Global Automotive Aluminum Market

Market Size in USD Billion

USD

32.41 Billion

USD

64.10 Billion

2025

2033

USD

32.41 Billion

USD

64.10 Billion

2025

2033

| 2026 - 2033 | |

| USD 32.41 Billion | |

| USD 64.10 Billion | |

| % | |

|

Automotive Aluminum Market Size

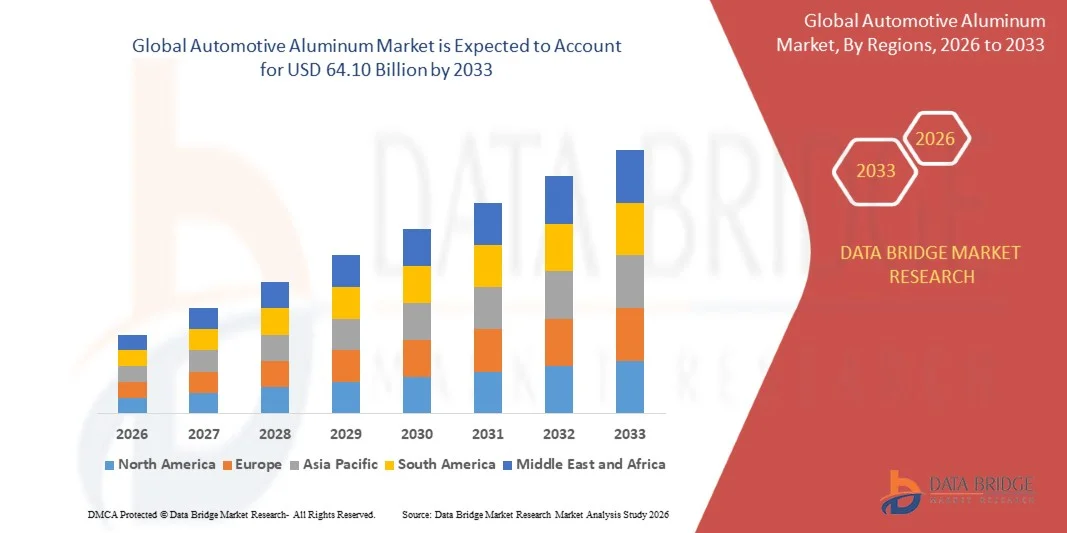

- The global automotive aluminum market size was valued at USD 32.41 billion in 2025 and is expected to reach USD 64.10 billion by 2033, at a CAGR of 8.90% during the forecast period

- The market growth is largely fueled by the increasing demand for vehicle lightweighting and improved fuel efficiency, leading to higher adoption of aluminum as a key structural and body material in automotive manufacturing

- Furthermore, rapid expansion of electric vehicle production, stringent emission regulations, and continuous advancements in aluminum alloy technologies are strengthening the shift toward high-performance lightweight materials, thereby significantly boosting the industry’s growth

Automotive Aluminum Market Analysis

- Automotive aluminum, widely used in vehicle body panels, engine components, chassis systems, and battery enclosures, has become a critical material in modern vehicle design due to its high strength-to-weight ratio, corrosion resistance, and recyclability

- The escalating demand for automotive aluminum is primarily driven by the global transition toward electric mobility, increasing focus on carbon emission reduction, and rising adoption of sustainable and fuel-efficient vehicle architectures

- Asia-Pacific dominated the automotive aluminum market with a share of6% in 2025, due to strong vehicle production, rapid electrification, and rising demand for lightweight components in passenger and commercial vehicles

- North America is expected to be the fastest growing region in the automotive aluminum market during the forecast period due to rising demand for electric vehicles, pickup trucks, and fuel-efficient automotive designs

- Cast Aluminum segment dominated the market with a market share of 45.5% in 2025, due to its extensive use in complex automotive components such as engine blocks, transmission housings, and structural parts. Automakers prefer cast aluminum due to its excellent castability, allowing the production of intricate shapes with high precision and reduced material waste

Report Scope and Automotive Aluminum Market Segmentation

|

Attributes |

Automotive Aluminum Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Aditya Birla Management Corporation Pvt. Ltd. (India) · Alcoa Corporation (U.S.) · Constellium (France) · AMG Aluminium (Netherlands) · UACJ Corporation (Japan) · Norsk Hydro ASA (Norway) · Rio Tinto (U.K.) · Novelis Aluminum (U.S.) · ElringKlinger (Germany) · Progress-Werk Oberkirch AG (Germany) · Dynacast (U.S.) · Aluminium Bahrain (Alba) (Bahrain) · Gränges (Sweden) · GIBBS (U.S.) · Endurance Technologies Limited (India) · RYOBI Aluminium Casting (UK) Ltd (U.K.) · CITIC Dicastal Co., Ltd (China) · Vedanta Resources Limited (India) |

|

Market Opportunities |

· Expansion of Electric Vehicle Battery Enclosures and Structural Applications · Growth in Automotive Recycling and Circular Aluminum Supply Chains |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Automotive Aluminum Market Trends

“Increasing Adoption of Aluminum in Electric Vehicle Lightweighting”

- A significant trend in the automotive aluminum market is the rising adoption of aluminum in electric vehicle platforms, where manufacturers are increasingly focusing on lightweight structural designs to extend driving range and improve energy efficiency. This shift is accelerating the use of aluminum in body-in-white structures, battery housings, and crash management systems across global EV production

- For instance, Tesla Inc. uses extensive aluminum-intensive body structures in models such as the Model S and Model X, supporting weight reduction and improved battery efficiency. Such applications highlight how aluminum is becoming central to EV design optimization and performance enhancement

- Automakers are increasingly integrating high-strength aluminum alloys into chassis and closure systems to replace heavier steel components, improving overall vehicle dynamics and reducing emissions. This transition is strengthening aluminum’s role in next-generation mobility platforms focused on sustainability and efficiency

- The growing penetration of electric SUVs and long-range EVs is further increasing demand for advanced aluminum solutions that offer durability while maintaining low weight. This is encouraging continuous innovation in alloy development and structural engineering within the automotive sector

- Global automotive OEMs are also collaborating with aluminum producers to develop customized lightweight solutions tailored for EV architectures. This collaboration is accelerating material innovation and expanding application scope across passenger and commercial electric vehicles

- The trend is further reinforced by the industry-wide push toward decarbonization, where aluminum’s recyclability and energy efficiency advantages are making it a preferred material in sustainable vehicle manufacturing strategies

Automotive Aluminum Market Dynamics

Driver

“Rising Demand for Fuel-Efficient and Low-Emission Vehicles”

- The growing emphasis on fuel efficiency and emission reduction across global automotive markets is driving strong demand for aluminum due to its lightweight properties and ability to enhance vehicle performance. This is leading to increased substitution of traditional materials such as steel with aluminum in critical automotive applications

- For instance, Ford Motor Company has significantly increased aluminum usage in its F-150 pickup trucks to improve fuel efficiency and reduce overall vehicle weight. This application demonstrates how automakers are leveraging aluminum to meet stringent emission standards while maintaining performance and durability

- Stringent regulatory frameworks in regions such as Europe and North America are encouraging automakers to adopt lightweight materials that help reduce carbon emissions across vehicle fleets. This regulatory pressure is accelerating aluminum integration in both internal combustion engine vehicles and hybrid models

- The rising cost of fuel and growing consumer preference for energy-efficient vehicles are further supporting aluminum adoption across automotive production lines. This demand is influencing OEMs to redesign vehicle structures using advanced aluminum alloys for improved mileage performance

- Overall, the combined impact of regulatory mandates, consumer demand, and technological advancements is reinforcing aluminum’s position as a key enabler of lightweight and low-emission vehicle development

Restraint/Challenge

“High Cost of Primary Aluminum Production and Energy Intensive Processing”

- The automotive aluminum market faces significant challenges due to the high cost and energy-intensive nature of primary aluminum production, which increases overall material pricing and impacts profitability for manufacturers. The smelting process requires substantial electricity consumption, making production highly sensitive to energy price fluctuations

- For instance, Rio Tinto operates large-scale aluminum smelting facilities that rely heavily on stable and low-cost energy sources, highlighting the cost burden associated with primary aluminum production. These operational requirements significantly influence production economics and global supply chain competitiveness

- The dependence on bauxite mining, alumina refining, and electrolysis adds multiple cost layers to the production process, making aluminum more expensive compared to conventional automotive materials. This cost structure limits its adoption in cost-sensitive vehicle segments despite its performance benefits

- Energy price volatility in major producing regions further impacts manufacturing stability and increases uncertainty in long-term supply contracts. This creates challenges for automakers seeking consistent and affordable material sourcing

- Overall, the combination of high energy consumption, complex production processes, and regulatory compliance burdens continues to restrain cost competitiveness in the automotive aluminum market despite strong demand growth

Automotive Aluminum Market Scope

The market is segmented on the basis of product form, vehicle type, and application.

- By Product Form

On the basis of product form, the automotive aluminum market is segmented into cast aluminum, rolled aluminum, and extruded aluminum. The cast aluminum segment dominated the market with the largest market revenue share of 45.5% in 2025, driven by its extensive use in complex automotive components such as engine blocks, transmission housings, and structural parts. Automakers prefer cast aluminum due to its excellent castability, allowing the production of intricate shapes with high precision and reduced material waste. The segment benefits from strong demand for lightweight yet durable components that enhance fuel efficiency and reduce emissions. In addition, advancements in casting technologies have improved mechanical strength and thermal performance, making cast aluminum suitable for both conventional and electric vehicles. Its cost-effectiveness in mass production further strengthens its dominance across global automotive manufacturing.

The extruded aluminum segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for lightweight structural components and improved crash management systems. Extruded aluminum offers high strength-to-weight ratio and design flexibility, making it ideal for applications such as frames, beams, and battery enclosures in electric vehicles. The growing focus on vehicle electrification and safety regulations is driving the adoption of extruded components due to their energy absorption capabilities. Automakers are increasingly leveraging extrusion processes to develop modular and scalable vehicle architectures. In addition, recyclability and sustainability benefits of extruded aluminum align with environmental goals, further supporting its rapid market expansion.

- By Vehicle Type

On the basis of vehicle type, the automotive aluminum market is segmented into passenger cars, light commercial vehicles (LCV), and heavy commercial vehicles (HCV). The passenger cars segment dominated the market with the largest market revenue share in 2025, driven by high production volumes and increasing integration of aluminum to improve fuel efficiency and reduce overall vehicle weight. Stringent emission regulations and rising consumer demand for performance-oriented vehicles have encouraged manufacturers to replace traditional steel with aluminum in body panels, engine components, and structural parts. The segment also benefits from rapid growth in electric passenger vehicles, where lightweight materials are essential for extending battery range. Continuous innovations in aluminum alloys further enhance durability and safety, strengthening adoption in this segment.

The light commercial vehicles (LCV) segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by expanding e-commerce logistics and last-mile delivery demand. LCV manufacturers are increasingly adopting aluminum to enhance payload capacity while maintaining fuel efficiency and compliance with emission norms. The shift toward electric delivery vans is further accelerating aluminum usage, as lightweight materials help optimize battery performance and vehicle range. In addition, durability and corrosion resistance of aluminum make it suitable for intensive commercial operations. Growing urbanization and transportation needs are expected to significantly boost demand for aluminum in this segment.

- By Application

On the basis of application, the automotive aluminum market is segmented into powertrain, chassis and suspension, and car body. The powertrain segment dominated the market with the largest market revenue share in 2025, driven by widespread use of aluminum in engine components, transmission systems, and heat exchangers. Aluminum’s excellent thermal conductivity and lightweight properties make it highly suitable for improving engine efficiency and reducing overall vehicle emissions. Automakers increasingly utilize aluminum in both internal combustion engines and hybrid systems to enhance performance and fuel economy. The segment also benefits from advancements in alloy formulations that improve strength and durability under high temperatures. Its critical role in optimizing vehicle efficiency continues to support its dominance.

The car body segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising adoption of lightweight body structures in electric and premium vehicles. Aluminum is increasingly used in body panels, doors, hoods, and structural frames to reduce vehicle weight and improve energy efficiency. The shift toward electric mobility has intensified demand for lightweight materials to extend driving range and enhance performance. In addition, aluminum offers superior corrosion resistance and design flexibility, enabling modern vehicle aesthetics and durability. Growing investments in aluminum-intensive vehicle platforms are expected to significantly accelerate growth in this segment.

Automotive Aluminum Market Regional Analysis

- Asia-Pacific dominated the automotive aluminum market with the largest revenue share of 38.6% in 2025, driven by strong vehicle production, rapid electrification, and rising demand for lightweight components in passenger and commercial vehicles

- The region benefits from large-scale aluminum refining and smelting capacity, cost-efficient manufacturing ecosystems, and strong integration across automotive OEM supply chains

- Rapid industrialization, expansion of electric vehicle production, and increasing adoption of fuel-efficient lightweight materials are accelerating market expansion

China Automotive Aluminum Market Insight

China held the largest share in the Asia-Pacific automotive aluminum market in 2025, supported by its dominant automotive manufacturing base and extensive aluminum production infrastructure. The country is a leading hub for electric vehicle manufacturing, which significantly increases demand for lightweight aluminum components in body structures and battery enclosures. Strong domestic consumption, integrated supply chains, and high production capacity across primary and secondary aluminum strengthen its leadership position. In addition, continuous investments in green mobility and advanced metallurgy are reinforcing China’s dominance in automotive aluminum usage.

India Automotive Aluminum Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by rising passenger vehicle production, expanding two-wheeler demand, and increasing adoption of fuel-efficient materials. Government initiatives supporting electric mobility and domestic manufacturing are boosting aluminum consumption in automotive applications. The growing presence of global OEMs and expansion of local component manufacturing are further strengthening market demand. In addition, infrastructure development and rising export-oriented automotive production are accelerating long-term growth.

Europe Automotive Aluminum Market Insight

The Europe automotive aluminum market is expanding steadily, supported by strong automotive engineering capabilities and strict emission reduction targets. The region emphasizes lightweight vehicle design to improve fuel efficiency and support electric mobility transition. High adoption of premium vehicles and advanced automotive technologies is further increasing aluminum usage in structural and powertrain components. In addition, sustainability regulations and circular economy practices are encouraging greater recycling and reuse of aluminum materials.

Germany Automotive Aluminum Market Insight

Germany accounted for the largest share in the Europe automotive aluminum market in 2025, driven by its strong automotive manufacturing industry and leadership in premium vehicle production. The country extensively uses aluminum in vehicle body structures, chassis systems, and electric mobility platforms. Advanced engineering expertise and strong R&D capabilities support continuous innovation in lightweight automotive materials. In addition, collaboration between automotive OEMs and aluminum producers is strengthening Germany’s position in high-performance vehicle manufacturing.

U.K. Automotive Aluminum Market Insight

The U.K. market is supported by growing demand for lightweight vehicles, increasing electric vehicle adoption, and strong automotive R&D activities. The country is focusing on reducing vehicle emissions, which is driving the shift toward aluminum-intensive vehicle design. Expanding luxury and performance vehicle segments are further supporting aluminum consumption. In addition, investments in automotive innovation hubs and material engineering development are strengthening market growth.

North America Automotive Aluminum Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising demand for electric vehicles, pickup trucks, and fuel-efficient automotive designs. Strong adoption of aluminum in vehicle lightweighting applications is supporting improved performance and emission reduction goals. Continuous innovation in aluminum alloys and automotive engineering is expanding application scope. In addition, reshoring of automotive manufacturing and increasing investment in EV battery and structural components are accelerating regional growth.

U.S. Automotive Aluminum Market Insight

The U.S. accounted for the largest share in the North America automotive aluminum market in 2025, supported by strong automotive production, high EV adoption, and advanced material innovation capabilities. The country benefits from a well-established automotive supply chain and strong presence of leading aluminum producers. Aluminum is widely used in body panels, engine components, and electric vehicle structures to improve efficiency and reduce weight. In addition, stringent fuel economy standards and ongoing technological advancements are reinforcing the U.S. leadership in automotive aluminum demand.

Automotive Aluminum Market Share

The automotive aluminum industry is primarily led by well-established companies, including:

- Aditya Birla Management Corporation Pvt. Ltd. (India)

- Alcoa Corporation (U.S.)

- Constellium (France)

- AMG Aluminium (Netherlands)

- UACJ Corporation (Japan)

- Norsk Hydro ASA (Norway)

- Rio Tinto (U.K.)

- Novelis Aluminum (U.S.)

- ElringKlinger (Germany)

- Progress-Werk Oberkirch AG (Germany)

- Dynacast (U.S.)

- Aluminium Bahrain (Alba) (Bahrain)

- Gränges (Sweden)

- GIBBS (U.S.)

- Endurance Technologies Limited (India)

- RYOBI Aluminium Casting (UK) Ltd (U.K.)

- CITIC Dicastal Co., Ltd (China)

- Vedanta Resources Limited (India)

Latest Developments in Global Automotive Aluminum Market

- In September 2024, Novelis advanced its automotive recycling and alloy innovation strategy by introducing high-performance aluminum alloys engineered to incorporate increased recycled content without reducing structural integrity or durability. The company also deployed AI-driven sorting systems and optical identification technologies to improve separation of end-of-life vehicle scrap, enabling more efficient closed-loop recycling. These advancements support single-alloy vehicle closure designs such as doors and hoods, strengthening design-for-disassembly practices. The development significantly reduces dependence on primary aluminum, enhances circular economy integration, and improves sustainability performance across automotive manufacturing

- In July 2024, Hydro strengthened its decarbonization strategy through a long-term agreement with Porsche to supply low-carbon and recycled aluminum for automotive applications. The collaboration ensures delivery of aluminum with a high proportion of post-consumer scrap content while also promoting joint development of advanced alloys with lower carbon intensity. The partnership further focuses on integrating emission-free smelting technologies into future production systems. This initiative is accelerating the shift toward sustainable material sourcing and supporting automakers in achieving carbon neutrality targets across premium vehicle segments

- In April 2024, Vedanta Aluminium expanded its automotive-focused portfolio through the AutoEdge 2024 industry conclave in New Delhi, where it introduced a wide range of specialized aluminum products for modern vehicle manufacturing. The company showcased high-strength crash-resistant components and advanced foundry alloys designed for engine and structural applications in both ICE and electric vehicles. The initiative emphasized localized supply capabilities and customized alloy development to meet evolving automotive design requirements. This development is strengthening domestic value chains while supporting lightweighting and performance optimization in the automotive sector

- In March 2024, Rio Tinto announced the expansion of its low-carbon aluminum production capabilities through enhanced renewable energy integration at its smelting operations in Canada, aimed at supplying the automotive industry with greener material solutions. The initiative focuses on reducing greenhouse gas emissions across primary aluminum production while increasing availability of sustainably produced metal for vehicle manufacturing. The company also emphasized collaboration with automotive OEMs to scale adoption of low-emission aluminum in structural and body applications. This development is accelerating sustainability transformation in the automotive aluminum supply chain and supporting global decarbonization efforts

- In January 2024, Constellium unveiled its next-generation automotive aluminum solutions at CES 2024 in Las Vegas, focusing on structural innovations for electric vehicles and lightweight mobility systems. The company introduced advanced crash management systems, laser-welded battery enclosures, and reinforced structural components designed to enhance safety and stiffness while reducing overall vehicle weight. These innovations directly address the growing demand for EV-specific lightweight materials. The development is reinforcing the role of high-performance aluminum in improving energy efficiency, safety standards, and emissions reduction in modern automotive design

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Automotive Aluminum Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Automotive Aluminum Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Automotive Aluminum Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.