Global Automotive Engine Management System Market

Market Size in USD Billion

USD

54.76 Billion

USD

62.67 Billion

2025

2033

USD

54.76 Billion

USD

62.67 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 54.76 Billion |

Market Size (Forecast Year) |

USD 62.67 Billion |

CAGR |

% |

Major Markets Players |

|

What is the Global Automotive Engine Management System Market Size and Growth Rate?

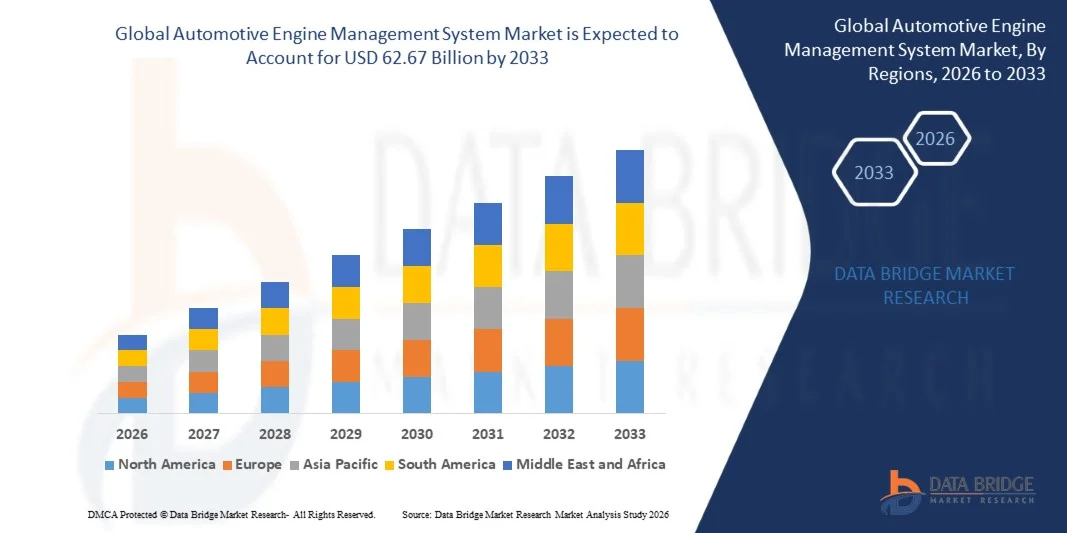

- As per Data Bridge Market Research Analysis the global automotive engine management system market size was valued at USD 54.76 billion in 2025 and is expected to reach USD 62.67 billion by 2033, at a CAGR of1.70% during the forecast period

- The automotive engine management system market has a huge potential to grow over the forecast period, owing to the strict emission and fuel economy standards. In addition, the improved vehicle performance and rapid increase in the sales of new vehicles are also largely influencing the growth of the automotive engine management system market.

Market Size & Forecast

- Global Market Value (2025): USD 54.76 billion

- Expected Market Value (2033): USD 62.67 billion

- Forecast CAGR (2026–2033):1.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

What are the Major Takeaways of Automotive Engine Management System Market?

- The high per capita income as well as the booming automotive industry associated with increasing registration of new car is another driver flourishing the automotive engine management system market growth

- In addition, the increasing involvement of new market players has augmented the willingness of established players to offer relatively affordable prices for quality products and are projected to witness significant growth

- North America dominated the automotive engine management system market with a 36.31% revenue share in 2025, driven by strong automotive R&D capabilities, advanced powertrain engineering, and early adoption of emission-compliant engine control technologies across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 7.69% from 2026 to 2033, driven by rapid vehicle production growth, expanding automotive manufacturing ecosystems, and rising adoption of fuel-efficient and emission-compliant engine technologies across China, Japan, India, South Korea, and Southeast Asia

- The Controller Area Network (CAN) segment dominated the market with an estimated 52.6% share in 2025, owing to its wide adoption in engine control units, powertrain modules, and real-time vehicle communication systems

Report Scope and Automotive Engine Management System Market Segmentation

|

Attributes |

Automotive Engine Management System Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Automotive Engine Management System Market?

“Increasing Shift Toward Electrification, Software-Defined Control, and Real-Time Engine Optimization”

- The automotive engine management systems market is witnessing a strong shift toward software-driven, compact, and high-speed control units designed to optimize fuel efficiency, emissions compliance, and engine performance in real time

- OEMs are increasingly adopting advanced ECUs with multi-core processors, high-speed sensors, and real-time data processing to support complex combustion strategies, hybrid powertrains, and emission control technologies

- Rising integration of AI-based algorithms, adaptive engine mapping, and predictive diagnostics is enhancing engine responsiveness, durability, and regulatory compliance

- For instance, companies such as Bosch, Continental, DENSO, and BorgWarner are upgrading engine management platforms with enhanced processing capability, integrated diagnostics, and compatibility with hybrid and EV architectures

- Growing demand for precise engine calibration, real-time monitoring, and multi-sensor data fusion is accelerating the transition toward intelligent and software-defined engine management systems

- As vehicles become more connected, electrified, and regulation-driven, automotive engine management systems will remain critical for powertrain efficiency, emissions reduction, and vehicle performance optimization

What are the Key Drivers of Automotive Engine Management System Market?

- Rising demand for affordable, accurate, and easy-to-use logic analyzers to support rapid debugging and validation in microcontroller, FPGA, and digital circuit development

- For instance, in 2025, leading companies such as Saleae, Yokogawa, and Good Will Instrument upgraded their analyzer portfolios to support higher sampling rates, enhanced protocol decoding, and flexible software interfaces

- Growing adoption of IoT devices, consumer electronics, robotics, EV systems, and smart automation is boosting demand for digital signal testing tools across the U.S., Europe, and Asia-Pacific

- Advancements in signal acquisition, memory depth, waveform compression, and USB-powered architectures have strengthened performance, portability, and efficiency

- Rising use of AI chips, high-speed serial interfaces, and complex communication buses is creating demand for high-density, multi-channel portable analyzers

- Supported by steady investments in electronics R&D, semiconductor innovation, and testing infrastructure, the Automotive Engine Management System market is expected to witness strong long-term growth

Which Factor is Challenging the Growth of the Automotive Engine Management System Market?

- High development and integration costs associated with advanced ECUs, high-precision sensors, and software validation restrict adoption, particularly among low-cost vehicle segments

- For instance, during 2024–2025, rising costs of semiconductors, automotive-grade chips, and electronic components increased production expenses for global engine management system suppliers

- Increasing complexity of engine calibration, software validation, and compliance with diverse global emission standards raises development timelines and engineering costs

- Limited availability of skilled automotive software engineers and calibration experts poses challenges for system optimization and deployment

- Growing competition from electrification trends and reduced ICE vehicle volumes creates long-term uncertainty for traditional engine management system demand

- To overcome these challenges, manufacturers are focusing on modular system designs, software reusability, scalable platforms, and integration with hybrid architectures to sustain adoption of automotive engine management systems

How is the Automotive Engine Management System Market Segmented?

The market is segmented on the basis of communication technology, engine type, component, and vehicle type.

- By Communication Technology

On the basis of communication technology, the automotive engine management system market is segmented into Controller Area Network (CAN), Local Interconnect Network (LIN), and FlexRay. The Controller Area Network (CAN) segment dominated the market with an estimated 52.6% share in 2025, owing to its wide adoption in engine control units, powertrain modules, and real-time vehicle communication systems. CAN offers high reliability, robust error handling, and efficient data transmission, making it the preferred protocol for engine speed, fuel injection, ignition timing, and emissions control applications. Its cost-effectiveness and compatibility with legacy vehicle architectures further strengthen its dominance across passenger and commercial vehicles.

The FlexRay segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for high-speed, deterministic communication in advanced powertrains, hybrid vehicles, and performance-oriented automotive systems. Growing ECU complexity and demand for synchronized data transmission are accelerating FlexRay adoption.

- By Engine Type

On the basis of engine type, the automotive engine management system market is segmented into Gasoline Engine Management Systems and Diesel Engine Management Systems. The Gasoline Engine Management System segment dominated the market with a 58.1% share in 2025, supported by high global production of gasoline-powered passenger vehicles and continuous advancements in fuel injection, ignition control, and emission optimization technologies. Gasoline EMS solutions are widely used to enhance fuel efficiency, throttle response, and compliance with emission regulations such as Euro 6 and BS-VI. Increasing integration of turbocharging and direct injection further drives demand for advanced gasoline engine control systems.

The Diesel Engine Management System segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising demand for diesel engines in commercial vehicles, construction equipment, and long-haul transportation. Stricter emission norms and the need for precise combustion control are boosting adoption of advanced diesel EMS technologies.

- By Component

On the basis of component, the automotive engine management system market is segmented into Engine Control Unit (ECU), Engine Sensors, Fuel Pump, and Others. The Engine Control Unit (ECU) segment dominated the market with a 44.3% share in 2025, as it serves as the central processing unit responsible for managing fuel injection, ignition timing, air–fuel ratio, and emission control. Increasing ECU integration with advanced software algorithms, real-time diagnostics, and adaptive engine mapping strengthens its market leadership. OEMs increasingly rely on high-performance ECUs to support hybrid powertrains and regulatory compliance.

The Engine Sensors segment is expected to register the fastest CAGR from 2026 to 2033, driven by growing demand for real-time data from oxygen sensors, crankshaft position sensors, temperature sensors, and pressure sensors. Rising emphasis on precision control, predictive diagnostics, and emission monitoring is accelerating sensor deployment across vehicle platforms.

- By Vehicle Type

On the basis of vehicle type, the automotive engine management system market is segmented into Passenger Cars, Light Commercial Vehicles (LCVs), and Heavy Commercial Vehicles (HCVs). The Passenger Cars segment dominated the market with a 61.7% share in 2025, driven by high global vehicle production volumes, increasing consumer demand for fuel efficiency, and stricter emission regulations. Advanced engine management systems are widely integrated into passenger cars to optimize performance, reduce emissions, and enhance drivability. Rapid adoption of connected features and hybrid variants further strengthens this segment.

The Heavy Commercial Vehicle segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by expanding logistics, infrastructure development, and demand for long-haul transportation. Increasing focus on fuel optimization, engine durability, and emission compliance is driving adoption of advanced engine management systems in heavy-duty vehicles.

Which Region Holds the Largest Share of the Automotive Engine Management System Market?

- North America dominated the automotive engine management system market with a 36.31% revenue share in 2025, driven by strong automotive R&D capabilities, advanced powertrain engineering, and early adoption of emission-compliant engine control technologies across the U.S. and Canada. High integration of electronic control units (ECUs), sensors, and real-time engine monitoring systems across passenger and commercial vehicles continues to fuel market demand

- Leading OEMs and Tier-1 suppliers in the region are investing in advanced engine control architectures, software-driven calibration tools, and compliance-ready engine management platforms, strengthening regional technological leadership

- Strong engineering talent availability, mature automotive supply chains, and sustained investments in electrification and hybrid powertrains further reinforce North America’s market dominance

U.S. Automotive Engine Management System Market Insight

The U.S. is the largest contributor in North America, supported by strong automotive manufacturing, advanced engine calibration capabilities, and rapid adoption of emission-optimized engine technologies. Increasing development of turbocharged engines, hybrid powertrains, and advanced fuel injection systems intensifies demand for high-performance Automotive Engine Management Systems. Presence of major OEMs, Tier-1 suppliers, and testing facilities further supports market growth.

Canada Automotive Engine Management System Market Insight

Canada contributes significantly to regional growth, driven by rising automotive electronics production, expanding powertrain R&D activities, and growing investment in emission-reduction technologies. Increasing use of advanced engine control systems in commercial vehicles and automotive testing centers supports steady market adoption.

Asia-Pacific Automotive Engine Management System Market

Asia-Pacific is projected to register the fastest CAGR of 7.69% from 2026 to 2033, driven by rapid vehicle production growth, expanding automotive manufacturing ecosystems, and rising adoption of fuel-efficient and emission-compliant engine technologies across China, Japan, India, South Korea, and Southeast Asia. High-volume production of passenger cars, commercial vehicles, and automotive ECUs significantly increases demand for reliable and cost-effective Automotive Engine Management Systems. Growth in hybrid vehicles, stricter emission regulations, and rising investments in automotive electronics continue to accelerate regional market expansion.

China Automotive Engine Management System Market Insight

China is the largest contributor to Asia-Pacific due to massive vehicle production capacity, strong government support for emission control, and rapid adoption of advanced engine electronics. Growing deployment of turbocharged and hybrid engines drives demand for sophisticated engine management systems.

Japan Automotive Engine Management System Market Insight

Japan shows steady growth supported by technological leadership in automotive engineering, precision manufacturing, and continuous innovation in powertrain systems. Strong focus on fuel efficiency and reliability drives adoption of advanced Automotive Engine Management Systems.

India Automotive Engine Management System Market Insight

India is emerging as a high-growth market, driven by rising vehicle production, BS-VI emission compliance, and expanding automotive electronics manufacturing. Increasing localization of ECUs and sensors accelerates market penetration.

South Korea Automotive Engine Management System Market Insight

South Korea contributes significantly due to strong OEM presence, advanced automotive electronics capabilities, and increasing development of fuel-efficient and hybrid vehicles. Continuous innovation and manufacturing strength support sustained market growth.

Which are the Top Companies in Automotive Engine Management System Market?

The automotive engine management system industry is primarily led by well-established companies, including:

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- DENSO CORPORATION (Japan)

- BorgWarner Inc. (U.S.)

- HELLA GmbH & Co. KGaA (Germany)

- Hitachi Automotive Systems Americas, Inc. (U.S.)

- Valeo (France)

- Infineon Technologies AG (Germany)

- NGK SPARK PLUG CO., LTD. (Japan)

- SANKEN ELECTRIC CO., LTD. (Japan)

- DURA AUTOMOTIVE SYSTEMS (U.S.)

- MBE Systems (U.S.)

- Sensata Technologies, Inc. (U.S.)

- Mercedes-Benz India Pvt. Ltd. (India)

- CTS Corporation (U.S.)

- JTEKT Corporation (Japan)

- Mobiletron Electronics Co., Ltd. (Thailand)

- TE Connectivity (Switzerland)

- NXP Semiconductors (Netherlands)

- ZF Friedrichshafen AG (Germany)

What are the Recent Developments in Global Automotive Engine Management System Market?

- In September 2024, Sensata Technologies launched a new range of high-precision pressure sensors for automotive applications, designed to enhance engine management systems by providing real-time, accurate data on engine and environmental conditions, thereby improving overall vehicle efficiency and performance

- In January 2022, Hitachi developed an advanced EMS system for gasoline-powered engines using A.I. to optimize fuel injection and timing, enhancing fuel efficiency and supporting smarter engine control for modern vehicles

- In December 2021, Bosch introduced an EMS for hydrogen fuel cell vehicles, leveraging advanced sensors to manage the fuel cell stack, optimize performance, and reduce emissions, marking a step forward in sustainable automotive technology

- In November 2021, Magneti Marelli developed an EMS for electric and hybrid vehicles to optimize battery, motor, and power electronics performance, improving overall efficiency and supporting the growing EV and hybrid vehicle market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.