Global Automotive Semiconductor Market

Market Size in USD Billion

USD

39.74 Billion

USD

92.91 Billion

2025

2033

USD

39.74 Billion

USD

92.91 Billion

2025

2033

| 2026 - 2033 | |

| USD 39.74 Billion | |

| USD 92.91 Billion | |

| % | |

|

Automotive Semiconductor Market Overview

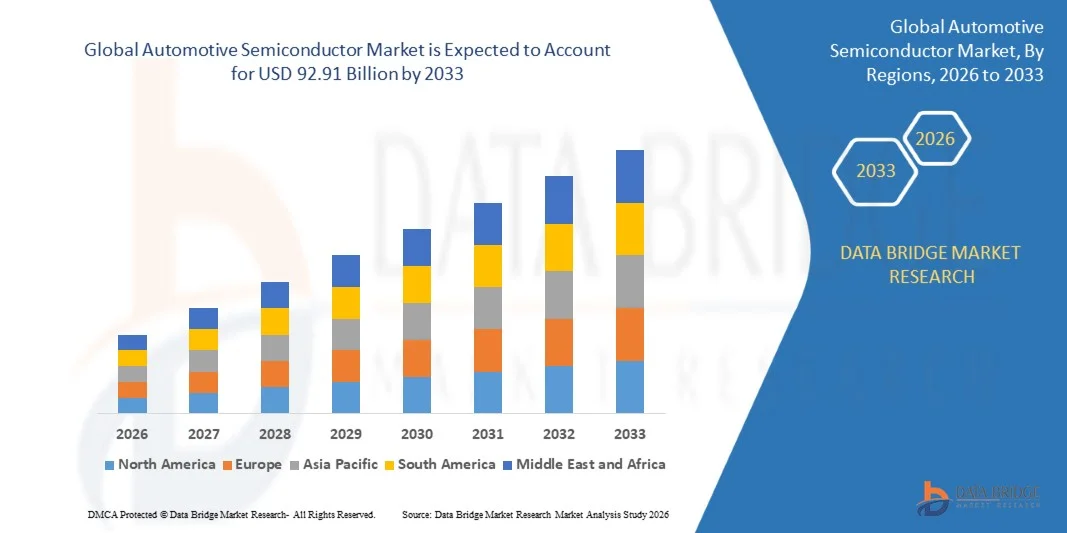

As per Data Bridge Market Research analysis, the automotive semiconductor market was valued at USD 39.74 billion in 2025 and is projected to reach USD 92.91 billion by 2033, growing at a CAGR of 11.2% from 2026 to 2033. The market is experiencing consistent growth driven by increasing penetration of electronic components in vehicles, rising adoption of electronic control units (ECUs), growing demand for advanced vehicle safety systems, and expanding integration of connected car technologies.

The increasing adoption of electric vehicles, autonomous driving technologies, and advanced driver assistance systems (ADAS), combined with growing focus on vehicle safety, connectivity, and fuel efficiency standards, is compelling automotive manufacturers to integrate advanced semiconductor solutions. Discrete power semiconductors, sensors, processors, and memory components are enabling enhanced vehicle electrification, real-time monitoring, connectivity, and intelligent mobility solutions, creating significant growth opportunities for automotive semiconductor manufacturers.

Market Size & Forecast

- Global Market Value (2025): USD 39.74 Billion

- Expected Market Value (2033): USD 92.91 Billion

- Forecast CAGR (2026–2033): 11.2%

- Leading Region in 2025: Asia Pacific

- Fastest Growing Region: Europe

Key Market Trends & Insights

- Asia-Pacific dominated the automotive semiconductor market with a revenue share of 45.2% in 2025, supported by the presence of major automotive manufacturing hubs, increasing vehicle production, rising adoption of electric vehicles, and strong demand for advanced automotive electronic components across the region

- The processor segment led the market with a 30.35% share in 2025, driven by increasing demand for high-performance computing solutions in modern vehicles

- Europe is expected to be the fastest-growing region at a CAGR of 7.2% from 2026 to 2033, fueled by increasing electric vehicle adoption, stringent vehicle emission and safety regulations, and rising investments in automotive semiconductor technologies

- Sensor are the fastest-growing component type, projected to register a CAGR of 12.4%, reflecting the surge in adoption of ADAS, autonomous vehicles, and vehicle safety technologies

- The passenger vehicles segment dominated the vehicle type category with a 70.75% revenue share in 2025, led by increasing integration of semiconductor components in passenger cars worldwide

- Internal combustion engine accounted for 60.65% of the market, preferred by the large installed base of conventional vehicles globally

- The electric segment is the fastest-growing propulsion type category, with a CAGR of 15.8%, driven by increasing electric vehicle adoption and rising demand for advanced power semiconductor solutions

Report Scope and Automotive Semiconductor Market Segmentation

|

Attributes |

Automotive Semiconductor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Semiconductor Market Trends

Trend: Rising Adoption of Semiconductor Solutions in Electric Vehicle

The increasing adoption of electric vehicles (EVs) is accelerating demand for advanced automotive semiconductor solutions used in battery management systems, power control modules, inverters, and charging technologies. Semiconductor manufacturers are developing high-performance power devices such as silicon carbide (SiC) and gallium nitride (GaN) components to improve vehicle efficiency, charging speed, and driving range. The transition toward vehicle electrification is also encouraging automotive OEMs to redesign vehicle architectures with greater semiconductor content, enabling enhanced energy management, connectivity, and intelligent mobility functions. For instance, in February 2025, Infineon Technologies announced the rollout of its first silicon carbide (SiC) products based on advanced 200 mm SiC wafer manufacturing technology, supporting high-voltage applications including electric vehicles and renewable energy systems, highlighting the growing role of advanced semiconductors in vehicle electrification and energy efficiency.

The rapid shift toward electric mobility is creating significant growth opportunities for automotive semiconductor providers by increasing demand for advanced power electronics and efficient vehicle architectures.

Automotive Semiconductor Market Dynamics

Key Market Driver: Growing Adoption of ADAS and Autonomous Driving Technologies

The rapid advancement of autonomous vehicles and ADAS technologies is creating substantial demand for automotive semiconductors that enable real-time sensing, processing, connectivity, and decision-making capabilities. Modern vehicles increasingly rely on semiconductor-based solutions, including sensors, microcontrollers, processors, and system-on-chip platforms, to support functions such as automated braking, lane assistance, adaptive cruise control, and autonomous navigation. Automotive OEMs and technology companies are investing heavily in semiconductor-powered computing platforms to manage increasing data requirements generated by cameras, radar, lidar, and vehicle communication systems. For instance, in September 2022, NVIDIA introduced DRIVE Thor, its next-generation centralized automotive computer designed to support automated driving, AI workloads, and intelligent vehicle applications, demonstrating increasing semiconductor demand for autonomous mobility systems.

The expansion of ADAS and autonomous driving technologies remains a major growth driver, increasing semiconductor content per vehicle and accelerating innovation in automotive computing platforms.

Key Restraint/Challenge: Semiconductor Supply Chain Disruptions and Manufacturing Complexity

A significant challenge in the automotive semiconductor market is the complexity of semiconductor manufacturing and vulnerability of global supply chains. Automotive-grade chips require stringent reliability standards, long qualification cycles, and specialized manufacturing processes, making production expansion difficult compared with consumer electronics semiconductors. Supply shortages, geopolitical risks, and limited availability of advanced semiconductor fabrication capacity can affect vehicle production schedules and increase procurement challenges for automotive manufacturers. For instance, in June 2024, the European Union adopted the European Chips Act initiative to strengthen semiconductor manufacturing capacity and reduce dependency on external chip supply chains, reflecting the strategic challenge of securing automotive semiconductor availability.

Supply chain resilience and expansion of semiconductor manufacturing capacity remain critical challenges that will influence the long-term growth and stability of the automotive semiconductor market.

Key Market Opportunity: Development of AI-Powered Automotive Semiconductor Platforms

The integration of artificial intelligence and high-performance computing platforms presents a significant market opportunity for automotive semiconductor manufacturers. AI-enabled semiconductor solutions can process large volumes of vehicle data, enhance autonomous driving capabilities, improve predictive maintenance, and support connected vehicle applications. The increasing deployment of edge computing, automotive processors, and dedicated AI accelerators is creating opportunities for semiconductor companies to develop advanced solutions for next-generation vehicles. For instance, in January 2025, Qualcomm Technologies expanded its Snapdragon Digital Chassis platform with AI-powered automotive solutions, including enhanced Snapdragon Cockpit and Snapdragon Ride platforms, to support connected vehicles, digital cockpits, and advanced driver assistance systems (ADAS), demonstrating the growing opportunity for AI-based automotive semiconductor solutions.

AI-driven automotive semiconductor platforms are expected to become a key growth opportunity by enabling smarter, safer, and more connected vehicles worldwide.

Automotive Semiconductor Market Scope

The automotive semiconductor market is segmented on the basis of component, vehicle type, propulsion type, and application.

- By Component

On the basis of component, the automotive semiconductor market is segmented into processor, discrete power, sensor, memory, and others. The processor segment dominated the automotive semiconductor market with an estimated revenue share of 30.35% in 2025, driven by increasing demand for high-performance computing solutions in modern vehicles. Processors are becoming essential for managing complex automotive applications, including advanced driver assistance systems (ADAS), autonomous driving, digital cockpits, and connected vehicle platforms. The growing volume of data generated by cameras, sensors, and vehicle communication systems is increasing the need for advanced processing capabilities. Automotive manufacturers are shifting toward centralized electronic architectures that require powerful computing platforms. Rising adoption of artificial intelligence and machine learning in vehicles is further supporting processor integration. Continuous advancements in automotive computing technologies are expected to strengthen the segment’s leading position.

The sensor segment is projected to register the fastest growth with an estimated CAGR of 12.4% during the forecast period, supported by increasing adoption of ADAS, autonomous vehicles, and vehicle safety technologies. Sensors such as radar, lidar, cameras, and ultrasonic systems enable real-time vehicle monitoring and automated decision-making. Growing government regulations focused on vehicle safety are encouraging manufacturers to integrate advanced sensing technologies. The increasing development of autonomous driving systems is creating significant demand for semiconductor-based sensors. Rising investments in connected vehicle technologies are further accelerating sensor adoption. Continuous innovation in sensor accuracy, miniaturization, and cost efficiency is expected to drive rapid segment expansion.

- By Vehicle Type

On the basis of vehicle type, the automotive semiconductor market is segmented into passenger vehicle, light commercial vehicle (LCV), and heavy commercial vehicle (HCV). The passenger vehicle segment dominated the automotive semiconductor market with an estimated revenue share of 70.75% in 2025, owing to increasing integration of semiconductor components in passenger cars worldwide. Passenger vehicles are witnessing strong adoption of ADAS, infotainment systems, connectivity solutions, and electronic control units (ECUs). Growing consumer preference for safer, smarter, and connected vehicles is increasing semiconductor content per vehicle. Automotive OEMs are investing significantly in digital vehicle platforms and advanced electronic systems. Rising adoption of electric passenger vehicles is further increasing demand for power semiconductors and battery management solutions. Continuous technological advancements in passenger mobility are expected to maintain the segment’s dominance.

The heavy commercial vehicle (HCV) segment is expected to witness the fastest growth with an estimated CAGR of 9.1% during the forecast period, driven by increasing adoption of automation, fleet management systems, and connected transportation technologies. Heavy commercial vehicles require advanced semiconductor solutions for power management, telematics, safety systems, and operational efficiency. Growing logistics activities and expansion of smart transportation infrastructure are increasing demand for intelligent commercial vehicles. The adoption of electric trucks and buses is further creating opportunities for semiconductor manufacturers. Rising focus on reducing fuel consumption and improving fleet performance is supporting technology integration. Increasing government regulations for commercial vehicle safety are expected to accelerate semiconductor adoption in this segment.

- By Propulsion Type

On the basis of propulsion type, the automotive semiconductor market is segmented into internal combustion engine, electric, and other. The internal combustion engine (ICE) segment dominated the automotive semiconductor market with an estimated revenue share of 60.65% in 2025, supported by the large installed base of conventional vehicles globally. ICE vehicles increasingly incorporate semiconductor components for engine control, emissions management, safety systems, and infotainment applications. The growing use of electronic control units and vehicle automation features is increasing semiconductor demand in traditional vehicles. Automotive manufacturers are adopting advanced electronic technologies to improve fuel efficiency and comply with emission regulations. The continued production of conventional vehicles, particularly in emerging markets, supports segment growth. However, the gradual transition toward electrification is expected to shift future semiconductor demand toward electric propulsion systems.

The electric segment is projected to register the fastest growth with an estimated CAGR of 15.8% during the forecast period, driven by increasing electric vehicle adoption and rising demand for advanced power semiconductor solutions. Electric vehicles require higher semiconductor content for battery management systems, power inverters, charging systems, and electric powertrains. Government initiatives supporting emission reduction and clean transportation are accelerating EV adoption globally. Semiconductor technologies such as silicon carbide (SiC) and gallium nitride (GaN) are gaining importance due to their efficiency and performance benefits. Increasing investments in EV manufacturing facilities are creating new opportunities for semiconductor suppliers. The rapid transition toward vehicle electrification is expected to significantly accelerate segment growth.

- By Application

On the basis of application, the automotive semiconductor market is segmented into chassis, powertrain, safety, telematics & infotainment, and body electronics. The safety segment dominated the automotive semiconductor market with an estimated revenue share of 25.30% in 2025, driven by increasing adoption of advanced driver assistance systems (ADAS) and vehicle safety technologies. Semiconductor components enable critical safety functions, including collision avoidance, automated emergency braking, lane assistance, and adaptive cruise control. Rising regulatory requirements for vehicle safety are encouraging manufacturers to integrate advanced semiconductor-enabled systems. Automotive OEMs are increasingly investing in sensor-based safety platforms to support autonomous driving development. Growing consumer demand for safer vehicles is further increasing adoption of safety electronics. The expansion of autonomous vehicle technologies continues to strengthen semiconductor demand within safety applications.

The telematics & infotainment segment is projected to register the fastest growth with an estimated CAGR of 12.5% during the forecast period, supported by rising demand for connected vehicles, digital cockpits, and advanced communication systems. Modern vehicles increasingly depend on semiconductor solutions for navigation, entertainment, connectivity, and cloud-based services. The expansion of 5G connectivity and Internet of Things (IoT) technologies is accelerating development of intelligent vehicle platforms. Consumer demand for enhanced digital experiences is encouraging automotive manufacturers to integrate advanced infotainment solutions. Increasing adoption of connected mobility services is creating new opportunities for semiconductor companies. The growing shift toward software-defined vehicles is expected to further accelerate segment growth.

Automotive Semiconductor Market Regional Analysis

Asia-Pacific dominated the automotive semiconductor market with a revenue share of 45.2% in 2025, supported by the presence of major automotive manufacturing hubs, increasing vehicle production, rising adoption of electric vehicles, and strong demand for advanced automotive electronic components across the region. The region also benefits from rapid deployment of advanced driver assistance systems (ADAS), connected vehicle technologies, and intelligent mobility solutions across China, Japan, South Korea, and India. Growing investments in electric vehicle manufacturing, semiconductor fabrication facilities, and automotive technology development are accelerating market expansion. Increasing demand for vehicle electrification, autonomous driving platforms, and high-performance computing solutions continues to strengthen Asia-Pacific’s leading position in the global automotive semiconductor market.

U.S. Automotive Semiconductor Market Insight

The U.S. automotive semiconductor market is witnessing strong growth due to rising investments in electric vehicles, advanced driver assistance systems (ADAS), autonomous driving technologies, and connected vehicle platforms. The country’s strong automotive technology ecosystem, along with increasing adoption of artificial intelligence-powered vehicle computing systems and semiconductor innovations, is driving demand across passenger vehicles, commercial vehicles, and mobility applications. In addition, growing investments in domestic semiconductor manufacturing and supply chain development are accelerating market expansion. In December 2024, the U.S. Department of Commerce announced multiple CHIPS Act incentive awards, including up to USD 7.865 billion for Intel and up to USD 6.6 billion for TSMC, to expand domestic semiconductor manufacturing capacity and strengthen the U.S. semiconductor supply chain supporting advanced technologies, including automotive applications.

Europe Automotive Semiconductor Market Insight

The Europe automotive semiconductor market is expected to witness fastest growing, driven by strong automotive manufacturing capabilities, increasing electric vehicle adoption, and rising demand for ADAS and vehicle electrification technologies. The region benefits from established automotive OEMs, semiconductor companies, and government initiatives focused on strengthening semiconductor supply chains. Increasing investments in automotive chips, power semiconductors, and intelligent mobility solutions are supporting regional growth. The European Union continued implementation of the European Chips Act to mobilize more than EUR 43 billion in public and private investments to strengthen semiconductor manufacturing and reduce supply chain dependency.

U.K. Automotive Semiconductor Market Insight

The U.K. automotive semiconductor market is experiencing steady growth, supported by increasing adoption of electric vehicles, automotive electronics, and semiconductor-based mobility solutions. The country’s strong automotive research ecosystem and focus on vehicle electrification are encouraging demand for advanced chips used in power management, connectivity, and autonomous driving applications. Increasing collaboration between automotive manufacturers and technology companies is further supporting semiconductor innovation. In May 2024, the U.K. Government announced the allocation of approximately USD 127 million in the first phase of its National Semiconductor Strategy to support semiconductor research, innovation, and supply chain development, strengthening the country’s semiconductor ecosystem for advanced technologies including automotive applications.

Germany Automotive Semiconductor Market Insight

The Germany automotive semiconductor market is expanding steadily due to the country’s strong automotive manufacturing base, advanced engineering capabilities, and increasing adoption of electric and autonomous vehicle technologies. Automotive manufacturers and semiconductor suppliers are investing in advanced chip solutions for ADAS, power electronics, and connected vehicle systems. The country’s focus on vehicle electrification and digital mobility is further accelerating semiconductor integration. Infineon Technologies opened its new semiconductor fabrication facility in Dresden, Germany, strengthening production capacity for automotive and industrial semiconductor applications.

Japan Automotive Semiconductor Market Insight

The Japan automotive semiconductor market is witnessing consistent growth due to rising investments in vehicle electrification, autonomous driving technologies, and advanced automotive electronics. The country’s strong automotive manufacturing ecosystem and semiconductor expertise are supporting development of high-performance chips for safety, power management, and vehicle computing applications. Increasing collaboration between automotive OEMs and semiconductor manufacturers is further strengthening market expansion. In November 2024, Renesas Electronics introduced its fifth-generation R-Car automotive system-on-chip (SoC) platform, designed to support software-defined vehicles, advanced driver assistance systems (ADAS), in-vehicle infotainment (IVI), and centralized vehicle computing architectures, demonstrating the increasing demand for advanced automotive semiconductor solutions.

China Automotive Semiconductor Market Insight

The China automotive semiconductor market is growing rapidly, driven by increasing electric vehicle production, expanding automotive electronics demand, and government initiatives supporting semiconductor development. The country’s large automotive manufacturing base and leadership in EV production are significantly increasing demand for power semiconductors, sensors, processors, and vehicle connectivity solutions. Growing investments in domestic semiconductor capabilities are further supporting market development. In January 2025, the China Association of Automobile Manufacturers (CAAM) reported that China’s new energy vehicle (NEV) production reached 12.888 million units in 2024, increasing demand for semiconductor components used in electric powertrains, battery management systems, power electronics, and intelligent driving technologies.

Automotive Semiconductor Market Share

The automotive semiconductor industry is primarily led by well-established companies, including:

- NVIDIA Corporation (U.S.)

- Qualcomm Technologies, Inc. (U.S.)

- Intel Corporation (U.S.)

- Advanced Micro Devices, Inc. (U.S.)

- Texas Instruments Incorporated (U.S.)

- NXP Semiconductors (Netherlands)

- Infineon Technologies AG (Germany)

- STMicroelectronics (Switzerland)

- Renesas Electronics Corporation (Japan)

- ROHM Co., Ltd. (Japan)

- Semiconductor Components Industries, LLC (U.S.)

- Analog Devices, Inc. (U.S.)

- Microchip Technology Inc (U.S.)

- Broadcom Inc. (U.S.)

- Marvell Technology, Inc. (U.S.)

- Monolithic Power Systems, Inc. (U.S.)

- MediaTek (Taiwan)

- TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION (Japan)

- Mitsubishi Electric Corporation (Japan)

- Vishay Intertechnology, Inc. (U.S.)

Latest Developments in Automotive Semiconductor Market

- In October 2025, Infineon Technologies introduced its CoolGaN Automotive Transistor 100 V G1 family, the company’s first automotive-qualified gallium nitride (GaN) transistor solutions designed for automotive applications. The new products support applications such as DC-DC converters, auxiliary systems, infotainment, and future electric vehicle power architectures. This launch demonstrates the increasing adoption of advanced power semiconductor technologies to improve efficiency and performance in electric and software-defined vehicles

- In March 2025, Infineon Technologies announced its new automotive microcontroller family based on RISC-V architecture, expanding its AURIX™ automotive MCU portfolio to support software-defined vehicles, advanced driver assistance systems (ADAS), and future automotive computing requirements. The new RISC-V-based microcontrollers are designed to improve scalability, flexibility, and real-time processing capabilities for next-generation vehicle architectures. This launch highlights the increasing demand for advanced automotive semiconductor solutions supporting vehicle digitalization and electrification

- In March 2025, Renesas Electronics launched the DA14533, its first automotive-qualified Bluetooth Low Energy (BLE) system-on-chip (SoC), designed for applications including tire pressure monitoring systems, keyless entry, wireless sensors, and battery management systems. The new automotive BLE SoC integrates a radio transceiver, Arm Cortex-M0+ microcontroller, memory, peripherals, and security features in a compact design. This product launch demonstrates the growing role of connectivity semiconductors in connected and intelligent vehicle ecosystems

- In November 2024, Renesas Electronics introduced the R-Car X5H, a fifth-generation automotive system-on-chip (SoC) built using 3-nanometer process technology, designed for centralized vehicle computing, ADAS, in-vehicle infotainment (IVI), and gateway applications. The new SoC combines multiple automotive domains into a single high-performance computing platform, supporting the transition toward software-defined vehicles. This launch reflects increasing demand for advanced processors capable of handling artificial intelligence, autonomous driving, and connected vehicle workloads

- In January 2023, Qualcomm Technologies launched the Snapdragon Ride Flex System-on-Chip (SoC) platform, designed to simultaneously support digital cockpit systems, advanced driver assistance systems (ADAS), and automated driving functions on a single automotive computing architecture. The new SoC integrates mixed-criticality computing capabilities, enabling automakers and Tier-1 suppliers to develop centralized vehicle platforms and software-defined vehicle architectures

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.