pediatric and genetic departments is boosting demand. Collaboration with technology providers enables deployment of advanced assistive solutions. Rehabilitation units within hospitals further contribute to usage. Overall, hospitals remain the central hub of clinical intervention.

The Homecare Settings segment is expected to witness the fastest growth rate with a CAGR of 12.3% from 2026 to 2033, driven by rising preference for personalized, family-based care. Increasing availability of portable assistive devices is enabling effective home-based support. Telehealth platforms and remote monitoring systems are reducing dependence on institutional care. Families are increasingly involved in long-term developmental management. Cost-effectiveness of homecare compared to hospital visits is driving adoption. AI-powered learning and communication tools are improving at-home outcomes. Growing internet penetration and smart device usage are supporting digital assistive solutions. Government initiatives promoting community-based care are further accelerating growth. Expansion of e-learning and home therapy programs is strengthening adoption. These factors collectively position Homecare Settings as the fastest-growing end user segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Direct Tender, Retail Sales, and Others. The Direct Tender segment dominated the largest market revenue share of 48.9% in 2025, driven by bulk procurement by hospitals, government agencies, and healthcare institutions. Centralized purchasing systems ensure cost efficiency and standardized deployment of assistive technologies. Government-funded disability programs significantly contribute to demand. Hospitals and rehabilitation centers rely heavily on direct procurement channels. Long-term contracts with manufacturers support stable supply chains. Institutional adoption of assistive technologies is streamlined through structured procurement processes. Regulatory compliance requirements also favor direct tender systems. Strong collaboration between governments and vendors enhances distribution efficiency. Large-scale public health initiatives further strengthen this channel. Overall, direct tender remains the dominant institutional distribution route.

The Retail Sales segment is expected to witness the fastest growth rate with a CAGR of 13.0% from 2026 to 2033, driven by rising consumer awareness and expanding e-commerce penetration. Increasing demand for direct-to-consumer assistive technologies is reshaping purchasing behavior. Online platforms are improving accessibility to a wide range of assistive devices. Families are increasingly opting for easy-to-use home-based solutions. Growth of digital marketplaces is enabling faster product availability. Rising disposable incomes are supporting retail adoption in developing regions. Advancements in mobile-enabled assistive devices are further driving demand. Manufacturers are expanding direct retail and online distribution networks. Increased digital literacy among caregivers is boosting online purchasing trends. These factors collectively make Retail Sales the fastest-growing distribution channel.

Assistive Technology in Down Syndrome Market Regional Analysis

- North America dominated the assistive technology in down syndrome market with the largest revenue share of approximately 38% in 2025, supported by advanced healthcare infrastructure, strong adoption of digital therapeutics, high awareness of developmental disorders, and the presence of leading assistive technology providers. The region is witnessing significant uptake of AI-powered speech therapy applications, augmentative and alternative communication (AAC) devices, and adaptive learning tools across both educational institutions and home-care settings, particularly in the U.S.

- Consumers in North America increasingly prefer integrated, user-friendly assistive solutions that enhance communication, learning, and daily living skills for individuals with Down syndrome. Growing adoption of mobile-based therapy platforms, cloud-enabled progress tracking, and personalized AI-driven interventions is further strengthening market expansion across schools, therapy centers, and home environments

- This widespread adoption is further supported by favorable reimbursement frameworks, strong caregiver awareness programs, and continuous technological innovation, making the region a key hub for next-generation assistive technologies

U.S. Assistive Technology in Down Syndrome Market Insight

The U.S. assistive technology in down syndrome market captured the largest revenue share within North America in 2025, driven by rapid adoption of AI-enabled communication tools and expanding use of digital therapeutic platforms. Educational institutions and home-care providers are increasingly integrating AAC devices, speech-generating applications, and AI-based language development tools to support individuals with Down syndrome. Growing preference for personalized learning interventions, combined with strong demand for mobile apps offering real-time speech correction, cognitive training, and behavioral support, is further propelling market growth. In addition, the integration of assistive technologies with smart devices and teletherapy platforms is enhancing accessibility and continuity of care.

Europe Assistive Technology in Down Syndrome Market Insight

The Europe assistive technology in down syndrome market is projected to grow at a steady CAGR during the forecast period, driven by strong public healthcare systems, inclusive education policies, and increasing emphasis on early diagnosis and intervention for developmental disorders. Rising adoption of digital learning tools, AAC devices, and therapy-support software across schools and rehabilitation centers is contributing to market expansion. European countries are also focusing on improving accessibility standards and promoting inclusive digital education, which is accelerating the integration of assistive technologies in both public and private care systems.

U.K. Assistive Technology in Down Syndrome Market Insight

The U.K. assistive technology in down syndrome market is expected to grow at a notable CAGR, supported by increasing investment in special education needs (SEN) programs and strong adoption of digital health solutions. Rising awareness among caregivers and educators about early intervention tools is driving demand for speech therapy apps, communication boards, and AI-powered learning platforms. The National Health Service (NHS) and educational institutions are increasingly incorporating assistive technologies to improve developmental outcomes and communication skills.

Germany Assistive Technology in Down Syndrome Market Insight

The Germany assistive technology in down syndrome market is witnessing steady expansion due to strong healthcare infrastructure, technological innovation, and a high focus on rehabilitation and inclusive education. Demand for structured, privacy-compliant, and clinically validated assistive solutions is increasing, particularly in the areas of speech development and cognitive training. Germany’s emphasis on precision healthcare and digital transformation is supporting the integration of AI-based therapy tools and adaptive communication systems in both clinical and educational environments.

Asia-Pacific Assistive Technology in Down Syndrome Market Insight

The Asia-Pacific assistive technology in down syndrome market is expected to grow at the fastest CAGR during the forecast period of 2026 to 2033. Growth is driven by improving healthcare access, rising government initiatives for special needs education, increasing disposable incomes, and expanding penetration of mobile-based assistive applications. Countries such as India, China, and Southeast Asian nations are witnessing rapid adoption of affordable digital therapy platforms, speech development apps, and cloud-based learning tools. Expanding internet connectivity and growing awareness of developmental disorders are further accelerating market penetration across both urban and semi-urban regions.

Japan Assistive Technology in Down Syndrome Market Insight

The Japan assistive technology in down syndrome market is gaining momentum due to its advanced healthcare ecosystem, strong technological adoption, and high emphasis on precision learning solutions. Demand is increasing for AI-driven communication tools, robotics-assisted learning aids, and integrated AAC systems designed for both educational and home environments. Japan’s aging population and strong focus on inclusive education are also contributing to the adoption of user-friendly, adaptive assistive technologies.

China Assistive Technology in Down Syndrome Market Insight

The China assistive technology in down syndrome market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid urbanization, a growing middle class, and strong government support for digital healthcare and inclusive education initiatives. Widespread adoption of mobile-based learning applications, AI-powered speech development tools, and affordable AAC solutions is significantly boosting market growth. The expansion of domestic technology providers and smart education platforms is further improving accessibility and affordability, enabling broader adoption across schools, therapy centers, and home-care settings.

Assistive Technology in Down Syndrome Market Share

The Assistive Technology in Down Syndrome industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Sonova Group (Switzerland)

- Tobii Dynavox (Sweden)

- OrCam Technologies (Israel)

- Widex (Denmark)

- GN Store Nord (Denmark)

- Cochlear Limited (Australia)

- Jabbla (Belgium)

- AbleNet Inc. (U.S.)

- Attainment Company (U.S.)

- Lingraphica (U.S.)

- Smartbox Assistive Technology (U.K.)

- PRC-Saltillo (U.S.)

- LeapFrog Enterprises (U.S.)

- Sensory Software International (U.K.)

- Rehadapt Engineering (Germany)

- Freedom Scientific (U.S.)

- Don Johnston Inc. (U.S.)

- Inclusive Technology (U.K.)

- Komodo OpenLab (U.S.)

Latest Developments in Global Assistive Technology in Down Syndrome Market

- In June 2021, Tobii Dynavox introduced significant updates to its Snap Core First AAC (Augmentative and Alternative Communication) platform, enhancing its symbol-based communication system to better support individuals with speech and cognitive challenges, including those with Down syndrome. The update focused on improving ease of navigation, expanding vocabulary access, and adding smarter word prediction features, making it easier for users to construct sentences and communicate daily needs with greater independence

- In September 2022, Apple strengthened its accessibility ecosystem across iPhone and iPad devices, enabling smoother integration of third-party communication applications such as Proloquo2Go. These improvements included deeper compatibility with system-level accessibility tools like VoiceOver and voice-based interaction features. As a result, individuals with Down syndrome benefited from more seamless communication experiences using mainstream consumer devices rather than specialized assistive hardware

- In May 2023, AssistiveWare released a major upgrade to its AAC applications, including Proloquo2Go, focusing on improving usability for individuals with complex communication needs. The update introduced more intuitive vocabulary organization, faster symbol prediction, and simplified interface design. These enhancements were particularly valuable for users with Down syndrome, as they reduced cognitive load and made it easier to form expressive communication in everyday environments such as home and school

- In June 2023, researchers advanced the development of an AI-based communication system known as Talkitt, designed to interpret and translate unclear or non-standard speech patterns into understandable spoken language. The system was evaluated for its potential use among individuals with Down syndrome and other speech impairments. This development marked an important step toward using machine learning to bridge communication gaps and support natural speech expression

- In March 2024, new research introduced generative AI-assisted tools aimed at simplifying the creation of personalized communication boards and visual support systems. These tools were designed for caregivers and educators working with individuals with Down syndrome, enabling them to quickly generate customized communication aids without requiring technical expertise. The focus was on improving accessibility and reducing the time needed to build effective communication support systems

- In April 2024, studies examining the use of assistive communication technologies found a growing adoption of mobile-based applications among individuals with Down syndrome. The research highlighted that smartphones and tablets were becoming central tools for communication support, while also emphasizing the need for more adaptive and personalized solutions that align with individual learning abilities and daily environments

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.