Global Automotive Laminated Glass Market

Market Size in USD Billion

USD

17.64 Billion

USD

26.06 Billion

2025

2033

USD

17.64 Billion

USD

26.06 Billion

2025

2033

| 2026 - 2033 | |

| USD 17.64 Billion | |

| USD 26.06 Billion | |

| % | |

|

Automotive Laminated Glass Market Overview

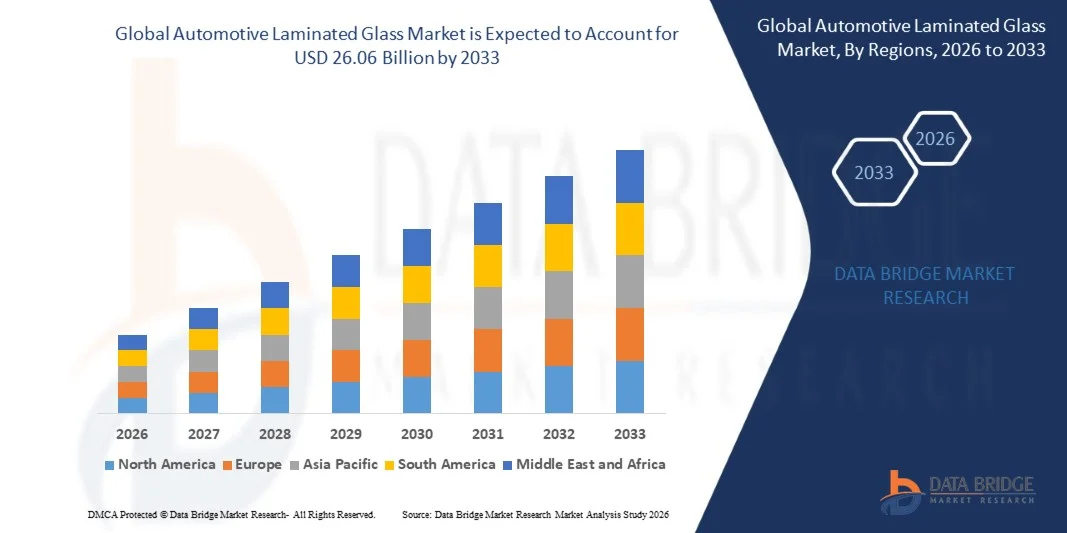

The Automotive Laminated Glass Market was valued at USD 17.64 Billion in 2025 and is projected to reach USD 26.06 Billion by 2033, growing at a CAGR of 5.00% from 2026 to 2033. The market is experiencing consistent growth driven by rising vehicle production, increasing adoption of advanced safety glazing systems, and growing integration of laminated glass in windshields, side windows, and panoramic roof systems. Expanding demand for electric vehicles and premium automobiles, along with advancements in acoustic, UV-protection, and lightweight glazing technologies, is further supporting market expansion across major automotive manufacturing regions.

The growing emphasis on vehicle safety regulations, passenger comfort, and energy efficiency is accelerating the adoption of automotive laminated glass across OEM and aftermarket channels. Increasing penetration of electric and autonomous vehicles is further boosting demand for advanced glazing solutions that enhance cabin insulation, reduce noise, and support sensor integration in modern automotive designs.

Key Market Trends & Insights

- Asia-Pacific dominated the Automotive Laminated Glass Market with the largest revenue share of 45% in 2025, supported by high vehicle production volumes, strong automotive OEM presence, and expanding demand for safety and comfort-focused glazing solutions

- The passive glass segment led the market with a 74.1% share in 2025, driven by its widespread usage in standard automotive glazing applications and lower production costs

- North America is expected to be the fastest-growing region at a CAGR of 7.35% from 2026 to 2033, fueled by increasing adoption of advanced automotive safety technologies, rising electric vehicle penetration, and strong demand for premium vehicle features

- Active Smart Glass are the fastest-growing technology type, projected to register a CAGR of 12.4% from 2026 to 2033, supported by rising adoption of advanced vehicle technologies and connected mobility solutions

- The Passenger Car segment dominated the vehicle type category with a 61.8% revenue share in 2025, led by high production volumes and increasing integration of safety-focused glazing solutions

- Standard safety windshield accounted for 53.1% of the market in 2025, preferred by its extensive use across passenger cars, light commercial vehicles, and heavy-duty vehicles due to its proven safety performance and affordability

- The metal coated glass segment is the fastest-growing material type category, with a CAGR of 10.1% from 2026 to 2033, driven by rising demand for advanced thermal insulation and electromagnetic shielding properties

Market Size & Forecast

- Global Market Value (2025): USD 17.64 Billion

- Expected Market Value (2033): USD 26.06 Billion

- Forecast CAGR (2026–2033): 5.00%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Report Scope and Automotive Laminated Glass Market Segmentation

|

Attributes |

Automotive Laminated Glass Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Saint-Gobain Group (France) · Asahi India Glass Limited (India) · Fuyao Glass America Inc. (U.S.) · Motherson Group (India) · Webasto Group (Germany) · Nippon Sheet Glass Co., Ltd. (Japan) · Gentex Corporation (U.S.) · Magna International Inc. (Canada) · Xinyi Glass Holdings Limited (China) · Corning Incorporated (U.S.) · Hitachi Chemical Co., Ltd. (Japan) · Showa Denko Materials Co., Ltd. (Japan) · PGW Auto Glass, LLC (U.S.) · Polytronix, Inc. (U.S.) · Vitro S.A.B. de C.V. (Mexico) · Olimpia Auto Glass Inc. (Canada) · Guardian Industries (U.S.) · Shatterprufe (South Africa) · Central Glass Co., Ltd. (Japan) |

|

Market Opportunities |

· Expansion of Electric and Autonomous Vehicle Integration · Growth in Panoramic Roof and Large Glazing Surface Demand · Rising Aftermarket Replacement Demand in Emerging Economies |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Laminated Glass Market Trends

Trend: Rising Adoption of Smart and Acoustic Laminated Glass in Electric Vehicles

Automotive manufacturers are increasingly integrating smart, acoustic, and lightweight laminated glass to enhance vehicle comfort, safety, and energy efficiency, particularly in electric and premium vehicle segments. The shift toward larger glazing areas, panoramic roofs, and advanced cockpit designs is driving strong adoption of high-performance laminated solutions. Rising demand for electrochromic and solar-control glass is also supporting the development of adaptive vehicle interiors with improved thermal management.

Companies such as Saint-Gobain Sekurit have introduced advanced acoustic laminated glass solutions for electric vehicles in Europe, improving cabin quietness and energy efficiency while supporting OEM requirements for next-generation EV platforms.

Automotive Laminated Glass Market Dynamics

Key Market Driver: Increasing Vehicle Safety Regulations and Crash Protection Standards

The growing enforcement of stringent vehicle safety regulations across major automotive markets is significantly driving demand for laminated glass, particularly in windshields and side glazing applications. Regulatory frameworks such as Euro NCAP safety standards and U.S. Federal Motor Vehicle Safety requirements are compelling OEMs to adopt high-strength laminated glazing systems. Increasing consumer awareness regarding crash safety and occupant protection is further reinforcing this demand across passenger and commercial vehicles.

Companies such as AGC Inc. and Nippon Sheet Glass Co., Ltd. are supplying advanced laminated windshields that comply with global safety standards while improving impact resistance and passenger protection in modern vehicles.

Key Restraint/Challenge: High Production Cost of Advanced Laminated Glass Technologies

The high manufacturing cost associated with advanced laminated glass technologies, including smart glass, acoustic interlayers, and lightweight composite glazing, remains a key challenge for market expansion. Complex production processes, use of specialty interlayers such as PVB and ionoplast, and integration of electronic components significantly increase overall product cost. This cost burden limits large-scale adoption in mass-market vehicles, particularly in price-sensitive emerging economies.

Corning Incorporated’s automotive Gorilla Glass solutions, while offering improved durability and weight reduction benefits, highlight the higher cost structure compared to conventional laminated glass systems, limiting their penetration primarily to premium and select OEM vehicle platforms.

Key Market Opportunity: Growth in Panoramic Roof and Large Glazing Surface Demand

The increasing consumer preference for panoramic sunroofs, large windshields, and extended side glazing is creating strong growth opportunities for automotive laminated glass manufacturers. Automakers are adopting larger laminated glass surfaces to enhance aesthetics, cabin lighting, and passenger experience while maintaining safety and structural integrity. This trend is particularly strong in SUVs, luxury vehicles, and electric vehicle platforms where design differentiation is critical.

Webasto Group has expanded its panoramic roof systems integrating advanced laminated glazing solutions, supporting OEMs in delivering enhanced cabin visibility, comfort, and premium vehicle design features across global automotive platforms.

Automotive Laminated Glass Market Scope

The Automotive Laminated Glass market is segmented on the basis of glass type, sales channel, technology, vehicle type, application, and material type.

- By Glass Type

On the basis of glass type, the automotive laminated glass market is segmented into Standard Safety Windshield, Acoustic Laminated Glass, Solar Control Glass, HUD (Head-Up Display) Glass, Heated Laminated Glass, Antenna Glass, and Bullet-Resistant Glass. The Standard Safety Windshield segment dominated the market with the largest share of 53.1% in 2025, supported by its extensive use across passenger cars, light commercial vehicles, and heavy-duty vehicles due to its proven safety performance and affordability. The segment benefits from stringent automotive safety regulations, high replacement demand in the aftermarket, and widespread adoption by automakers seeking reliable and cost-efficient glazing solutions.

The Heated Laminated Glass segment is projected to register the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by increasing demand for improved visibility and faster defogging and de-icing capabilities in adverse weather conditions. Rising adoption in premium, luxury, and electric vehicles, coupled with advancements in energy-efficient heating technologies and growing consumer preference for enhanced driving comfort and safety, is expected to accelerate segment growth.

- By Sales Channel

On the basis of sales channel, the market is segmented into original equipment manufacturer and aftermarket replacement glass. The Original Equipment Manufacturer segment dominated the market with a share of 68.7% in 2025, driven by strong integration of laminated glass in new vehicle production lines across global automotive brands. OEMs prefer laminated solutions to meet stringent safety regulations and design requirements in modern vehicles. High-volume production of passenger cars and commercial vehicles further strengthens OEM dominance. Long-term supply agreements between glass manufacturers and automakers reinforce stable demand.

The Aftermarket Replacement Glass segment is projected to register the fastest growth at a CAGR of 9.6% from 2026 to 2033, supported by rising vehicle parc and increasing incidence of windshield damage. Growing awareness of safety compliance during glass replacement is boosting demand for certified laminated products. Expansion of organized automotive repair networks and insurance-backed replacement services is accelerating adoption. Increasing vehicle ownership in developing regions is further driving aftermarket penetration.

- By Technology

On the basis of technology, the market is segmented into active smart glass and passive glass. The Passive Glass segment dominated the market with a share of 74.1% in 2025, supported by its widespread usage in standard automotive glazing applications and lower production costs. Passive laminated glass offers reliable safety and durability without requiring electronic integration, making it suitable for mass-market vehicles. Established manufacturing processes and large-scale OEM adoption further reinforce dominance. Consistent demand across passenger and commercial vehicle segments sustains its leading position.

The Active Smart Glass segment is projected to register the fastest growth at a CAGR of 12.4% from 2026 to 2033, driven by rising adoption of advanced vehicle technologies and connected mobility solutions. Smart laminated glass with electrochromic and adaptive tinting features is gaining traction in premium and luxury vehicles. Increasing consumer preference for enhanced comfort, UV protection, and energy efficiency is accelerating integration. Automotive electrification trends and intelligent cabin systems are further supporting segment expansion.

- By Vehicle Type

On the basis of vehicle type, the market is segmented into passenger cars, light commercial vehicles, trucks, and buses. The Passenger Cars segment dominated the market with a share of 61.8% in 2025, driven by high production volumes and increasing integration of safety-focused glazing solutions. Growing demand for comfort, noise reduction, and advanced driver assistance system compatibility is boosting laminated glass adoption. OEM emphasis on passenger safety standards further strengthens segment dominance. Expanding urban mobility and rising car ownership contribute to sustained demand.

The Light Commercial Vehicle segment is projected to register the fastest growth at a CAGR of 9.3% from 2026 to 2033, supported by rapid growth in logistics, e-commerce, and last-mile delivery services. Increasing fleet modernization is driving demand for durable and safety-enhanced glazing solutions. Manufacturers are incorporating laminated glass to improve driver protection and operational reliability. Rising commercial transportation activities in emerging economies are further accelerating segment growth.

- By Application

On the basis of application, the market is segmented into windshield, sidelite, backlite, rear quarter glass, sideview mirror, and rearview mirror. The Windshield segment dominated the market with a share of 58.6% in 2025, driven by mandatory safety regulations and extensive use of laminated glass for impact resistance and passenger protection. Advanced driver assistance systems are increasingly integrated into windshield assemblies, further boosting demand. OEM preference for laminated windshields in both passenger and commercial vehicles strengthens market leadership. Continuous innovation in acoustic and UV protection properties enhances adoption.

The Sidelite segment is projected to register the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by rising demand for improved cabin safety and noise insulation in side windows. Increasing use of laminated glass in premium vehicles for enhanced break-in resistance is supporting adoption. Automotive manufacturers are focusing on passenger comfort and structural safety enhancements. Growing penetration of advanced glazing solutions in mid-range vehicles is further accelerating segment expansion.

- By Material Type

On the basis of material type, the market is segmented into metal coated glass, tinted glass, and others. The Tinted Glass segment dominated the market with a share of 49.2% in 2025, driven by strong demand for heat reduction, glare control, and enhanced aesthetic appeal in modern vehicles. Automakers increasingly integrate tinted laminated glass to improve cabin comfort and energy efficiency. High adoption across passenger cars and SUVs further strengthens segment leadership. Established production capabilities and cost-effective manufacturing support widespread usage.

The Metal Coated Glass segment is projected to register the fastest growth at a CAGR of 10.1% from 2026 to 2033, driven by rising demand for advanced thermal insulation and electromagnetic shielding properties. Increasing adoption in electric and luxury vehicles is accelerating integration of coated laminated glass solutions. Manufacturers are focusing on improving solar control performance to enhance vehicle energy efficiency. Expanding application in smart mobility and premium automotive designs is further supporting segment growth.

Automotive Laminated Glass Market Regional Analysis

Asia-Pacific dominated the automotive laminated glass market and accounted for the largest revenue share of 45% in 2025, supported by high vehicle production volumes, strong automotive OEM presence, and expanding demand for safety and comfort-focused glazing solutions. The region benefits from cost-efficient manufacturing ecosystems, large-scale supply chains, and rapid adoption of advanced automotive technologies. Rising passenger vehicle sales, growing premium vehicle penetration, and increasing regulatory emphasis on occupant safety are accelerating market expansion. Strong investments in electric vehicles and smart mobility solutions further reinforce regional dominance.

China Automotive Laminated Glass Market Insight

China held the largest share in the Asia-Pacific automotive laminated glass market in 2025, supported by its dominant position in global automotive manufacturing and extensive OEM production base. The country benefits from large-scale integration of laminated glass in passenger cars, electric vehicles, and commercial fleets driven by stringent safety regulations. Strong domestic demand for advanced glazing solutions is supported by rising consumer preference for noise reduction, UV protection, and enhanced cabin comfort. In addition, rapid expansion of electric vehicle production and smart cockpit technologies is significantly strengthening China’s leadership in the regional market.

India Automotive Laminated Glass Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by increasing vehicle ownership, expanding automotive manufacturing capacity, and rising demand for safety-enhanced glazing solutions. Growth in passenger car production, coupled with strong expansion in the light commercial vehicle segment, is accelerating laminated glass adoption. OEMs are increasingly integrating laminated windshields to comply with evolving safety standards and improve passenger protection. In addition, rising urbanization, infrastructure development, and growth in ride-hailing and logistics services are further supporting long-term market expansion.

Europe Automotive Laminated Glass Market Insight

The Europe automotive laminated glass market is expanding steadily, supported by stringent vehicle safety regulations, strong adoption of advanced driver assistance systems, and high demand for premium vehicles. The region benefits from a well-established automotive industry with strong focus on sustainability, lightweight materials, and energy-efficient vehicle designs. Increasing integration of acoustic and solar-control laminated glass in electric and luxury vehicles is further driving demand. In addition, rising emphasis on reducing vehicle emissions and improving passenger comfort is strengthening regional market growth.

Germany Automotive Laminated Glass Market Insight

Germany accounted for the largest share in the Europe automotive laminated glass market in 2025, driven by its strong automotive manufacturing base and leadership in premium vehicle production. The country has extensive adoption of laminated glazing in luxury vehicles, electric cars, and high-performance automotive segments. Strong focus on vehicle safety, acoustic insulation, and advanced cockpit design is further supporting market demand. In addition, presence of leading automotive OEMs and glass technology suppliers is reinforcing Germany’s dominant position in the regional market.

U.K. Automotive Laminated Glass Market Insight

The U.K. market is supported by rising demand for advanced safety glazing solutions across passenger vehicles and commercial fleets. Increasing adoption of electric vehicles and connected mobility solutions is driving demand for smart and high-performance laminated glass. Consumer preference for comfort, UV protection, and noise reduction is further boosting market penetration. In addition, strong automotive aftermarket activity and growing focus on vehicle safety standards are supporting steady market growth.

North America Automotive Laminated Glass Market Insight

North America is projected to grow at the fastest CAGR of 7.35% from 2026 to 2033, driven by increasing adoption of advanced automotive safety technologies, rising electric vehicle penetration, and strong demand for premium vehicle features. The region benefits from high consumer awareness regarding crash safety standards and growing integration of laminated glass in windshields and side glazing. Expanding automotive production and strong aftermarket replacement demand are further accelerating growth. In addition, rising investments in autonomous and connected vehicles are reinforcing regional expansion.

U.S. Automotive Laminated Glass Market Insight

The U.S. accounted for the largest share in the North America automotive laminated glass market in 2025, supported by strong automotive OEM presence and high demand for safety-enhanced vehicles. The country has extensive adoption of laminated glass in passenger cars, SUVs, and electric vehicles driven by strict safety regulations and insurance standards. Growing consumer preference for acoustic comfort, UV protection, and advanced driver assistance system compatibility is further strengthening demand. In addition, well-developed automotive aftermarket networks and rising vehicle parc are reinforcing the U.S. leadership position in the regional market.

Automotive Laminated Glass Market Share

The automotive laminated glass industry is primarily led by well-established companies, including:

- Saint-Gobain Group (France)

- Asahi India Glass Limited (India)

- Fuyao Glass America Inc. (U.S.)

- Motherson Group (India)

- Webasto Group (Germany)

- Nippon Sheet Glass Co., Ltd. (Japan)

- Gentex Corporation (U.S.)

- Magna International Inc. (Canada)

- Xinyi Glass Holdings Limited (China)

- Corning Incorporated (U.S.)

- Hitachi Chemical Co., Ltd. (Japan)

- Showa Denko Materials Co., Ltd. (Japan)

- PGW Auto Glass, LLC (U.S.)

- Polytronix, Inc. (U.S.)

- Vitro S.A.B. de C.V. (Mexico)

- Olimpia Auto Glass Inc. (Canada)

- Guardian Industries (U.S.)

- Shatterprufe (South Africa)

- Central Glass Co., Ltd. (Japan)

Latest Developments in Automotive Laminated Glass Market

- In March 2025, AGC Inc. expanded its collaboration with Gauzy for smart laminated glass solutions. This development has strengthened the automotive laminated glass market by accelerating the commercialization of electrochromic and SPD-based glazing systems. The integration of switchable laminated glass into windshields, panoramic roofs, and side windows is enhancing vehicle comfort, safety, and energy efficiency. It is also increasing adoption in premium and electric vehicle segments where demand for adaptive cabin environments is rising. The collaboration is further supporting OEMs in differentiating vehicle interiors through advanced glazing technologies

- In January 2025, Fuyao Glass America expanded production capacity in Ohio, U.S. This expansion has positively impacted the automotive laminated glass market by improving regional supply availability for major North American OEMs. Increased production capacity for laminated and tempered glass is reducing lead times and strengthening local sourcing strategies. It is also supporting growing demand from EV and SUV manufacturers requiring high-performance safety glazing. The move enhances supply chain resilience while reinforcing Fuyao’s competitive positioning in the global automotive glass ecosyste

- In November 2024, Corning expanded automotive adoption of Gorilla Glass in windshield applications. This development has influenced the automotive laminated glass market by driving demand for lightweight, durable glazing alternatives in modern vehicles. The increasing use of Gorilla Glass in collaboration with OEMs such as Ford is improving vehicle weight reduction and fuel efficiency performance. It also enhances impact resistance and durability, supporting safety-focused design requirements. The innovation is contributing to broader acceptance of advanced hybrid laminated glass solutions in premium automotive platform

- In September 2024, Saint-Gobain Sekurit advanced acoustic laminated glass solutions for electric vehicles. This development has strengthened the automotive laminated glass market by addressing rising demand for cabin noise reduction and thermal comfort in EVs. Enhanced acoustic laminated glass is improving passenger experience by minimizing road and wind noise in electric mobility platforms. It is also supporting energy efficiency by reducing HVAC load in EV cabins. The innovation is reinforcing Saint-Gobain’s leadership in high-performance automotive glazing systems

- In July 2024, NSG Group enhanced lightweight laminated glass solutions for next-generation vehicles. This development has impacted the automotive laminated glass market by supporting vehicle weight reduction goals critical for electric and fuel-efficient vehicles. The adoption of lightweight laminated glazing is improving driving range and overall vehicle efficiency. It also aligns with OEM requirements for enhanced safety and structural performance without increasing vehicle mass. The advancement strengthens NSG Group’s role in supplying next-generation automotive glazing technologies globally

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.