Global Automotive Gas Sensor Market

Market Size in USD Billion

USD

2.37 Billion

USD

4.38 Billion

2025

2033

USD

2.37 Billion

USD

4.38 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.37 Billion | |

| USD 4.38 Billion | |

| % | |

|

Automotive Gas Sensor Market Overview

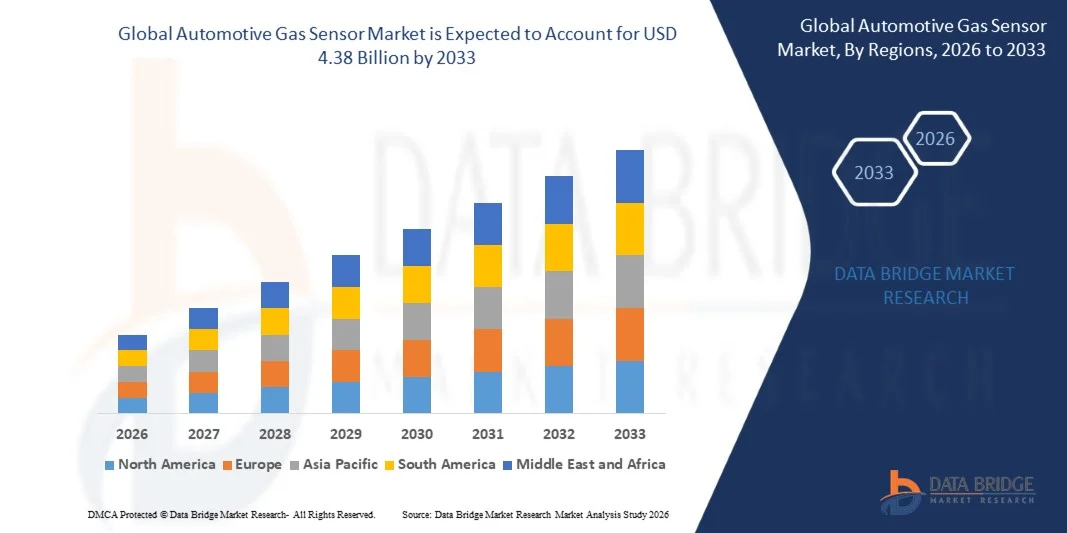

The Automotive Gas Sensor Market was valued at USD 2.37 billion in 2025 and is projected to reach USD 4.38 billion by 2033, growing at a CAGR of 8.00% from 2026 to 2033. The Automotive Gas Sensor Market is experiencing consistent growth driven by increasing demand for vehicle emission monitoring systems, stricter government regulations on automotive emissions, and rising adoption of advanced sensing technologies in modern vehicles. The growing focus on reducing greenhouse gas emissions, improving fuel efficiency, and enhancing vehicle safety is encouraging automotive manufacturers to integrate gas sensors across passenger vehicles, commercial vehicles, and electric mobility platforms.

The implementation of stringent emission standards globally, combined with increasing adoption of advanced driver assistance systems (ADAS), connected vehicles, and smart engine management technologies, is accelerating the demand for automotive gas sensors. Sensors such as oxygen sensors, nitrogen oxide (NOx) sensors, carbon monoxide sensors, and particulate matter sensors are becoming essential components for real-time exhaust monitoring, emission control, and engine optimization. Advancements in MEMS-based sensing technologies, increasing electrification of vehicles, and growing investments in intelligent vehicle systems are further supporting market expansion across developed and emerging automotive markets.

Key Market Trends & Insights

- North America dominated the Automotive Gas Sensor Market with the largest revenue share of 36.2% in 2025, supported by strong adoption of advanced vehicle safety technologies, stringent emission regulations, and increasing integration of gas sensing systems in passenger and commercial vehicles. The region benefits from the presence of major automotive manufacturers, sensor technology providers, and regulatory frameworks focused on reducing vehicle emissions and improving cabin air quality. Increasing deployment of oxygen (O₂), carbon monoxide (CO), nitrogen oxide (NOx), and volatile organic compound (VOC) sensors in vehicles is further strengthening market growth across the region.

- The Wired connectivity segment dominated the market with a 68.7% share in 2025, supported by widespread adoption in conventional automotive architectures, emission control systems, and safety-critical applications.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by rapid automotive production growth, increasing vehicle electrification, rising environmental regulations, and expanding adoption of advanced sensing technologies in China, India, Japan, and South Korea. Growing investments by automotive OEMs and component manufacturers in emission monitoring, electric vehicles, and smart mobility solutions are accelerating demand for automotive gas sensors across the region.

- Solid-state or metal–oxide–semiconductor (MOS) technology is the fastest-growing technology segment, projected to register a CAGR of 8.4% from 2026 to 2033, reflecting increasing demand for compact, cost-effective, and highly sensitive gas detection solutions. MOS-based sensors are gaining adoption due to their durability, miniaturization capability, low production cost, and suitability for real-time monitoring of gases such as CO, VOCs, methane, and hydrogen in automotive applications.

- The passenger cars segment dominates the end-user category with a 63.7% revenue share in 2025, supported by increasing adoption of advanced safety systems, cabin air quality monitoring technologies, and emission control solutions in passenger vehicles. Automotive manufacturers are increasingly integrating gas sensors to enhance occupant safety, improve engine performance, and comply with emission regulations. The rising demand for connected and intelligent vehicles is further driving sensor deployment in passenger cars.

Market Size & Forecast

- Global Market Value (2025): USD 2.37 Billion

- Expected Market Value (2033): USD 4.38 Billion

- Forecast CAGR (2026–2033): 8.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Automotive Gas Sensor Market Segmentation

|

Attributes |

Automotive Gas Sensor Key Market Insights |

|

Segments Covered |

· By Gas Type: Oxygen (O₂), Carbon Monoxide (CO), Carbon Dioxide (CO₂), Ammonia (NH₃), Chlorine (Cl), Hydrogen Sulfide (H₂S), Nitrogen Oxide (NOx), Volatile Organic Compounds (VOC), Hydrocarbons (Propane, Butane), Methane (CH₄), and Hydrogen (H₂) · By Technology: Electrochemical, Photoionization Detectors (PID), Solid-State or Metal–Oxide–Semiconductor (MOS), Catalytic, Infrared, Laser, Zirconia, Holographic, and Others · By Connectivity: Wired and Wireless · By End Users: Passenger Cars and Commercial Vehicles |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Bosch (Germany) |

|

Market Opportunities |

· Growing Adoption of Advanced Emission Control Technologies in Vehicles · Expansion of Electric, Hybrid, and Connected Vehicle Technologies · Advancements in MEMS, AI-Based Sensing, and Smart Sensor Technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Automotive Gas Sensor Market Trends

Trend: Rising Adoption of Advanced Gas Sensing Technologies in Connected and Electric Vehicles

The Automotive Gas Sensor Market is witnessing increasing adoption of advanced gas sensing technologies due to growing demand for emission monitoring, vehicle safety, and cabin air quality management. Automotive manufacturers are integrating gas sensors for detecting gases such as oxygen (O₂), carbon monoxide (CO), carbon dioxide (CO₂), nitrogen oxides (NOx), volatile organic compounds (VOC), hydrogen (H₂), and methane (CH₄) to improve vehicle efficiency and meet stringent environmental regulations. The rising adoption of electric vehicles (EVs) is further creating opportunities for hydrogen and battery safety monitoring applications, where accurate gas detection is essential for preventing thermal events and improving passenger protection. Governments worldwide are implementing stricter emission regulations, including advanced vehicle emission standards in regions such as North America, Europe, and Asia-Pacific, encouraging OEMs to adopt high-performance gas sensing solutions. For instance, automotive manufacturers are increasingly deploying NOx sensors in diesel and gasoline vehicles equipped with Selective Catalytic Reduction (SCR) systems to monitor exhaust emissions and ensure compliance with emission limits. The increasing focus on smart mobility, connected vehicles, and autonomous driving technologies is further accelerating demand for compact, accurate, and real-time automotive gas sensing systems. Companies such as Bosch, Denso, Continental, and Sensata Technologies are continuously developing advanced automotive sensor solutions to support emission control, vehicle diagnostics, and safety applications. The integration of semiconductor-based sensing technologies, wireless connectivity, and AI-enabled analytics is enabling faster detection, predictive maintenance, and improved vehicle performance monitoring. Growing automotive production in emerging economies, particularly China and India, is also contributing to increased adoption of automotive gas sensors.

Automotive Gas Sensor Market Dynamics

Key Market Driver: Increasing Stringency of Vehicle Emission Regulations and Demand for Cleaner Mobility Solutions

The growing implementation of strict vehicle emission regulations is a major driver of the Automotive Gas Sensor Market. Governments and regulatory agencies are enforcing stricter standards to reduce greenhouse gas emissions and harmful pollutants from vehicles, increasing the requirement for accurate gas monitoring technologies. Automotive gas sensors play a critical role in exhaust monitoring systems by measuring emissions and enabling real-time adjustment of engine performance and after-treatment systems. The increasing adoption of NOx sensors, oxygen sensors, and CO sensors in modern vehicles is driven by the need to optimize fuel efficiency, reduce emissions, and comply with regulatory requirements. Automotive OEMs are integrating advanced sensing solutions into internal combustion engine vehicles as well as hybrid and electric vehicles to improve environmental performance. For instance, the implementation of advanced emission regulations such as Euro 7 standards in Europe and evolving emission norms in countries including India and China is encouraging manufacturers to invest in improved gas sensing technologies. In addition, the rising production of connected and intelligent vehicles is increasing demand for sensors capable of providing real-time data for vehicle control systems and diagnostics. The expansion of EV and hydrogen vehicle technologies is further creating new applications for gas sensors in battery safety and hydrogen leakage detection.

Key Restraint/Challenge: High Cost of Advanced Gas Sensor Technologies and Integration Complexity

A significant challenge in the Automotive Gas Sensor Market is the high cost associated with developing, integrating, and maintaining advanced sensing systems. Modern automotive gas sensors require precise calibration, advanced semiconductor materials, and sophisticated electronic systems to achieve high accuracy and reliability under varying temperature, pressure, and environmental conditions. The integration of multiple sensors into modern vehicles increases system complexity and manufacturing costs, particularly for electric vehicles, autonomous vehicles, and premium automotive models. Smaller automotive manufacturers and cost-sensitive markets may face challenges in adopting advanced sensing technologies due to higher component costs and the need for specialized testing infrastructure. In addition, fluctuations in the availability and pricing of raw materials used in sensor manufacturing, such as rare metals and semiconductor components, can impact production costs. Sensor manufacturers must continuously invest in research and development to improve sensitivity, durability, miniaturization, and cost efficiency while meeting evolving regulatory requirements.

Key Market Opportunity: Integration of AI, IoT, and Smart Vehicle Monitoring Platforms

The integration of artificial intelligence (AI), Internet of Things (IoT), and connected vehicle platforms presents significant growth opportunities for the Automotive Gas Sensor market. AI-enabled automotive systems can analyze real-time gas sensor data to optimize engine performance, predict maintenance requirements, detect abnormal emissions, and improve vehicle safety. The growing adoption of connected vehicles is enabling advanced data-driven applications where gas sensors communicate with vehicle control systems and cloud platforms for continuous monitoring and analytics. This is creating opportunities for manufacturers to develop intelligent sensors capable of supporting predictive diagnostics and autonomous vehicle ecosystems. The increasing adoption of hydrogen fuel cell vehicles is also opening new opportunities for hydrogen gas sensors due to the need for accurate leak detection and safety monitoring. Companies are investing in advanced sensor technologies that provide faster response times, higher sensitivity, and improved reliability. For instance, automotive technology providers are developing next-generation gas sensing solutions using MEMS-based sensors, wireless connectivity, and AI-powered analytics to support future mobility applications. The expansion of electric mobility, smart transportation infrastructure, and autonomous vehicle development across Asia-Pacific, North America, and Europe is expected to further accelerate demand for advanced automotive gas sensor technologies during the forecast period.

Automotive Gas Sensor Market Scope

The automotive gas sensor market is segmented on the basis of gas type, technology, connectivity, and end user.

- By Gas Type

On the basis of gas type, the Automotive Gas Sensor Market is segmented into Oxygen (O2), Carbon Monoxide (CO), Carbon Dioxide (CO2), Ammonia (NH3), Chlorine (Cl), Hydrogen Sulfide (H2S), Nitrogen Oxide (NOx), Volatile Organic Compounds (VOC), Hydrocarbons (Propane, Butane), Methane (CH4), and Hydrogen (H2). The Nitrogen Oxide (NOx) sensor segment dominated the market with a 28.6% share in 2025, owing to increasing regulatory pressure for vehicle emission reduction, stringent standards such as Euro 6/7 and EPA regulations, and growing adoption of exhaust after-treatment systems including Selective Catalytic Reduction (SCR). Automotive manufacturers are integrating NOx sensors extensively in diesel and commercial vehicles to monitor emissions and optimize engine performance. The rising production of fuel-efficient vehicles and increasing focus on reducing greenhouse gas emissions are further supporting segment growth. In addition, government initiatives promoting cleaner transportation technologies are driving demand for advanced NOx detection solutions across passenger and commercial vehicles.

The hydrogen (H2) gas sensor segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, driven by increasing adoption of hydrogen fuel cell vehicles and investments in hydrogen mobility infrastructure. Automotive companies are developing hydrogen-powered vehicles as part of zero-emission transportation strategies, creating demand for reliable hydrogen leakage detection systems. The expansion of hydrogen refueling networks and safety requirements in fuel cell electric vehicles (FCEVs) are accelerating sensor adoption. Advancements in miniaturized and highly sensitive hydrogen sensing technologies are further supporting market expansion. Growing government funding for hydrogen economies across regions such as Europe, North America, and Asia-Pacific is expected to create significant growth opportunities.

- By Technology

On the basis of technology, the Automotive Gas Sensor Market is segmented into Electrochemical, Photoionization Detectors (PID), Solid-State or Metal–Oxide–Semiconductor (MOS), Catalytic, Infrared, Laser, Zirconia, Holographic, and Others. The Electrochemical sensor segment dominated the market with a 35.4% share in 2025, due to its high sensitivity, reliability, compact size, and cost-effectiveness in detecting gases such as oxygen, carbon monoxide, and nitrogen oxides. These sensors are widely used in automotive emission monitoring systems, cabin air quality monitoring, and safety applications. The increasing integration of emission control systems and onboard diagnostics (OBD) in modern vehicles is driving adoption. In addition, electrochemical sensors offer low power consumption and accurate detection performance, making them suitable for mass-market automotive applications.

The solid-state or metal–oxide–semiconductor (MOS) sensor segment is expected to witness the fastest CAGR of 9.1% from 2026 to 2033, driven by rising demand for smart automotive sensing technologies and connected vehicle systems. MOS sensors provide rapid response times, durability, and compatibility with advanced electronic systems. Increasing adoption of intelligent vehicles, autonomous driving technologies, and real-time environmental monitoring systems is accelerating demand. Automotive manufacturers are increasingly integrating MOS-based sensors for air quality monitoring, battery safety, and alternative fuel vehicle applications. Continuous advancements in nanomaterials and semiconductor technologies are further improving sensor performance and expanding application areas.

- By Connectivity

On the basis of connectivity, the Automotive Gas Sensor Market is segmented into Wired and Wireless. The Wired connectivity segment dominated the market with a 68.7% share in 2025, supported by widespread adoption in conventional automotive architectures, emission control systems, and safety-critical applications. Wired sensors provide stable communication, low latency, and reliable data transmission, making them preferred for engine management systems and exhaust monitoring applications. Automotive OEMs continue to utilize wired sensor networks due to their proven reliability and compatibility with existing vehicle electronic control units (ECUs). Increasing vehicle production and regulatory compliance requirements are further strengthening the dominance of wired connectivity.

The Wireless connectivity segment is projected to register the fastest CAGR of 11.0% from 2026 to 2033, driven by increasing adoption of connected vehicles, IoT-based automotive systems, and smart sensing platforms. Wireless gas sensors enable flexible installation, reduced wiring complexity, and real-time data transmission. Growing demand for advanced vehicle monitoring, battery safety systems, and autonomous vehicle technologies is accelerating adoption. The integration of wireless communication technologies such as Bluetooth, Zigbee, and advanced automotive networking solutions is expected to enhance market opportunities during the forecast period.

- By End User

On the basis of end user, the Automotive Gas Sensor Market is segmented into Passenger Cars and Commercial Vehicles. The Passenger Cars segment dominated the market with a 62.3% share in 2025, driven by increasing vehicle production, rising consumer demand for advanced safety features, and growing adoption of emission monitoring technologies. Passenger vehicle manufacturers are integrating gas sensors for cabin air quality management, emission compliance, and powertrain optimization. The increasing penetration of electric vehicles, hybrid vehicles, and advanced driver assistance systems is further supporting sensor demand. Additionally, strict environmental regulations and consumer awareness regarding vehicle emissions are encouraging automotive OEMs to adopt advanced gas sensing solutions.

The commercial vehicles segment is expected to witness the fastest CAGR of 8.7% from 2026 to 2033, driven by increasing adoption of emission control systems in trucks, buses, and fleet vehicles. Commercial vehicle operators are focusing on fuel efficiency, reduced emissions, and regulatory compliance, increasing demand for advanced gas monitoring technologies. The expansion of logistics, transportation, and public mobility networks is further supporting market growth. Government regulations targeting heavy-duty vehicle emissions and the transition toward cleaner fuels such as hydrogen and natural gas are creating new opportunities for automotive gas sensor adoption.

Automotive Gas Sensor Market Regional Analysis

North America dominated the Automotive Gas Sensor Market with the largest revenue share of 36.2% in 2025, supported by strong adoption of advanced vehicle safety technologies, stringent emission regulations, and increasing integration of gas sensing systems in passenger and commercial vehicles. The region benefits from the presence of major automotive manufacturers, sensor technology providers, and regulatory frameworks focused on reducing vehicle emissions and improving cabin air quality. Increasing deployment of oxygen (O₂), carbon monoxide (CO), nitrogen oxide (NOx), and volatile organic compound (VOC) sensors in vehicles is further strengthening market growth across the region. Growing demand for efficient emission control systems, connected vehicle technologies, and advanced automotive monitoring solutions is driving further adoption of gas sensors in North America.

U.S. Automotive Gas Sensor Market Insight

The U.S. automotive gas sensor market is witnessing strong growth due to rising demand for advanced emission monitoring technologies, increasing adoption of fuel-efficient vehicles, and strict government regulations aimed at reducing automotive emissions. The country’s established automotive industry, presence of leading sensor manufacturers, and increasing integration of NOx, oxygen, and VOC sensors in modern vehicles are supporting market expansion. In addition, growing investments in electric vehicles, hybrid mobility solutions, and smart vehicle technologies are creating new opportunities for automotive gas sensor applications.

Europe Automotive Gas Sensor Market Insight

The Europe automotive gas sensor market remains a significant contributor to global revenue, driven by strict emission standards, strong automotive manufacturing capabilities, and increasing focus on sustainable mobility solutions. The region’s regulatory emphasis on reducing vehicle pollutants and improving air quality is encouraging automotive manufacturers to integrate advanced gas sensing technologies. Rising adoption of exhaust monitoring systems, selective catalytic reduction (SCR) technologies, and advanced emission control solutions is supporting market growth across European countries.

U.K. Automotive Gas Sensor Market Insight

The U.K. automotive gas sensor market is experiencing steady growth, supported by increasing focus on vehicle emission reduction, adoption of advanced automotive technologies, and growing demand for cleaner transportation solutions. Automotive manufacturers and component suppliers are increasingly integrating gas sensors to improve engine efficiency, monitor exhaust emissions, and comply with environmental regulations. The rising adoption of electric and hybrid vehicles, along with investments in smart mobility technologies, is further contributing to market expansion.

Germany Automotive Gas Sensor Market Insight

The Germany automotive gas sensor market is expanding steadily due to the country’s strong automotive manufacturing base, advanced engineering capabilities, and increasing adoption of emission control technologies. Leading automotive manufacturers are integrating NOx, oxygen, and other gas sensors into vehicles to meet strict European emission regulations and improve vehicle performance. Continuous advancements in automotive electronics, fuel-efficient powertrains, and exhaust after-treatment systems are further driving demand for gas sensing solutions in Germany.

Asia-Pacific Automotive Gas Sensor Market Insight

The Asia-Pacific automotive gas sensor market is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by rapid automotive production growth, increasing vehicle electrification, rising environmental regulations, and expanding adoption of advanced sensing technologies in China, India, Japan, and South Korea. Growing investments by automotive OEMs and component manufacturers in emission monitoring, electric vehicles, and smart mobility solutions are accelerating demand for automotive gas sensors across the region. Increasing vehicle production, urban air quality concerns, and government initiatives supporting cleaner transportation are further strengthening regional market growth.

Japan Automotive Gas Sensor Market Insight

The Japan automotive gas sensor market is witnessing consistent growth due to rising investments in automotive innovation, advanced emission control systems, and next-generation vehicle technologies. Japanese automotive manufacturers are increasingly adopting high-performance gas sensors for exhaust monitoring, fuel efficiency improvement, and compliance with environmental standards. The country’s strong focus on hybrid vehicles, electric mobility, and intelligent transportation systems is further supporting the adoption of advanced automotive sensing technologies.

China Automotive Gas Sensor Market Insight

The China automotive gas sensor market is growing rapidly, driven by expanding vehicle production, increasing government focus on emission reduction, and rising adoption of advanced automotive technologies. The country’s growing electric vehicle ecosystem, strict vehicle emission regulations, and increasing investments in smart mobility solutions are accelerating demand for automotive gas sensors. In addition, rising adoption of NOx, oxygen, carbon monoxide, and VOC sensors in passenger and commercial vehicles is positioning China as one of the fastest-growing markets for automotive gas sensor technologies globally.

Automotive Gas Sensor Market Share

The Automotive Gas Sensor industry is primarily led by well-established companies, including:

• Bosch (Germany)

• Denso Corporation (Japan)

• Continental AG (Germany)

• Sensata Technologies (U.S.)

• Honeywell International Inc. (U.S.)

• Robertshaw Controls Company (U.S.)

• Figaro Engineering Inc. (Japan)

• Amphenol Corporation (U.S.)

• TDK Corporation (Japan)

• STMicroelectronics (Switzerland)

• Texas Instruments Incorporated (U.S.)

• Analog Devices, Inc. (U.S.)

• Infineon Technologies AG (Germany)

• NXP Semiconductors N.V. (Netherlands)

• Semiconductor Components Industries, LLC (onsemi) (U.S.)

• Microchip Technology Inc. (U.S.)

• Sensirion AG (Switzerland)

• Murata Manufacturing Co., Ltd. (Japan)

• Panasonic Industry Co., Ltd. (Japan)

• Yokogawa Electric Corporation (Japan)

• Figaro Engineering Inc. (Japan)

• NGK Spark Plug Co., Ltd. (Japan)

• Tenneco Inc. (U.S.)

• Hitachi Astemo, Ltd. (Japan)

• Melexis (Belgium)

• Aeroqual Limited (New Zealand)

• Alphasense (United Kingdom)

• City Technology Ltd. (United Kingdom)

• Membrapor AG (Switzerland)

• Drägerwerk AG & Co. KGaA (Germany)

• Senseair AB (Sweden)

• Winsen Electronics Technology Co., Ltd. (China)

• Zhengzhou Winsen Electronics Technology Co., Ltd. (China)

• Cubic Sensor and Instrument Co., Ltd. (China)

Latest Developments in Automotive Gas Sensor Market

- In March 2021, Bosch Sensortec announced the launch of its BME688 AI-enabled gas sensor, a compact MEMS-based sensor designed to detect gases while measuring humidity, temperature, and pressure. The sensor integrated artificial intelligence capabilities for advanced gas classification and environmental monitoring. This development highlighted the growing adoption of intelligent sensing technologies and supported future automotive applications such as cabin air quality monitoring and smart vehicle environmental sensing

- In November 2021, Bosch introduced new automotive exhaust gas sensor solutions, including advanced oxygen and NOx sensors, to improve vehicle emission monitoring and engine efficiency. The sensors were designed to support accurate exhaust gas measurement, optimize after-treatment systems, and help automotive manufacturers comply with increasingly strict emission regulations across passenger and commercial vehicles

- In February 2022, Sensata Technologies announced advancements in its automotive sensor technology portfolio, focusing on improved sensing solutions for emission control, powertrain optimization, and vehicle safety applications. The development supported the automotive industry’s transition toward cleaner mobility solutions by enabling more accurate monitoring and control of vehicle operating conditions

- In September 2022, Bosch Mobility highlighted improvements in its NOx sensor technology for diesel vehicles and commercial transportation applications. The enhanced sensors provided higher measurement accuracy and reliability for Selective Catalytic Reduction (SCR) systems, helping manufacturers reduce nitrogen oxide emissions and meet global environmental regulations

- In May 2023, Bosch Mobility expanded its automotive gas sensing solutions with advanced NOx sensor technologies designed for passenger cars and commercial vehicles. The improved sensors offered better durability, faster response, and accurate emission monitoring capabilities, enabling vehicle manufacturers to optimize exhaust treatment systems and improve compliance with evolving emission standards

- In October 2023, Denso Corporation announced continued development of advanced automotive sensing technologies to support next-generation vehicles. The company focused on improving sensor performance for emission control, fuel efficiency, and vehicle monitoring systems, supporting the increasing demand for reliable sensing solutions in hybrid, electric, and conventional vehicles

- In April 2024, Bosch Mobility strengthened its focus on advanced vehicle sensing technologies supporting connected vehicles, automated driving, and emission management systems. The company’s developments emphasized the importance of accurate real-time sensor data for improving vehicle efficiency, safety, and compliance with regulatory requirements

- In August 2024, automotive technology companies increased investments in hydrogen gas sensing solutions to support the growing adoption of hydrogen fuel cell vehicles. The development of hydrogen leakage detection sensors became increasingly important for improving safety in fuel cell vehicles and supporting the expansion of hydrogen-based transportation systems

- In January 2025, Bosch Mobility continued enhancing NOx sensor solutions for passenger and commercial vehicles to support upcoming emission regulations. The advanced sensors enabled precise exhaust monitoring and improved SCR system performance, helping automotive manufacturers achieve lower emissions and better fuel efficiency

- In June 2025, automotive sensor manufacturers accelerated the development of smart automotive gas sensors with improved connectivity, miniaturized designs, and digital communication capabilities. These advancements supported the growing adoption of connected vehicles, electric mobility, and advanced emission monitoring systems, creating new growth opportunities for the Automotive Gas Sensor Market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.