Global Automotive Exhaust Shield Market

Market Size in USD Billion

USD

16.61 Billion

USD

20.39 Billion

2025

2033

USD

16.61 Billion

USD

20.39 Billion

2025

2033

| 2026 - 2033 | |

| USD 16.61 Billion | |

| USD 20.39 Billion | |

| % | |

|

Automotive Exhaust Shield Market Overview

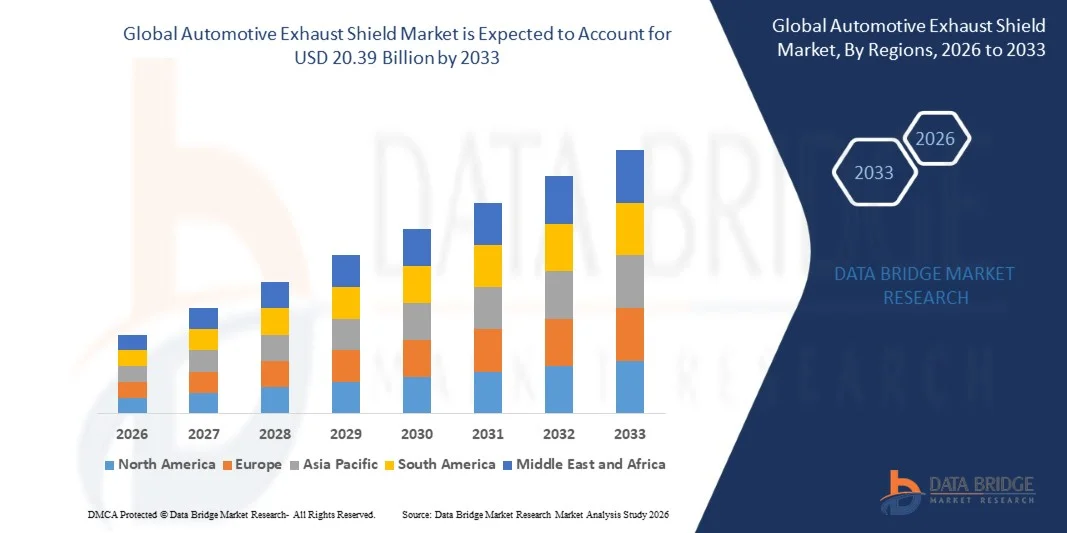

The Automotive Exhaust Shield Market was valued at USD 16.61 billion in 2025 and is projected to reach USD 20.39 billion by 2033, growing at a CAGR of 2.60% from 2026 to 2033. The market is witnessing steady expansion driven by increasing demand for effective thermal management solutions in vehicles, rising focus on passenger safety, and growing adoption of lightweight and heat-resistant materials in automotive manufacturing.

The growing implementation of stringent emission norms and fuel efficiency standards is encouraging automakers to integrate advanced exhaust shielding systems to reduce heat transfer and improve overall vehicle performance. In addition, rising automotive production, especially in emerging economies, is supporting market growth. The increasing adoption of turbocharged engines and high-performance powertrains is further amplifying the need for efficient thermal insulation solutions. Moreover, advancements in materials such as stainless steel, aluminum composites, and high-temperature polymers are enhancing durability and efficiency, making exhaust shields essential across passenger vehicles, commercial vehicles, and motorsport applications.

Key Market Trends & Insights

- North America dominated the automotive exhaust shield market with the largest revenue share of 37.8% in 2025, supported by strong automotive manufacturing activity, high adoption of advanced thermal management technologies, and stringent vehicle safety and emission compliance standards.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 3.8% from 2026 to 2033. Growth is driven by rapid urbanization, expanding vehicle production, increasing demand for affordable automobiles, and strong government initiatives supporting emission reduction and fuel efficiency improvements.

- The Double Shell segment held the largest market revenue share of approximately 38.0% in 2025 driven by its superior thermal insulation performance, structural rigidity, and widespread adoption in modern passenger and commercial vehicles. Double shell configurations are widely used to minimize heat transfer in high-temperature exhaust systems and provide enhanced durability under continuous thermal cycling conditions.

- The Single Shell segment accounted for around 42.5% share in 2025 supported by its cost-effectiveness, lightweight structure, and extensive use in entry-level vehicles and compact automotive platforms where moderate thermal insulation is sufficient. The Sandwich segment is projected to hold approximately 19.5% share, driven by increasing adoption in premium and performance vehicles requiring advanced heat resistance and noise reduction capabilities.

- The Non-Acoustic segment dominated with approximately 72.0% market share in 2025 driven by its primary use in thermal insulation applications across exhaust systems and engine compartments. These shields are widely deployed to prevent heat damage to surrounding components and improve overall vehicle safety performance.

- The Acoustic segment accounted for around 28.0% share in 2025 and is gaining traction due to increasing demand for noise, vibration, and harshness (NVH) reduction in passenger vehicles. For instance luxury vehicle manufacturers are increasingly integrating acoustic exhaust shields to reduce engine and exhaust noise transmission into the cabin, improving driving comfort and refinement.

- The Metallic segment held the largest market share of approximately 78.0% in 2025 driven by high thermal resistance, durability, and cost efficiency of materials such as stainless steel and aluminum alloys. Metallic shields are widely used across passenger cars, light commercial vehicles, and heavy-duty applications due to their ability to withstand extreme exhaust temperatures exceeding 800°C.

- The Non-Metallic segment accounted for around 22.0% share in 2025 and is projected to grow steadily due to rising adoption of ceramic-based composites, fiber-reinforced polymers, and advanced insulation materials in electric and hybrid vehicle platforms where lightweight construction is critical.

- The PC segment held the largest share of approximately 58.0% in 2025 driven by high production volumes, increasing demand for passenger safety, and growing adoption of advanced thermal shielding systems in compact and mid-size vehicles.

- The LCV segment accounted for around 24.0% share in 2025 supported by expanding logistics and e-commerce sectors requiring durable thermal protection systems. The HCV segment held approximately 18.0% share driven by heavy-duty diesel engines and long-haul transportation applications where exhaust heat management is critical for operational safety and component longevity.

- The Exhaust System Heat Shield segment dominated with approximately 30.0% share in 2025 driven by its essential role in controlling extreme exhaust heat and protecting adjacent vehicle components.

- The Engine Compartment Heat Shield segment accounted for around 22.0% share supported by rising engine downsizing and turbocharging trends generating higher thermal loads. The Under Bonnet segment held approximately 18.0% share, while Under Chassis Heat Shield accounted for 15.0% share driven by improved vehicle safety regulations and thermal protection requirements.

Market Size & Forecast

- Global Market Value (2025): USD 16.61 Billion

- Expected Market Value (2033): USD 20.39 Billion

- Forecast CAGR (2026–2033): 2.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Automotive Exhaust Shield Market Segmentation

|

Attributes |

Automotive Exhaust Shield Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Morgan Advanced Materials (U.K.) |

|

Market Opportunities |

• Expansion Of Lightweight Heat Shield Materials |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Exhaust Shield Market Trends

Trend: Growth In Lightweight Thermal Insulation And Advanced Exhaust Shielding Materials

Increasing demand for high-performance thermal management solutions in automotive systems is driving the adoption of advanced exhaust shielding materials across passenger vehicles, commercial vehicles, and motorsport applications. Conventional metal-based shielding systems are being replaced with multilayer composites and ceramic-coated structures due to their superior heat resistance, reduced weight, and improved durability under extreme engine conditions.

In modern internal combustion and hybrid vehicles, automakers are increasingly integrating advanced exhaust shields, For instance stainless steel-aluminum composite shields and mica-based insulation layers, to reduce heat transfer from exhaust systems to surrounding components such as fuel lines, battery packs, and cabin floors, improving safety and thermal efficiency. In high-performance vehicles, thermal shielding is critical for turbocharged engines where exhaust temperatures can exceed 900°C, requiring materials capable of maintaining structural integrity under continuous thermal cycling.

The rapid expansion of lightweight vehicle manufacturing and electric hybrid platforms is also increasing demand for compact and heat-efficient shielding solutions capable of reducing overall vehicle weight while maintaining regulatory compliance for thermal safety standards. In addition, automotive OEMs such as BMW and Toyota have increasingly adopted multi-layer exhaust shielding systems in their hybrid platforms to optimize underbody heat management and improve energy efficiency, particularly in urban driving conditions where heat accumulation is higher.

Automotive Exhaust Shield Market Dynamics

Key Market Driver: Increasing Demand For Vehicle Thermal Safety And Emission Compliance

Automotive manufacturers are under growing regulatory pressure to control underbody heat emissions, improve passenger safety, and comply with stringent global emission standards such as Euro 6 and BS-VI regulations. Exhaust systems in modern engines generate extremely high temperatures, requiring effective shielding to protect nearby components and reduce thermal damage risks.

Automakers are increasingly integrating advanced exhaust shielding systems, For instance double-layer metallic shields and ceramic fiber reinforced barriers, to enhance heat dissipation control and improve vehicle safety performance. In passenger vehicles, exhaust shielding is essential for preventing heat-related degradation of wiring harnesses, fuel tanks, and interior flooring systems, especially in compact vehicle architectures.

Similarly, commercial vehicle manufacturers are adopting reinforced thermal shielding systems to improve durability under long-distance and heavy-load operations, particularly in diesel-powered trucks and buses operating in high-temperature environments. Real-world automotive testing in 2024 across European commercial fleets indicated that advanced exhaust shielding systems reduced underbody heat exposure by nearly 18–25% compared to conventional single-layer steel shields.

Key Restraint/Challenge: High Material Costs And Design Complexity

The development and integration of advanced exhaust shielding systems require high-performance materials such as stainless steel alloys, aluminum composites, and ceramic-coated textiles, which significantly increase manufacturing costs compared to traditional shielding solutions. This cost burden becomes more pronounced in entry-level and economy vehicle segments where pricing sensitivity is high.

In addition, complex vehicle architectures and tighter engine compartments in modern automobiles increase engineering challenges related to fitting and maintaining effective thermal insulation without affecting overall vehicle weight or performance. Limited standardization across OEM platforms further complicates large-scale adoption.

Industry benchmarks indicate that advanced multi-layer exhaust shielding systems, For instance ceramic-coated stainless steel shields, can increase component costs by approximately 20–35% compared to conventional stamped steel heat shields, limiting adoption in cost-sensitive emerging markets.

Key Market Opportunity: Expansion Of Electric Hybrid Platforms And Lightweight Vehicle Design

The rapid growth of hybrid electric vehicles and next-generation lightweight automotive platforms is creating significant opportunities for advanced exhaust shielding solutions. These systems are increasingly required to manage complex thermal interactions between combustion engines, electric drivetrains, and battery modules within confined vehicle structures.

Automotive manufacturers are increasingly adopting advanced shielding systems, For instance integrated thermal barriers between exhaust assemblies and EV battery enclosures in hybrid SUVs, to enhance safety, optimize space utilization, and improve overall system efficiency. In performance and luxury vehicles, advanced thermal insulation is being used to support high-output engines while maintaining cabin comfort and reducing NVH (noise, vibration, and harshness) levels.

In addition, rising investments in electric hybrid platforms across Asia-Pacific and Europe are accelerating demand for next-generation heat shielding technologies. Automotive testing programs conducted in 2025 in Germany and Japan reported that optimized multi-layer exhaust shielding reduced peak underbody temperatures by approximately 15–22°C in hybrid vehicle prototypes under high-load driving conditions.

Automotive Exhaust Shield Market Scope

The market is segmented on the basis of product type, function type, material type, vehicle type, application, and sales channel.

• By Product Type

On the basis of product type, the automotive exhaust shield market is segmented into Single Shell, Double Shell, and Sandwich. The Double Shell segment held the largest market revenue share of approximately 38.0% in 2025 driven by its superior thermal insulation performance, structural rigidity, and widespread adoption in modern passenger and commercial vehicles. Double shell configurations are widely used to minimize heat transfer in high-temperature exhaust systems and provide enhanced durability under continuous thermal cycling conditions.

The Single Shell segment accounted for around 42.5% share in 2025 supported by its cost-effectiveness, lightweight structure, and extensive use in entry-level vehicles and compact automotive platforms where moderate thermal insulation is sufficient. The Sandwich segment is projected to hold approximately 19.5% share, driven by increasing adoption in premium and performance vehicles requiring advanced heat resistance and noise reduction capabilities.

• By Function Type

On the basis of function type, the market is segmented into Acoustic and Non-Acoustic. The Non-Acoustic segment dominated with approximately 72.0% market share in 2025 driven by its primary use in thermal insulation applications across exhaust systems and engine compartments. These shields are widely deployed to prevent heat damage to surrounding components and improve overall vehicle safety performance.

The Acoustic segment accounted for around 28.0% share in 2025 and is gaining traction due to increasing demand for noise, vibration, and harshness (NVH) reduction in passenger vehicles. For instance luxury vehicle manufacturers are increasingly integrating acoustic exhaust shields to reduce engine and exhaust noise transmission into the cabin, improving driving comfort and refinement.

• By Material Type

On the basis of material type, the market is segmented into Metallic and Non-Metallic. The Metallic segment held the largest market share of approximately 78.0% in 2025 driven by high thermal resistance, durability, and cost efficiency of materials such as stainless steel and aluminum alloys. Metallic shields are widely used across passenger cars, light commercial vehicles, and heavy-duty applications due to their ability to withstand extreme exhaust temperatures exceeding 800°C.

The Non-Metallic segment accounted for around 22.0% share in 2025 and is projected to grow steadily due to rising adoption of ceramic-based composites, fiber-reinforced polymers, and advanced insulation materials in electric and hybrid vehicle platforms where lightweight construction is critical.

• By Vehicle Type

On the basis of vehicle type, the market is segmented into PC, LCV, and HCV. The PC segment held the largest share of approximately 58.0% in 2025 driven by high production volumes, increasing demand for passenger safety, and growing adoption of advanced thermal shielding systems in compact and mid-size vehicles.

The LCV segment accounted for around 24.0% share in 2025 supported by expanding logistics and e-commerce sectors requiring durable thermal protection systems. The HCV segment held approximately 18.0% share driven by heavy-duty diesel engines and long-haul transportation applications where exhaust heat management is critical for operational safety and component longevity.

• By Application

On the basis of application, the market is segmented into Exhaust System Heat Shield, Engine Compartment Heat Shield, Under Bonnet Heat Shield, Under Chassis Heat Shield, and Turbocharger Heat Shield. The Exhaust System Heat Shield segment dominated with approximately 30.0% share in 2025 driven by its essential role in controlling extreme exhaust heat and protecting adjacent vehicle components.

The Engine Compartment Heat Shield segment accounted for around 22.0% share supported by rising engine downsizing and turbocharging trends generating higher thermal loads. The Under Bonnet segment held approximately 18.0% share, while Under Chassis Heat Shield accounted for 15.0% share driven by improved vehicle safety regulations and thermal protection requirements.

• By Sales Channel

On the basis of sales channel, the market is segmented into OEM and Aftermarket. The OEM segment dominated with approximately 81.0% market share in 2025 driven by direct integration of exhaust shielding systems during vehicle manufacturing and increasing collaboration between automakers and component suppliers for advanced thermal management solutions.

The Aftermarket segment accounted for around 19.0% share driven by replacement demand, vehicle modification trends, and increasing focus on performance upgrades and thermal efficiency improvements in older vehicle fleets.

Automotive Exhaust Shield Market Regional Analysis

North America Automotive Exhaust Shield Market Insight

North America dominated the automotive exhaust shield market with the largest revenue share of 37.8% in 2025, supported by strong automotive production, high adoption of advanced thermal management technologies, and stringent vehicle safety and emission regulations. The region benefits from a well-established automotive manufacturing base, particularly in the U.S. and Mexico, where OEMs are increasingly integrating advanced exhaust shielding systems to improve vehicle performance and passenger safety. Rising demand for high-performance SUVs, pickup trucks, and commercial vehicles is further accelerating the adoption of durable heat shield solutions designed to withstand high exhaust temperatures and extended operating cycles.

U.S. Automotive Exhaust Shield Market Insight

The U.S. automotive exhaust shield market captured the largest revenue share of approximately 29.5% in 2025 within North America, driven by high vehicle production volumes, strong presence of leading automotive OEMs, and increasing demand for advanced thermal insulation systems in both passenger and commercial vehicles. Consumers and manufacturers are prioritizing vehicle safety, fuel efficiency, and emission compliance, leading to widespread integration of multi-layer exhaust shielding systems. The growing adoption of turbocharged engines and hybrid powertrains is further boosting demand for high-temperature resistant shielding materials across automotive platforms.

Europe Automotive Exhaust Shield Market Insight

The Europe automotive exhaust shield market is expected to witness the fastest growth rate of 3.1% CAGR from 2026 to 2033, primarily driven by strict emission regulations such as Euro 6 and upcoming Euro 7 standards, along with increasing demand for lightweight and fuel-efficient vehicles. The region’s strong focus on sustainability and carbon reduction is encouraging automakers to adopt advanced thermal shielding materials such as ceramic composites and aluminum-based multilayer systems. Rising electric and hybrid vehicle penetration across Germany, France, and Italy is further supporting market expansion across both OEM and aftermarket segments.

U.K. Automotive Exhaust Shield Market Insight

The U.K. automotive exhaust shield market is expected to witness steady growth from 2026 to 2033, driven by increasing adoption of hybrid vehicles and stringent vehicle safety standards focused on thermal protection and emission control. Growing consumer awareness regarding vehicle efficiency and safety is encouraging OEMs to integrate advanced exhaust shielding solutions in both new vehicle models and aftermarket upgrades. The expansion of premium and performance vehicle segments is also contributing to rising demand for high-performance thermal insulation systems.

Germany Automotive Exhaust Shield Market Insight

The Germany automotive exhaust shield market is expected to witness strong growth from 2026 to 2033, supported by the country’s advanced automotive engineering ecosystem and strong emphasis on precision manufacturing and sustainability. Leading German automakers are increasingly adopting lightweight and high-durability exhaust shielding systems to improve thermal efficiency and comply with strict environmental regulations. The integration of advanced shielding materials in luxury and performance vehicles is further enhancing market demand, particularly in turbocharged and hybrid vehicle platforms.

Asia-Pacific Automotive Exhaust Shield Market Insight

The Asia-Pacific automotive exhaust shield market is expected to witness the fastest growth rate of 3.8% CAGR from 2026 to 2033, supported by rapid urbanization, rising vehicle production, and increasing demand for affordable passenger and commercial vehicles. Countries such as China, India, Japan, and South Korea are witnessing strong expansion in automotive manufacturing, driving large-scale adoption of cost-effective and efficient exhaust shielding systems. Government initiatives promoting emission reduction and fuel efficiency are further accelerating market growth across both OEM and aftermarket channels.

Japan Automotive Exhaust Shield Market Insight

The Japan automotive exhaust shield market is expected to witness steady growth from 2026 to 2033, driven by the country’s strong automotive innovation ecosystem and high adoption of hybrid and fuel-efficient vehicles. Japanese automakers are increasingly integrating advanced thermal shielding technologies to improve engine efficiency, reduce emissions, and enhance passenger safety. Rising demand for compact vehicles with optimized thermal management systems is further supporting market expansion, particularly in urban mobility applications.

China Automotive Exhaust Shield Market Insight

The China automotive exhaust shield market accounted for the largest revenue share of approximately 48.6% in Asia Pacific in 2025, attributed to rapid automotive production growth, expanding middle-class vehicle ownership, and strong presence of domestic automotive manufacturers. The country’s aggressive push toward emission control standards and new energy vehicle adoption is driving increased integration of advanced exhaust shielding systems. Expanding production of passenger cars, electric hybrids, and commercial fleets is further strengthening demand for cost-efficient and high-performance thermal shielding solutions across the automotive sector.

Automotive Exhaust Shield Market Share

The Automotive Exhaust Shield industry is primarily led by well-established companies, including:

• Morgan Advanced Materials (U.K.)

• Dana Limited (U.S.)

• Tenneco Inc. (U.S.)

• Autoneum (Switzerland)

• Lydall, Inc. (U.S.)

• ElringKlinger AG (Germany)

• Progress-Werk Oberkirch AG (Germany)

• UGN (U.S.)

• Zircotec (U.K.)

• HAPPICH GmbH (Germany)

• Isolite Insulating Products Co., Ltd. (Japan)

• HKO (Germany)

• Heatshield Products, Inc. (U.S.)

• ACS Industries, Inc. (U.S.)

• J&S GmbH Automotive Technology (Germany)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.