Global Automotive Tempered Glass Market

Market Size in USD Billion

USD

20.79 Billion

USD

30.25 Billion

2025

2033

USD

20.79 Billion

USD

30.25 Billion

2025

2033

| 2026 - 2033 | |

| USD 20.79 Billion | |

| USD 30.25 Billion | |

| % | |

|

Automotive Tempered Glass Market Overview

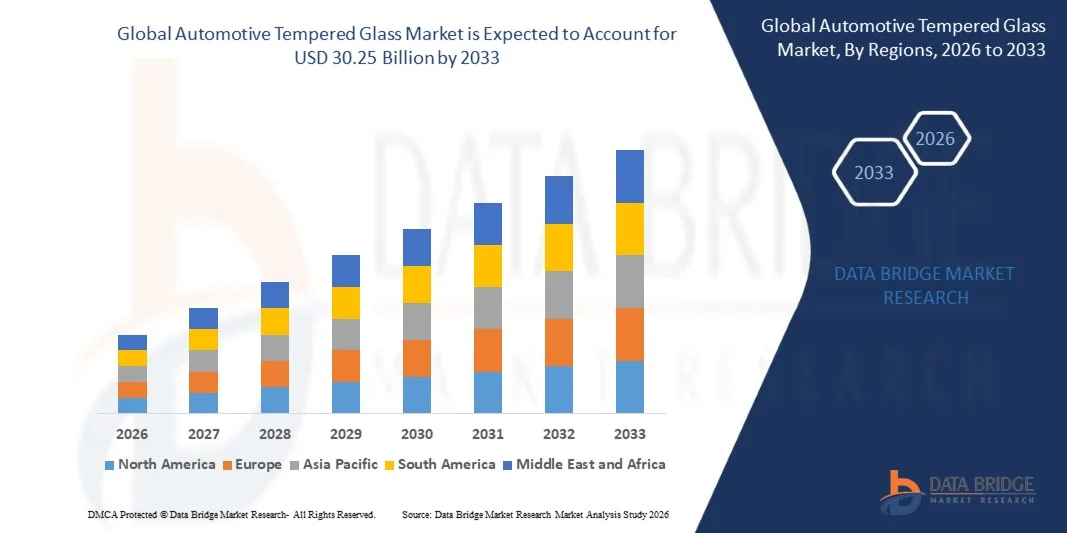

The Automotive Tempered Glass Market was valued at USD 20.79 billion in 2025 and is projected to reach USD 30.25 billion by 2033, growing at a CAGR of 4.80% from 2026 to 2033 The Automotive Tempered Glass Market is experiencing steady growth driven by increasing vehicle production, rising consumer demand for enhanced safety features, and stringent automotive safety regulations worldwide. Tempered glass is widely used in side windows, rear windows, and sunroofs due to its superior strength, impact resistance, and ability to shatter into small, less harmful fragments, significantly improving passenger safety. The growing adoption of premium and luxury vehicles, coupled with increasing integration of panoramic sunroofs and advanced glazing solutions, is further accelerating market expansion. In addition, rapid advancements in glass manufacturing technologies, including lightweight and high-durability tempered glass products, are supporting automakers’ efforts to improve fuel efficiency and vehicle performance. The rising popularity of electric vehicles (EVs), which require lightweight materials to maximize battery efficiency and driving range, is creating new growth opportunities for tempered glass manufacturers. Furthermore, increasing urbanization, higher disposable incomes, and expanding automotive production in emerging economies are strengthening demand across both passenger and commercial vehicle segments. Continuous investments in automotive safety innovations and sustainable manufacturing processes are also contributing to the long-term growth of the automotive tempered glass market globally.

Key Market Trends & Insights

- North America dominated the Automotive Tempered Glass Market with the largest revenue share of 35.72% in 2025, supported by strong automotive production, high adoption of advanced vehicle safety technologies, increasing demand for premium vehicles, and the presence of leading automotive OEMs and glass manufacturers across the region.

- The Passive Glass segment dominated the market with a share of 71.84% in 2025 due to its widespread adoption across passenger and commercial vehicles, cost-effectiveness, durability, and compliance with global automotive safety regulations.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 6.9% from 2026 to 2033, fueled by rising vehicle ownership, rapid expansion of automotive manufacturing facilities, growing electric vehicle production, and increasing demand for advanced glazing solutions across China, India, and Southeast Asia.

- The Active Smart Glass segment is the fastest-growing technology category, projected to register a CAGR of 8.1%, reflecting growing demand for intelligent glazing systems that enhance passenger comfort, privacy control, solar heat management, and energy efficiency.

- The Passenger Car segment dominates the vehicle type category with a 67.28% revenue share in 2025, supported by large-scale passenger vehicle production, rising consumer awareness regarding vehicle safety, and increasing incorporation of premium glass features.

- The Windshield segment accounts for 34.91% of the market in 2025, driven by mandatory safety requirements, continuous replacement demand, and extensive utilization of high-strength tempered glass for improved visibility and occupant protection.

- The IR PVB segment dominates the material type category with a 42.37% market share in 2025, driven by increasing demand for heat-reducing and UV-blocking glass solutions that improve cabin comfort and vehicle energy efficiency.

- The Active Smart Glass material category is expected to witness the fastest growth, recording a CAGR of 8.4% during the forecast period, supported by technological advancements in electrochromic and switchable glass technologies, growing luxury vehicle sales, and rising adoption of smart mobility solutions.

Market Size & Forecast

- Global Market Value (2025): USD 20.79 Billion

- Expected Market Value (2033): USD 30.25 Billion

- Forecast CAGR (2026–2033): 4.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Automotive Tempered Glass Market Segmentation

|

Attributes |

Automotive Tempered Glass Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Saint-Gobain S.A. (France) |

|

Market Opportunities |

· Growing Adoption of Electric Vehicles (EVs) · Rising Demand for Smart and Advanced Glazing Technologies · Expansion of Automotive Production in Emerging Economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Automotive Tempered Glass Market Trends

Trend: Rising Adoption of Smart and Energy-Efficient Automotive Glazing Solutions

Automotive manufacturers are increasingly incorporating advanced tempered glass solutions with solar control, UV protection, acoustic insulation, and smart tinting capabilities to enhance vehicle comfort, safety, and energy efficiency. The growing popularity of panoramic sunroofs, large window surfaces, and premium vehicle designs is accelerating demand for high-performance tempered glass products. In addition, the emergence of smart glass technologies that can dynamically regulate light transmission is gaining traction among luxury and electric vehicle manufacturers. As consumers increasingly prioritize comfort, aesthetics, and sustainability, automakers are investing in next-generation glazing technologies that improve cabin experience while supporting vehicle lightweighting initiatives.

Automotive Tempered Glass Market Dynamics

Key Market Driver: Growing Demand for Vehicle Safety and Regulatory Compliance

The increasing emphasis on passenger safety and stringent automotive safety regulations worldwide are major drivers of the automotive tempered glass market. Tempered glass offers superior impact resistance and shatters into small, less harmful fragments upon breakage, significantly reducing the risk of injury during accidents. Regulatory authorities across North America and Europe continue to enforce strict vehicle safety standards, encouraging automakers to adopt high-quality tempered glass solutions. North America accounted for the largest market share of 35.72% in 2025, supported by strong automotive production, widespread adoption of advanced safety technologies, and the presence of leading automotive OEMs and glass manufacturers. The growing integration of ADAS-equipped vehicles and premium automotive features is further strengthening demand for advanced tempered glass products.

Key Restraint/Challenge: Volatility in Raw Material and Energy Costs

A significant challenge facing the Automotive Tempered Glass Market is the fluctuation in raw material and energy prices. The manufacturing process for tempered glass requires high-quality silica, specialized coatings, and energy-intensive heating and cooling operations. Rising electricity and natural gas costs, coupled with supply chain disruptions affecting raw material availability, can increase production expenses and pressure manufacturer profit margins. Furthermore, compliance with environmental regulations and sustainability requirements necessitates additional investments in cleaner production technologies, creating operational challenges for manufacturers, particularly in cost-sensitive markets.

Key Market Opportunity: Expansion of Electric Vehicles and Advanced Glazing Technologies

The rapid growth of the electric vehicle (EV) industry presents a substantial opportunity for automotive tempered glass manufacturers. EV producers increasingly require lightweight and thermally efficient glazing solutions to improve battery performance and vehicle range. Advanced tempered glass products featuring infrared-reflective interlayers, solar control coatings, and smart glass functionality are gaining popularity among EV and premium vehicle manufacturers. Asia-Pacific is projected to be the fastest-growing regional market, registering a CAGR of 6.9% from 2026 to 2033, driven by expanding automotive production, rising EV adoption, and increasing investments in advanced vehicle technologies across China, India, Japan, and Southeast Asia. These trends are expected to create significant growth opportunities for innovative tempered glass suppliers over the forecast period.

Automotive Tempered Glass Market Scope

The Automotive Tempered Glass market is segmented on the basis of technology, vehicle type, application, and material type

- By Technology

On the basis of technology, the Automotive Tempered Glass Market is segmented into Active Smart Glass and Passive Glass. The Passive Glass segment dominated the market with a share of 71.84% in 2025 due to its widespread adoption across passenger and commercial vehicles, cost-effectiveness, durability, and compliance with global automotive safety regulations. Passive tempered glass remains the industry standard for side windows, rear windows, and other glazing applications because it offers excellent impact resistance and occupant protection at a competitive cost. Automotive OEMs continue to prefer passive glass for mass-market vehicles owing to its proven reliability, ease of manufacturing, and compatibility with existing vehicle platforms. Rising vehicle production volumes globally, particularly in emerging economies, are further supporting segment growth. In addition, stringent safety standards and increasing consumer awareness regarding vehicle safety continue to drive adoption, reinforcing the dominant position of the passive glass segment in the global market.

The Active Smart Glass segment is expected to witness the fastest CAGR of 8.1% from 2026 to 2033, driven by increasing demand for premium vehicle features, enhanced passenger comfort, and energy-efficient glazing technologies. Active smart glass enables dynamic control of light transmission, glare reduction, heat management, and privacy functions. Luxury vehicle manufacturers and electric vehicle producers are increasingly integrating electrochromic and switchable glass technologies into sunroofs and side windows. Furthermore, advancements in smart glazing materials and declining technology costs are accelerating commercialization. Growing consumer preference for connected and intelligent vehicles is also creating strong demand for active smart glass solutions across developed and emerging automotive markets.

- By Vehicle Type

On the basis of vehicle type, the Automotive Tempered Glass Market is segmented into Passenger Car, Light Commercial Vehicle (LCV), Truck, and Bus. The Passenger Car segment dominated the market with a share of 67.28% in 2025 due to high global passenger vehicle production and growing consumer demand for enhanced safety, comfort, and aesthetics. Passenger cars utilize tempered glass extensively in side windows, rear windows, and sunroof applications. Increasing adoption of panoramic roofs, advanced glazing technologies, and premium vehicle features is further driving segment growth. Rising disposable incomes, urbanization, and vehicle ownership rates across emerging economies are also supporting demand. In addition, strong production activity among major automotive OEMs and increasing electric vehicle sales are reinforcing the leading position of the passenger car segment in the market.

The Light Commercial Vehicle (LCV) segment is expected to witness the fastest CAGR of 7.2% from 2026 to 2033, driven by rapid growth in e-commerce, logistics, and last-mile delivery services worldwide. Fleet operators are increasingly investing in modern LCVs equipped with advanced safety and comfort features. Rising demand for lightweight and durable tempered glass solutions to improve fuel efficiency and vehicle performance is supporting market expansion. Growing urban freight transportation and expanding commercial vehicle production in Asia-Pacific are further accelerating segment growth during the forecast period.

- By Application

On the basis of application, the Automotive Tempered Glass Market is segmented into Windshield, Sidelite, Backlite, Rear Quarter Glass, Sideview Mirror, and Rearview Mirror. The Windshield segment dominated the market with a share of 34.91% in 2025 due to its critical role in vehicle safety, structural integrity, and driver visibility. Windshields represent one of the largest glass components in vehicles and require advanced glazing technologies to meet safety and performance requirements. Increasing integration of ADAS sensors, cameras, and heads-up display systems within windshield structures is driving demand for high-performance automotive glass solutions. Growing vehicle production and replacement demand in aftermarket channels are also contributing to segment dominance. Furthermore, regulatory requirements related to occupant safety continue to support strong adoption across all vehicle categories.

The Rear Quarter Glass segment is projected to register the fastest CAGR of 7.0% from 2026 to 2033, driven by increasing popularity of premium vehicle designs, panoramic glass configurations, and modern vehicle aesthetics. Automotive manufacturers are increasingly incorporating larger glass surfaces to enhance cabin appearance and passenger experience. Rising demand for electric vehicles and luxury vehicles is further accelerating adoption of advanced rear quarter glass solutions globally.

- By Material Type

On the basis of material type, the Automotive Tempered Glass Market is segmented into IR PVB, Metal Coated Glass, Tinted Glass, and Others. The IR PVB segment dominated the market with a share of 42.37% in 2025 due to its superior heat-insulation properties, UV protection capabilities, and ability to improve passenger comfort. IR PVB interlayers help reduce solar heat gain inside vehicle cabins, lowering air-conditioning requirements and improving energy efficiency. This is particularly important in electric vehicles where thermal management directly impacts battery performance and driving range. Growing demand for fuel-efficient vehicles and increasing consumer preference for enhanced cabin comfort are driving widespread adoption. Furthermore, automotive OEMs are increasingly utilizing IR PVB materials to meet environmental regulations and sustainability goals, strengthening the segment's leadership position.

The Metal Coated Glass segment is expected to witness the fastest CAGR of 7.4% from 2026 to 2033, driven by increasing demand for advanced solar-control glazing and energy-efficient vehicle solutions. Metal-coated glass offers enhanced thermal insulation, glare reduction, and infrared reflection properties that improve cabin comfort and vehicle efficiency. The growing adoption of premium vehicles, electric vehicles, and smart glazing technologies is accelerating demand. In addition, continuous advancements in coating technologies and rising investments in next-generation automotive glass solutions are expected to support strong growth throughout the forecast period.

Automotive Tempered Glass Market Regional Analysis

North America dominated the Automotive Tempered Glass market and accounted for the largest revenue share of 35.72% in 2025, supported by strong automotive production, high adoption of advanced vehicle safety technologies, increasing demand for premium and luxury vehicles, and the presence of leading automotive OEMs and glass manufacturers across the region. The market also benefits from stringent vehicle safety regulations, growing integration of ADAS technologies, and rising consumer preference for enhanced comfort and energy-efficient glazing solutions. Increasing adoption of panoramic sunroofs, smart glass technologies, and lightweight automotive materials is further strengthening regional demand. Continuous investments in electric vehicle manufacturing and advanced automotive technologies continue to reinforce North America's leadership position in the Automotive Tempered Glass Market.

U.S. Automotive Tempered Glass Market Insight

The U.S. Automotive Tempered Glass market is witnessing strong growth due to rising vehicle production, increasing consumer demand for safety-enhanced vehicles, and growing adoption of advanced glazing technologies. The country's well-established automotive industry, coupled with strong investments in electric vehicle development and autonomous driving technologies, is driving demand for high-performance tempered glass solutions. In addition, increasing integration of infrared-reflective glass, panoramic roofs, and smart glazing systems is supporting market expansion. Growing emphasis on fuel efficiency, passenger comfort, and regulatory compliance continues to accelerate adoption among automotive manufacturers operating in the U.S.

Europe Automotive Tempered Glass Market Insight

The Europe Automotive Tempered Glass market remains a significant contributor to global revenue, driven by the presence of leading luxury vehicle manufacturers, stringent automotive safety standards, and increasing demand for sustainable mobility solutions. Growing adoption of advanced glazing materials, lightweight vehicle components, and smart glass technologies is supporting market growth across the region. Furthermore, increasing production of premium vehicles and electric vehicles is creating additional opportunities for tempered glass manufacturers. Continuous technological advancements and strong investments in automotive innovation continue to support market expansion throughout Europe.

U.K. Automotive Tempered Glass Market Insight

The U.K. Automotive Tempered Glass market is experiencing steady growth, supported by rising demand for premium automobiles, increasing electric vehicle adoption, and growing investments in automotive innovation. Automotive manufacturers are increasingly utilizing advanced tempered glass solutions to improve vehicle safety, energy efficiency, and passenger comfort. The growing popularity of panoramic roofs, acoustic glass systems, and solar-control glazing technologies is further contributing to market growth. In addition, supportive government initiatives promoting sustainable transportation are encouraging greater adoption of advanced automotive glass products.

Germany Automotive Tempered Glass Market Insight

The Germany Automotive Tempered Glass market is expanding steadily due to the country's strong automotive manufacturing base and leadership in automotive engineering and innovation. Major automotive OEMs are increasingly adopting advanced tempered glass solutions to enhance vehicle performance, safety, and aesthetics. Rising investments in electric vehicle production, smart mobility solutions, and lightweight vehicle technologies are driving market demand. Furthermore, stringent environmental regulations and increasing focus on vehicle efficiency continue to accelerate the adoption of technologically advanced automotive glazing systems across Germany.

Asia-Pacific Automotive Tempered Glass Market Insight

The Asia-Pacific Automotive Tempered Glass market is expected to witness the fastest growth, registering a CAGR of 6.9% from 2026 to 2033, driven by rising vehicle ownership, rapid expansion of automotive manufacturing facilities, growing electric vehicle production, and increasing demand for advanced glazing solutions across China, India, Japan, and Southeast Asia. The region benefits from a strong automotive supply chain, rising disposable incomes, and increasing investments by global automakers. Growing awareness regarding vehicle safety, comfort, and energy efficiency is further supporting demand for high-quality tempered glass products. In addition, expanding production of passenger vehicles and electric vehicles is accelerating market growth throughout the region.

Japan Automotive Tempered Glass Market Insight

The Japan Automotive Tempered Glass market is witnessing consistent growth due to strong automotive production capabilities, continuous technological innovation, and increasing adoption of advanced vehicle safety features. Japanese automakers are increasingly incorporating high-performance tempered glass and smart glazing technologies into next-generation vehicles. Rising demand for electric and hybrid vehicles, coupled with a focus on energy efficiency and passenger comfort, is further driving market expansion. Moreover, advancements in automotive glass coatings and lightweight materials continue to support industry growth.

China Automotive Tempered Glass Market Insight

The China Automotive Tempered Glass market is growing rapidly, driven by expanding automotive production, rising electric vehicle sales, and increasing investments in advanced vehicle technologies. As the world's largest automotive manufacturing hub, China is witnessing substantial demand for tempered glass across passenger cars, commercial vehicles, and electric vehicles. Growing consumer preference for premium vehicle features, increasing adoption of panoramic sunroofs, and rising implementation of vehicle safety regulations are significantly boosting market demand. Furthermore, continuous investments in automotive R&D and smart mobility solutions are positioning China as one of the fastest-growing markets for Automotive Tempered Glass globally.

Automotive Tempered Glass Market Share

The Automotive Tempered Glass industry is primarily led by well-established companies, including:

- Saint-Gobain S.A. (France)

- AGC Inc. (Japan)

- Nippon Sheet Glass Co., Ltd. (NSG Group) (Japan)

- Fuyao Glass Industry Group Co., Ltd. (China)

- Xinyi Glass Holdings Limited (China)

- Central Glass Co., Ltd. (Japan)

- Guardian Glass (U.S.)

- Vitro, S.A.B. de C.V. (Mexico)

- Webasto SE (Germany)

- Corning Incorporated (U.S.)

- Gentex Corporation (U.S.)

- Magna International Inc. (Canada)

- Asahi India Glass Limited (AIS) (India)

- Sisecam Automotive (Turkey)

- Taiwan Glass Industry Corporation (Taiwan)

- PGW Auto Glass (U.S.)

- Carlex Glass America, LLC (U.S.)

- XYG North America (U.S.)

- Benson Auto Glass (China)

- Shatterprufe (Pty) Ltd. (South Africa)

- Glavista Autoglas GmbH (Germany)

- Saint-Gobain Sekurit (France)

- AGP eGlass (Peru)

- Guardian Automotive Products (U.S.)

- Pilkington Automotive (United Kingdom)

- NordGlass (Poland)

- KRD Sicherheitstechnik GmbH (Germany)

- Ficosa International S.A. (Spain)

- Samvardhana Motherson Group (India)

- Glas Trösch Group (Switzerland)

- Yachiyo Industry Co., Ltd. (Japan)

- Minda Corporation Limited (India)

- China Glass Holdings Limited (China)

Latest Developments in Automotive Tempered Glass Market

- In February 2022, Saint-Gobain announced the rebranding of its automotive glass replacement business Autover to Sekurit Service. The initiative included a new digital platform offering online ordering, product identification tools, training resources, and logistics support for automotive glazing professionals. The development strengthened Saint-Gobain’s position in the automotive glass value chain while enhancing customer service and aftermarket capabilities

- In December 2023, AGC Inc. announced the showcase of more than 20 next-generation automotive glass solutions at CES 2024. The company introduced advanced glazing technologies focused on connectivity, sensor integration, passenger comfort, and autonomous mobility applications. The innovations included integrated 5G glass antennas, LiDAR-compatible roof glass, and advanced display-integrated glazing systems, highlighting the increasing role of automotive glass in connected and autonomous vehicles

- In January 2024, Pulsaart by AGC unveiled its Connected Glass Roof at CES 2024. The solution integrates high-performance antennas for 5G, UWB, WLAN, and other connectivity functions directly into the vehicle glass roof structure. The innovation eliminates the need for traditional external antennas while improving vehicle connectivity, aerodynamics, and design flexibility, representing a significant advancement in smart automotive glazing technology

- In July 2024, Fuyao Glass Industry Group confirmed the continued operation of its major automotive glass manufacturing facility in Ohio following a federal investigation involving a third-party labor services company. The company stated that Fuyao Glass America was not the target of the investigation and that production and customer deliveries continued with minimal disruption. The development highlighted the strategic importance of North American automotive glass manufacturing capacity in global vehicle supply chains

- In November 2024, reports emerged that Saint-Gobain was evaluating strategic options for its Sekurit automotive glazing business. The potential review of the automotive glass division reflected increasing industry focus on portfolio optimization and the growing value of automotive glazing technologies amid rising demand for advanced, safety-oriented, and smart glass solutions in modern vehicles

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.