Global Audio Codec Market

Market Size in USD Billion

USD

7.65 Billion

USD

12.47 Billion

2025

2033

USD

7.65 Billion

USD

12.47 Billion

2025

2033

| 2026 - 2033 | |

| USD 7.65 Billion | |

| USD 12.47 Billion | |

| % | |

|

Audio Codec Market Overview

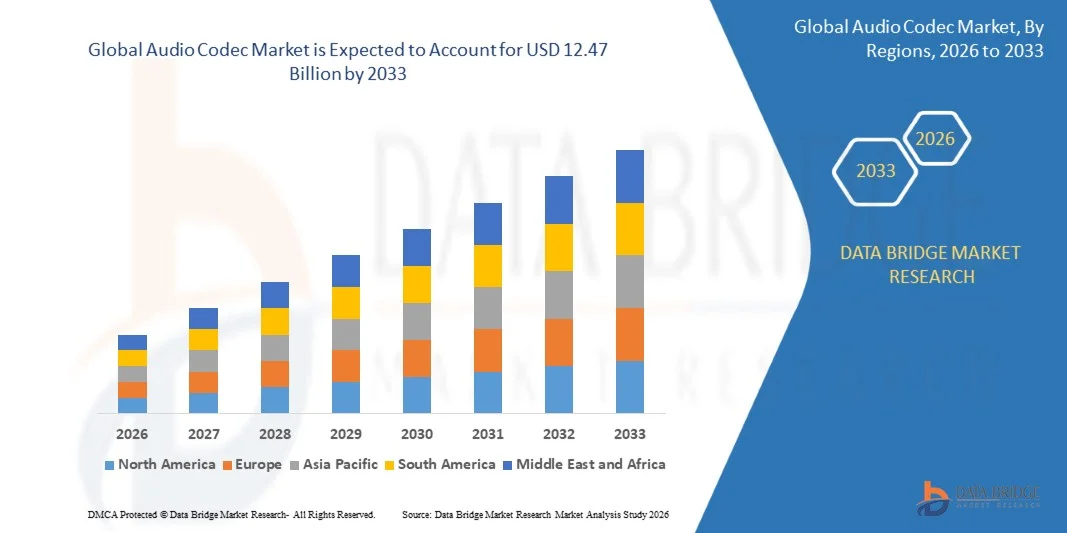

The Audio Codec Market was valued at USD 7.65 billion in 2025 and is projected to reach USD 12.47 billion by 2033, growing at a CAGR of 12.47% from 2026 to 2033. The market is experiencing steady growth driven by rising demand for high-quality audio streaming, increasing penetration of smartphones and smart devices, and growing consumption of digital media content across music, gaming, and video streaming platforms.

The rapid expansion of internet connectivity, combined with increasing adoption of wireless audio devices, smart speakers, and IoT-enabled consumer electronics, is driving demand for advanced audio codecs that deliver efficient compression, low latency, and high-fidelity sound quality. In addition, advancements in audio processing technologies, growing use of VoIP and video conferencing solutions, and increasing integration of immersive audio experiences in automotive infotainment and gaming applications are further supporting market expansion across both developed and emerging economies.

Market Size & Forecast

- Global Market Value (2025): USD 7.65 Billion

- Expected Market Value (2033): USD 12.47 Billion

- Forecast CAGR (2026–2033): 12.47%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the Audio Codec Market with the largest revenue share of 34.12% in 2025, supported by strong penetration of premium smartphones, advanced automotive infotainment systems, and early adoption of high-resolution audio technologies across consumer electronics and streaming platforms.

- The Lossy Audio Codecs segment dominated the market with a 52.34% share in 2025, driven by widespread adoption in streaming platforms, mobile communication, and digital content distribution where bandwidth efficiency and storage optimization are critical

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.8% from 2026 to 2033, driven by rapid smartphone manufacturing, expanding IoT ecosystems, increasing gaming console adoption, and strong semiconductor production bases in China, South Korea, Japan, and India.

- The smartphones & tablets segment dominated the application category with a 38.45% revenue share in 2025, owing to continuous demand for high-quality voice processing, music streaming optimization, and integration of AI-powered audio enhancement features in mobile devices.

- The automotive infotainment systems segment is projected to register the fastest CAGR of 8.1% from 2026 to 2033, supported by rising adoption of connected vehicles, in-car voice assistants, and premium audio systems integrated with ADAS and AI-based cockpit experiences.

Report Scope and Audio Codec Market Segmentation

|

Attributes |

Audio Codec Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Rising Demand for High-Quality Streaming and Immersive Audio Experiences · Growth in Smart Devices, IoT, and Automotive Infotainment Systems · Expansion of AI-Powered Communication and Real-Time Applications |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Audio Codec Market Trends

Trend: Growth in Immersive Audio, Gaming & Professional Simulation Ecosystems

The Audio Codec Market is increasingly shaped by the rising demand for high-resolution, low-latency, and spatial audio experiences across gaming, motorsports simulation, and professional training environments. Companies such as Dolby Laboratories have accelerated adoption of Dolby Atmos-enabled spatial audio codecs, which are now widely integrated into gaming consoles, VR headsets, and automotive infotainment systems. In 2023, Sony Interactive Entertainment expanded spatial audio support in the PlayStation ecosystem, enabling more realistic environmental sound positioning for racing and simulation games, significantly improving driver training simulators used in esports and professional motorsport academies. Similarly, automotive racing simulators used by teams in Formula racing increasingly rely on low-latency audio encoding pipelines integrated with real-time telemetry systems to replicate engine feedback, tire noise, and environmental acoustics with near-real-world accuracy.

Audio Codec Market Dynamics

Key Market Driver: Rising Adoption in Smartphones, Streaming & Automotive Infotainment

The rapid expansion of smartphones, OTT streaming platforms, and connected vehicles is a major driver of audio codec demand. Leading semiconductor firms such as Qualcomm have integrated advanced audio processing codecs into Snapdragon platforms, enabling high-efficiency compression for music streaming, voice assistants, and wireless earbuds. The rollout of 5G-enabled devices from 2021 onward significantly increased demand for efficient lossy codecs such as AAC and Opus, particularly for platforms like Spotify, YouTube, and Apple Music, where adaptive bitrate streaming requires optimized compression performance. In automotive, companies such as Bosch and major OEM infotainment suppliers have increasingly integrated advanced codec support into connected cockpit systems to enable multi-zone audio, voice assistants, and real-time navigation feedback.

Key Restraint/Challenge: Licensing Complexity and High IP Costs

A major challenge in the audio codec ecosystem is the fragmented intellectual property (IP) and licensing structure, especially for proprietary standards such as AAC, MP3 legacy licensing, and Dolby technologies. For instance, adoption of advanced codecs like Dolby AC-4 or MPEG-H often requires royalty-based licensing agreements, increasing cost burdens for OEMs and device manufacturers. This becomes particularly restrictive for low-cost smartphone manufacturers in emerging markets. In addition, interoperability issues between different codec standards (Opus vs AAC vs SBC in Bluetooth ecosystems) continue to create compatibility challenges in cross-device streaming and automotive infotainment integration.

Key Market Opportunity: AI-Powered Audio Processing and Edge Computing Integration

The integration of AI-based audio enhancement and edge processing represents a major growth opportunity. Modern audio codecs are increasingly combined with AI algorithms for noise cancellation, voice enhancement, and adaptive bitrate control. In 2024, Apple Inc. enhanced its spatial audio and adaptive EQ systems in AirPods Pro, leveraging real-time machine learning-based audio tuning to improve listening experiences in dynamic environments. Similarly, NVIDIA has expanded AI-driven audio processing capabilities in gaming and VR ecosystems, enabling real-time voice isolation and spatial sound reconstruction. The rise of edge AI chips in smartphones, IoT devices, and automotive systems is expected to further accelerate adoption of next-generation audio codecs optimized for ultra-low latency and high-efficiency compression.

Audio Codec Market Scope

The Audio Codec market is segmented on the basis of codec type, application, end user, technology, and deployment type

By Codec Type

On the basis of codec type, the Audio Codec Market is segmented into lossy audio codecs, lossless audio codecs, and hybrid codecs. The Lossy Audio Codecs segment dominated the market with a 52.34% share in 2025, driven by widespread adoption in streaming platforms, mobile communication, and digital content distribution where bandwidth efficiency and storage optimization are critical. These codecs, including AAC, MP3, and Opus, are extensively used across smartphones, OTT platforms, and gaming applications due to their ability to balance audio quality with compression efficiency. Growing consumption of online music and video streaming services continues to reinforce demand for lossy compression formats globally. Additionally, increasing integration of lossy codecs in automotive infotainment systems and smart devices is further strengthening their market dominance. Rising internet penetration and expansion of 5G networks are also accelerating adoption of high-efficiency streaming audio formats. The segment is expected to maintain its dominance but witness moderate maturity growth, with a CAGR of 5.9% from 2026 to 2033, as hybrid and AI-enhanced codecs gradually gain traction. Continuous optimization of perceptual audio encoding techniques is further improving compression efficiency. However, legacy ecosystem dependency continues to support long-term demand stability.

The Hybrid Codecs segment is expected to witness the fastest growth at a CAGR of 8.4% from 2026 to 2033, driven by rising demand for adaptive audio compression technologies that dynamically balance quality and bandwidth usage. Hybrid codecs combine features of both lossy and lossless formats, making them highly suitable for modern streaming, gaming, and immersive XR applications. Increasing adoption in cloud gaming platforms and real-time communication systems is significantly boosting segment growth. Expansion of spatial audio and AI-enhanced audio processing is further supporting hybrid codec innovation. These codecs are also gaining traction in automotive infotainment systems for adaptive in-cabin audio experiences. Continuous advancements in edge computing and AI-driven audio optimization are improving performance efficiency. Rising demand for ultra-low latency communication in metaverse applications is further fueling adoption. The segment is expected to see strong R&D investments from major semiconductor and audio technology companies.

By Application

On the basis of application, the Audio Codec Market is segmented into Smartphones & Tablets, Laptops & PCs, Smart Speakers & IoT Devices, Automotive Infotainment Systems, and Gaming Consoles. The Smartphones & Tablets segment dominated the market with a 39.18% share in 2025, driven by massive global smartphone penetration and increasing demand for high-quality audio streaming, voice communication, and AI-based voice assistants. Audio codecs are a core component in mobile chipsets enabling efficient media playback and real-time voice processing. Strong adoption of OTT platforms such as music and video streaming services continues to reinforce demand. Increasing use of Bluetooth audio devices and wireless earbuds further supports codec integration. The segment benefits from continuous chipset innovation by companies like Qualcomm and MediaTek. Growth in short-video platforms and social media audio content is also driving demand. Expansion of 5G networks enhances real-time high-resolution audio transmission. Rising consumer preference for immersive mobile audio experiences continues to strengthen market dominance. The segment is expected to grow steadily with a CAGR of 6.8% from 2026 to 2033.

The Automotive Infotainment Systems segment is expected to witness the fastest growth at a CAGR of 9.1% from 2026 to 2033, driven by rapid digitalization of vehicle cabins and increasing integration of connected infotainment platforms. Modern vehicles are increasingly adopting multi-zone audio systems and voice-controlled interfaces powered by advanced codecs. Growth of electric and autonomous vehicles is further accelerating in-car digital experience requirements. OEMs are integrating spatial audio and AI-based voice assistants to enhance user experience. Rising demand for premium in-vehicle entertainment systems is boosting adoption of high-efficiency codecs. Expansion of software-defined vehicle architectures is further supporting integration flexibility. Increasing use of real-time navigation and communication systems is enhancing codec relevance. Continuous innovation in automotive HMI systems is expected to significantly drive long-term market expansion.

By End User

On the basis of end user, the Audio Codec Market is segmented into Consumer Electronics, Automotive, Media & Entertainment, Telecommunications, Healthcare, and Others. The Consumer Electronics segment dominated the market with a 42.76% share in 2025, driven by widespread adoption of smartphones, smart speakers, laptops, wireless earbuds, and home entertainment devices. Increasing demand for high-fidelity audio streaming and voice-enabled smart devices continues to fuel codec integration. Strong ecosystem development by major technology companies is accelerating adoption of advanced compression standards. Growing popularity of smart home devices and IoT ecosystems further strengthens demand. Continuous innovation in wearable audio devices is also supporting growth. Rising consumption of digital media content globally is a major contributing factor. Expansion of cloud-based streaming platforms is further increasing codec utilization. The segment is expected to grow steadily with a CAGR of 6.5% from 2026 to 2033.

The Automotive segment is expected to witness the fastest growth at a CAGR of 9.0% from 2026 to 2033, driven by increasing integration of advanced infotainment systems and in-vehicle communication technologies. Rising adoption of electric vehicles and autonomous driving platforms is enhancing demand for immersive audio experiences. OEMs are increasingly focusing on personalized cabin experiences powered by AI-driven audio systems. Growth in connected car ecosystems is further accelerating codec deployment. Increasing demand for voice-based vehicle control systems is strengthening adoption. Expansion of premium vehicle segments is supporting high-end audio system integration. Rising collaboration between automotive OEMs and semiconductor companies is driving innovation. Continuous advancement in software-defined vehicle architecture is expected to further accelerate market expansion.

Audio Codec Market Regional Analysis

North America dominated the Audio Codec Market and accounted for the largest revenue share of 34.12% in 2025, supported by strong penetration of premium smartphones, advanced automotive infotainment systems, and early adoption of high-resolution audio technologies across consumer electronics and streaming platforms. The region also benefits from a highly developed digital ecosystem, widespread availability of high-speed internet, and strong demand for immersive audio experiences across entertainment, gaming, and communication applications.

U.S. Audio Codec Market Insight

The U.S. audio codec market is witnessing strong growth due to rising consumption of streaming services, increasing adoption of wireless audio devices, and rapid expansion of smart home ecosystems. Strong presence of leading technology companies and continuous innovation in audio compression, spatial audio, and AI-driven sound processing are further driving market demand across consumer electronics, automotive, and media applications.

Europe Audio Codec Market Insight

The Europe audio codec market remains a major contributor to global revenue, driven by high adoption of premium consumer electronics, strong automotive infotainment integration, and increasing demand for high-quality digital media experiences. Growth is further supported by advancements in wireless communication technologies and expanding use of audio codecs in automotive, telecommunications, and smart device ecosystems.

U.K. Audio Codec Market Insight

The U.K. audio codec market is experiencing steady growth, supported by increasing streaming consumption, rising demand for smart devices, and growing integration of advanced audio technologies in automotive and media applications. Expanding adoption of cloud-based communication platforms and digital entertainment services is further contributing to market expansion.

Germany Audio Codec Market Insight

The Germany audio codec market is expanding steadily due to strong automotive industry integration, rising adoption of premium infotainment systems, and increasing demand for high-quality audio in industrial and consumer applications. Continuous advancements in connected vehicle technologies and smart electronics are further supporting market growth.

Asia-Pacific Audio Codec Market Insight

The Asia-Pacific audio codec market is expected to be the fastest-growing region, registering a CAGR of 7.8% from 2026 to 2033, driven by rapid smartphone manufacturing, expanding IoT ecosystems, increasing gaming console adoption, and strong semiconductor production bases in China, South Korea, Japan, and India. Rising digital consumption, growing middle-class population, and strong demand for affordable smart devices are further accelerating regional market expansion.

Japan Audio Codec Market Insight

The Japan audio codec market is witnessing consistent growth due to strong demand for advanced consumer electronics, high adoption of gaming devices, and increasing integration of premium audio technologies in automotive infotainment systems. The country’s focus on high-quality audio engineering and innovation in electronics continues to support market development.

China Audio Codec Market Insight

The China audio codec market is growing rapidly, driven by large-scale smartphone production, expanding smart device ecosystem, and rising consumption of digital entertainment content. Strong semiconductor manufacturing base, increasing adoption of IoT devices, and rapid growth of streaming platforms are positioning China as one of the fastest-growing markets globally.

Audio Codec Market Share

The Audio Codec industry is primarily led by well-established companies, including:

- Moog Inc. (U.S.)

- Dallara (Italy)

- Exail (France)

- IPG Automotive GmbH (Germany)

- aiMotive (Hungary)

- VI‑grade GmbH (Germany)

- Cruden B.V. (Netherlands)

- Dynisma Ltd. (UK)

- Applied Intuition Inc. (U.S.)

- rFpro (rFpro Limited) (England)

- Siemens AG (Germany)

- Dassault Systèmes SE (France)

- MTS Systems Corporation (U.S.)

- CAE Inc. (Canada)

- NVIDIA Corporation (U.S.)

- AB Dynamics PLC (U.K.)

- Forum8 (Japan)

- Mitsubishi Precision Co., Ltd. (Japan)

- FAAC Incorporated (U.S.)

- DriveSafety (U.S.)

- Simtec Simulation Technology GmbH (Germany)

- MB Dynamics Inc. (U.S.)

- Sanlab Simulation (India)

- SimCraft (U.S.)

- CXC Simulations (U.S.)

- XPI Simulation (United Kingdom)

- Tecknotrove Simulator Systems Pvt. Ltd. (India)

- Zhejiang Kechi Intelligent Technology Co., Ltd. (China)

- Shenzhen Zhongzhi Simulation (China)

- Hindustan Simulators (India)

- DriveSimSolutions (U.S.)

- Teksim Technologies (India)

- iMVR Inc. (U.S.)

- SimXperience (U.S.)

Latest Developments in Audio Codec Market

- In September 2025, Moog Inc. has unveiled its latest motion systems all electric E60 Series and the electro pneumatic P60 Series, setting a new benchmark for simulation across aviation, land, and maritime training with support for up to 14,000 kg loads and high fidelity motion for Level D flight simulators and other professional uses. The upgraded platforms deliver enhanced reliability, compact design and sustained operational uptime, reflecting modernized electronics and sustainable operation. These new systems strengthen Moog’s market leadership in simulation motion technology by boosting performance, energy efficiency, and usability

- In January 2025, Exail Technologies has acquired Leukos, a French photonics specialist known for pulsed micro lasers, supercontinuum laser sources, ultrafast lasers, and simulation-enabled optical systems, strengthening its technological and industrial capabilities in advanced laser and simulation technologies. The deal integrates Leukos’s expertise with Exail’s photonics, optical, and simulation platforms, broadening product offerings for applications in biophotonics, microelectronics, and high-fidelity training simulations. This strategic acquisition accelerates Exail’s innovation in high-tech technologies, creating synergies that expand its reach in scientific, industrial, and simulation applications while reinforcing its position as a leading advanced-technology provider

- In November 2025, IPG Automotive launched CarMaker 15.0, the latest version of its driving simulation software used for virtual vehicle development. The new release improves simulation accuracy by integrating virtual electronic control units (vECUs), allowing engineers to test software and vehicle systems at earlier development stages. It also includes enhanced sensor models and improved endurance testing capabilities for ADAS and autonomous vehicles. This development strengthens IPG Automotive’s position in the driving simulator market, as CarMaker enables automotive manufacturers to perform complex vehicle tests in a virtual driving environment instead of physical road testing.

- In November 2024, IPG Automotive released CarMaker 14.0, introducing new simulation capabilities including advanced sensor models and more realistic virtual environments. The update allows developers to simulate complex traffic scenarios involving pedestrians, vehicles, and different weather conditions. These features help automotive companies test ADAS and autonomous driving systems more efficiently in driving simulators, reducing development time and cost. The upgrade also expanded simulation capabilities for heavy-duty vehicles using the TruckMaker platform.

- In June 2023, IPG Automotive participated in the UNICARagil research project, collaborating with universities and industry partners to develop automated vehicle architectures. The company contributed its CarMaker driving simulation platform to support simulation and validation of automated driving systems in Software-in-the-Loop (SIL) and Hardware-in-the-Loop (HIL) environments. This collaboration demonstrates the application of Audio Codec in research and development of autonomous mobility solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.