Global Automotive Angular Positions Sensors Market

Market Size in USD Billion

USD

14.88 Billion

USD

27.33 Billion

2025

2033

USD

14.88 Billion

USD

27.33 Billion

2025

2033

| 2026 - 2033 | |

| USD 14.88 Billion | |

| USD 27.33 Billion | |

| % | |

|

Automotive Angular Positions Sensors Market Overview

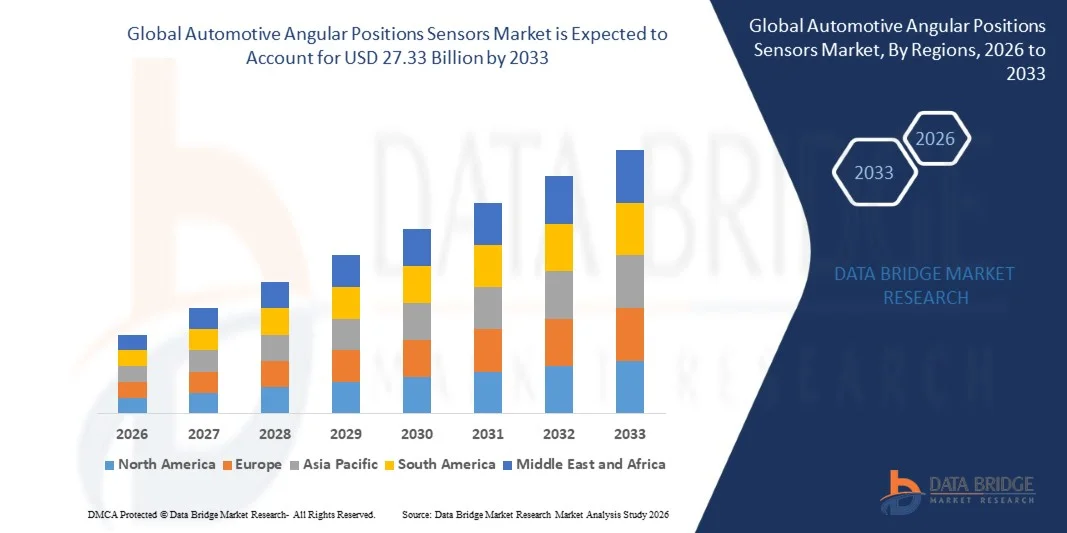

The Automotive Angular Positions Sensors Market was valued at USD 14.88 billion in 2025 and is projected to reach USD 27.33 billion by 2033, growing at a CAGR of 7.90% from 2026 to 2033. The market is experiencing strong growth driven by increasing vehicle electrification, rising adoption of advanced driver assistance systems (ADAS), and growing demand for precise motion detection in modern automotive systems. These sensors play a critical role in monitoring steering angle, throttle position, crankshaft position, and other rotational components, enabling improved vehicle safety, efficiency, and performance.

The rapid transition toward electric vehicles and autonomous driving technologies is further accelerating the adoption of angular position sensors across automotive platforms. Automakers are increasingly integrating high-precision, contactless sensor technologies such as Hall-effect and magnetoresistive sensors to enhance durability, accuracy, and reliability under harsh operating conditions. In addition, stringent safety regulations and growing emphasis on fuel efficiency and emission reduction are compelling OEMs to adopt advanced sensing systems, supporting the expansion of this market globally.

Key Market Trends & Insights

- North America dominated the automotive angular position sensors market with the largest revenue share of 39.8% in 2025, supported by strong EV adoption, advanced automotive manufacturing infrastructure, and high integration of sensor-based safety and control systems across vehicles.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 9.2% from 2026 to 2033. Growth is driven by rapid expansion of electric vehicle production, increasing automotive manufacturing activities, and strong government support for smart mobility and electrification initiatives across China, India, and Japan.

- The Rotary Position Sensors segment held the largest market revenue share of approximately 58.4% in 2025 driven by its extensive use in steering angle detection, throttle position monitoring, and electric motor control systems. These sensors are widely adopted due to their high accuracy, durability, and ability to operate effectively in harsh automotive environments. Growing integration in electric power steering systems and drivetrain control units is further strengthening segment demand. Automotive OEMs prefer rotary sensors as they provide real time feedback for safety critical applications such as stability control and ADAS functionalities. Increasing electrification of vehicles is further expanding their deployment across next generation automotive platforms.

- The Linear Type segment is projected to register the fastest growth at a CAGR of 9.6% from 2026 to 2033, driven by increasing integration in suspension systems, pedal position sensing, and advanced chassis control applications in electric and autonomous vehicles. Rising demand for improved ride comfort and vehicle stability is accelerating adoption of linear sensing technologies. These sensors are also gaining traction in battery management systems for EVs to ensure precise mechanical movement monitoring. Advancements in compact sensor design and improved signal accuracy are further supporting market penetration. Expanding use in intelligent suspension and braking systems is expected to significantly boost long term demand.

- The Angular segment accounted for the largest market share of approximately 46.7% in 2025 due to its widespread use in steering systems, drivetrain monitoring, and engine control applications. These sensors are critical for ensuring precise angular measurement in rotating automotive components. Increasing integration in electronic stability programs and torque vectoring systems is further driving demand. Automotive manufacturers rely heavily on angular sensors to enhance vehicle safety and driving precision. Rising production of hybrid and electric vehicles is also strengthening segment growth globally.

- The Multi-Axis segment is expected to register the fastest growth at a CAGR of 10.4% from 2026 to 2033, driven by rising demand for high precision motion tracking in autonomous driving systems, robotics integration, and advanced driver assistance systems requiring real time multi directional sensing. These sensors enable simultaneous measurement across multiple planes, improving overall system intelligence. Increasing use in self driving platforms and smart mobility solutions is further boosting adoption. Automotive testing programs are increasingly deploying multi axis sensors for advanced vehicle dynamics analysis. Continuous innovation in sensor fusion technologies is expected to accelerate future growth.

- The Non-Contact Type segment dominated the market with a revenue share of approximately 71.2% in 2025 driven by strong adoption in electric vehicles and safety critical automotive systems. These sensors offer higher reliability, longer lifespan, and reduced wear and tear compared to traditional contact based systems. Their ability to function in harsh temperature and vibration conditions makes them ideal for automotive applications. Increasing adoption in EV powertrains and steering systems is further strengthening demand. Automotive OEMs prefer non contact sensors due to their maintenance free operation and higher accuracy levels.

- The Contact Type segment is anticipated to grow at a CAGR of 6.8% from 2026 to 2033 due to its continued use in cost sensitive vehicle segments and basic mechanical sensing applications. These sensors are widely used in entry level vehicles where affordability is a key consideration. Despite lower durability compared to non contact types, they remain relevant in conventional automotive systems. Manufacturers continue to optimize contact sensor designs to improve reliability and cost efficiency. Their usage is expected to remain steady in developing automotive markets.

- The Digital Output segment held the largest market share of approximately 62.9% in 2025 driven by increasing integration in modern electronic control units, ADAS systems, and EV platforms requiring high precision signal processing. Digital sensors provide enhanced accuracy, noise immunity, and seamless integration with vehicle control systems. Growing demand for software defined vehicles is further supporting adoption. Automotive OEMs are increasingly shifting toward digital architectures for improved performance. Rising electrification and connectivity trends are reinforcing segment dominance.

- The Analog Output segment is expected to grow steadily at a CAGR of 7.1% from 2026 to 2033 supported by its use in legacy systems and cost effective automotive applications. These sensors remain widely used in older vehicle platforms and industrial automotive applications. Their simple design and low cost make them suitable for basic sensing functions. However, gradual transition toward digital systems may limit long term expansion. Despite this, demand will persist in aftermarket and budget vehicle segments.

- The Electric segment dominated the market with a share of approximately 38.5% in 2025 driven by rapid global EV adoption and increasing demand for advanced sensing systems in electric drivetrains, battery management, and regenerative braking systems. EV manufacturers heavily rely on angular sensors for precise motor control and energy optimization. Government incentives supporting electric mobility are further accelerating adoption. Increasing EV production in China, Europe, and North America is strengthening demand. Integration of smart sensing technologies is becoming standard in modern EV architectures.

- The High End segment is projected to register the fastest growth at a CAGR of 9.9% from 2026 to 2033 due to increasing integration of advanced driver assistance systems and autonomous driving technologies in premium vehicles. Luxury automakers are incorporating high precision sensors for enhanced safety and performance features. Demand for intelligent mobility solutions and connected vehicle systems is further boosting adoption. High end vehicles are early adopters of advanced sensor technologies before mass market rollout. Continuous innovation in autonomous driving platforms is expected to accelerate segment growth.

- The Motion Systems segment held the largest market share of approximately 34.6% in 2025 driven by its widespread use in automotive steering, drivetrain control, and industrial automation systems. These systems require precise angular measurement for smooth and efficient operation. Increasing adoption in EV drivetrains and smart manufacturing systems is strengthening demand. Motion control applications benefit significantly from high accuracy sensing technologies. Rising automation trends across industries are further supporting segment expansion.

- The Robotics segment is expected to grow at the fastest CAGR of 10.7% from 2026 to 2033 due to rising adoption of automated manufacturing, warehouse robotics, and precision motion control systems across industries. Angular position sensors play a critical role in enabling precise robotic movement and coordination. Increasing deployment of industrial robots in automotive production lines is driving demand. Growth of e commerce logistics and warehouse automation is further accelerating adoption. Continuous advancements in AI enabled robotics are expected to support long term market growth.

Market Size & Forecast

- Global Market Value (2025): USD 14.88 Billion

- Expected Market Value (2033): USD 27.33 Billion

- Forecast CAGR (2026–2033): 7.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Automotive Angular Positions Sensors Market Segmentation

|

Attributes |

Automotive Angular Positions Sensors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Honeywell International Inc. (U.S.) |

|

Market Opportunities |

• Expansion Of Electric Vehicle Production And Electrification Of Automotive Systems • Increasing Integration Of Advanced Driver Assistance Systems And Autonomous Driving Technologies |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Angular Positions Sensors Market Trends

Trend: Growth In Electrification Driven Sensing And High Precision Motion Detection Systems

Increasing demand for high accuracy, compact, and energy efficient sensing technologies across automotive powertrain, safety, and electrification applications is driving strong adoption of angular position sensors. Conventional mechanical sensing systems are increasingly being replaced by contactless technologies such as Hall effect and magnetoresistive sensors due to higher durability, reduced wear, and improved performance under harsh automotive conditions.

In modern electric vehicles, manufacturers are integrating angular position sensors in steering systems, motor control units, and pedal position monitoring to improve driving precision and energy efficiency. For instance, Bosch has expanded its sensor integration in EV platforms for rotor position detection in electric motors, enabling smoother torque control and improved regenerative braking efficiency. In internal combustion and hybrid systems, these sensors are widely used for crankshaft and camshaft position monitoring, improving ignition timing accuracy and fuel efficiency.

The rapid expansion of advanced driver assistance systems and autonomous driving platforms is also increasing demand for multi axis angular sensing solutions capable of real time motion tracking. In addition, industrial and robotics applications are increasingly adopting high precision angular sensors for automated motion control and predictive maintenance systems. Growing validation through automotive testing programs in 2025 integrating high resolution angular sensors into EV steering and drivetrain systems has demonstrated improvements of nearly 6–10% in torque response accuracy and motion control stability under dynamic driving conditions

Global Automotive Angular Position Sensors Market Dynamics

Key Market Driver: Rising Adoption Of Vehicle Electrification And Advanced Driver Assistance Systems

Automotive manufacturers are facing increasing pressure to improve vehicle safety, efficiency, and automation capabilities, leading to widespread integration of high precision sensing technologies. Angular position sensors play a critical role in enabling accurate monitoring of rotational components such as steering wheels, electric motors, and throttle systems, supporting enhanced vehicle control and safety performance.

Automotive OEMs are increasingly deploying these sensors in electric and hybrid vehicles to support efficient motor control and regenerative braking systems. For instance, Tesla and several European automakers have integrated advanced rotor position sensing technologies to optimize electric drivetrain efficiency and improve acceleration response. Similarly, rising adoption of ADAS features such as lane keeping assist and electronic stability control is further strengthening demand for precise angular measurement systems.

In addition, growing regulatory focus on vehicle safety standards and emission reduction is accelerating adoption across global automotive platforms. Industry deployment data from 2024 indicates that modern ADAS equipped vehicles incorporate multiple angular sensing points per vehicle architecture, significantly increasing overall sensor penetration rates across passenger and commercial vehicle segments

Key Restraint/Challenge: High Calibration Complexity And Cost Sensitivity In Entry Level Vehicles

Despite strong adoption, angular position sensors face challenges related to calibration complexity, integration costs, and sensitivity to electromagnetic interference in automotive environments. High precision sensor systems require advanced calibration processes during vehicle assembly, increasing manufacturing time and system integration complexity.

In addition, cost sensitivity in entry level and mass market vehicles limits adoption of premium sensor technologies, particularly in emerging economies where affordability remains a key purchasing factor. Variability in operating conditions such as temperature fluctuations, vibration, and dust exposure can also impact long term sensor accuracy, requiring additional protective engineering and validation testing.

Industry assessments indicate that high precision automotive grade angular sensors can increase system cost by approximately 15–25% compared to conventional sensing solutions, creating adoption barriers in cost constrained vehicle segments despite their performance advantages

Key Market Opportunity: Expansion Of Electric Mobility And Autonomous Vehicle Development

The rapid growth of electric mobility, autonomous driving technologies, and software defined vehicles is creating significant opportunities for advanced angular position sensor integration. Modern EV platforms require precise real time monitoring of motor position, steering dynamics, and pedal inputs to ensure safe and efficient vehicle operation under varying driving conditions.

Automotive companies are increasingly deploying angular position sensors in EV traction motors, battery management systems, and electronic steering systems to improve efficiency and control accuracy. For instance, BYD and Hyundai have expanded sensor integration in their latest EV architectures to enhance torque vectoring and driving stability under high load conditions.

In addition, advancements in sensor miniaturization and digital signal processing are enabling integration into compact vehicle architectures and next generation autonomous systems. Pilot autonomous vehicle programs conducted in 2025 across China and the U.S. have demonstrated improved steering response precision of around 8–12% after integrating high resolution angular position sensing systems into real time vehicle control modules.

Automotive Angular Positions Sensors Market Scope

The market is segmented on the basis of types, category, contact type, output, vehicle type, application, and end-user.

• By Types

On the basis of types, the automotive angular position sensors market is segmented into Linear Type, Rotary Position Sensors, and Other Sensors. The Rotary Position Sensors segment held the largest market revenue share of approximately 58.4% in 2025 driven by its extensive use in steering angle detection, throttle position monitoring, and electric motor control systems. These sensors are widely adopted due to their high accuracy, durability, and ability to operate effectively in harsh automotive environments. Growing integration in electric power steering systems and drivetrain control units is further strengthening segment demand. Automotive OEMs prefer rotary sensors as they provide real time feedback for safety critical applications such as stability control and ADAS functionalities. Increasing electrification of vehicles is further expanding their deployment across next generation automotive platforms.

The Linear Type segment is projected to register the fastest growth at a CAGR of 9.6% from 2026 to 2033, driven by increasing integration in suspension systems, pedal position sensing, and advanced chassis control applications in electric and autonomous vehicles. Rising demand for improved ride comfort and vehicle stability is accelerating adoption of linear sensing technologies. These sensors are also gaining traction in battery management systems for EVs to ensure precise mechanical movement monitoring. Advancements in compact sensor design and improved signal accuracy are further supporting market penetration. Expanding use in intelligent suspension and braking systems is expected to significantly boost long term demand.

• By Category

On the basis of category, the market is segmented into Multi-Axis, Angular, and Linear. The Angular segment accounted for the largest market share of approximately 46.7% in 2025 due to its widespread use in steering systems, drivetrain monitoring, and engine control applications. These sensors are critical for ensuring precise angular measurement in rotating automotive components. Increasing integration in electronic stability programs and torque vectoring systems is further driving demand. Automotive manufacturers rely heavily on angular sensors to enhance vehicle safety and driving precision. Rising production of hybrid and electric vehicles is also strengthening segment growth globally.

The Multi-Axis segment is expected to register the fastest growth at a CAGR of 10.4% from 2026 to 2033, driven by rising demand for high precision motion tracking in autonomous driving systems, robotics integration, and advanced driver assistance systems requiring real time multi directional sensing. These sensors enable simultaneous measurement across multiple planes, improving overall system intelligence. Increasing use in self driving platforms and smart mobility solutions is further boosting adoption. Automotive testing programs are increasingly deploying multi axis sensors for advanced vehicle dynamics analysis. Continuous innovation in sensor fusion technologies is expected to accelerate future growth.

• By Contact Type

On the basis of contact type, the market is segmented into Non-Contact Type and Contact Type. The Non-Contact Type segment dominated the market with a revenue share of approximately 71.2% in 2025 driven by strong adoption in electric vehicles and safety critical automotive systems. These sensors offer higher reliability, longer lifespan, and reduced wear and tear compared to traditional contact based systems. Their ability to function in harsh temperature and vibration conditions makes them ideal for automotive applications. Increasing adoption in EV powertrains and steering systems is further strengthening demand. Automotive OEMs prefer non contact sensors due to their maintenance free operation and higher accuracy levels.

The Contact Type segment is anticipated to grow at a CAGR of 6.8% from 2026 to 2033 due to its continued use in cost sensitive vehicle segments and basic mechanical sensing applications. These sensors are widely used in entry level vehicles where affordability is a key consideration. Despite lower durability compared to non contact types, they remain relevant in conventional automotive systems. Manufacturers continue to optimize contact sensor designs to improve reliability and cost efficiency. Their usage is expected to remain steady in developing automotive markets.

• By Output

On the basis of output, the market is segmented into Digital Output and Analog Output. The Digital Output segment held the largest market share of approximately 62.9% in 2025 driven by increasing integration in modern electronic control units, ADAS systems, and EV platforms requiring high precision signal processing. Digital sensors provide enhanced accuracy, noise immunity, and seamless integration with vehicle control systems. Growing demand for software defined vehicles is further supporting adoption. Automotive OEMs are increasingly shifting toward digital architectures for improved performance. Rising electrification and connectivity trends are reinforcing segment dominance.

The Analog Output segment is expected to grow steadily at a CAGR of 7.1% from 2026 to 2033 supported by its use in legacy systems and cost effective automotive applications. These sensors remain widely used in older vehicle platforms and industrial automotive applications. Their simple design and low cost make them suitable for basic sensing functions. However, gradual transition toward digital systems may limit long term expansion. Despite this, demand will persist in aftermarket and budget vehicle segments.

• By Vehicle Type

On the basis of vehicle type, the market is segmented into High End, Mid End, Low End, and Electric. The Electric segment dominated the market with a share of approximately 38.5% in 2025 driven by rapid global EV adoption and increasing demand for advanced sensing systems in electric drivetrains, battery management, and regenerative braking systems. EV manufacturers heavily rely on angular sensors for precise motor control and energy optimization. Government incentives supporting electric mobility are further accelerating adoption. Increasing EV production in China, Europe, and North America is strengthening demand. Integration of smart sensing technologies is becoming standard in modern EV architectures.

The High End segment is projected to register the fastest growth at a CAGR of 9.9% from 2026 to 2033 due to increasing integration of advanced driver assistance systems and autonomous driving technologies in premium vehicles. Luxury automakers are incorporating high precision sensors for enhanced safety and performance features. Demand for intelligent mobility solutions and connected vehicle systems is further boosting adoption. High end vehicles are early adopters of advanced sensor technologies before mass market rollout. Continuous innovation in autonomous driving platforms is expected to accelerate segment growth.

• By Application

On the basis of application, the market is segmented into Machine Tools, Robotics, Motion Systems, Material Handling, Test Equipment, and Others. The Motion Systems segment held the largest market share of approximately 34.6% in 2025 driven by its widespread use in automotive steering, drivetrain control, and industrial automation systems. These systems require precise angular measurement for smooth and efficient operation. Increasing adoption in EV drivetrains and smart manufacturing systems is strengthening demand. Motion control applications benefit significantly from high accuracy sensing technologies. Rising automation trends across industries are further supporting segment expansion.

The Robotics segment is expected to grow at the fastest CAGR of 10.7% from 2026 to 2033 due to rising adoption of automated manufacturing, warehouse robotics, and precision motion control systems across industries. Angular position sensors play a critical role in enabling precise robotic movement and coordination. Increasing deployment of industrial robots in automotive production lines is driving demand. Growth of e commerce logistics and warehouse automation is further accelerating adoption. Continuous advancements in AI enabled robotics are expected to support long term market growth.

• By End-User

On the basis of end-user, the market is segmented into Manufacturing, Automotive, Aerospace, Packaging, Healthcare, Electronics, and Others. The Automotive segment dominated the market with a revenue share of approximately 42.8% in 2025 driven by strong adoption of angular position sensors in electric vehicles, ADAS systems, and powertrain control applications. Automotive manufacturers rely heavily on these sensors for safety critical and performance enhancing functions. Increasing vehicle electrification is further boosting demand across OEM platforms. Rising integration in autonomous and connected vehicles is strengthening market dominance. Continuous innovation in automotive electronics is supporting long term growth.

The Aerospace segment is expected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033 due to increasing use in flight control systems, navigation systems, and high precision motion monitoring in defense and commercial aviation platforms. Aerospace applications require extremely accurate and reliable sensing solutions. Growing investments in unmanned aerial vehicles and defense modernization programs are further supporting adoption. Increasing focus on lightweight and high performance sensor systems is driving technological advancement. Expanding commercial aviation fleet size globally is expected to further accelerate demand.

Automotive Angular Positions Sensors Market Regional Analysis

North America Automotive Angular Position Sensors Market Insight

North America dominated the automotive angular position sensors market with the largest revenue share of 39.8% in 2025, supported by strong adoption of electric vehicles, advanced driver assistance systems, and high integration of electronic control units across modern vehicles. The region benefits from a well-established automotive manufacturing base, strong presence of leading OEMs, and rapid adoption of sensor-based safety technologies. Consumers and manufacturers in North America increasingly prioritize vehicle safety, precision control, and performance efficiency, driving widespread deployment of angular position sensors in steering systems, drivetrains, and powertrain applications.

U.S. Automotive Angular Position Sensors Market Insight

The U.S. automotive angular position sensors market captured the largest revenue share in 2025 within North America, fueled by rapid electrification of vehicles and strong demand for advanced mobility technologies. Automotive manufacturers in the country are increasingly integrating high-precision angular sensors in EV powertrains, ADAS platforms, and autonomous driving systems to enhance vehicle responsiveness and safety. The growing adoption of connected vehicles and software-defined automotive architectures is further accelerating sensor penetration. In addition, increasing investments by companies such as Tesla and General Motors in EV innovation are strengthening the demand for advanced sensing technologies across next-generation vehicle platforms.

Europe Automotive Angular Position Sensors Market Insight

The Europe automotive angular position sensors market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent automotive safety regulations, rapid EV adoption, and strong emphasis on emission reduction. European automakers are increasingly integrating advanced sensor systems to support electrification and autonomous driving capabilities. The region’s focus on vehicle safety standards such as Euro NCAP is encouraging widespread adoption of high-precision sensing technologies. Growth is also supported by increasing production of premium vehicles and rising demand for intelligent mobility solutions across passenger and commercial vehicle segments.

U.K. Automotive Angular Position Sensors Market Insight

The U.K. automotive angular position sensors market is expected to witness the fastest growth rate from 2026 to 2033, driven by growing demand for electric vehicles, connected mobility solutions, and advanced driver assistance systems. Rising consumer preference for safer and more efficient vehicles is encouraging automakers to integrate high-accuracy angular sensing systems. The country’s strong focus on automotive innovation and increasing investments in EV infrastructure are further supporting market expansion. In addition, growing adoption of smart mobility platforms and autonomous vehicle testing programs is strengthening sensor deployment across the automotive ecosystem.

Germany Automotive Angular Position Sensors Market Insight

The Germany automotive angular position sensors market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country’s strong automotive manufacturing base and leadership in automotive engineering innovation. German OEMs are heavily investing in electrification, autonomous driving technologies, and precision control systems, increasing demand for angular position sensors. Integration of advanced sensing technologies in luxury and high-performance vehicles is a key growth driver. In addition, Germany’s focus on Industry 4.0 and smart manufacturing is further enhancing adoption across automotive and industrial applications.

Asia-Pacific Automotive Angular Position Sensors Market Insight

The Asia-Pacific automotive angular position sensors market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, increasing vehicle production, and strong growth in electric vehicle adoption across China, Japan, and India. The region is emerging as a global hub for automotive manufacturing, leading to large-scale deployment of sensor technologies in both passenger and commercial vehicles. Government initiatives promoting electric mobility and smart transportation systems are further accelerating demand. In addition, the availability of cost-effective manufacturing and expanding domestic OEM presence are strengthening market penetration.

Japan Automotive Angular Position Sensors Market Insight

The Japan automotive angular position sensors market is expected to witness strong growth from 2026 to 2033 due to the country’s advanced automotive technology ecosystem and high focus on precision engineering. Japanese automakers are increasingly integrating angular sensors in hybrid and electric vehicles to improve efficiency, safety, and control accuracy. The growing adoption of autonomous driving technologies and robotics-based vehicle systems is further driving demand. In addition, Japan’s aging population is increasing the need for safer and easier-to-operate vehicle systems, supporting adoption of advanced sensor technologies across automotive platforms.

China Automotive Angular Position Sensors Market Insight

The China automotive angular position sensors market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid expansion of the electric vehicle industry, strong government support for smart mobility, and large-scale automotive production. China is one of the leading global EV markets, driving significant demand for high-precision sensing technologies in powertrains, steering systems, and battery management applications. The presence of strong domestic sensor manufacturers and increasing investments in autonomous vehicle development are further strengthening market growth. In addition, smart city initiatives and connected vehicle deployment are accelerating adoption across the automotive ecosystem.

Automotive Angular Positions Sensors Market Share

The Automotive Angular Positions Sensors industry is primarily led by well-established companies, including:

• Honeywell International Inc. (U.S.)

• SICK AG (Germany)

• TE Connectivity (U.S.)

• MTS Systems Corporation (U.S.)

• ams AG (Austria)

• Vishay Intertechnology (U.S.)

• Infineon Technologies AG (Germany)

• STMicroelectronics (Switzerland)

• Bourns, Inc. (U.S.)

• Allegro MicroSystems, LLC (U.S.)

• Renishaw plc. (U.K.)

• HEIDENHAIN (Germany)

• Hans Turck GmbH & Co. KG (Germany)

• Novotechnik U.S. Inc. (U.S.)

• PIHER SENSORS AND CONTROLS SA. (Spain)

• Hamamatsu Photonics K.K (Japan)

• Broadcom (U.S.)

• General Electric (U.S.)

• Methode Electronics (U.S.)

• IFM electronic gmbh (Germany)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.