Global Automotive Heat Exchanger Market

Market Size in USD Billion

CAGR :

%

USD

27.28 Billion

USD

44.48 Billion

2025

2033

USD

27.28 Billion

USD

44.48 Billion

2025

2033

| 2026 –2033 | |

| USD 27.28 Billion | |

| USD 44.48 Billion | |

| % | |

|

Automotive Heat Exchanger Market Size

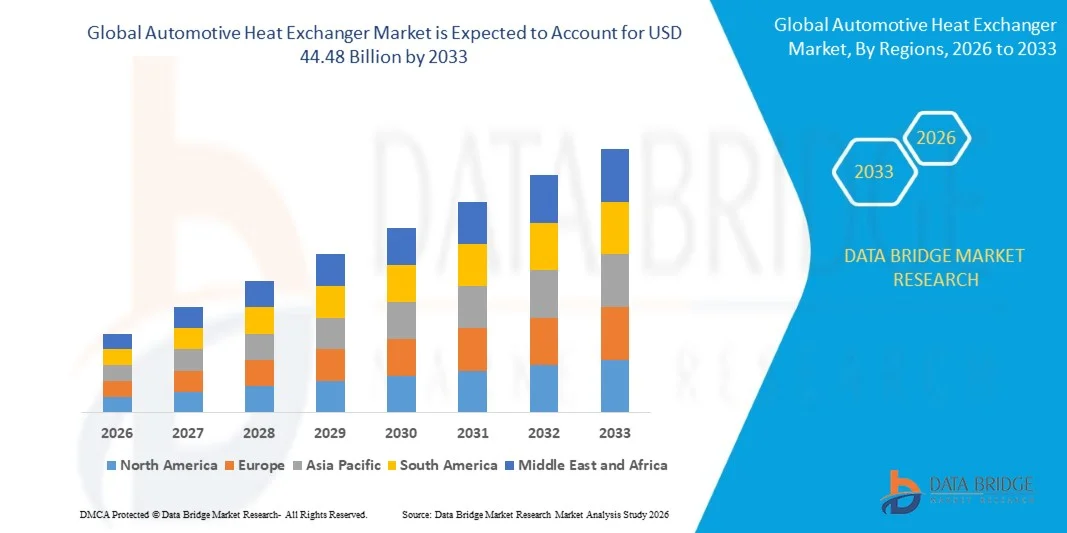

- The global automotive heat exchanger market size was valued at USD 27.28 billion in 2025 and is expected to reach USD 44.48 billion by 2033, at a CAGR of 6.3% during the forecast period

- The market growth is largely driven by the rapid advancement and integration of electrified powertrains, hybrid vehicles, and next-generation internal combustion engine technologies, leading to higher demand for efficient thermal management systems across automotive platforms

- Furthermore, tightening emission regulations and rising focus on fuel efficiency are compelling automakers to adopt advanced heat exchanger systems that optimize engine performance, battery cooling, and cabin comfort, thereby significantly strengthening industry growth

Automotive Heat Exchanger Market Analysis

- Automotive heat exchangers are critical thermal management components used to transfer heat between fluids in vehicles, supporting engine cooling, battery temperature regulation in electric vehicles, and HVAC systems for passenger comfort. These systems include radiators, intercoolers, condensers, and oil coolers designed to maintain optimal operating temperatures under varying driving conditions

- The escalating demand for automotive heat exchangers is primarily driven by the rising production of electric and hybrid vehicles, increasing engine downsizing with turbocharging technologies, and stricter global emission and efficiency standards. In addition, growing consumer expectations for enhanced vehicle performance and climate-controlled cabin experiences are further accelerating adoption across passenger and commercial vehicle segments

- Asia-Pacific dominated the automotive heat exchanger market with a share of 47.38% in 2025, due to strong automotive production, expanding vehicle parc, and high demand for passenger and commercial vehicles

- North America is expected to be the fastest growing region in the automotive heat exchanger market during the forecast period due to rising EV adoption, strong automotive manufacturing base, and increasing demand for advanced thermal management systems

- Aluminium segment dominated the market with a market share of 73.34% in 2025, due to its lightweight nature, strong corrosion resistance, and high thermal conductivity. Aluminium is extensively used in radiators and condensers due to its ability to reduce overall vehicle weight and improve fuel efficiency. Its cost-effectiveness compared to alternative materials further enhances its widespread adoption across mass-market vehicles

Report Scope and Automotive Heat Exchanger Market Segmentation

|

Attributes |

Automotive Heat Exchanger Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Automotive Heat Exchanger Market Trends

“Integration of Advanced Thermal Systems in EVs and Hybrids”

- A key trend in the automotive heat exchanger market is the increasing integration of advanced thermal management systems within electric and hybrid vehicles, driven by the need to efficiently regulate battery temperature, power electronics, and cabin climate. This integration is strengthening the role of heat exchangers as essential components in next-generation vehicle architectures focused on performance and energy optimization

- For instance, Mahle GmbH and Valeo provide advanced thermal management modules and heat exchangers used in electric vehicles to ensure stable battery cooling and improved drivetrain efficiency. These solutions enhance vehicle reliability and support extended battery life under varying operating conditions

- The rising electrification of vehicles is accelerating the adoption of compact and high-efficiency heat exchanger designs that can manage multiple thermal loads within limited vehicle space. This is pushing manufacturers to develop integrated systems that combine cooling and heating functions for improved system efficiency

- Automakers are increasingly focusing on reducing vehicle weight while maintaining thermal performance, leading to the use of aluminum-based and lightweight composite heat exchangers. This trend is improving energy efficiency and supporting overall vehicle range enhancement in EVs

- The growing complexity of hybrid powertrains is also increasing the need for multi-circuit thermal systems capable of handling both engine and electric components simultaneously. This is encouraging innovation in modular and scalable heat exchanger designs across vehicle platforms

- The shift toward electrified mobility is reinforcing the demand for advanced thermal systems that ensure safety, efficiency, and durability. This ongoing transformation is positioning integrated heat exchanger solutions as a core requirement in modern automotive engineering

Automotive Heat Exchanger Market Dynamics

Driver

“Rising Demand for Fuel Efficiency and Emission Compliance”

- The increasing global emphasis on fuel efficiency and stringent emission regulations is driving automakers to adopt advanced heat exchanger systems that enhance engine performance and reduce energy losses. These systems play a critical role in optimizing combustion efficiency and maintaining ideal operating temperatures across vehicle components

- For instance, DENSO Corporation supplies high-efficiency radiators and intercoolers that support improved fuel economy and reduced emissions in passenger and commercial vehicles. These components help automakers comply with regulatory standards while maintaining engine performance stability

- The push for lower carbon emissions is encouraging the use of advanced thermal management solutions that improve heat transfer efficiency and reduce fuel consumption. This is strengthening the adoption of next-generation heat exchangers across internal combustion and hybrid vehicles

- Governments across major automotive markets are implementing stricter emission norms, which is accelerating the integration of efficient cooling and exhaust heat recovery systems. This regulatory pressure is directly influencing design improvements in automotive thermal systems

- The continuous focus on sustainable mobility and reduced environmental impact is reinforcing the need for efficient thermal control solutions. This driver is shaping long-term adoption of advanced heat exchanger technologies across the automotive industry

Restraint/Challenge

“High Cost and Complexity of Advanced Designs”

- The automotive heat exchanger market faces challenges due to the increasing complexity of advanced thermal system designs, which require precision engineering, specialized materials, and integration across multiple vehicle subsystems. These factors significantly raise development and production costs for manufacturers

- For instance, Modine Manufacturing Company develops advanced thermal management systems that involve complex engineering processes and high-performance materials to meet EV and hybrid vehicle requirements. These design complexities increase production timelines and overall system cost structures

- The use of lightweight materials such as aluminum alloys and advanced composites, while improving efficiency, adds to manufacturing challenges due to higher processing requirements. This results in increased production expenses and limits cost competitiveness for large-scale deployment

- Integration of multi-functional heat exchangers that handle engine, battery, and cabin cooling simultaneously requires advanced design coordination and testing. This increases engineering complexity and raises development investment needs for automakers and suppliers

- The combination of rising material costs and sophisticated engineering requirements continues to constrain market scalability. This challenge is pushing industry players to focus on cost optimization and manufacturing efficiency improvements to maintain competitiveness

Automotive Heat Exchanger Market Scope

The market is segmented on the basis of application, design type, material, and propulsion type and vehicle type.

• By Application

On the basis of application, the automotive heat exchanger market is segmented into intercooler, radiator, air conditioning, oil cooler, and others. The radiator segment dominated the largest market revenue share in 2025, supported by its essential role in maintaining optimal engine temperature across all vehicle types and its wide integration in both passenger and commercial vehicles. Growing vehicle production and the need for efficient thermal regulation in internal combustion engines continue to reinforce radiator demand. Radiators also benefit from continuous design improvements that enhance heat dissipation efficiency and durability under extreme operating conditions. Their universal application across vehicle platforms further strengthens their dominant position in the market.

The air conditioning segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by rising consumer demand for enhanced cabin comfort and increasing adoption of advanced HVAC systems in electric and premium vehicles. Expansion of electric vehicle platforms, which require highly efficient thermal management systems, is accelerating the integration of advanced air conditioning heat exchangers. Automakers are focusing on energy-efficient cooling solutions to optimize battery performance and passenger comfort. Increasing urbanization and higher vehicle ownership rates are also supporting sustained demand for advanced automotive air conditioning systems.

• By Design Type

On the basis of design type, the automotive heat exchanger market is segmented into tube fin, plate bar, and others. The tube fin segment dominated the largest market revenue share in 2025, driven by its cost-effectiveness, proven thermal performance, and widespread use across conventional vehicle cooling systems. Its robust structure and ease of manufacturing make it suitable for high-volume automotive applications. Tube fin designs are widely preferred in radiators and condensers due to their reliable heat transfer efficiency under varying load conditions. Established production processes and compatibility with existing vehicle architectures further strengthen its dominance in the market.

The plate bar segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for compact, lightweight, and high-efficiency heat exchangers in modern vehicles. This design offers superior thermal performance in limited installation spaces, making it highly suitable for electric and hybrid vehicles. Automakers are increasingly adopting plate bar configurations to improve energy efficiency and reduce overall vehicle weight. Advancements in brazing technology and material engineering are also supporting wider adoption of this segment.

• By Material

On the basis of material, the automotive heat exchanger market is segmented into aluminium, copper, and others. The aluminium segment dominated the largest market revenue share of 73.34% in 2025, driven by its lightweight nature, strong corrosion resistance, and high thermal conductivity. Aluminium is extensively used in radiators and condensers due to its ability to reduce overall vehicle weight and improve fuel efficiency. Its cost-effectiveness compared to alternative materials further enhances its widespread adoption across mass-market vehicles. Continuous advancements in aluminium alloy processing are also improving performance and durability in automotive thermal systems.

The copper segment is anticipated to witness the fastest growth rate from 2026 to 2033, supported by its superior heat transfer efficiency and increasing use in high-performance and electric vehicle thermal systems. Copper-based heat exchangers are gaining traction in applications requiring rapid and efficient thermal regulation. The growing focus on battery cooling and power electronics thermal management in electric vehicles is accelerating demand. Material innovations and hybrid designs combining copper with other metals are further enhancing adoption in specialized automotive applications.

• By Propulsion Type

On the basis of propulsion type, the automotive heat exchanger market is segmented into internal combustion engine (ICE) and electric vehicle (EV). The ICE segment dominated the largest market revenue share in 2025, driven by the large existing global vehicle fleet and continued production of conventional automobiles. ICE vehicles require multiple heat exchangers such as radiators, intercoolers, and oil coolers to manage engine heat efficiently. Established manufacturing infrastructure and cost advantages continue to support strong demand for ICE-based thermal systems. Despite gradual electrification trends, ICE vehicles remain the backbone of current automotive heat exchanger consumption.

The electric vehicle (EV) segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by rapid EV adoption and increasing investments in advanced thermal management systems. EVs require highly efficient heat exchangers for battery cooling, power electronics, and cabin climate control. Government incentives and tightening emission regulations are accelerating the shift toward electrified mobility. Continuous innovation in compact and energy-efficient thermal solutions is further strengthening the growth trajectory of this segment.

• By Vehicle Type

On the basis of vehicle type, the automotive heat exchanger market is segmented into passenger car, light commercial vehicle (LCV), and heavy commercial vehicle (HCV). The passenger car segment dominated the largest market revenue share in 2025, driven by high global production volumes and increasing demand for comfort-oriented features such as advanced air conditioning and efficient cooling systems. Rising urban mobility and expanding middle-class vehicle ownership continue to support strong demand in this segment. Passenger cars also benefit from continuous integration of advanced thermal management technologies to improve fuel efficiency and performance. Large-scale manufacturing and global distribution networks further reinforce its dominant position.

The heavy commercial vehicle (HCV) segment is anticipated to witness the fastest growth rate from 2026 to 2033, supported by rising freight transportation activities and increasing adoption of advanced cooling systems for high-load operations. HCVs require robust heat exchangers to manage extreme engine and transmission temperatures during long-haul operations. Expansion of logistics infrastructure and growing e-commerce activities are further driving fleet modernization. Technological advancements in durable and high-capacity thermal systems are also accelerating adoption in this segment.

Automotive Heat Exchanger Market Regional Analysis

- Asia-Pacific dominated the automotive heat exchanger market with the largest revenue share of 47.38% in 2025, driven by strong automotive production, expanding vehicle parc, and high demand for passenger and commercial vehicles

- The region benefits from a well-established manufacturing base, cost-efficient production ecosystem, and large-scale integration of heat exchangers across ICE and emerging EV platforms

- Rapid industrialization, increasing vehicle exports, and growing adoption of advanced thermal management systems are accelerating market expansion. Continuous investments in automotive components and rising demand for fuel-efficient and electric mobility solutions further strengthen regional growth

China Automotive Heat Exchanger Market Insight

China held the largest share in the Asia-Pacific automotive heat exchanger market in 2025, supported by its massive automotive manufacturing capacity and strong presence of OEMs and component suppliers. The country has a highly integrated supply chain that enables large-scale production of radiators, condensers, and advanced thermal systems. Strong demand from both ICE vehicles and rapidly expanding EV adoption is reinforcing market growth. In addition, government support for new energy vehicles and continuous investment in automotive technology are strengthening China’s leadership position.

India Automotive Heat Exchanger Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by rising vehicle production, expanding commercial transport demand, and increasing adoption of passenger vehicles. Growing automotive manufacturing capabilities and localization of component production are supporting heat exchanger demand across vehicle categories. Increasing focus on fuel efficiency and regulatory push for emission reduction are further driving adoption of advanced thermal systems. In addition, expansion of EV manufacturing and infrastructure development is accelerating long-term market growth.

Europe Automotive Heat Exchanger Market Insight

The Europe automotive heat exchanger market is expanding steadily, supported by strong automotive engineering capabilities, high penetration of premium vehicles, and strict emission regulations. The region shows strong demand for advanced and efficient thermal management systems across ICE, hybrid, and EV platforms. Focus on lightweight materials and energy-efficient vehicle design is further driving adoption of advanced heat exchangers. In addition, continuous innovation in automotive technologies and strong presence of luxury and performance vehicle manufacturers are supporting market growth.

Germany Automotive Heat Exchanger Market Insight

Germany accounted for the largest share in the Europe automotive heat exchanger market in 2025, driven by its strong automotive manufacturing base and presence of leading global OEMs. The country has extensive use of advanced heat exchangers in passenger cars, commercial vehicles, and high-performance mobility systems. Strong engineering capabilities and R&D investment are supporting continuous innovation in thermal management technologies. In addition, export-oriented production and high adoption of advanced automotive components are reinforcing Germany’s leadership.

U.K. Automotive Heat Exchanger Market Insight

The U.K. market is supported by strong demand from passenger vehicles, commercial fleets, and premium automotive segments. Increasing focus on electrification and emission reduction is driving adoption of advanced thermal management systems. The country’s automotive R&D ecosystem supports development of efficient and compact heat exchanger technologies. In addition, growing investments in EV production and mobility innovation are further supporting market expansion.

North America Automotive Heat Exchanger Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising EV adoption, strong automotive manufacturing base, and increasing demand for advanced thermal management systems. The region benefits from high vehicle production, technological advancements, and strong presence of leading automotive OEMs and suppliers. Growing focus on fuel efficiency, emission reduction, and electrification is accelerating adoption of advanced heat exchangers. In addition, reshoring of manufacturing activities and investments in next-generation automotive technologies are supporting regional growth.

U.S. Automotive Heat Exchanger Market Insight

The U.S. accounted for the largest share in the North America automotive heat exchanger market in 2025, supported by strong automotive production, advanced R&D capabilities, and high adoption of EVs and hybrid vehicles. The country has a well-developed supply chain for automotive components and strong presence of global automotive manufacturers. Increasing demand for high-performance thermal systems in passenger cars, trucks, and electric vehicles is driving market growth. In addition, continuous innovation in lightweight and energy-efficient heat exchanger technologies is reinforcing the U.S. leadership position.

Automotive Heat Exchanger Market Share

The automotive heat exchanger industry is primarily led by well-established companies, including:

- MAHLE GmbH (Germany)

- DENSO Corporation (Japan)

- Kelvion Holdings (Germany)

- Banco Products (India) Ltd. (India)

- Valeo SA (France)

- T.RAD Co. Ltd. (Japan)

- American Industrial Heat Transfer (U.S.)

- Hanon Systems (South Korea)

- Climetal SL (Spain)

- Marelli (Calsonic Kansei) (Japan)

- Dana Incorporated (U.S.)

- GEA Group (Germany)

- Modine Manufacturing Company (U.S.)

- Nippon Light Metal Holdings (Japan)

- Sanden Holdings (Japan)

- Behr Hella Service (Germany)

- Constellium SE (France)

- AKG Thermal Systems (Germany)

- GandM Radiator (U.S.)

- Valeo SA (Thermal Systems) (France)

- IHI Corporation (Japan)

- KUHN SAS (France)

- Deere & Company (U.S.)

- CNH Industrial N.V. (U.K.)

- CLAAS KGaA mbH (Germany)

- AGCO Corporation (U.S.)

Latest Developments in Global Automotive Heat Exchanger Market

- In October 2025, Marelli introduced next-generation thermal management solutions including a high-performance chiller, eAxle oil cooler, and advanced aluminum radiator designed for electrified powertrains. These systems are improving heat dissipation efficiency in high-voltage EV architectures, where precise temperature control is critical for battery life and power electronics stability. The upgraded components also contribute to weight reduction and better energy efficiency, supporting extended driving range in electric vehicles. By integrating multiple thermal functions into compact designs, Marelli is enhancing system-level efficiency and strengthening demand for advanced heat exchanger technologies in modern EV platforms

- In May 2025, BorgWarner secured its largest North American high-voltage coolant heater contract for 400-V plug-in hybrid vehicles, with production scheduled to begin in 2027. This development highlights the growing importance of efficient thermal management in hybrid systems, particularly for maintaining optimal cabin comfort and battery performance in varying climates. The coolant heater solution enhances energy utilization by reducing dependence on engine waste heat, thereby improving overall vehicle efficiency. This contract also reinforces BorgWarner’s position in electrified thermal systems and reflects rising demand for advanced heat exchanger components in hybrid mobility applications

- In March 2025, Denso entered a strategic collaboration with MAHLE to jointly develop advanced thermal management systems for electrified powertrains. The partnership focuses on improving integration between multiple heat exchanger components such as radiators, condensers, and battery cooling systems to achieve higher efficiency and compact design. This collaboration is expected to enhance thermal regulation in EVs, ensuring stable battery performance and improved vehicle safety. By combining engineering expertise, both companies are accelerating innovation in next-generation thermal solutions, thereby supporting the rapid evolution of electric mobility

- In November 2024, Hankook completed the acquisition of Hanon Systems, significantly expanding its global automotive thermal management footprint. This acquisition strengthens Hankook’s access to advanced heat exchanger technologies and diversified product portfolios across ICE and EV applications. The integration is expected to improve manufacturing scalability, supply chain efficiency, and global market reach in automotive thermal systems. It also enhances the company’s capability to deliver integrated thermal solutions, supporting increasing demand for efficient cooling systems in electrified vehicles

- In October 2024, Hanon Systems inaugurated a new manufacturing facility in Ontario with the capacity to produce up to 900,000 electric compressors annually starting from 2025. This expansion significantly boosts production capabilities for EV thermal management systems, particularly in heat pump and climate control applications. The facility is designed to support high-volume demand from electric vehicle manufacturers, ensuring consistent supply of critical thermal components. By increasing localized production in North America, Hanon Systems is strengthening supply reliability and supporting the growing adoption of advanced automotive heat exchanger technologies in electrified mobility

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Automotive Heat Exchanger Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Automotive Heat Exchanger Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Automotive Heat Exchanger Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.