Global Automotive Backlight Moldings Market

Market Size in USD Billion

USD

6.12 Billion

USD

8.77 Billion

2025

2033

USD

6.12 Billion

USD

8.77 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.12 Billion | |

| USD 8.77 Billion | |

| % | |

|

What is the Global Automotive Backlight Moldings Market Size and Growth Rate?

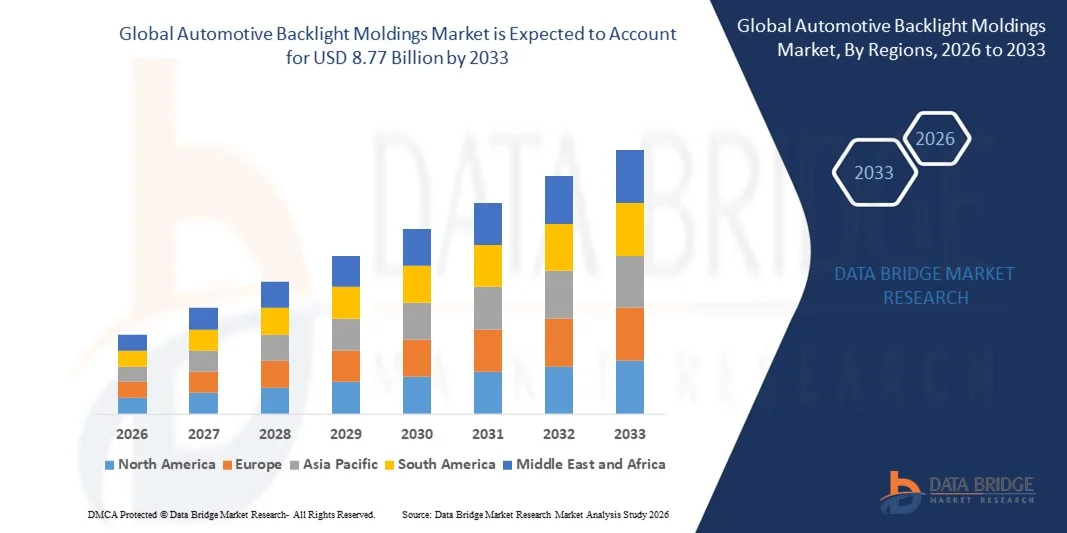

- The global automotive backlight moldings market size was valued at USD 6.12 billion in 2025 and is expected to reach USD 8.77 billion by 2033, at a CAGR of 4.60% during the forecast period

- The increase in the production rate of automobiles across the globe acts as one of the major factors driving the growth of the automotive backlight moldings market

- The rise in the demand for electric automotive vehicle designs coupled with frequently modification, and increase in demand for customized products forcing automotive backlight moldings manufactures to offer competitive pricing along with flexibility in design/ shape in order to cater each type of customer’s requirements accelerate the market growth

What are the Major Takeaways of Automotive Backlight Moldings Market?

- The rise in the use of plastic resins and additives in injection molding process for its flexibility for automotive backlight moldings designers, and use of the equipment for preventing backlight from corrosions and other effects due to harsh weather conditions further influence the market

- In addition, expansion of automotive sector, increase in the vehicle sales and demand aesthetically pleasing vehicles positively affect the automotive backlight moldings market. Furthermore, rise in demand for chromium material for automotive backlight moldings owning to its flexibility, strength, and anti-corrosive, among others, extend profitable opportunities

- North America dominated the Automotive Backlight Moldings market with a 42.05% revenue share in 2025, driven by strong growth in semiconductor design, embedded system development, electronics manufacturing, and rapid expansion of R&D activities across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 10.69% from 2026 to 2033, driven by rapid semiconductor expansion, strong electronics manufacturing ecosystems, 5G deployment, and rising adoption of embedded systems across China, Japan, India, South Korea, and Southeast Asia

- The Plastic segment dominated the market with a 41.8% share in 2025, driven by its lightweight properties, cost efficiency, corrosion resistance, and design flexibility

Report Scope and Automotive Backlight Moldings Market Segmentation

|

Attributes |

Automotive Backlight Moldings Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Automotive Backlight Moldings Market?

Increasing Shift Toward Lightweight, Aerodynamic, and LED-Integrated Backlight Molding Designs

- The automotive backlight moldings market is witnessing strong adoption of lightweight, high-durability materials such as advanced polymers, ABS blends, and chrome-plated composites to enhance vehicle aesthetics and fuel efficiency

- Manufacturers are increasingly integrating LED lighting elements, aerodynamic contours, and seamless body designs into rear windshield molding systems to support modern vehicle styling trends

- Growing demand for electric vehicles (EVs), premium SUVs, and connected vehicles is driving innovation in sleek, corrosion-resistant, and weatherproof backlight molding solutions

- For instance, leading automotive component manufacturers are developing precision injection-molded backlight trims with enhanced UV resistance, scratch protection, and integrated lighting compatibility

- Rising focus on vehicle differentiation, brand identity, and improved rear visibility aesthetics is accelerating product innovation across global OEMs

- As vehicle designs become more aerodynamic and technologically advanced, automotive backlight moldings will remain essential for structural reinforcement, visual appeal, and integrated lighting functionality

What are the Key Drivers of Automotive Backlight Moldings Market?

- Rising global vehicle production, particularly in electric vehicles, SUVs, and luxury cars, is increasing demand for high-quality exterior trim components

- For instance, in 2025, major automotive OEMs across China, Japan, Germany, and the U.S. expanded EV and hybrid vehicle production, boosting demand for lightweight and integrated rear molding systems

- Growing consumer preference for premium styling, chrome accents, and seamless glass integration is strengthening adoption in mid-range and high-end vehicle segments

- Advancements in plastic injection molding, surface coating technologies, and automated manufacturing processes have improved durability, finish quality, and cost efficiency

- Increasing emphasis on fuel efficiency and emission reduction is encouraging automakers to adopt lightweight molding materials

- Supported by expanding automotive manufacturing hubs and rising EV penetration, the Automotive Backlight Moldings market is expected to witness strong long-term growth

Which Factor is Challenging the Growth of the Automotive Backlight Moldings Market?

- Volatility in raw material prices, particularly engineering plastics and specialty coatings, increases production costs and impacts profit margins

- For instance, during 2024–2025, fluctuations in petrochemical prices and supply chain disruptions affected plastic component manufacturing across major automotive markets

- Stringent automotive safety and durability standards require continuous product testing, certification, and compliance investments

- Intense competition among global and regional mold manufacturers creates pricing pressure and limits differentiation

- Increasing shift toward frameless glass designs in certain EV models may reduce reliance on traditional molding structures

- To address these challenges, manufacturers are focusing on sustainable materials, cost-optimized tooling processes, enhanced design flexibility, and strategic partnerships with OEMs to strengthen global adoption

How is the Automotive Backlight Moldings Market Segmented?

The market is segmented on the basis of material, vehicle type, and sales channel.

- By Material

On the basis of material, the automotive backlight moldings market is segmented into Chromium, Steel, Aluminum, Plastic, and Other. The Plastic segment dominated the market with a 41.8% share in 2025, driven by its lightweight properties, cost efficiency, corrosion resistance, and design flexibility. Advanced polymers such as ABS and polypropylene are widely used due to their durability, ease of molding, and compatibility with chrome plating and coating technologies. Automakers prefer plastic moldings to reduce overall vehicle weight and improve fuel efficiency while maintaining aesthetic appeal.

The Aluminum segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by rising demand for premium vehicles and electric vehicles (EVs). Aluminum offers high strength-to-weight ratio, improved durability, and enhanced recyclability, making it suitable for high-end automotive applications focused on sustainability and performance.

- By Vehicle Type

On the basis of vehicle type, the market is segmented into Passenger Car, Compact, Mid-Size, SUV, Luxury, Commercial Vehicle, Light Commercial Vehicle, and Heavy Commercial Vehicle. The Passenger Car segment dominated the market with a 52.6% share in 2025, supported by high global production volumes and rising consumer preference for stylish exterior components. Increasing demand for compact and mid-size vehicles in emerging economies significantly contributes to molding adoption.

The SUV segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising global popularity of crossover and sport utility vehicles. SUV models often incorporate premium chrome accents, larger rear glass panels, and integrated lighting features, increasing the requirement for durable and aesthetically refined backlight molding systems. Growth in EV-based SUVs further accelerates demand for lightweight and aerodynamic molding materials.

- By Sales Channel

On the basis of sales channel, the automotive backlight moldings market is segmented into Original Equipment Manufacturer (OEM) and Aftermarket. The OEM segment dominated the market with a 73.4% share in 2025, as most backlight moldings are installed during vehicle assembly. Strong partnerships between automotive OEMs and component manufacturers ensure design precision, quality control, and integration with rear windshield and lighting systems. Increasing vehicle production and model launches further strengthen OEM demand.

The Aftermarket segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising vehicle parc, increasing accident repairs, customization trends, and replacement demand. Growing consumer interest in aesthetic upgrades and chrome-finished trims is further supporting aftermarket sales, particularly in developing automotive markets.

Which Region Holds the Largest Share of the Automotive Backlight Moldings Market?

- Asia-Pacific dominated the automotive backlight moldings market with a 44.12% revenue share in 2025, driven by high vehicle production volumes, strong automotive manufacturing ecosystems, and rapid expansion of electric vehicle (EV) production across China, Japan, India, and South Korea. The region’s cost-efficient manufacturing capabilities and large OEM presence significantly boost demand for lightweight, durable, and aesthetically advanced backlight molding components

- Leading automotive component manufacturers in Asia-Pacific are investing in advanced plastic injection molding, chrome plating technologies, and automated production lines to enhance product quality and scalability. Growing adoption of SUVs, premium vehicles, and EVs further strengthens demand

- Strong supply chain networks, expanding domestic vehicle demand, and government support for automotive manufacturing reinforce regional market leadership

China Automotive Backlight Moldings Market Insight

China is the largest contributor in Asia-Pacific, supported by the world’s largest automotive production base and rapid EV expansion. Rising demand for stylish rear designs, chrome-finished trims, and integrated LED elements drives adoption of advanced backlight moldings. Strong domestic OEM presence, large-scale exports, and continuous investments in smart manufacturing further accelerate market growth.

Japan Automotive Backlight Moldings Market Insight

Japan shows steady growth due to its advanced automotive engineering capabilities and strong focus on precision components. Increasing production of hybrid vehicles, compact cars, and premium SUVs supports consistent demand. Emphasis on lightweight materials, aerodynamic design, and long-term durability strengthens molding innovation.

India Automotive Backlight Moldings Market Insight

India is emerging as a high-growth market driven by expanding passenger vehicle production, rising SUV demand, and increasing foreign investments in automotive manufacturing. Government initiatives supporting local production and EV adoption further boost demand for cost-effective and lightweight molding components.

South Korea Automotive Backlight Moldings Market Insight

South Korea contributes significantly due to strong global automotive exports and advanced vehicle styling trends. Rapid EV adoption and integration of modern exterior trims drive demand for high-quality, weather-resistant backlight molding systems.

North America Automotive Backlight Moldings Market

North America is projected to register the fastest CAGR of 8.89% from 2026 to 2033, driven by rising EV adoption, growing SUV sales, and increasing consumer preference for premium exterior styling. Expansion of domestic EV manufacturing plants and technological upgrades in automotive assembly facilities are strengthening demand for advanced molding solutions.

U.S. Automotive Backlight Moldings Market Insight

The U.S. is the largest contributor within North America, supported by strong SUV and EV demand, premium vehicle sales, and continuous innovation in exterior automotive design. Increasing focus on lightweight materials and aerodynamic efficiency accelerates product adoption.

Canada Automotive Backlight Moldings Market Insight

Canada contributes steadily due to automotive component manufacturing expansion and growing integration within North American supply chains. Rising investments in EV assembly and sustainable manufacturing practices further support market growth.

Which are the Top Companies in Automotive Backlight Moldings Market?

The automotive backlight moldings industry is primarily led by well-established companies, including:

- NTF GROUP (Poland)

- Sino Mould (China)

- Motherson. (India)

- The Platinum Tool Group (U.S.)

- Fabrïk Molded Plastics (U.S.)

- GREEN VITALITY INDUSTRY CO., LTD. (Taiwan)

- PIM Industries (U.S.)

- Taizhou Toolsong Mould Co., Ltd. (China)

- Dongguan Humen Haofeng Plastic Mould Factory (China)

- Yingdai International Trade (Hebei) Co., Ltd. (China)

- ABERY (China)

- RÖHM (Germany)

- WESEM (Poland)

- Coast to Coast International (U.S.)

- Sino Mould (China)

- Motherson (India)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.