Global Automotive Communication Protocol Market

Market Size in USD Billion

USD

7.45 Billion

USD

10.07 Billion

2025

2033

USD

7.45 Billion

USD

10.07 Billion

2025

2033

| 2026 - 2033 | |

| USD 7.45 Billion | |

| USD 10.07 Billion | |

| % | |

|

Automotive Communication Protocol Market Overview

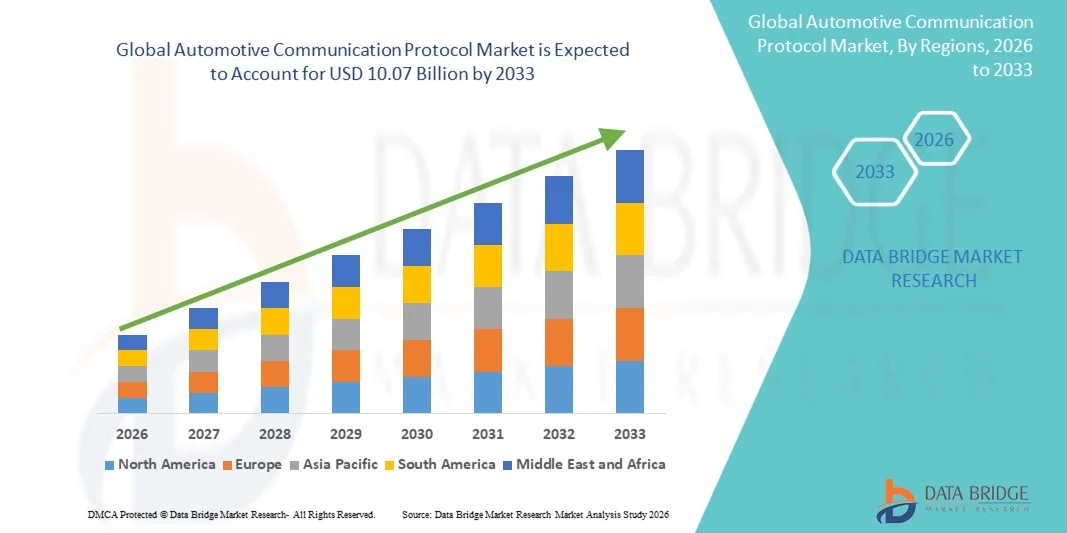

The global automotive communication protocol market was valued at USD 7.45 billion in 2025 and is projected to reach USD 10.07 billion by 2033, growing at a CAGR of 3.85% from 2026 to 2033. The market is witnessing steady growth driven by increasing vehicle electrification, rising adoption of advanced driver assistance systems (ADAS), and growing integration of in-vehicle networking technologies across modern automobiles.

The increasing demand for connected and software-defined vehicles is significantly accelerating the adoption of high-speed and reliable communication protocols such as CAN, LIN, FlexRay, and Ethernet. Automakers are increasingly focusing on enhancing real-time data exchange between electronic control units (ECUs) to improve vehicle safety, performance, and diagnostic capabilities. In addition, the expansion of electric vehicles and autonomous driving technologies is further supporting the need for robust, low-latency communication architectures across the automotive ecosystem.

Key Market Trends & Insights

- The Hardware segment held the largest market revenue share of approximately 52.6% in 2025 driven by the extensive deployment of electronic control units, wiring harnesses, gateways, and communication interfaces across modern vehicles. Increasing integration of ADAS, infotainment systems, and electrified powertrains is further strengthening hardware demand due to rising ECU complexity in passenger and commercial vehicles.

- The Software segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by increasing adoption of software defined vehicles, over the air updates, and cybersecurity solutions for in vehicle networks. Growing reliance on middleware, protocol management software, and diagnostic tools for real time communication optimization is accelerating segment expansion.

- The CAN segment held the largest market revenue share of approximately 41.3% in 2025 driven by its widespread adoption in powertrain systems, body electronics, and safety critical applications due to its reliability, cost efficiency, and proven performance in automotive environments.

- The Automotive Ethernet segment, while not part of traditional legacy grouping but increasingly adopted in modern architectures, is projected to register the fastest growth at a CAGR of 12.1% from 2026 to 2033, driven by rising demand for high bandwidth communication in ADAS, autonomous driving systems, and infotainment applications requiring real time data transmission.

- The Passenger Cars segment held the largest market revenue share of approximately 68.5% in 2025 driven by high production volumes, increasing integration of advanced electronics, and rapid adoption of connected vehicle technologies across global automotive markets.

- The Commercial Vehicles segment is projected to register the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by rising demand for fleet connectivity, telematics systems, and regulatory requirements for vehicle safety and emission monitoring. Integration of advanced communication protocols in logistics and transportation fleets is further supporting segment expansion.

- North America dominated the automotive communication protocol market with the largest revenue share of 39.6% in 2025, supported by strong penetration of connected vehicles, rapid adoption of ADAS technologies, and increasing integration of high speed in vehicle networking systems.

- Asia-Pacific automotive communication protocol market is expected to witness the fastest growth rate from 2026 to 2033, supported by rising vehicle production, rapid urbanization, and increasing adoption of electric vehicles in countries such as China, Japan, South Korea, and India.

Market Size & Forecast

- Global Market Value (2025): USD 7.45 Billion

- Expected Market Value (2033): USD 10.07 Billion

- Forecast CAGR (2026–2033): 3.85%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Automotive Communication Protocol Market Segmentation

|

Attributes |

Automotive Communication Protocol Key Market Insights |

|

Segments Covered |

· By Component: Hardware, Software, and Services · By Bus Type: CAN (Controller Area Network), LIN (Local Interconnect Network), MOST (Media Oriented Systems Transport), and FlexRay · By Vehicle Type: Passenger Cars, Commercial Vehicles (Light and Heavy Duty), Two Wheelers, Off-Highway Vehicles |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Robert Bosch GmbH (Germany) |

|

Market Opportunities |

• Expansion Of Electric And Hybrid Vehicle Architecture |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Global Automotive Communication Protocol Market Trends

Trend: Growth In Vehicle Electrification And High Speed In Vehicle Networking Architectures

Increasing adoption of electric vehicles, hybrid powertrains, and software defined vehicle platforms is driving demand for robust, low latency automotive communication protocols across vehicle systems. Traditional analog and basic digital signaling architectures are being replaced by high speed networks such as CAN FD, Automotive Ethernet, and FlexRay to support real time data exchange between multiple electronic control units.

In modern electric and autonomous vehicle platforms, manufacturers are integrating advanced communication protocols to manage battery management systems, ADAS sensors, infotainment units, and powertrain control modules, for instance Automotive Ethernet enabling data speeds up to 1 Gbps to support high resolution camera and radar data processing in real time. In industrial testing environments, OEMs are using upgraded CAN FD networks to improve bandwidth efficiency by nearly 5–8 times compared to classical CAN systems, enabling smoother vehicle diagnostics and predictive maintenance operations.

The rapid expansion of connected mobility, vehicle to everything (V2X) communication, and over the air software updates is also increasing demand for secure and scalable in vehicle networking systems capable of handling large data loads with minimal latency. In addition, autonomous driving development programs by major automotive manufacturers such as Tesla, BMW, and Toyota continue to validate next generation communication architectures, with real world testing showing improved sensor synchronization accuracy of nearly 20–30% in advanced multi domain controller setups under high computational loads.

Global Automotive Communication Protocol Market Dynamics

Key Market Driver: Rising Demand For Advanced Driver Assistance Systems And Connected Vehicles

The automotive industry is experiencing strong pressure to improve vehicle safety, automation, and connectivity, leading to widespread integration of ADAS technologies and connected car platforms. These systems require continuous high speed communication between sensors, cameras, radar units, and electronic control units, significantly boosting demand for advanced communication protocols.

Automotive manufacturers are increasingly deploying CAN FD and Automotive Ethernet networks to support features such as lane keeping assist, adaptive cruise control, and collision avoidance systems. For instance, modern premium vehicles integrate more than 70–100 ECUs, all requiring synchronized communication for real time decision making and safety critical operations.

Similarly, global regulatory frameworks such as Euro NCAP safety standards and U.S. NHTSA guidelines are pushing automakers to enhance vehicle intelligence and diagnostic capabilities through improved in vehicle networking. Industry deployment studies indicate that ADAS enabled vehicles using high speed Ethernet based architectures demonstrate data transmission latency reductions of up to 40% compared to traditional multiplex wiring systems, improving system response time and driving safety performance.

Key Restraint/Challenge: Cybersecurity Risks And Complex System Integration

As vehicles become more connected and software driven, automotive communication networks are increasingly exposed to cybersecurity threats, including data interception, ECU manipulation, and unauthorized access. The complexity of integrating multiple communication protocols across legacy and modern vehicle platforms further increases system vulnerability and development costs.

Automakers are required to implement advanced encryption, intrusion detection systems, and secure gateway modules, which significantly increase design complexity and production expenses. In addition, interoperability challenges between different protocol standards such as CAN, LIN, FlexRay, and Ethernet create integration bottlenecks during vehicle development cycles.

Cybersecurity testing reports in 2024 indicated that connected vehicle platforms with insufficient protocol isolation experienced potential attack surface expansion across more than 15–20 interconnected ECUs, highlighting critical risks in large scale automotive networking systems, particularly in autonomous and connected vehicle environments.

Key Market Opportunity: Expansion Of Software Defined Vehicles And Over The Air Connectivity

The transition toward software defined vehicles is creating significant opportunities for next generation automotive communication protocols that can support centralized computing architectures and continuous software updates. These systems require high bandwidth, scalable, and secure communication frameworks capable of handling real time data processing and remote software deployment.

Automotive OEMs are increasingly adopting Ethernet based zonal architectures and domain controllers to simplify wiring complexity and improve vehicle scalability. For instance, over the air update systems now enable manufacturers such as Tesla and Mercedes Benz to remotely enhance vehicle performance, fix software bugs, and introduce new features without physical intervention.

In addition, the growth of autonomous driving research and connected fleet management systems in regions such as North America and Asia Pacific is driving demand for high performance in vehicle communication networks. Pilot deployments in 2025 have demonstrated that zonal architecture based communication systems can reduce vehicle wiring harness weight by nearly 25–30%, improving overall vehicle efficiency and manufacturing optimization.

Global Automotive Communication Protocol Market Scope

The market is segmented on the basis of component, bus type, and vehicle type.

- By Component

On the basis of component, the automotive communication protocol market is segmented into Hardware, Software, and Services. The Hardware segment held the largest market revenue share of approximately 52.6% in 2025 driven by the extensive deployment of electronic control units, wiring harnesses, gateways, and communication interfaces across modern vehicles. Increasing integration of ADAS, infotainment systems, and electrified powertrains is further strengthening hardware demand due to rising ECU complexity in passenger and commercial vehicles.

The Software segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by increasing adoption of software defined vehicles, over the air updates, and cybersecurity solutions for in vehicle networks. Growing reliance on middleware, protocol management software, and diagnostic tools for real time communication optimization is accelerating segment expansion.

- By Bus Type

On the basis of bus type, the market is segmented into CAN (Controller Area Network), LIN (Local Interconnect Network), MOST (Media Oriented Systems Transport), and FlexRay. The CAN segment held the largest market revenue share of approximately 41.3% in 2025 driven by its widespread adoption in powertrain systems, body electronics, and safety critical applications due to its reliability, cost efficiency, and proven performance in automotive environments.

The Automotive Ethernet segment, while not part of traditional legacy grouping but increasingly adopted in modern architectures, is projected to register the fastest growth at a CAGR of 12.1% from 2026 to 2033, driven by rising demand for high bandwidth communication in ADAS, autonomous driving systems, and infotainment applications requiring real time data transmission.

- By Vehicle Type

On the basis of vehicle type, the market is segmented into Passenger Cars, Commercial Vehicles (Light and Heavy Duty), Two Wheelers, and Off Highway Vehicles. The Passenger Cars segment held the largest market revenue share of approximately 68.5% in 2025 driven by high production volumes, increasing integration of advanced electronics, and rapid adoption of connected vehicle technologies across global automotive markets.

The Commercial Vehicles segment is projected to register the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by rising demand for fleet connectivity, telematics systems, and regulatory requirements for vehicle safety and emission monitoring. Integration of advanced communication protocols in logistics and transportation fleets is further supporting segment expansion.

Global Automotive Communication Protocol Market Regional Analysis

North America Automotive Communication Protocol Market Insight

North America dominated the automotive communication protocol market with the largest revenue share of 39.6% in 2025, supported by strong penetration of connected vehicles, rapid adoption of ADAS technologies, and increasing integration of high speed in vehicle networking systems. The region benefits from a mature automotive ecosystem, high R&D investment by OEMs, and early deployment of advanced architectures such as Automotive Ethernet and CAN FD across passenger and commercial vehicles. Growing consumer demand for connected mobility and infotainment systems is further accelerating protocol adoption across vehicle platforms.

U.S. Automotive Communication Protocol Market Insight

The U.S. automotive communication protocol market captured the largest revenue share in North America in 2025, driven by the rapid expansion of electric vehicles, autonomous driving programs, and software defined vehicle development. Leading automakers and technology companies are increasingly integrating high bandwidth communication systems to support real time data exchange between sensors, ECUs, and cloud connected platforms. The presence of major OEMs and Tier 1 suppliers, along with strong deployment of over the air update systems and vehicle telematics, is significantly contributing to market growth.

Europe Automotive Communication Protocol Market Insight

The Europe automotive communication protocol market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by strict vehicle safety regulations, rising adoption of electric mobility, and increasing demand for advanced driver assistance systems. Regulatory frameworks such as Euro NCAP and EU cybersecurity mandates are pushing automakers to adopt secure and high speed communication architectures. Growing emphasis on reducing vehicle emissions and improving energy efficiency is also accelerating the integration of advanced networking protocols across automotive platforms.

U.K. Automotive Communication Protocol Market Insight

The U.K. automotive communication protocol market is expected to witness steady growth from 2026 to 2033, driven by increasing adoption of connected vehicle technologies and rising investment in autonomous vehicle testing programs. Strong focus on vehicle safety, coupled with growing demand for fleet management solutions and intelligent transport systems, is supporting protocol integration. In addition, the expansion of smart mobility initiatives and increasing use of cloud connected automotive services are further enhancing market penetration in the region.

Germany Automotive Communication Protocol Market Insight

The Germany automotive communication protocol market is expected to witness significant growth from 2026 to 2033, fueled by strong automotive manufacturing capabilities, high adoption of premium vehicles, and leadership in automotive engineering innovation. German OEMs are actively integrating advanced communication systems to support electrification, autonomous driving, and Industry 4.0 aligned vehicle production. Increasing focus on high precision engineering and secure in vehicle data transmission is driving widespread deployment of CAN FD, FlexRay, and Ethernet based architectures.

Asia-Pacific Automotive Communication Protocol Market Insight

The Asia-Pacific automotive communication protocol market is expected to witness the fastest growth rate from 2026 to 2033, supported by rising vehicle production, rapid urbanization, and increasing adoption of electric vehicles in countries such as China, Japan, South Korea, and India. The region is becoming a major hub for automotive electronics manufacturing, enabling cost efficient deployment of advanced communication systems. Strong government support for smart mobility, coupled with expanding EV infrastructure, is significantly boosting demand for high speed in vehicle networking solutions.

Japan Automotive Communication Protocol Market Insight

The Japan automotive communication protocol market is expected to grow steadily from 2026 to 2033, driven by advanced automotive innovation, high adoption of hybrid vehicles, and strong focus on vehicle safety and reliability. Japanese OEMs are integrating sophisticated communication architectures to support autonomous driving research and energy efficient vehicle systems. The increasing use of robotics and AI enabled mobility solutions is also contributing to demand for high precision and low latency communication protocols across automotive platforms.

China Automotive Communication Protocol Market Insight

The China automotive communication protocol market accounted for the largest revenue share in Asia Pacific in 2025, attributed to massive vehicle production volumes, rapid electrification, and strong government support for intelligent connected vehicles. China is a global leader in electric vehicle adoption, with widespread integration of advanced in vehicle communication systems across both passenger and commercial fleets. The expansion of smart city initiatives and autonomous driving pilot programs is further accelerating demand for scalable, high speed automotive networking technologies.

Global Automotive Communication Protocol Market Share

The Automotive Communication Protocol industry is primarily led by well-established companies, including:

• Robert Bosch GmbH (Germany)

• Continental AG (Germany)

• DENSO Corporation (Japan)

• Aptiv PLC (U.K.)

• NXP Semiconductors (Netherlands)

• Infineon Technologies AG (Germany)

• Texas Instruments Incorporated (U.S.)

• STMicroelectronics N.V. (Switzerland)

• Renesas Electronics Corporation (Japan)

• Vector Informatik GmbH (Germany)

• Cisco Systems, Inc. (U.S.)

• Broadcom Inc. (U.S.)

• Autoliv Inc. (Sweden)

• ZF Friedrichshafen AG (Germany)

• Hitachi Astemo, Ltd. (Japan)

Latest Developments in Global Automotive Communication Protocol Market

- In October 2024, Kvaser, product launch, introduced CanKing 7 CAN analysis software, enabling engineers to test and debug CAN networks with enhanced features such as CAN Trace, Bus Statistics, Send, and Periodic Send, while improving usability through a modern GUI and expanded Linux support on ARM64 and x64 systems, thereby improving development efficiency and accelerating vehicle network validation processes

- In February 2023, Renesas Electronics Corporation, technology development, developed four new SoC technologies for in vehicle communication gateways, designed to support next generation electrical and electronic (E/E) architecture in automobiles, thereby enhancing data processing efficiency, improving communication reliability between ECUs, and enabling scalable integration of advanced automotive networking systems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.