Global Automotive Fuel Pump Market

Market Size in USD Billion

USD

13.00 Billion

USD

19.80 Billion

2025

2033

USD

13.00 Billion

USD

19.80 Billion

2025

2033

| 2026 - 2033 | |

| USD 13.00 Billion | |

| USD 19.80 Billion | |

| % | |

|

Automotive Fuel Pump Market Overview

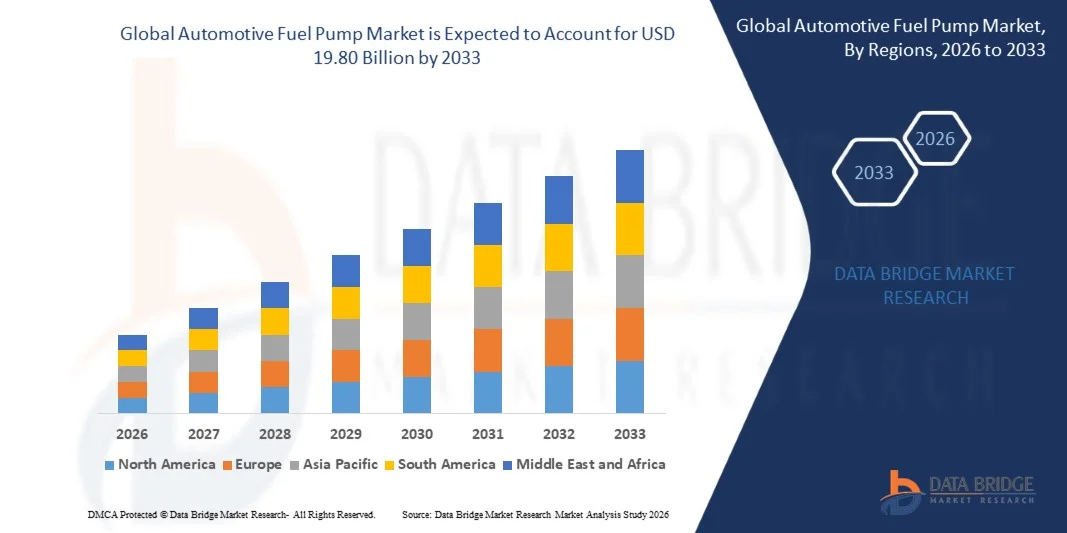

The Automotive Fuel Pump Market was valued at USD 13.00 billion in 2025 and is projected to reach USD 19.80 billion by 2033, growing at a CAGR of 5.40% from 2026 to 2033. The market is witnessing steady growth driven by increasing global vehicle production, rising demand for fuel-efficient automotive systems, and the continued expansion of passenger and commercial vehicle fleets across emerging and developed economies. Advancements in fuel injection technologies and the growing adoption of high-performance fuel delivery systems are further supporting market expansion.

The growing emphasis on vehicle efficiency, emission reduction, and engine performance is encouraging automakers to integrate advanced fuel pump technologies capable of delivering precise fuel flow and pressure. Stringent environmental regulations and fuel economy standards across major automotive markets are accelerating the replacement of conventional fuel systems with more efficient electric fuel pumps. In addition, the expanding aftermarket for automotive components and increasing vehicle parc worldwide are creating sustained demand for fuel pump replacement and maintenance, contributing to long-term market growth.

Key Market Trends & Insights

- North America dominated the automotive fuel pump market with the largest revenue share of 34.6% in 2025, supported by high vehicle ownership rates, strong presence of leading automotive OEMs, and widespread adoption of advanced fuel injection technologies. The region benefits from a mature automotive industry, high demand for pickup trucks and SUVs, and continuous technological upgrades in fuel delivery systems.

- Asia-Pacific automotive fuel pump market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, increasing vehicle production, and rising demand for passenger and commercial vehicles in countries such as China, India, Japan, and South Korea.

- The HEV segment held the largest market revenue share of approximately 46.2% in 2025 driven by strong global hybrid adoption as automakers continue to use internal combustion engines alongside electric drivetrains for improved fuel efficiency and reduced emissions. Hybrid models from manufacturers such as Toyota and Honda continue to rely heavily on advanced electric fuel pumps for optimized fuel delivery during engine activation phases.

- The PHEV segment is projected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by increasing consumer preference for extended driving range combined with lower fuel consumption. Rising PHEV adoption in Europe and China, along with expanding model availability from OEMs such as BMW and BYD, is accelerating demand for high-pressure fuel pump systems integrated with dual powertrain architectures.

- The passenger cars segment held the largest market revenue share of approximately 58.5% in 2025 driven by high global production volumes and increasing adoption of advanced fuel injection systems in compact, mid-size, and premium vehicle categories. Strong demand in Asia-Pacific, particularly in India and China, continues to support segment dominance.

- The light commercial vehicles segment is projected to register the fastest growth at a CAGR of 6.6% from 2026 to 2033, driven by expanding logistics, e-commerce delivery networks, and urban transportation fleets requiring efficient and durable fuel delivery systems. Growth in last-mile delivery services is further increasing adoption of high-performance electric fuel pumps for improved engine reliability and fuel economy.

- The electric segment held the largest market revenue share of approximately 67.9% in 2025 driven by widespread adoption of in-tank electric fuel pumps in modern fuel injection systems, including gasoline direct injection (GDI) and hybrid vehicles. Electric pumps offer precise fuel control, higher efficiency, and compatibility with advanced emission standards such as BS-VI and Euro 6.

- The electric segment is also projected to register the fastest growth at a CAGR of 5.9% from 2026 to 2033, driven by increasing electrification of fuel systems in hybrid vehicles and rising demand for electronically controlled fuel delivery in turbocharged engines. Continuous innovation in compact, high-pressure pump designs is further supporting segment expansion.

- The fixed displacement segment held the largest market revenue share of approximately 54.3% in 2025 driven by its extensive use in conventional internal combustion engine vehicles due to lower cost, simpler design, and reliable fuel delivery performance across standard driving conditions.

- The variable displacement segment is projected to register the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by increasing demand for fuel-efficient systems capable of adjusting fuel flow based on engine load and driving conditions. Growing adoption in hybrid and performance vehicles is further supporting segment expansion due to improved efficiency and reduced energy loss.

- The construction equipment segment held the largest market revenue share of approximately 61.7% in 2025 driven by high usage of fuel-powered machinery such as excavators, loaders, and bulldozers across infrastructure development projects globally. Rising urbanization and large-scale construction activities in Asia-Pacific are further supporting demand for durable fuel pump systems.

- The mining equipment segment is projected to register the fastest growth at a CAGR of 6.4% from 2026 to 2033, driven by increasing mining exploration activities and rising demand for high-performance fuel systems in heavy-duty equipment operating under extreme conditions. Expansion of mineral extraction projects in Latin America and Africa is further accelerating segment growth.

Market Size & Forecast

- Global Market Value (2025): USD 13.00 Billion

- Expected Market Value (2033): USD 19.80 Billion

- Forecast CAGR (2026–2033): 5.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Automotive Fuel Pump Market Segmentation

|

Attributes |

Automotive Fuel Pump Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Continental AG (Germany) |

|

Market Opportunities |

• Growing Adoption Of Advanced Fuel Injection Systems • Rising Demand For Fuel-Efficient And Low-Emission Vehicles |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Fuel Pump Market Trends

Trend: Growth In Electrification Of Fuel Delivery Systems And High-Pressure Direct Injection Technologies

The automotive fuel pump market is witnessing a strong shift toward electronically controlled, high-pressure, and smart fuel delivery systems driven by increasing demand for fuel efficiency and stringent emission regulations across global automotive markets. Traditional mechanical pumps are being rapidly replaced by electric in-tank and high-pressure fuel pumps that support advanced engine architectures such as gasoline direct injection (GDI), turbocharged engines, and hybrid powertrains, enabling precise fuel metering and improved combustion efficiency.

In modern vehicle platforms, automakers are increasingly integrating high-pressure fuel pump systems, for instance in GDI engines used by major OEMs such as Hyundai and Ford, to achieve better atomization of fuel and enhanced thermal efficiency under varying driving conditions. Hybrid vehicles are also adopting dual-mode fuel pump systems that optimize fuel supply during engine start-stop cycles to reduce wastage and improve overall drivetrain responsiveness.

The expansion of hybrid and downsized engine technologies is further increasing demand for compact, variable-speed electric fuel pumps capable of maintaining stable pressure across diverse operating loads. Industry testing and benchmarking in 2025 indicate that advanced high-pressure fuel pump systems can improve combustion efficiency by approximately 10–15% compared to conventional port fuel injection systems, contributing to measurable reductions in fuel consumption and CO₂ emissions across real-world driving cycles

Automotive Fuel Pump Market Dynamics

Key Market Driver: Rising Vehicle Production And Strict Emission And Fuel Efficiency Regulations

The Automotive Fuel Pump Market is primarily driven by rising vehicle production across emerging and developed economies, combined with increasingly strict emission norms and fuel economy standards imposed by regulatory bodies worldwide. Growing passenger vehicle demand in Asia-Pacific and increasing commercial fleet expansion in logistics and transportation sectors are further strengthening the requirement for efficient fuel delivery systems that enhance engine performance and reduce fuel consumption.

Governments across major automotive markets are enforcing stricter emission frameworks such as Euro 6 in Europe and BS-VI in India, compelling OEMs to adopt advanced fuel injection and high-efficiency fuel pump technologies. For instance, automakers are integrating electronically controlled fuel pumps in new-generation BS-VI compliant vehicles to achieve optimized air-fuel ratios and lower particulate emissions. In addition, the global shift toward hybrid powertrains is increasing reliance on precision fuel delivery systems that support intermittent engine operation and improved thermal efficiency.

Industry data indicates that global vehicle production surpassed 90 million units in recent years, with a significant share increasingly adopting electronically controlled fuel systems, highlighting sustained demand for advanced fuel pump components across OEM and aftermarket segments

Key Restraint/Challenge: Rising Electrification Of Vehicles And Declining Internal Combustion Engine Dependency

The automotive fuel pump market faces significant challenges from the rapid global transition toward electric vehicles, which do not require traditional fuel delivery systems, thereby limiting long-term demand growth for fuel pumps in fully electric segments. Increasing EV adoption across China, Europe, and North America is gradually reducing the share of internal combustion engine (ICE) vehicles in overall production volumes, directly impacting future market expansion potential.

In addition, hybrid vehicle platforms, while still utilizing fuel pumps, are designed for reduced engine runtime and lower fuel consumption, which can decrease component wear and replacement frequency compared to conventional ICE vehicles. This shift is gradually affecting aftermarket demand cycles for fuel pump replacement and maintenance services.

Industry transition trends show that EV sales accounted for over 14 million units globally in 2024, reflecting a strong year-on-year increase, which is expected to continue reshaping automotive component demand structures and limiting long-term dependency on traditional fuel pump systems

Key Market Opportunity: Growth In High-Performance Hybrid Vehicles And Advanced Aftermarket Replacement Demand

Despite electrification trends, significant opportunities remain in hybrid vehicle expansion, high-performance ICE applications, and the growing global automotive aftermarket. Hybrid electric vehicles continue to rely on fuel pumps for internal combustion support systems, creating sustained demand for advanced electric and high-pressure fuel pump technologies designed for efficiency and durability under variable operating conditions.

Automakers are increasingly adopting advanced fuel pump modules, for instance in plug-in hybrid electric vehicles (PHEVs) used by Toyota and BMW, to optimize fuel efficiency during engine engagement phases while maintaining smooth power delivery and emission compliance. In addition, performance and luxury vehicle segments continue to demand high-pressure fuel systems capable of supporting turbocharged and direct injection engines for enhanced driving dynamics.

The expanding global vehicle parc is also driving strong aftermarket replacement demand, particularly in regions with aging vehicle fleets such as Asia-Pacific and Latin America. Industry estimates suggest that fuel system components, including fuel pumps, typically require replacement after 100,000–150,000 kilometers depending on operating conditions, creating recurring revenue opportunities across independent repair and service networks worldwide

Automotive Fuel Pump Market Scope

The market is segmented on the basis of electric vehicle type, vehicle type, technology, displacement, and off-highway vehicles.

• By Electric Vehicle Type

On the basis of electric vehicle type, the automotive fuel pump market is segmented into BEV, FCEV, HEV, and PHEV. The HEV segment held the largest market revenue share of approximately 46.2% in 2025 driven by strong global hybrid adoption as automakers continue to use internal combustion engines alongside electric drivetrains for improved fuel efficiency and reduced emissions. Hybrid models from manufacturers such as Toyota and Honda continue to rely heavily on advanced electric fuel pumps for optimized fuel delivery during engine activation phases.

The PHEV segment is projected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by increasing consumer preference for extended driving range combined with lower fuel consumption. Rising PHEV adoption in Europe and China, along with expanding model availability from OEMs such as BMW and BYD, is accelerating demand for high-pressure fuel pump systems integrated with dual powertrain architectures.

• By Vehicle Type

On the basis of vehicle type, the market is segmented into passenger cars, light commercial vehicles, and heavy commercial vehicles. The passenger cars segment held the largest market revenue share of approximately 58.5% in 2025 driven by high global production volumes and increasing adoption of advanced fuel injection systems in compact, mid-size, and premium vehicle categories. Strong demand in Asia-Pacific, particularly in India and China, continues to support segment dominance.

The light commercial vehicles segment is projected to register the fastest growth at a CAGR of 6.6% from 2026 to 2033, driven by expanding logistics, e-commerce delivery networks, and urban transportation fleets requiring efficient and durable fuel delivery systems. Growth in last-mile delivery services is further increasing adoption of high-performance electric fuel pumps for improved engine reliability and fuel economy.

• By Technology

On the basis of technology, the market is segmented into electric and mechanical fuel pumps. The electric segment held the largest market revenue share of approximately 67.9% in 2025 driven by widespread adoption of in-tank electric fuel pumps in modern fuel injection systems, including gasoline direct injection (GDI) and hybrid vehicles. Electric pumps offer precise fuel control, higher efficiency, and compatibility with advanced emission standards such as BS-VI and Euro 6.

The electric segment is also projected to register the fastest growth at a CAGR of 5.9% from 2026 to 2033, driven by increasing electrification of fuel systems in hybrid vehicles and rising demand for electronically controlled fuel delivery in turbocharged engines. Continuous innovation in compact, high-pressure pump designs is further supporting segment expansion.

• By Displacement

On the basis of displacement, the market is segmented into variable displacement and fixed displacement. The fixed displacement segment held the largest market revenue share of approximately 54.3% in 2025 driven by its extensive use in conventional internal combustion engine vehicles due to lower cost, simpler design, and reliable fuel delivery performance across standard driving conditions.

The variable displacement segment is projected to register the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by increasing demand for fuel-efficient systems capable of adjusting fuel flow based on engine load and driving conditions. Growing adoption in hybrid and performance vehicles is further supporting segment expansion due to improved efficiency and reduced energy loss.

• By Off High-Way Vehicles

On the basis of off-highway vehicles, the market is segmented into construction equipment and mining equipment. The construction equipment segment held the largest market revenue share of approximately 61.7% in 2025 driven by high usage of fuel-powered machinery such as excavators, loaders, and bulldozers across infrastructure development projects globally. Rising urbanization and large-scale construction activities in Asia-Pacific are further supporting demand for durable fuel pump systems.

The mining equipment segment is projected to register the fastest growth at a CAGR of 6.4% from 2026 to 2033, driven by increasing mining exploration activities and rising demand for high-performance fuel systems in heavy-duty equipment operating under extreme conditions. Expansion of mineral extraction projects in Latin America and Africa is further accelerating segment growth.

Automotive Fuel Pump Market Regional Analysis

North America Automotive Fuel Pump Market Insight

North America dominated the automotive fuel pump market with the largest revenue share of 34.6% in 2025, supported by high vehicle ownership rates, strong presence of leading automotive OEMs, and widespread adoption of advanced fuel injection technologies. The region benefits from a mature automotive industry, high demand for pickup trucks and SUVs, and continuous technological upgrades in fuel delivery systems. Consumers and manufacturers in the region prioritize performance, fuel efficiency, and compliance with stringent emission standards, driving the adoption of high-pressure electric fuel pumps and advanced fuel system modules across passenger and commercial vehicles.

U.S. Automotive Fuel Pump Market Insight

The U.S. automotive fuel pump market captured the largest revenue share in 2025 within North America, driven by strong automotive production, high demand for light trucks, and rapid integration of gasoline direct injection (GDI) and hybrid powertrains. Automakers such as Ford and General Motors are increasingly deploying advanced electric fuel pump systems to improve combustion efficiency and meet regulatory requirements under EPA emission standards. The rising adoption of hybrid vehicles and increasing replacement demand across the aftermarket segment further strengthen market expansion.

Europe Automotive Fuel Pump Market Insight

The Europe automotive fuel pump market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by strict emission regulations such as Euro 6 and upcoming Euro 7 standards, which are pushing automakers toward high-efficiency fuel injection systems. The region is experiencing strong demand for hybrid vehicles, especially in countries such as Germany, France, and Italy, where automotive innovation and sustainability initiatives are highly prioritized. Increasing adoption of advanced electric fuel pumps in downsized turbocharged engines is further accelerating market growth across both OEM and aftermarket channels.

U.K. Automotive Fuel Pump Market Insight

The U.K. automotive fuel pump market is expected to witness steady growth from 2026 to 2033, driven by rising adoption of hybrid vehicles and increasing focus on reducing vehicular emissions. Growing demand for fuel-efficient passenger cars and the expansion of fleet-based transportation services are encouraging the use of advanced electric fuel pump systems. In addition, strong aftermarket demand for fuel system replacement parts, supported by an aging vehicle fleet, is contributing to sustained market growth across the country.

Germany Automotive Fuel Pump Market Insight

The Germany automotive fuel pump market is expected to witness strong growth from 2026 to 2033, fueled by the country’s leadership in automotive engineering, high adoption of hybrid powertrains, and strong presence of premium OEMs such as Volkswagen, BMW, and Mercedes-Benz. Germany’s focus on fuel efficiency and precision engineering is driving demand for high-performance fuel pumps used in direct injection and turbocharged engines. The integration of advanced fuel delivery systems in luxury and performance vehicles is further supporting market expansion.

Asia-Pacific Automotive Fuel Pump Market Insight

The Asia-Pacific automotive fuel pump market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, increasing vehicle production, and rising demand for passenger and commercial vehicles in countries such as China, India, Japan, and South Korea. The region serves as a major automotive manufacturing hub, with expanding OEM production capacity and strong adoption of cost-effective electric fuel pump systems. Government initiatives promoting fuel efficiency and emission reduction are further accelerating market penetration across both ICE and hybrid vehicle segments.

Japan Automotive Fuel Pump Market Insight

The Japan automotive fuel pump market is expected to witness steady growth from 2026 to 2033 due to the country’s strong automotive technology base, high adoption of hybrid vehicles, and focus on fuel efficiency and reliability. Leading automakers such as Toyota and Honda continue to integrate advanced fuel pump systems in hybrid platforms to optimize fuel consumption and emissions performance. Japan’s emphasis on compact, high-efficiency automotive components is also driving demand for precision-engineered fuel delivery systems in both domestic and export markets.

China Automotive Fuel Pump Market Insight

The China automotive fuel pump market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to high vehicle production volumes, rapid expansion of the middle-class population, and strong domestic automotive manufacturing capabilities. China is one of the largest automotive markets globally, with significant adoption of passenger cars, hybrid vehicles, and commercial fleets requiring advanced fuel pump systems. The growing presence of local OEMs such as BYD and Geely, along with government support for emission reduction technologies, is further driving demand for efficient electric fuel pump solutions across the country.

Automotive Fuel Pump Market Share

The Automotive Fuel Pump industry is primarily led by well-established companies, including:

• Continental AG (Germany)

• DENSO CORPORATION (Japan)

• Delphi Auto Parts (U.S.)

• Robert Bosch Ltd (Germany)

• Hitachi Automotive Systems, Ltd. (Japan)

• Infineon Technologies AG (Germany)

• Perkins Engines Company Limited (U.K.)

• industrydiesel.com (U.S.)

• Arkansas Fuel Injection, Inc. (U.S.)

• Sagar Fuel (India)

• Shiyan QiJing Industry & Trading Co., Ltd. (China)

• DeatschWerks, LLC. (U.S.)

• Johnson Electric Holdings Limited (Hong Kong)

• Mitsubishi Electric Corporation (Japan)

• VALEO SERVICE (France)

• MAHLE GmbH (Germany)

• Cummins Inc. (U.S.)

• Daimler AG (Germany)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.