Global Automotive Metal Stamping Market

Market Size in USD Billion

USD

84.46 Billion

USD

106.99 Billion

2024

2032

USD

84.46 Billion

USD

106.99 Billion

2024

2032

| 2025 - 2032 | |

| USD 84.46 Billion | |

| USD 106.99 Billion | |

| % | |

|

What is the Global Automotive Metal Stamping Market Size and Growth Rate?

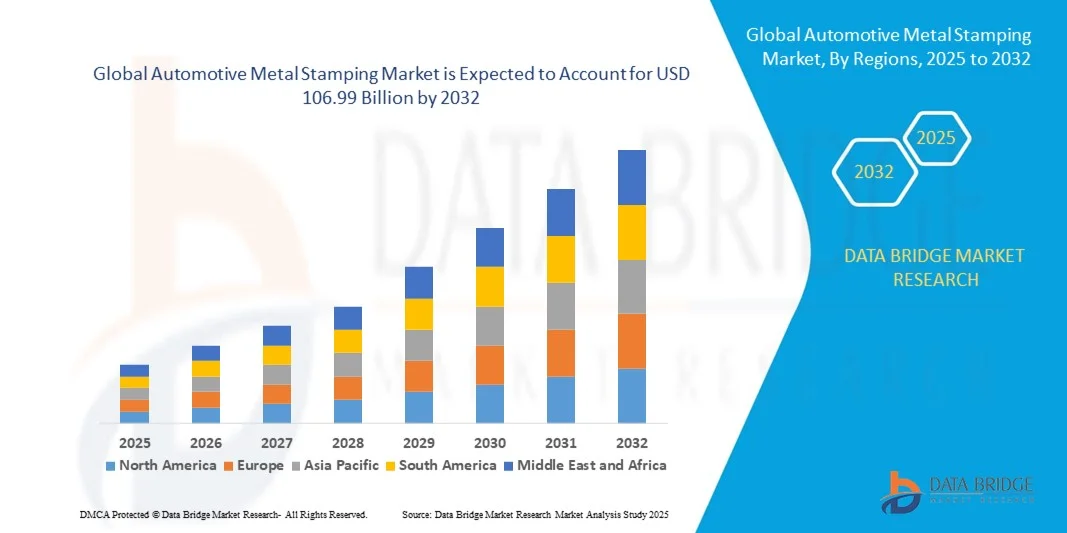

- The global automotive metal stamping market size was valued at USD 84.46 billion in 2024 and is expected to reach USD 106.99 billion by 2032, at a CAGR of 3.0% during the forecast period

- Rise in demand of the stamping machines to meet the demand of an impending growth in the automotive sector is a crucial factor accelerating the market growth, also rise in the usage of stamping machines in the automotive sector, rising demand for automobile, increasing production of the vehicle and rising presence of large number of manufacturers are the major factors among others boosting the automotive metal stamping market

What are the Major Takeaways of Automotive Metal Stamping Market?

- Rising modernization, increasing technological advancements in the machinery and rising research and development activities will further create new opportunities for automotive metal stamping market in the forecast period mentioned above

- However, rising emergence of plastics/composites as metal substitutes is the vital factor among others which will curtail the market growth, and will further challenge the automotive metal stamping market

- The Asia-Pacific region dominated the automotive metal stamping market with the largest revenue share of 41.5% in 2024, driven by rapid urbanization, industrialization, and increasing demand for high-quality automotive components

- The North America automotive metal stamping market is projected to grow at the fastest CAGR of 9.14% during 2025–2032, driven by increased adoption of lightweight, high-strength materials in vehicles and growing demand for electric and hybrid automobiles

- The blanking segment dominated the market with the largest revenue share of 38.5% in 2024, driven by its critical role in cutting metal sheets into precise shapes for various automotive components such as panels, chassis, and body parts

Report Scope and Automotive Metal Stamping Market Segmentation

|

Attributes |

Automotive Metal Stamping Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Automotive Metal Stamping Market?

Integration of Advanced Automation and Smart Manufacturing

- A major trend shaping the global automotive metal stamping market is the increasing incorporation of advanced automation technologies, including robotics, AI, and smart manufacturing systems. This integration is enhancing production efficiency, reducing defects, and enabling precise stamping of complex automotive components

- For instance, automated press lines equipped with AI-powered vision systems can detect material inconsistencies and adjust stamping parameters in real-time, minimizing waste and improving throughput. Similarly, robotics-assisted stamping cells allow manufacturers to handle high-strength steel with improved safety and accuracy

- AI-driven predictive maintenance in stamping operations is gaining traction, allowing manufacturers to anticipate equipment failures, reduce downtime, and optimize production schedules. Systems such as those deployed by major OEM suppliers leverage data analytics to enhance process reliability and consistency

- The integration of digital twins and Industry 4.0 platforms is facilitating centralized monitoring and control across stamping lines. Manufacturers can simulate process variations, optimize die designs, and remotely monitor performance, ensuring high-quality outputs and improved operational flexibility

- This move toward intelligent, automated, and connected stamping operations is redefining production standards in the automotive sector. Consequently, companies such as Magna International and Martinrea International are deploying AI-enabled stamping lines that deliver higher precision, improved yield, and faster production cycles

- Demand for smart, automated metal stamping solutions is rising across OEM and aftermarket segments, driven by the need for efficiency, cost reduction, and the ability to meet complex design requirements for modern vehicles

What are the Key Drivers of Automotive Metal Stamping Market?

- The growing demand for lightweight, high-strength automotive components to improve fuel efficiency and safety is a primary driver of the automotive metal stamping market. High-strength steels and advanced alloys require precision stamping processes to meet automotive specifications

- For instance, in January 2025, ArcelorMittal Nippon Steel India launched advanced automotive steel production lines designed for high-strength steel stamping, enhancing quality and enabling complex part fabrication. This demonstrates industry commitment to high-performance materials

- Increasing adoption of electric vehicles and connected cars is fueling the need for precise stamping of battery enclosures, chassis, and structural components. Manufacturers are investing in automated lines to ensure accuracy, repeatability, and compliance with stringent safety standards

- Furthermore, the trend toward smart factories and Industry 4.0 is driving investment in robotics, AI, and IoT-enabled stamping solutions, enabling seamless integration, reduced labor costs, and enhanced production monitoring

- The growing preference for outsourced stamping solutions by OEMs and tier-1 suppliers is also boosting market growth. Precision stamping providers offer high-quality, customized parts while reducing lead times and operational costs, supporting overall automotive manufacturing efficiency

Which Factor is Challenging the Growth of the Automotive Metal Stamping Market?

- The high capital expenditure required for advanced stamping equipment, robotics, and automation systems is a significant challenge, especially for small- and medium-sized manufacturers. High upfront costs can limit market entry and expansion

- For instance, investing in robotic press lines with AI-driven quality monitoring can involve multi-million-dollar budgets, which may be prohibitive for cost-sensitive suppliers in developing regions

- Skilled workforce shortages and the need for specialized training in automated stamping and Industry 4.0 technologies also hinder adoption. Manufacturers must invest in employee training and process development to maximize ROI

- Material challenges, such as handling ultra-high-strength steels and advanced alloys, require precise process control and can lead to higher defect rates without proper technology. Companies must balance production speed with quality assurance

- Addressing these challenges through financing solutions, workforce upskilling, and incremental adoption of automation technologies will be key to sustaining growth in the automotive metal stamping market

How is the Automotive Metal Stamping Market Segmented?

The market is segmented on the basis of technology, vehicle type, process, stamping process, and number of stations.

- By Technology

On the basis of technology, the automotive metal stamping market is segmented into blanking, embossing, bending, coining, flanging, and others. The blanking segment dominated the market with the largest revenue share of 38.5% in 2024, driven by its critical role in cutting metal sheets into precise shapes for various automotive components such as panels, chassis, and body parts. Blanking is widely adopted due to its efficiency, minimal material waste, and compatibility with both traditional and advanced high-strength steels.

The embossing segment is expected to witness the fastest CAGR of 22.3% from 2025 to 2032, fueled by the increasing demand for decorative and functional surface features in automotive interiors and exteriors. Rising adoption of embossed designs for aesthetic appeal and functional reinforcement, combined with automated embossing presses, is driving growth. Overall, the technology segment reflects the industry’s push for precision, efficiency, and innovative design integration.

- By Vehicle Type

On the basis of vehicle type, the automotive metal stamping market is segmented into passenger vehicles, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs). The passenger vehicle segment held the largest market revenue share of 47% in 2024, driven by the high production volume of passenger cars globally and the requirement for lightweight, high-strength components to meet fuel efficiency and safety standards.

LCVs are expected to witness the fastest CAGR of 21% from 2025 to 2032, due to rising demand for delivery vehicles, vans, and urban mobility solutions, which require precision metal stamping for chassis, cargo compartments, and structural reinforcements. Technological advancements in stamping processes tailored for LCV components, combined with increasing vehicle production in emerging markets, are contributing to the rapid growth of this segment. The vehicle type segmentation highlights the critical role of stamped components in both mass-market and specialized automotive applications.

- By Process

On the basis of process, the automotive metal stamping market is segmented into roll forming, hot stamping, sheet metal forming, metal fabrication, and other processes. The sheet metal forming segment dominated the market with the largest revenue share of 42% in 2024, due to its extensive use in producing automotive body panels, structural frames, and chassis components. Sheet metal forming offers versatility, compatibility with advanced steels, and high production efficiency, making it essential for passenger and commercial vehicles asuch as.

Hot stamping is expected to witness the fastest CAGR of 23% from 2025 to 2032, driven by the growing adoption of ultra-high-strength steels (UHSS) in automotive safety-critical components. Hot stamping enables enhanced strength-to-weight ratios, precise dimensional control, and crashworthiness, aligning with automotive industry trends toward lightweight, high-performance vehicles. The process segmentation emphasizes efficiency, quality, and innovation in automotive component manufacturing.

- By Stamping Process

On the basis of stamping process, the market is segmented into mechanical, hydraulic, and pneumatic processes. The mechanical stamping segment held the largest market revenue share of 40% in 2024, owing to its high precision, repeatability, and suitability for high-volume automotive production. Mechanical stamping is widely used for critical body and structural components where consistent tolerances are crucial.

The hydraulic stamping segment is expected to witness the fastest CAGR of 21.5% from 2025 to 2032, driven by its ability to handle thicker and high-strength materials, particularly for chassis, powertrain, and commercial vehicle components. Hydraulic presses enable complex forming operations and reduce the risk of material cracking or deformation. Overall, the stamping process segmentation reflects manufacturers’ focus on optimizing throughput, material utilization, and component quality.

- By Number of Stations

On the basis of the number of stations, the automotive metal stamping market is segmented into single tool stations and progressive stations. The progressive stations segment dominated the market with the largest revenue share of 44% in 2024, due to its efficiency in performing multiple sequential operations on metal sheets, reducing labor requirements and increasing production speed.

Single tool stations are expected to witness the fastest CAGR of 20.8% from 2025 to 2032, driven by demand for low-volume, specialized, and custom automotive components. Manufacturers adopting single tool stations benefit from flexibility, lower capital investment, and adaptability to different part designs. The segmentation by number of stations emphasizes operational efficiency, scalability, and responsiveness to evolving automotive production demands.

Which Region Holds the Largest Share of the Automotive Metal Stamping Market?

- The Asia-Pacific region dominated the automotive metal stamping market with the largest revenue share of 41.5% in 2024, driven by rapid urbanization, industrialization, and increasing demand for high-quality automotive components

- Consumers and manufacturers in APAC highly value cost-effective, technologically advanced, and lightweight metal stamping solutions, contributing to wide adoption across passenger vehicles, light commercial vehicles, and heavy commercial vehicles

- This dominance is further supported by the presence of large-scale automotive manufacturing hubs, increasing investments in advanced stamping technologies, and growing automotive exports, establishing APAC as the primary revenue contributor to the global market

China Automotive Metal Stamping Market Insight

The China market accounted for the largest revenue share of 42% in APAC in 2024, fueled by rapid industrial growth, rising vehicle production, and adoption of advanced high-strength steels. China’s automotive sector increasingly integrates precision stamping solutions for chassis, body panels, and structural components. Government support for smart factories, along with the push for electric and hybrid vehicles, is driving further adoption. Strong domestic manufacturers and growing exports are key contributors to market leadership in China.

Japan Automotive Metal Stamping Market Insight

The Japan market is witnessing steady growth, driven by a high-tech automotive culture and precision engineering standards. Japanese manufacturers are adopting advanced stamping processes, including hot stamping and roll forming, to produce lightweight, safe, and eco-friendly vehicles. Increasing demand for high-strength automotive components and electric vehicles supports growth. Integration of advanced automation and IoT-enabled quality control is also fueling adoption, ensuring Japan remains a significant contributor to the APAC market.

India Automotive Metal Stamping Market Insight

The India market is expanding rapidly due to growing domestic vehicle production, rising disposable incomes, and increasing adoption of safety standards. Automotive Metal Stampings are widely applied in passenger and commercial vehicles to improve performance and safety. Government incentives for automotive manufacturing and the development of industrial clusters are accelerating market growth. Rising exports and investments from global automakers are also strengthening India’s position in the APAC market.

Which Region is the Fastest Growing Region in the Automotive Metal Stamping Market?

The North America automotive metal stamping market is projected to grow at the fastest CAGR of 9.14% during 2025–2032, driven by increased adoption of lightweight, high-strength materials in vehicles and growing demand for electric and hybrid automobiles. Expansion of automotive manufacturing, automation in production lines, and demand for precision-stamped components are key growth factors. In addition, North America’s focus on sustainability, energy-efficient manufacturing, and innovation in stamping technologies is accelerating regional market growth.

U.S. Automotive Metal Stamping Market Insight

The U.S. market captured the largest revenue share of 81% in North America in 2024, fueled by investments in advanced stamping technologies, electric vehicle production, and rising adoption of automated processes. Manufacturers are increasingly leveraging robotics and high-precision stamping solutions to enhance efficiency and quality. The growing emphasis on lightweight vehicles and safety compliance is also driving demand. The U.S. market is expected to remain the fastest-growing in the forecast period due to continuous technological innovation and strong automotive sector recovery.

Canada Automotive Metal Stamping Market Insight

The Canada market is witnessing steady growth with rising vehicle manufacturing and exports. Adoption of advanced metal stamping processes for automotive components, coupled with government incentives for electric vehicles and industrial automation, is fueling expansion. The country’s emphasis on sustainable production and precision manufacturing further supports market growth. Rising investments in tooling, presses, and automated quality control systems are expected to continue driving Canada’s market growth during the forecast period.

Which are the Top Companies in Automotive Metal Stamping Market?

The automotive metal stamping industry is primarily led by well-established companies, including:

- Alcoa Corporation (U.S.)

- Martinrea International Inc. (Canada)

- Shiloh Industries (U.S.)

- ACRO Building Systems (U.S.)

- Manor Tool & Manufacturing (U.S.)

- Lindy Manufacturing Co Inc (U.S.)

- American Industrial Co (U.S.)

- Kenmode, Inc. (U.S.)

- Wisconsin Metal Parts, Inc. (U.S.)

- Clow Stamping Company (U.S.)

- ARO Metal Stamping Co Inc (U.S.)

- Tempco Manufacturing Company, Inc. (U.S.)

- Interplex Holdings Pte. Ltd. (Singapore)

- D&H Industries, Inc. (U.S.)

- PDQ Tool & Stamping Co. (U.S.)

- Magna International Inc.

- (Canada)

- Goshen Stamping Company (U.S.)

- Caparo Group (U.K.)

What are the Recent Developments in Global Automotive Metal Stamping Market?

- In March 2025, Hyundai Steel committed USD 5.8 billion to build an electric-arc-furnace complex in Louisiana, aimed at producing 2.7 million tonnes of automotive plate annually from 2029, marking a major step in strengthening its automotive steel production capabilities and supporting future vehicle manufacturing demand

- In March 2025, Techint Engineering & Construction secured a USD 255 million contract to expand Vinton Steel’s Texas mill to 400,000 tonnes per year using Tenova’s energy-efficient process, reflecting ongoing investments in sustainable and high-capacity steel production solutions

- In February 2025, Standex International acquired McStarlite Co. for USD 56.5 million, adding specialized cold deep-draw expertise to its engineered products portfolio, thereby enhancing its capabilities in precision metal components for diverse industrial applications

- In February 2025, Architect Equity purchased Gibbs Die Casting Corporation, bolstering its precision aluminum capabilities for multi-energy powertrains and strengthening its position in the evolving automotive and clean energy sectors

- In June 2024, BMW Manufacturing inaugurated a state-of-the-art press shop at its Spartanburg facility, capable of producing up to 10,000 components daily, which will support the manufacturing of BMW X3 body parts such as doors, fenders, and liftgate, significantly enhancing production efficiency and capacity

- In May 2024, BENTELER Group inaugurated a new plant in Bratislava, Slovakia, strategically located near Volkswagen, enabling efficient production, assembly, and logistics for the European market, and reinforcing its role as a key supplier in the region

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Automotive Metal Stamping Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Automotive Metal Stamping Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Automotive Metal Stamping Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.