Global Automotive Ball Joints Market

Market Size in USD Million

USD

5.29 Million

USD

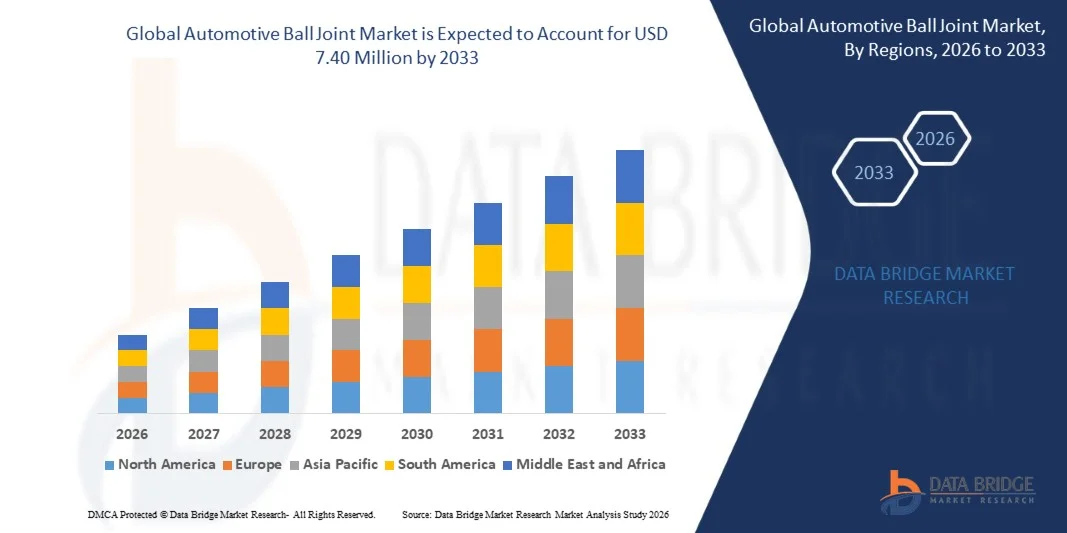

7.40 Million

2025

2033

USD

5.29 Million

USD

7.40 Million

2025

2033

| 2026 - 2033 | |

| USD 5.29 Million | |

| USD 7.40 Million | |

| % | |

|

What is the Global Automotive Ball Joint Market Size and Growth Rate?

- The global automotive ball joint market size was valued at USD 5.29 million in 2025 and is expected to reach USD 7.40 million by 2033, at a CAGR of4.27% during the forecast period

- Increasing adoption of passenger cars and commercial vehicles, rising preference for durable and lightweight materials such as aluminum and composites, growing focus on vehicle safety and suspension performance, expanding automotive production in emerging markets, and increasing replacement demand through aftermarket channels are some of the key factors driving the growth of the automotive ball joint market

What are the Major Takeaways of Automotive Ball Joint Market?

- Rising automotive production and modernization of vehicle suspension systems in developing economies, along with increasing aftermarket and e-commerce sales channels, are creating significant growth opportunities for the Automotive Ball Joint market

- Challenges such as high manufacturing costs for advanced material joints, stringent safety regulations, and design complexity in multi-vehicle platforms may restrain market growth during the forecast period

- Asia-Pacific dominated the automotive ball joint market with a 37.19% revenue share in 2025, driven by large-scale automotive manufacturing, extensive component sourcing, and rapid adoption of advanced suspension and chassis systems across China, Japan, India, South Korea, and Southeast Asia

- North America is projected to register the fastest CAGR of 11.36% from 2026 to 2033, driven by rising adoption of intelligent suspension systems, EVs, and high-precision chassis components in the U.S. and Canada

- The Lower Ball Joint segment dominated the market with a 42.5% share in 2025, owing to its widespread use in suspension systems, steering assemblies, and high-volume passenger cars

Report Scope and Automotive Ball Joint Market Segmentation

|

Attributes |

Automotive Ball Joint Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Automotive Ball Joint Market?

“Rising Adoption of Intelligent, High-Precision, and Durable Ball Joints”

- The automotive ball joint market is witnessing strong adoption of advanced ball joints integrated with sensors and high-precision components, designed to support modern suspension systems, steering modules, and automotive safety mechanisms

- Manufacturers are introducing multi-material, corrosion-resistant, and high-durability ball joints that offer enhanced load-bearing capacity, low friction, and longer service life

- Growing demand for lightweight, compact, and precision-engineered suspension components is driving adoption across passenger cars, commercial vehicles, and off-road vehicles

- For instance, companies such as ZF Group, Tenneco, KYB, SH Auto Parts, and Delphi have expanded their portfolios with smart and OE-quality ball joints optimized for sensor integration and chassis performance monitoring

- Increasing need for intelligent suspension systems, real-time wheel movement tracking, and enhanced vehicle handling is accelerating the shift toward sensor-integrated and high-performance ball joints

- As automotive designs become more complex and safety-focused, Automotive Ball Joints remain vital for ride comfort, handling precision, and vehicle longevity

What are the Key Drivers of Automotive Ball Joint Market?

- Rising demand for durable, high-performance, and sensor-enabled ball joints to enhance vehicle safety, ride stability, and chassis responsiveness

- For instance, in 2025, leading companies such as SH Auto Parts, ZF Group, and Tenneco introduced automated and smart factory-manufactured ball joints with improved material composition and precision engineering

- Growing production of EVs, luxury vehicles, off-road vehicles, and commercial trucks is boosting demand for advanced ball joints across North America, Europe, and Asia-Pacific

- Advancements in materials technology, such as high-strength steel, aluminum alloys, and composite materials, have enhanced performance, durability, and load-handling capacity

- Rising adoption of active suspension systems, ADAS integration, and connected vehicle technologies is creating demand for intelligent and sensor-integrated ball joints

- Supported by continuous investments in automotive R&D, smart manufacturing, and chassis innovation, the Automotive Ball Joint market is expected to witness strong long-term growth

Which Factor is Challenging the Growth of the Automotive Ball Joint Market?

- High costs associated with premium, sensor-integrated, and multi-material ball joints limit adoption among small OEMs and aftermarket suppliers

- For instance, during 2024–2025, fluctuations in raw material prices, specialized component shortages, and longer supply lead times increased manufacturing costs for global vendors

- Complexity in designing and integrating intelligent ball joints with vehicle electronic systems increases the need for advanced engineering and testing

- Limited awareness in emerging markets regarding performance benefits, durability advantages, and intelligent monitoring features slows adoption

- Competition from standard, low-cost ball joints and alternative suspension solutions creates pricing pressure and reduces differentiation for advanced products

- To address these challenges, companies are focusing on cost-efficient designs, enhanced material selection, smart factory production, and integrated sensor technology to increase global adoption of automotive ball joints

How is the Automotive Ball Joint Market Segmented?

The market is segmented on the basis of type, material, application, and sales channel.

• By Type

On the basis of type, the automotive ball joint market is segmented into Lower Ball Joint, Upper Ball Joint, Female Ball Joint, and Male Ball Joint. The Lower Ball Joint segment dominated the market with a 42.5% share in 2025, owing to its widespread use in suspension systems, steering assemblies, and high-volume passenger cars. Its robust load-bearing capacity, compatibility with multiple vehicle types, and ease of integration drive strong adoption across OEMs and aftermarket suppliers.

The Female Ball Joint segment is expected to grow at the fastest CAGR from 2026 to 2033, fueled by increasing adoption in advanced suspension systems, EVs, and off-road vehicles where precision, compact design, and sensor integration are critical. Rising development of intelligent chassis components is further accelerating demand for specialized female ball joints.

• By Material

On the basis of material, the market is segmented into Steel, Aluminum, Plastic, and Composite. The Steel segment dominated the market with a 48.3% share in 2025, due to its durability, high load-bearing capacity, and cost-effectiveness for conventional vehicles. Steel ball joints are extensively used across passenger cars, commercial vehicles, and heavy-duty trucks for both OEM and aftermarket applications.

The Composite segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by lightweight requirements in electric vehicles, off-road vehicles, and high-performance passenger cars. Composite materials enhance fuel efficiency, reduce unsprung mass, and allow integration with advanced sensors, making them preferred for next-generation suspension systems.

• By Application

On the basis of application, the automotive ball joint market is segmented into Passenger Cars, Commercial Vehicles, Heavy-Duty Trucks, and Off-Road Vehicles. The Passenger Cars segment dominated the market with a 45.6% share in 2025, supported by high vehicle production, rising demand for comfort and handling, and widespread aftermarket replacements.

The Off-Road Vehicles segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by increasing off-road vehicle sales, demand for rugged suspension systems, and adoption of intelligent ball joints in harsh terrains. The need for high-performance, durable components in extreme operating conditions is driving accelerated adoption of specialized ball joints for off-road applications.

• By Sales Channel

On the basis of sales channel, the market is segmented into OEM, Aftermarket, and E-Commerce. The OEM segment dominated the market with a 50.2% share in 2025, attributed to long-term supply contracts, quality assurance, and integration of advanced ball joints during vehicle assembly.

The E-Commerce segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing online penetration, convenient procurement for replacement parts, and growing awareness of digital platforms among vehicle owners and small-scale garages. Rising e-commerce adoption is enabling wider access to high-quality ball joints for both passenger and commercial vehicles.

Which Region Holds the Largest Share of the Automotive Ball Joint Market?

- Asia-Pacific dominated the automotive ball joint market with a 37.19% revenue share in 2025, driven by large-scale automotive manufacturing, extensive component sourcing, and rapid adoption of advanced suspension and chassis systems across China, Japan, India, South Korea, and Southeast Asia. Rising demand for passenger vehicles, commercial trucks, and off-road vehicles with intelligent suspension systems continues to fuel market growth. High-volume production of steel, aluminum, and composite ball joints further strengthen regional supply chains and market penetration

- Leading manufacturers in Asia-Pacific are investing in automated production, precision machining, and sensor-integrated ball joints, enhancing quality, durability, and innovation capabilities. Continuous development in EVs, ADAS systems, and smart mobility solutions drives long-term market expansion

- Strong industrial infrastructure, skilled workforce, and supportive government policies in automotive R&D reinforce the region’s leadership in the global market

China Automotive Ball Joint Market Insight

China is the largest contributor to Asia-Pacific, supported by massive automotive production, high demand for OE and aftermarket components, and strong government backing for EV and smart vehicle programs. The growth of electric and autonomous vehicles is accelerating adoption of advanced ball joints with higher precision, durability, and sensor integration. Local manufacturing capabilities and cost competitiveness further expand domestic and export market adoption.

Japan Automotive Ball Joint Market Insight

Japan demonstrates steady growth, supported by advanced manufacturing capabilities, high-quality engineering standards, and continuous modernization of automotive and commercial vehicle platforms. Adoption of lightweight and sensor-enabled ball joints in passenger cars and commercial vehicles enhances efficiency, safety, and performance, sustaining long-term market growth.

India Automotive Ball Joint Market Insight

India is emerging as a significant growth hub, driven by increasing vehicle production, automotive electronics adoption, and expanding suspension system innovations. Growing interest in EVs, off-road vehicles, and advanced chassis components fuels adoption of high-performance ball joints in both OEM and aftermarket segments. Rising investments in automotive R&D and digital manufacturing infrastructure accelerate market penetration.

South Korea Automotive Ball Joint Market Insight

South Korea contributes significantly due to the development of high-performance passenger vehicles, EVs, and smart mobility solutions. Advanced manufacturing capabilities, rising demand for lightweight materials, and integration of sensor-enabled ball joints are driving regional market growth. The presence of strong automotive OEMs and component suppliers supports continued expansion.

North America Automotive Ball Joint Market

North America is projected to register the fastest CAGR of 11.36% from 2026 to 2033, driven by rising adoption of intelligent suspension systems, EVs, and high-precision chassis components in the U.S. and Canada. Increasing demand for aftermarket upgrades, technological innovations in ball joint designs, and smart vehicle integration are boosting market growth. Expansion of automotive R&D, automated manufacturing, and advanced quality testing further accelerates adoption across engineering and production facilities.

Which are the Top Companies in Automotive Ball Joint Market?

The automotive ball joint industry is primarily led by well-established companies, including:

- ZF Aftermarket (TRW) (Germany)

- Tenneco (U.S.)

- Meyle AG (Germany)

- Delphi Technologies (U.S.)

- Federal-Mogul Motorparts (U.S.)

- Sidem (Belgium)

- Mevotech (Canada)

- Rane Limited (India)

- Ocap Chassis Parts S.r.l. (Italy)

- NTN Bearing Corporation (Japan)

- THK Co., Ltd. (Japan)

- CTR Manufacturing Corporation (South Korea)

- LEMFORDER (Germany)

- DANA Incorporated (U.S.)

- Denckermann (Poland)

- Fujian Fuerde Auto Parts Co.,Ltd (China)

- J.K. Fenner Ltd. (India)

- BorgWarner (U.S.)

- FEBEST GmbH (Germany)

- Masuma Auto Spare Parts Manufacture Co. (China)

What are the Recent Developments in Global Automotive Ball Joint Market?

- In October 2025, SH Auto Parts announced the launch of its smart factory in Taiwan, producing OEM-grade ball joints through fully automated manufacturing and sustainable processes, reinforcing its commitment to advanced production and environmental responsibility

- In July 2025, Cadillac’s ultra-luxury Celestiq integrated advanced sensors into its ball joints to monitor wheel movement and chassis behavior, reflecting the rising trend of intelligent, high-precision suspension components in the Automotive Ball Joint market

- In July 2025, ZF Group transferred full ownership of its Indian steering and suspension joint venture to Somic Ishikawa, enhancing the company’s focus on ball joints and chassis components in India, a rapidly expanding automotive manufacturing hub

- In July 2024, KYB Europe expanded its product lineup with a new range of steering components, including ball joints designed to meet OE specifications and subjected to rigorous quality testing, strengthening its position in the European suspension aftermarket

- In June 2024, DRIV (Tenneco) announced a major expansion of its Monroe Steering and Suspension portfolio, adding 750 new part numbers, including OE-quality ball joints with induction-hardened studs and advanced anti-corrosion coatings, boosting product durability and performance

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.