Global Automotive Finance Market

Market Size in USD Billion

USD

332.50 Billion

USD

582.06 Billion

2025

2033

USD

332.50 Billion

USD

582.06 Billion

2025

2033

| 2026 - 2033 | |

| USD 332.50 Billion | |

| USD 582.06 Billion | |

| % | |

|

Automotive Finance Market Overview

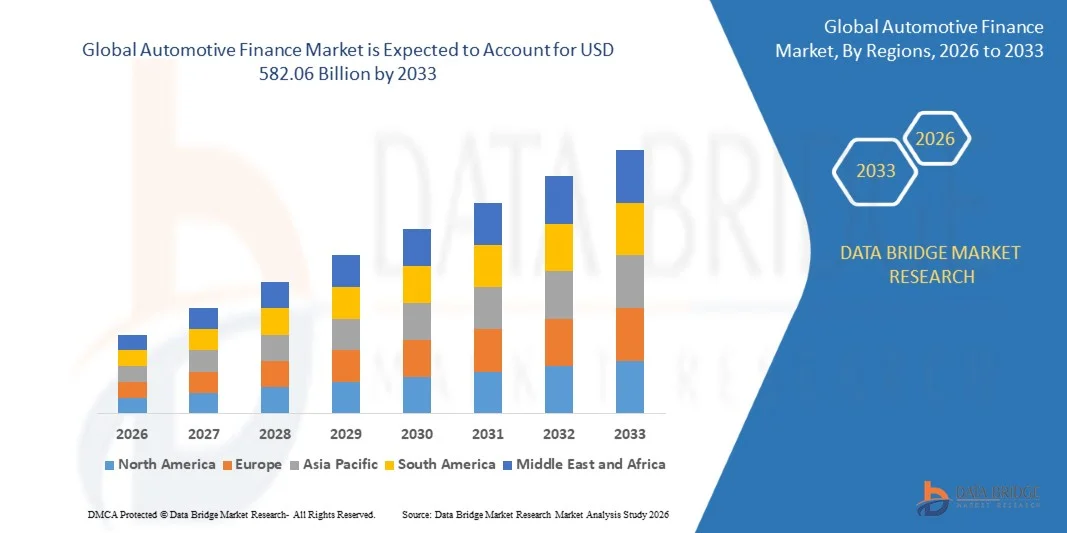

As per Data Bridge Market Research Analysis the automotive finance market was valued at USD 332.5 billion in 2025 and is projected to reach USD 582.06 billion by 2033, growing at a CAGR of 7.25% from 2026 to 2033. The market is experiencing robust growth driven by increasing vehicle sales, rising consumer demand for affordable payment solutions, and the expansion of digital lending platforms.

Automotive finance encompasses a broad spectrum of credit and leasing products designed to facilitate vehicle purchases across new and used segments. The market includes traditional banks, captive finance arms of original equipment manufacturers (OEMs), Innovations such as electric vehicles (EVs) and subscription-based ownership models are reshaping the market structure, creating demand for sustainable practices and advanced technology integration. Traditional bank financing is increasingly complemented by OEM-sponsored programs and fintech solutions that simplify the application process. The industry's future hinges on flexible strategies capable of navigating evolving customer preferences while effectively mitigating financing risks and market volatility.

Market Size & Forecast

- Global Market Value (2025): USD 332.5 Billion

- Expected Market Value (2033): USD 582.06 Billion

- Forecast CAGR (2026–2033): 7.25%

- Leading Region in 2025: Europe

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- Europe dominated the global automotive finance market in 2024, accounting for a 39.3% share of global revenue, supported by strong captive finance penetration from German OEMs and well-established dealer-linked lending networks.

- Asia-Pacific is expected to emerge as the fastest-growing regional market over the forecast period, driven by rising vehicle ownership, rapid motorization in China and India, and expanding digital finance access. The region accounts for roughly half of the used car financing market.

- The banks segment led the provider type category and accounted for a 57.5% share of global revenue in 2024, driven by their extensive reach, established financial infrastructure, and competitive lending rates.

- The direct distribution channel dominated the market in 2024, capturing a significant share of global revenue, as consumers increasingly prefer direct engagement with lenders for transparency and convenience.

- The loan segment generated the maximum revenue share of more than 60% in 2025 by purpose type, while the leasing segment is projected to record the largest growth from 2026 to 2035.

- Passenger vehicles captured a substantial share of the automotive finance market in 2025, with commercial vehicles projected to grow at a significant CAGR through 2031.

- Digital transformation is revolutionizing the automotive finance sector, with financial institutions adopting AI-driven credit scoring, automated loan processing, and mobile payment applications to enhance service quality and reduce customer wait times.

Report Scope and Automotive Finance Market Segmentation

|

Attributes |

Automotive Finance Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Finance Market Trends

Trend: Rising Used-Car Transactions Creating New Lending Volume

The used-car financing segment is emerging as a significant growth driver for the automotive finance market. Certified pre-owned (CPO) programs are reshaping consumer perceptions of second-hand vehicles, enabling lenders to offer loan-to-value ratios and rates closer to those on new cars. In Europe, used-vehicle financing accounted for 37.14% of the European automotive financing market in 2025 and is projected to expand at a 7.05% CAGR through 2031 (Source: Mordor Intelligence). According to Eurofinas, 16% of new consumer finance in Europe supported used car lending in the first half of 2025.

As used-car marketplaces integrate instant finance offers, origination conversion improves because consumers can lock rates before visiting a dealership, thereby shortening the sales funnel and reducing loan abandonment rates. Experts predict the used-car financing and leasing sector could grow at a CAGR of 15% from 2023 to 2030.

Automotive Finance Market Dynamics

Key Market Driver: Digital Transformation and AI-Enabled Lending

Technological advancements in digital finance tools and AI-driven credit models are driving market growth and improving accessibility for consumers worldwide. AI technology is increasingly being used in the automotive finance sector to improve the credit underwriting process, analyze data to predict delinquencies, and enhance the approval process. According to the Federal Reserve Bank of New York, auto loan balances reachedUSD1.69 trillion in Q1 2026.

Fintech platforms are leveraging AI-driven credit assessment to offer faster, more convenient financing solutions. Pagaya Technologies signed aUSD500 million forward flow agreement with Castlelake in 2025 to sell auto loans originated through its AI-driven lending platform. Digital origination platforms enable faster, more efficient loan processing, reducing costs and improving customer experience. Embedded finance integration with OEM e-commerce platforms allows captive finance arms to offer seamless financing options directly within the vehicle purchase journey.

Key Restraint/Challenge: Rising Interest Rates and Net-Interest Margin Compression

A significant challenge facing the automotive finance market is the impact of rising interest rates. As central banks tighten monetary policy, borrowing costs increase, potentially deterring some customers from financing or leasing vehicles. Commercial banks' 60-month and 72-month car loan rates remained at 7.52% and 7.55% in January and February 2026, up from 7.22% and 7.5% at the end of 2025. Auto loan rejection rates have increased as lenders tighten credit standards in response to economic uncertainty.

Policy rates in the United States remained in a 4.25-4.5% corridor as of May 2025. The higher funding cost has squeezed lender spreads; new-auto loan balances at banks fell 3.4% in 2024. In Europe, the European Central Bank has maintained an easing cycle, lowering policy rates by 200 basis points cumulatively between June 2024 and June 2025. However, the lagged pass-through of ECB rate cuts is dampening net-interest income, forcing originators to introduce tiered-rate structures that pass risk costs to lower-quality borrowers.

Key Market Opportunity: EV Financing and Battery Leasing Solutions

The rapid growth of electric vehicle adoption creates opportunities for specialized financing products. Financial institutions can develop tailored EV financing solutions, including battery leasing, which separates the cost of the battery from the vehicle itself. The combination of financing with value-added mobility services, such as subscription packages and battery leasing, is becoming a decisive competitive lever.

EV financing experienced a significant rise, reaching 25.35% in Q2 2024. As EV adoption continues to accelerate, the demand for specialized financing products that address the unique needs of EV buyers—including battery degradation concerns, charging infrastructure costs, and resale value uncertainty—is expected to grow substantially.

Automotive Finance Market Scope

The Automotive Finance market is segmented on the basis of provider type, finance type, vehicle type, purpose type, and distribution channel.

- By Provider Type

On the basis of provider type, the global automotive finance market is segmented into banks, OEMs/captive finance, fintech and other non-traditional providers. The banks segment led the market in 2024, accounting for a 57.5% share of global revenue. Banks benefit from established infrastructure, extensive branch networks, and strong capital reserves that enable them to offer competitive rates and terms. OEMs/captive finance providers are gaining market share, supported by manufacturer-backed financing incentives that allow them to absorb rate pressure and sustain showroom traffic. Fintech and other non-traditional providers are emerging as significant competitors, leveraging digital platforms and AI-driven credit assessment to offer faster, more convenient financing solutions. Companies such as Ford Credit, Toyota Financial Services, and Volkswagen Financial Services have expanded promotional financing programs to maintain vehicle affordability in the face of rising interest rates.

- By Finance Type

On the basis of finance type, the global automotive finance market is segmented into loan and leasing. The loan segment dominated the market in 2024, accounting for a significant share of global revenue. Loans remain the most common form of automotive finance, with consumers and businesses using them to purchase new and used vehicles. Leasing is gaining popularity, particularly among consumers who prefer lower monthly payments and the ability to switch vehicles more frequently. Flexible financing solutions such as balloon loans, deferred payments, and subscription services have emerged to cater to diverse customer needs. The growth of leasing and flexible financing options is driven by changing consumer preferences for mobility over ownership, particularly among younger demographics and urban dwellers.

- By Purpose Type

On the basis of purpose type, the global automotive finance market is segmented into new vehicles and used vehicles. Used vehicles accounted for a significant portion of the market in 2025, growing at a rapid pace. In Europe, used-vehicle financing accounted for 37.14% of the European automotive financing market in 2025. New vehicle financing remains significant, driven by rising vehicle prices and consumer preference for the latest models. The growth of certified pre-owned programs is boosting used vehicle financing by improving consumer confidence and enabling lenders to offer more competitive rates. The increasing adoption of electric vehicles is expected to drive growth in both new and used vehicle financing, as these vehicles often require larger loan amounts and specialized financing products.

- By End User

On the basis of distribution channel, the global automotive finance market is segmented into direct and indirect. Direct financing involves consumers securing loans directly from banks, credit unions, or online lenders. Indirect financing involves dealerships acting as intermediaries, connecting consumers with lenders and facilitating the financing process. Digital origination platforms are transforming both channels by enabling faster, more efficient loan processing. Digital origination platforms are transforming both channels by enabling faster, more efficient loan processing, reducing costs, and improving customer experience.

Automotive Finance Market Regional Analysis

Europe Automotive Finance Market Insight

Europe maintained a significant position in the global automotive finance market in 2025, supported by strong captive finance penetration from German OEMs, mature leasing markets in countries such as the U.K. and France, and advanced digital lending infrastructure. According to Grand View Research, Europe dominated the global automotive finance market in 2024, accounting for a 39.3% share of global revenue, with Germany holding a substantial market share. The Germany automotive finance market held a substantial market share in 2024, driven by strong captive finance penetration from German OEMs including Volkswagen Financial Services, BMW Financial Services, and Mercedes-Benz Financial Services. In the UK, Finance and Leasing Association (FLA) members provided £163 billion of new lending in 2025, financing over 85% of private new car registrations.

North America Automotive Finance Market Insight

North America commanded a significant share of the automotive finance market in 2025. The U.S. automotive finance market is estimated at approximately USD 64.7 billion in 2025. Auto loan balances grew by USD 18 billion in Q1 2026 to reach USD 1.69 trillion, according to the Federal Reserve Bank of New York. There wereUSD181 billion in new auto loans appearing on credit reports in Q4 2025. Auto loans constitute the second-largest consumer credit market after mortgages, with 108 million outstanding loans totaling USD 1.67 trillion as of the end of 2025.

The region's strong industrial infrastructure and widespread use of automotive finance across consumer and commercial applications drive market growth. Digitized contracting volumes among dealers and lenders in North America surged year-on-year in 2024. For full-year 2025, the Dealertrack Credit Availability Index averaged 97.3, a 3.6% year-over-year gain from 2024's average of 93.9. However, rising interest rates (commercial bank 60-month car loan rates at 7.52% as of February 2026) and auto loan delinquencies (90-day-or-more reaching 5.60% in Q1 2026) are challenging lenders.

Asia-Pacific Automotive Finance Market Insight

Asia-Pacific is expected to emerge as the fastest-growing regional market over the forecast period. The region's rapid growth is fueled by rapid industrialization, increasing vehicle ownership, rising disposable incomes, and growing adoption of digital finance platforms. China, the world's second largest economy, is forecast to reach a projected market size of US$76.8 billion by 2032, trailing a CAGR of 9.8% over the analysis period 2025-2032. India is expected to register the highest CAGR from 2025 to 2030.Global vehicle sales climbed from 95.3 million units in 2024 to 99.8 million in 2025 (+4.7%), with Asia, Oceania and the Middle East increasing by 7.1% in 2025 to 55.02 million units. The region's expanding middle class and growing demand for personal and commercial vehicles are driving automotive finance growth. The proliferation of digital lending platforms and aggressive marketing campaigns by both global and local financial institutions have further fueled adoption. In India, Maruti Suzuki Smart Finance has disbursed loans worth more than ₹1,70,000 crore since its launch, demonstrating the scale of digital auto financing in the region.

South America Automotive Finance Market Insight

South America represents an emerging market for automotive finance, with growing demand influenced by increasing vehicle ownership, rising disposable incomes, and expanding banking infrastructure. Countries such as Brazil and Mexico are witnessing significant investments in automotive financing, supported by policies promoting vehicle ownership and consumer credit. The region's expanding middle class and growing awareness of financing options are creating opportunities for automotive finance providers. However, market growth is currently constrained by high interest rates, economic volatility, and fragmented regulatory frameworks. The Middle East and Africa region represents a nascent market for automotive finance, with demand primarily concentrated in the GCC countries and South Africa. Governments across the region are increasing investments in financial infrastructure and technology sectors to diversify their economies. The UAE and Saudi Arabia are investing in fintech innovation and digital transformation programs, creating opportunities for automotive finance applications in retail and consumer lending. However, relatively low adoption of formal automotive financing, limited credit infrastructure, and high costs continue to restrain market growth.

Automotive Finance Market Share

The automotive finance industry is primarily led by well-established companies, including:

- Ally Financial Inc. (U.S.)

- Bank of America Corporation (U.S.)

- Capital One Financial Corporation (U.S.)

- Chase Auto Finance (U.S.)

- Ford Motor Credit Company (U.S.)

- General Motors Financial Company Inc. (U.S.)

- Toyota Financial Services (Japan)

- Volkswagen Financial Services (Germany)

- BMW Financial Services (Germany)

- Mercedes-Benz Financial Services (Germany)

- Hyundai Capital (South Korea)

- Honda Financial Services (Japan)

- Nissan Motor Acceptance Corporation (Japan)

- BNP Paribas (France)

- Banco Santander S.A. (Spain)

- Wells Fargo & Company (U.S.)

- Hitachi Capital Corporation (Japan)

- Tata Motors Finance (India)

- Shriram Finance (India)

- Bajaj Finance (India)

Latest Developments in Automotive Finance Market

- In January 2026, Metro Bank Plc., a UK-based retail banking institution, expanded its digital car loan product under the RateSetter brand. These digital loans are structured as hire purchase agreements for used vehicles and are currently available through motor brokers utilizing advanced RateSetter technology. A key differentiator of this offering is the automated, real-time decision-making process that generates customized loan quotes for individual customers. This approach enables a paperless application journey, allowing eligible borrowers to receive instant approvals and take delivery of their vehicles on the same day.

- In May 2026, the Federal Reserve Bank of New York reported that auto loan balances grew byUSD18 billion in Q1 2026 to reachUSD1.69 trillion, while 90-day-or-more auto loan delinquencies reached 5.60%. This data highlights the dual trends of market expansion and rising credit risk.

- In November 2025, Pagaya Technologies, a consumer credit fintech, signed aUSD500 million forward flow agreement with Castlelake to sell auto loans originated through its AI-driven lending platform, expanding its auto financing and asset-backed securities (ABS) programs. This followed aUSD2.5 billion personal loan deal between the two firms in July 2025.

- In June 2025, Arra Finance LLC, a US-based subprime auto finance provider, acquired the auto finance division of Crescent Bank for an undisclosed amount. Through this acquisition, Arra Finance sought to substantially expand its auto loan origination capacity and dealer network, while integrating Crescent Bank's servicing infrastructure and technology platform to accelerate credit application decision-making.

- In 2025, Ford Credit reported full-year earnings before taxes (EBT) ofUSD2.6 billion, up 55% year-over-year. BMW Financial Services' share of new BMW Group vehicles either leased or credit financed increased by 3.8 percentage points to 44.4% in Q2 2025.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.