Global Automotive Engine And Engine Mounts Market

Market Size in USD Billion

USD

83.99 Billion

USD

136.94 Billion

2024

2032

USD

83.99 Billion

USD

136.94 Billion

2024

2032

| 2025 - 2032 | |

| USD 83.99 Billion | |

| USD 136.94 Billion | |

| % | |

|

Automotive Engine and Engine Mounts Market Size

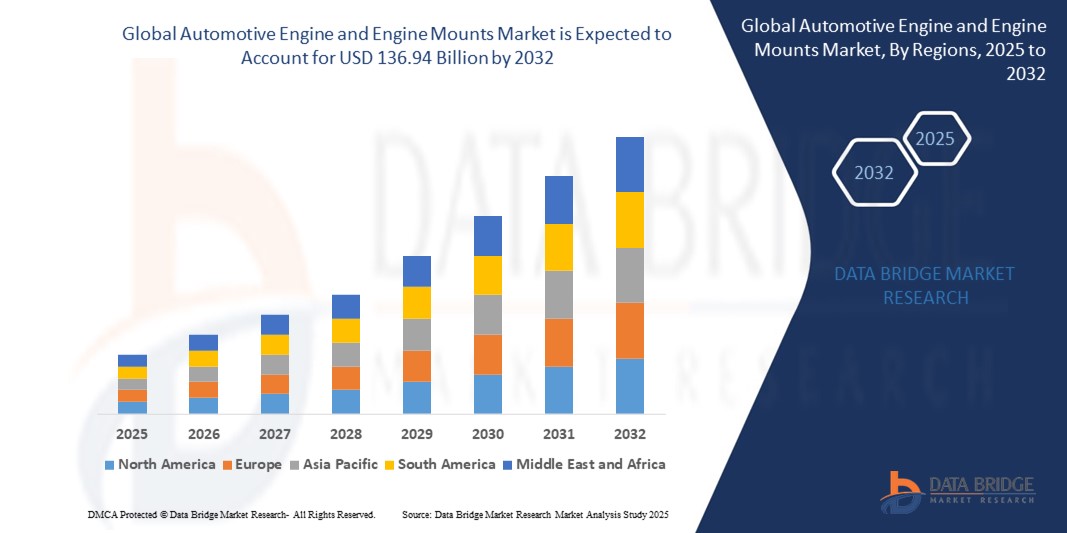

- The Global Automotive Engine and Engine Mounts Market size was valued at USD 83.99 billion in 2024 and is expected to reach USD 136.94 billion by 2032, at a CAGR of 6.30% during the forecast period

- This growth is driven by factors such as the increasing demand for fuel-efficient and lightweight vehicles, rising vehicle production globally, advancements in engine technology, and the growing preference for electric and hybrid vehicles that require specialized engine mounting systems.

Automotive Engine and Engine Mounts Market Analysis

- Automotive engine and engine mounts are critical tools used in various eye surgeries, providing magnified, high-resolution views of the eye’s internal structures. They are essential for procedures such as cataract surgery, retinal surgery, and corneal transplants

- The demand for these microscopes is significantly driven by the increasing prevalence of age-related eye conditions and advancements in surgical techniques.

- Asia-Pacific dominates the Automotive Engine and Engine Mounts Market with the largest revenue share of 37.24% in 2024, fueled by rapid urbanization, strong automotive production, and increasing vehicle ownership across major economies such as China, Japan, and India.

- North America is Fastest Growing in the Automotive Engine and Engine Mounts Market with a revenue share of 29.15% in 2024, driven by the growing demand for high-performance vehicles, SUV dominance, and strong innovation in engine mounting technologies.

- The L4 Engine segment holds the largest market revenue share in 2024, driven by its compact design, fuel efficiency, and suitability for a wide range of passenger vehicles. L4 engines are cost-effective and offer balanced performance, making them the preferred choice among manufacturers for entry-level and mid-size vehicles.

Report Scope and Automotive Engine and Engine Mounts Market Segmentation

|

Attributes |

Automotive Engine and Engine Mounts Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Automotive Engine and Engine Mounts Market Trends

“Rising Use of Smart Engine Mounting Systems”

- Active engine mounts are increasingly replacing traditional rubber or hydraulic mounts due to their ability to reduce noise, vibration, and harshness more effectively, especially in premium and performance vehicles

- These mounts use sensors and actuators to adapt in real-time to changing driving conditions, which enhances engine stability and passenger comfort during both idle and motion

- Automotive manufacturers are prioritizing smoother and quieter ride experiences, prompting the integration of electronically controlled mounts across more vehicle categories beyond just luxury cars

- For instance, some mid-range vehicle models are now being equipped with active engine mounts, showing how this technology is becoming more accessible and not limited to high-end models

- In conclusion, continuous innovation in vehicle dynamics and growing consumer expectations for enhanced driving experiences are pushing suppliers to develop mounts that are smarter, lighter, and more responsive

Automotive Engine and Engine Mounts Market Dynamics

Driver

“Increasing Demand for Fuel-Efficient and Lightweight Vehicles”

- Automakers are focusing on reducing vehicle weight to enhance fuel efficiency, leading to a shift from traditional heavy metal mounts to lighter materials like aluminum composites and high-strength plastics

- Lightweight engine mounts decrease unsprung mass, improving handling and fuel economy while supporting better engine performance due to reduced vibrational resistance

- For instance, Toyota and BMW have integrated aluminum-based engine mounts in select models to align with their lightweight vehicle strategies

- The increasing production of electric and hybrid vehicles is accelerating demand for compact and customized mounting systems that suit new drivetrain layouts

- Governments worldwide are introducing stricter fuel economy standards and incentives for lightweight vehicle components, encouraging manufacturers to adopt advanced mount technologies

- In conclusion, this demand for lightweight mounts is growing steadily as it aligns with both regulatory goals and consumer preferences

Restraint/Challenge

“High Cost of Advanced Engine Mount Technologies”

- Advanced engine mounts with features like adaptive damping and sensor integration offer performance benefits but come with significantly higher production and integration costs

- For instance, luxury models from Mercedes-Benz and Audi adopt electronically controlled mounts, while budget brands often avoid them due to their high cost

- Smaller automakers and mass-market brands face challenges in adopting these technologies as it can raise vehicle prices and impact competitiveness

- Rising raw material costs and global supply chain disruptions are further increasing the financial burden, making it harder for manufacturers to justify the upgrade

- Adopting these mounts often requires redesigning vehicle platforms and production lines, leading to longer development timelines and added engineering expenses

- In conclusion, this cost-related challenge slows down widespread adoption and limits innovation across mid and low-tier segments

Automotive Engine and Engine Mounts Market Scope

The market is segmented on the basis of engine type, fuel type, vehicle type, engine mount, product type, and end user.

- By Engine Type

On the basis of engine type, the Automotive Engine and Engine Mounts Market is segmented into L4 Engine, L6 Engine, V6 Engine, and V8 Engine. The L4 Engine segment holds the largest market revenue share in 2024, driven by its compact design, fuel efficiency, and suitability for a wide range of passenger vehicles. L4 engines are cost-effective and offer balanced performance, making them the preferred choice among manufacturers for entry-level and mid-size vehicles.

The V6 Engine segment is expected to witness the fastest CAGR from 2025 to 2032, owing to rising demand for high-performance vehicles and SUVs. V6 engines offer superior power and smoother operation, appealing to consumers looking for an enhanced driving experience.

- By Fuel Type

On the basis of fuel type, the market is segmented into Gasoline, Diesel, Hybrid, and Natural Gas. The Gasoline segment dominated the market share in 2024 due to the widespread availability of gasoline infrastructure and the affordability of gasoline-powered vehicles. Gasoline engines offer a smoother and quieter ride, which remains a key factor in their popularity.

The Hybrid segment is projected to grow at the fastest rate through 2032, driven by increasing environmental concerns, fuel efficiency, and regulatory support for cleaner vehicles. Automakers are investing heavily in hybrid technologies to comply with emission norms and appeal to eco-conscious consumers..

- By Vehicle Type

On the basis of vehicle type, the market is segmented into Passenger Car, LCV, HCV, and Two-Wheeler. The Passenger Car segment accounted for the largest share in 2024, supported by high global production volumes and consumer preference for personal mobility solutions. Innovations in engine technology and engine mounts to reduce noise and vibration have further boosted this segment.

The LCV (Light Commercial Vehicle) segment is expected to experience the fastest growth, fueled by the expansion of the e-commerce and logistics sectors. These vehicles require durable engine mounts to handle frequent starts, stops, and load changes.

- By Engine Mount

On the basis of engine mount, the market is segmented into Elastomer, Hydraulic, and Electrohydraulic. The Elastomer segment dominated the market in 2024, attributed to its cost-effectiveness and widespread usage in small and mid-size vehicles. Elastomer mounts are simple in construction and provide adequate vibration damping for standard vehicle models.

The Electrohydraulic segment is expected to register the fastest CAGR from 2025 to 2032. These advanced mounts offer dynamic damping characteristics, adjusting in real-time based on driving conditions. Their adoption is growing in premium and luxury vehicles for enhanced comfort and reduced cabin noise.

- By Product Type

On the basis of product type, the market is segmented into Semi-Active Engine Mount and Active Engine Mount. The Semi-Active Engine Mount segment held the largest revenue share in 2024, due to its balance between cost and performance. These mounts use passive materials but can adjust stiffness to a limited extent based on engine behavior.

The Active Engine Mount segment is anticipated to grow at the fastest rate, driven by the demand for high-end comfort and reduced NVH (Noise, Vibration, and Harshness) levels. Active mounts use sensors and actuators to counteract engine vibrations, becoming increasingly common in luxury and hybrid vehicles.

- By End User

On the basis of end user, the market is segmented into SUV and Sedan. The SUV segment led the market in 2024, supported by the global trend toward larger, more powerful vehicles. SUVs often require robust engine systems and advanced mounts to support heavier loads and off-road capabilities.

The Sedan segment is expected to grow at a steady pace, favored for urban commuting and fuel economy. Improvements in lightweight engine design and comfort-enhancing engine mounts are driving adoption among family and corporate buyers.

Automotive Engine and Engine Mounts Market Regional Analysis

- Asia-Pacific dominates the Automotive Engine and Engine Mounts Market with the largest revenue share of 37.24% in 2024, fueled by rapid urbanization, strong automotive production, and increasing vehicle ownership across major economies such as China, Japan, and India.

- The region benefits from cost-effective manufacturing, rising disposable incomes, and growing consumer preference for technologically advanced vehicles with reduced noise and vibration.

- Government initiatives supporting automotive innovation and green technologies, coupled with the rising demand for fuel-efficient engines and premium vehicles, are accelerating the market growth.

China Automotive Engine and Engine Mounts Market Insight

The China Automotive Engine and Engine Mounts Market captured the largest market revenue share within Asia-Pacific in 2024, driven by the country’s vast automotive production capacity and consumer demand for enhanced vehicle comfort and engine performance. The presence of key automakers and component suppliers, along with a supportive regulatory framework, makes China a central hub for both domestic consumption and export-oriented manufacturing of engine systems and mounts.

Japan Automotive Engine and Engine Mounts Market Insight

The Japan market is experiencing steady growth, supported by high adoption of hybrid and electric vehicles and strong investments in R&D for advanced engine technologies. Japanese consumers value vehicle refinement and comfort, prompting demand for premium engine mounts that reduce NVH (Noise, Vibration, and Harshness). The integration of active and semi-active mounts in newer vehicle models is gaining traction.

India Automotive Engine and Engine Mounts Market Insight

India is emerging as a high-growth market for automotive engines and mounts, supported by rising vehicle production, infrastructure development, and favorable government schemes like “Make in India.” The demand is especially high for LCVs and passenger cars, with elastomer engine mounts dominating due to cost efficiency. However, adoption of hydraulic and semi-active mounts is gradually increasing in urban markets.

North America Automotive Engine and Engine Mounts Market Insight

North America is fastest growing in the Automotive Engine and Engine Mounts Market with a revenue share of 29.15% in 2024, driven by the growing demand for high-performance vehicles, SUV dominance, and strong innovation in engine mounting technologies. Consumer preference for smooth driving experience, enhanced safety, and vehicle durability continues to support market growth. The integration of electrohydraulic mounts in high-end models is also a key trend.

U.S. Automotive Engine and Engine Mounts Market Insight

The U.S. market held the largest share in North America with 74.33% in 2024, driven by strong automotive manufacturing infrastructure and consumer inclination toward large vehicles such as SUVs and trucks. The country is also witnessing increased adoption of hybrid engines and active mounts, especially in premium vehicle segments. Additionally, ongoing developments in electric vehicles are reshaping demand patterns in the engine mounts segment.

Europe Automotive Engine and Engine Mounts Market Insight

Europe holds significant market share at 24.49% in 2024, primarily supported by stringent emission regulations, premium vehicle production, and technological innovation in engine performance and vibration control. The market is seeing strong momentum in the adoption of semi-active and active mounts across electric, hybrid, and high-end internal combustion vehicles..

Germany Automotive Engine and Engine Mounts Market Insight

Germany, being a global leader in automotive engineering, is at the forefront of advanced engine and mount system adoption. The market is driven by the production of luxury vehicles and a strong R&D ecosystem. Active engine mounts are increasingly used in German sedans and electric models to meet consumer expectations for silent and smooth rides.

U.K. Automotive Engine and Engine Mounts Market Insight

The U.K. market is expanding at a notable pace, driven by the country’s strong focus on automotive innovation and export. Demand for engine mounts in EVs and hybrid vehicles is growing, with manufacturers prioritizing comfort, efficiency, and compliance with EU-level noise and emission standards.

Automotive Engine and Engine Mounts Market Share

The Automotive Engine and Engine Mounts industry is primarily led by well-established companies, including:

- Cummins Inc (U.S.)

- Hyundai Motor Company (South Korea)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- MAHLE GmbH (Germany)

- Scania (Sweden)

- Fiat Chrysler Automobiles (Netherlands)

- HUTCHINSON (France)

- Cooper Standard (U.S.)

- Trelleborg AB (Sweden)

- TOYO TIRE U.S.A. CORP (U.S.)

- Yamashita Rubber (Japan)

- Sumitomo Riko Company Limited (Japan)

- ZF Friedrichshafen AG (Germany)

- BOGE Rubber & Plastics (Germany)

- BWI Group (China)

- Vibracoustic GmbH (Germany)

- Continental AG (Germany)

- Bridgestone Corporation (Japan)

- Nissin Kogyo Co., Ltd. (Japan)

- Magna International Inc. (Canada)

- DENSO Corporation (Japan)

- ElringKlinger AG (Germany)

- Tenneco Inc. (U.S.)

- Anvis Group GmbH (Germany)

- ACE International (India)

Latest Developments in Global Automotive Engine and Engine Mounts Market

- In March 2024, Trelleborg Group, a global leader in engineered polymer solutions, announced the expansion of its automotive anti-vibration solutions facility in India. This expansion aims to enhance production capacity for engine mounts and other NVH (Noise, Vibration, and Harshness) control products tailored for local and global automotive OEMs. The move aligns with the company’s strategy to strengthen its presence in emerging markets and meet the rising demand for high-performance engine mounting systems in Asia-Pacific.

- In February 2024, Hutchinson SA, a major player in automotive vibration control, unveiled its next-generation lightweight composite engine mounts designed to improve fuel efficiency and reduce overall vehicle weight. These mounts are developed specifically for hybrid and electric vehicles, reflecting Hutchinson’s commitment to innovation in sustainable mobility solutions and its response to evolving industry trends toward electrification.

- In December 2023, ZF Friedrichshafen AG introduced a new line of active engine mounts integrated with adaptive damping technology. Designed for luxury and electric vehicles, these mounts dynamically adjust to driving conditions, offering enhanced ride comfort and engine isolation. The launch emphasizes ZF’s focus on delivering advanced, intelligent mounting systems that align with modern vehicle architectures and consumer expectations for comfort and performance.

- In October 2023, BorgWarner Inc. announced the acquisition of Drivetek AG, a Swiss-based engineering company specializing in powertrain and vibration management systems. This strategic acquisition aims to broaden BorgWarner’s product portfolio in the engine mounts and e-mobility space, allowing it to deliver more integrated solutions for electric and hybrid vehicles while reinforcing its market position in advanced drivetrain technologies.

- In July 2023, Continental AG launched its innovative hydraulic engine mount system for high-performance and off-road vehicles. This product, developed using enhanced elastomer materials, delivers superior noise and vibration dampening even in extreme conditions. Continental’s development highlights its continued investment in vehicle comfort and durability, catering to niche and rugged automotive segments.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.