Global Automotive Platooning System Market

Market Size in USD Billion

USD

1.70 Billion

USD

8.50 Billion

2024

2032

USD

1.70 Billion

USD

8.50 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.70 Billion | |

| USD 8.50 Billion | |

| % | |

|

Automotive Platooning System Market Size

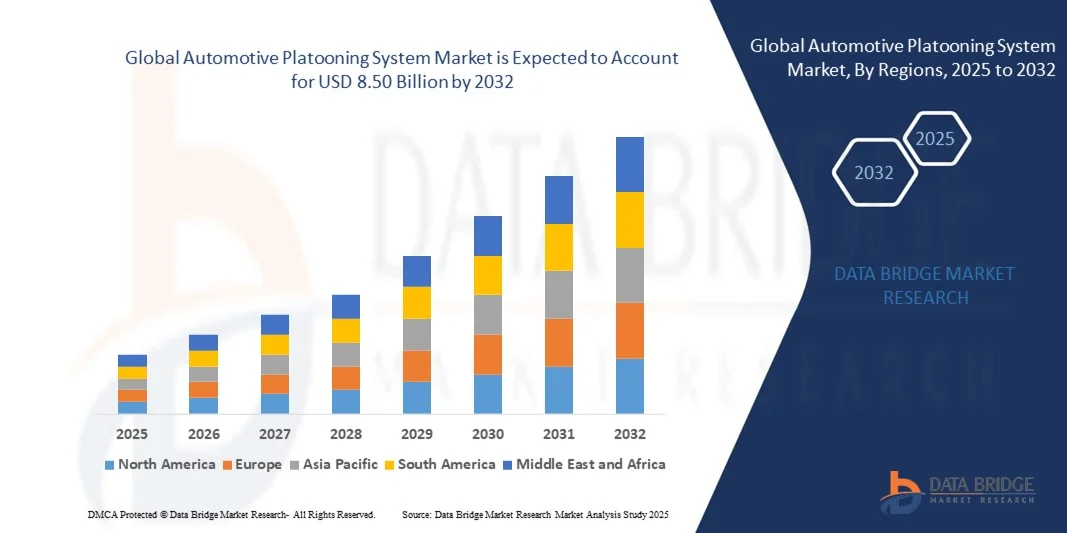

- The global automotive platooning system market size was valued at USD 1.70 billion in 2024 and is expected to reach USD 8.50 billion by 2032, at a CAGR of 22.30% during the forecast period

- The market growth is largely fuelled by the increasing demand for connected and autonomous vehicle technologies, growing emphasis on road safety, and the need to reduce fuel consumption and emissions in commercial transportation

- The rising adoption of advanced driver assistance systems (ADAS), government initiatives promoting intelligent transportation systems, and increasing investments by OEMs and tech companies in platooning solutions are further driving market expansion

Automotive Platooning System Market Analysis

- The market is witnessing rapid technological advancements, including vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication systems, which enable coordinated driving and enhance platooning efficiency

- Increasing collaborations between automotive manufacturers, technology providers, and logistics companies are facilitating large-scale pilot programs and commercial deployment of platooning systems

- North America dominated the automotive platooning system market with the largest revenue share of 38.50% in 2024, driven by a growing demand for connected and autonomous vehicle technologies, as well as supportive government policies for intelligent transportation systems

- Asia-Pacific region is expected to witness the highest growth rate in the global automotive platooning system market, driven by rising investments in intelligent transportation infrastructure, growing adoption of autonomous vehicle technologies, and increasing demand for fuel-efficient and safe long-haul transport solutions

- The HCV segment held the largest market revenue share in 2024, driven by the extensive use of long-haul trucks in freight and logistics operations. HCVs benefit the most from platooning systems due to their higher fuel consumption, longer travel distances, and greater operational costs, making platooning an ideal solution for improving efficiency, safety, and route coordination

Report Scope and Automotive Platooning System Market Segmentation

|

Attributes |

Automotive Platooning System Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Platooning System Market Trends

Rise of Connected and Autonomous Vehicle Platooning Systems

- The growing adoption of automotive platooning systems is transforming the transportation and logistics landscape by enabling synchronized and automated vehicle convoys. These systems improve road safety, reduce fuel consumption, and optimize traffic flow, especially on highways with long-haul freight operations, resulting in lower operational costs and enhanced efficiency. In addition, platooning allows for more predictable arrival times and reduces overall traffic congestion, benefiting fleet operators and end consumers alike. The integration of AI-driven control systems further enhances coordination and reliability within the platoon

- The high demand for intelligent transportation solutions in commercial trucking and logistics fleets is accelerating the deployment of vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication systems. These solutions are particularly effective in reducing driver fatigue and enhancing coordination across multiple vehicles in a platoon, ensuring timely and efficient cargo movement. Real-time data exchange between vehicles improves route optimization, load balancing, and hazard detection. Moreover, advanced platooning systems contribute to lower insurance premiums due to enhanced safety features

- The scalability and modularity of modern platooning systems are making them attractive for both large fleet operators and small logistics companies. Fleet managers benefit from reduced fuel expenses, improved convoy management, and real-time monitoring capabilities without requiring extensive modifications to existing vehicles. Modular solutions also allow operators to gradually equip their fleets with platooning technology, minimizing upfront costs. Enhanced telematics integration enables predictive maintenance, reducing downtime and overall fleet management costs

- For instance, in 2023, several European and North American trucking companies implemented platooning solutions on key highway corridors, resulting in improved fuel efficiency, decreased accident rates, and enhanced route coordination across long-haul operations. Operators reported smoother convoy operations and better adherence to delivery schedules. These successful deployments have encouraged further investment in autonomous and semi-autonomous technologies across the global logistics industry

- While platooning systems are accelerating operational efficiency and safety, their impact depends on continued technological innovation, standardization of communication protocols, and driver training. Manufacturers and service providers must focus on interoperability, AI-driven control, and cost-effective solutions to fully capitalize on the growing demand. Collaboration with regulatory authorities and infrastructure providers is also critical to ensure legal compliance and seamless adoption across regions

Automotive Platooning System Market Dynamics

Driver

Increasing Demand for Fuel Efficiency and Safe Long-Haul Transportation

- The rise in fuel prices and environmental regulations is pushing fleet operators to adopt platooning systems that optimize vehicle spacing and reduce aerodynamic drag. This leads to significant fuel savings and lower carbon emissions, encouraging investment in connected vehicle technologies. Moreover, fuel-efficient operations help fleets meet stringent sustainability targets and corporate social responsibility goals, increasing their market competitiveness

- Logistics companies are increasingly aware of the safety benefits associated with automated platooning, including collision prevention, consistent speed management, and reduced driver workload. This awareness is driving higher adoption across freight, e-commerce, and commercial trucking sectors. Reduced driver stress and improved compliance with working-hour regulations also enhance operational efficiency. Real-time monitoring of vehicle parameters ensures prompt interventions in case of anomalies, further strengthening fleet safety

- Government initiatives supporting intelligent transportation systems (ITS) and connected vehicle research are fostering investments in platooning technologies. From pilot programs to regulatory frameworks, supportive policies are enabling safer and more efficient deployment. Funding and grants for autonomous vehicle testing have encouraged manufacturers to develop standardized platooning solutions that can scale across different regions

- For instance, in 2022, several U.S. and European regulatory authorities conducted autonomous platooning trials to evaluate safety, traffic integration, and fuel savings, boosting adoption among forward-thinking fleet operators. These trials helped refine communication protocols, collision avoidance algorithms, and platoon formation strategies. Lessons learned from pilot programs have facilitated wider industry adoption and investor confidence

- While operational cost savings and regulatory support are driving the market, challenges such as infrastructure readiness, vehicle interoperability, and cybersecurity risks must be addressed for long-term adoption. Fleet operators and technology providers need to collaborate on secure data exchange, robust encryption, and standardization to prevent potential vulnerabilities. Policy alignment across countries is also essential for cross-border platooning operations

Restraint/Challenge

High Cost of Platooning Technology and Infrastructure Integration

- The high price of advanced platooning systems, including V2V communication modules, adaptive cruise control, and automated braking systems, limits accessibility for small and mid-sized fleet operators. Capital-intensive investments remain a significant barrier to widespread deployment. In addition, retrofitting existing fleets with platooning technology can require substantial modification, further increasing costs. Financial incentives or leasing models are often necessary to encourage adoption among smaller operators

- Many logistics companies lack trained personnel capable of implementing and maintaining platooning solutions. The absence of skilled workforce and supporting infrastructure further reduces adoption, particularly in developing regions. Comprehensive training programs, driver certifications, and specialized technical support are critical to ensure proper system operation and maintenance. Without trained staff, operational risks and system failures may reduce confidence in the technology

- Infrastructure challenges, including highway compatibility, roadside connectivity, and regulatory harmonization, can hinder platoon formation and efficiency. Variability in road conditions and traffic rules across regions may increase operational complexity and costs. Intelligent transport infrastructure, such as dedicated platooning lanes and connected traffic management systems, is needed to maximize benefits. Collaboration with government and private stakeholders is essential for successful integration

- For instance, in 2023, several Asian and African logistics operators reported delays in deploying platooning fleets due to insufficient infrastructure, limited driver training, and fragmented regulatory frameworks. These limitations reduced the potential operational efficiency and return on investment for early adopters. Pilot programs and phased deployment approaches are often used to mitigate these challenges

- While platooning technologies continue to evolve, addressing cost, technical complexity, and infrastructure gaps is crucial. Market stakeholders must focus on modular solutions, standardization, and workforce training to expand adoption and ensure sustainable growth. Ongoing R&D investments, public-private partnerships, and regulatory alignment will be key to enabling global scale deployment of platooning systems

Automotive Platooning System Market Scope

The market is segmented on the basis of vehicle type and mode of communication.

- By Vehicle Type

On the basis of vehicle type, the automotive platooning system market is segmented into Light Commercial Vehicles (LCVs) and Heavy Commercial Vehicles (HCVs). The HCV segment held the largest market revenue share in 2024, driven by the extensive use of long-haul trucks in freight and logistics operations. HCVs benefit the most from platooning systems due to their higher fuel consumption, longer travel distances, and greater operational costs, making platooning an ideal solution for improving efficiency, safety, and route coordination.

The LCV segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by increasing demand for last-mile delivery solutions, urban freight optimization, and smaller fleet operators adopting cost-efficient technologies. Platooning systems for LCVs offer improved fuel efficiency, reduced traffic congestion, and enhanced safety in dense urban settings, making them attractive for e-commerce and logistics service providers.

- By Mode of Communication

On the basis of mode of communication, the market is segmented into Vehicle-to-Vehicle (V2V) and Vehicle-to-Infrastructure (V2I) systems. The V2V segment held the largest market share in 2024, driven by the need for real-time data exchange between vehicles within a platoon to maintain optimal speed, spacing, and coordination. V2V communication ensures synchronized braking, acceleration, and lane management, which significantly reduces accident risks and improves operational efficiency.

The V2I segment is expected to witness the fastest growth rate from 2025 to 2032, propelled by increasing deployment of smart highways, connected traffic management systems, and roadside infrastructure supporting autonomous and semi-autonomous platooning. V2I systems enhance route planning, congestion management, and predictive maintenance, making them essential for future intelligent transportation ecosystems.

Automotive Platooning System Market Regional Analysis

- North America dominated the automotive platooning system market with the largest revenue share of 38.50% in 2024, driven by a growing demand for connected and autonomous vehicle technologies, as well as supportive government policies for intelligent transportation systems

- Fleet operators and logistics companies in the region highly value the fuel efficiency, safety benefits, and operational cost savings offered by platooning solutions

- This widespread adoption is further supported by advanced highway infrastructure, high fleet density, and strong investment in digital transportation technologies, establishing platooning systems as a preferred solution for both long-haul freight and commercial vehicle fleets

U.S. Automotive Platooning System Market Insight

The U.S. automotive platooning system market captured the largest revenue share in 2024 within North America, fueled by the increasing deployment of connected vehicle technologies and autonomous driving initiatives. Logistics and transportation companies are prioritizing fuel savings, reduced accident risks, and enhanced fleet coordination. The growing trend of smart highways and vehicle-to-vehicle (V2V) integration further propels market adoption. Moreover, government support through ITS pilot programs and autonomous vehicle testing initiatives is significantly contributing to the market’s expansion.

Europe Automotive Platooning System Market Insight

The Europe automotive platooning system market is expected to witness the fastest growth rate from 2025 to 2032, primarily driven by stringent emissions regulations, rising fuel costs, and the need for safer and more efficient freight operations. Increasing urbanization, coupled with demand for intelligent transport solutions, is fostering the adoption of platooning systems across commercial fleets. European fleet operators are also drawn to reduced operational costs and improved highway throughput. The region is witnessing significant growth across logistics, e-commerce, and long-haul transportation applications.

U.K. Automotive Platooning System Market Insight

The U.K. automotive platooning system market is expected to witness strong growth from 2025 to 2032, driven by the increasing adoption of autonomous and connected vehicle technologies, coupled with government initiatives promoting intelligent transportation. Logistics and freight companies are investing in platooning to enhance fuel efficiency, safety, and operational efficiency. The U.K.’s well-developed highway network and technological infrastructure are expected to continue stimulating market growth.

Germany Automotive Platooning System Market Insight

The Germany automotive platooning system market is expected to witness notable growth from 2025 to 2032, fueled by a strong focus on road safety, advanced automotive technologies, and the integration of connected vehicle solutions. Germany’s highly developed transportation infrastructure, coupled with stringent regulatory standards and a proactive approach toward autonomous driving technologies, promotes the adoption of platooning systems. Integration with fleet management platforms and V2V communication is becoming increasingly prevalent, supporting both commercial and industrial transport operations.

Asia-Pacific Automotive Platooning System Market Insight

The Asia-Pacific automotive platooning system market is expected to witness the fastest growth rate from 2025 to 2032, driven by rapid urbanization, increasing logistics demand, and government initiatives to implement intelligent transportation systems in countries such as China, Japan, and India. The region’s expanding commercial vehicle fleets and rising focus on fuel efficiency and road safety are accelerating adoption. Furthermore, APAC is emerging as a key market for the development and manufacturing of connected vehicle technologies, improving accessibility and affordability of platooning solutions for a wider range of fleet operators.

Japan Automotive Platooning System Market Insight

The Japan automotive platooning system market is expected to witness significant growth from 2025 to 2032, driven by the country’s high adoption of autonomous vehicle technologies, advanced road infrastructure, and focus on fuel efficiency and safety in freight operations. Japanese logistics and transportation companies are increasingly implementing platooning systems to optimize fleet coordination and reduce operational costs. The integration of V2V and V2I communication technologies, along with AI-based control systems, is further propelling market adoption in both commercial and industrial sectors.

China Automotive Platooning System Market Insight

The China automotive platooning system market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, growing commercial vehicle fleets, and the country’s push toward smart highway initiatives. China is heavily investing in intelligent transportation systems and autonomous vehicle technologies, driving widespread adoption of platooning solutions. The increasing focus on fuel efficiency, safety, and operational optimization, alongside supportive government policies, are key factors contributing to market growth in the region.

Automotive Platooning System Market Share

The Automotive Platooning System industry is primarily led by well-established companies, including:

- Peloton Technology (U.S.)

- Scania (Sweden)

- Volvo Car Corporation (Sweden)

- Continental AG (Germany)

- Delphi Technologies (U.K.)

- IVECO (Italy)

- MAN (Germany)

- Meritor, Inc (U.S.)

- Navistar, Inc. (U.S.)

- NGP Capital (U.K.)

- TomTom International BV (Netherlands)

- Robert Bosch GmbH (Germany)

- Delphi Automotive Plc (U.K.)

- Continental AG (Germany)

- Valeo (France)

- Autoliv Inc (U.S.)

- Omnivision Technologies Inc (U.S.)

Latest Developments in Global Automotive Platooning System Market

- In December 2025, Parallel Systems, headquartered in California, demonstrated its autonomous battery-electric rail vehicle platooning operations for the first time, highlighting the potential for energy-efficient and synchronized freight transport. This innovation is expected to enhance operational efficiency, reduce emissions, and set new benchmarks for sustainable logistics, positively influencing the adoption of autonomous platooning solutions in the market

- In September 2025, Vodafone Group Plc, based in the U.K., introduced the Safer Transport for Europe Platform (STEP), a cutting-edge technology aimed at enabling safer cooperative vehicle platooning via cellular communications. This development is designed to improve convoy safety, optimize traffic flow, and support the broader adoption of connected and autonomous platooning systems, strengthening market confidence in intelligent transportation solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.